原创 | Odaily星球日报

作者|Azuma

原标题|为什么说Raydium才是Letsbonk.fun崛起的最大受益者?

Letsbonk.fun 近期已在数据层面完成了对赛道“老大哥” Pump.fun 的逆袭。

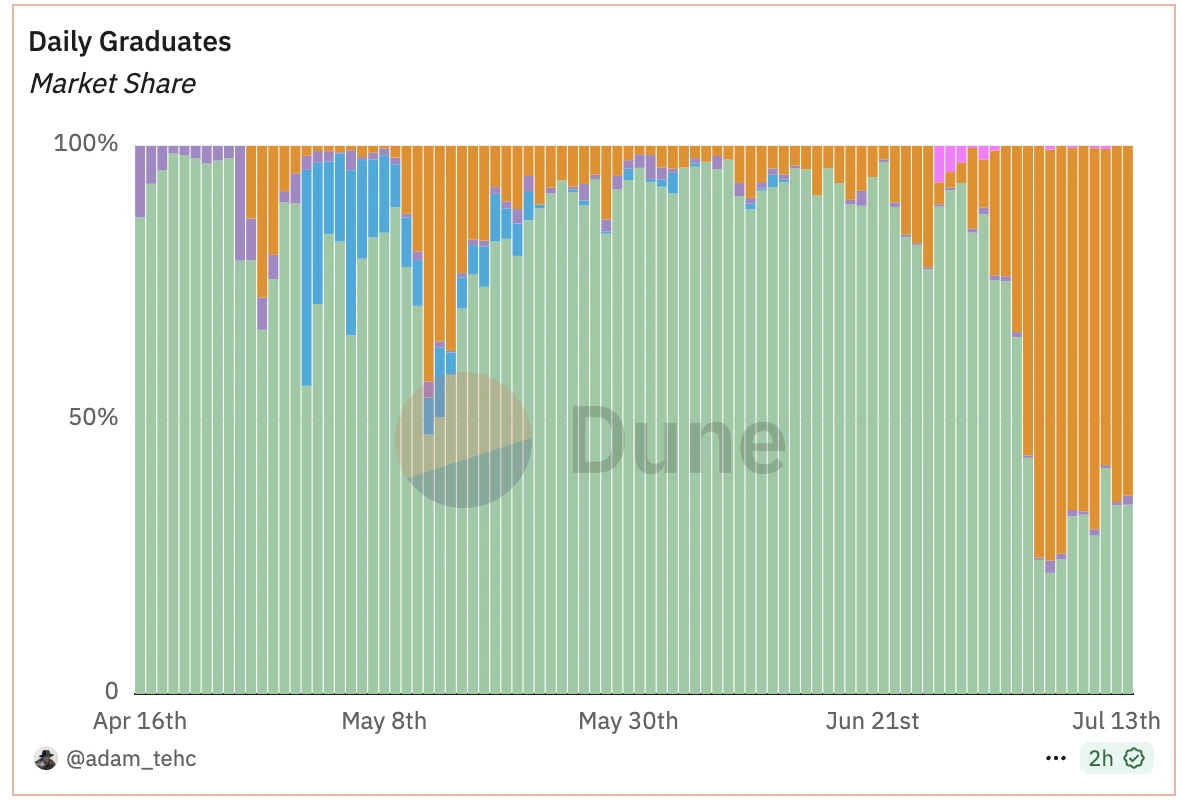

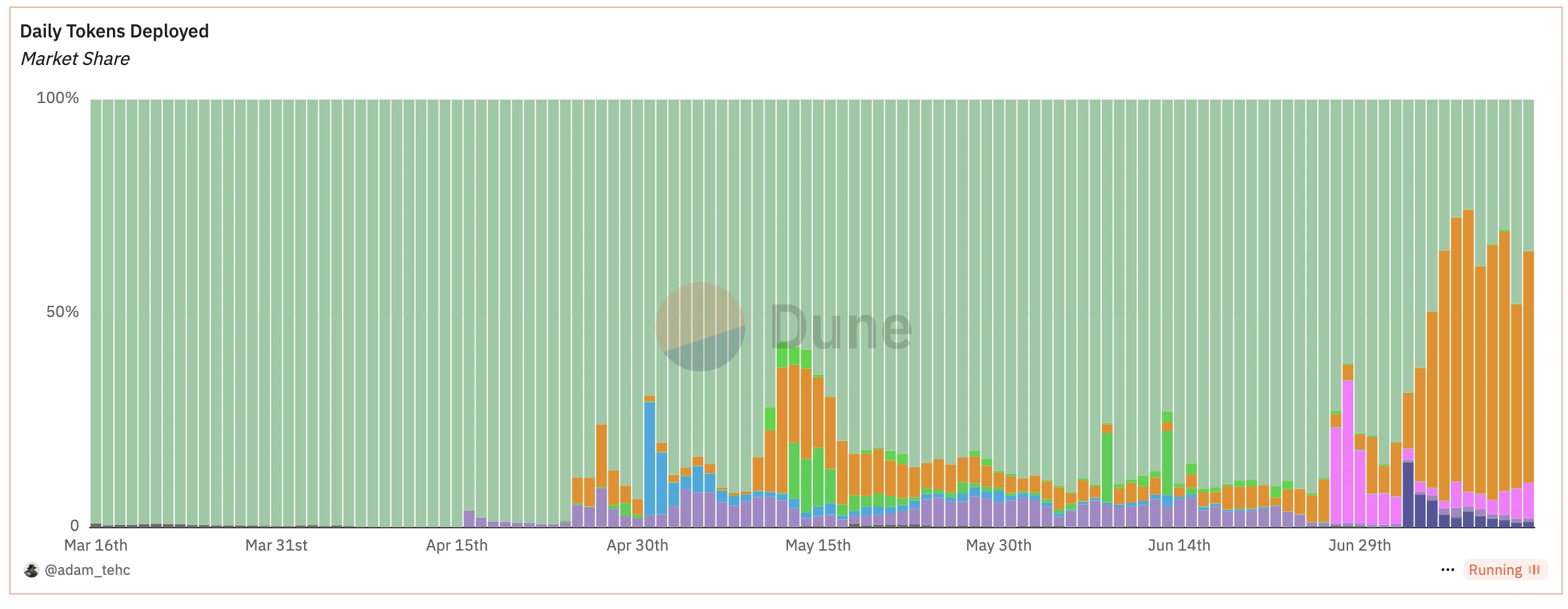

链上分析师 Adam 于 Dune 上所编绘的数据面板显示,近期 Letsbonk.fun(下图中橙色部分)在每日部署代币及每日毕业代币两项核心数据上均已反超 Pump.fun(下图中绿色部分),成为了当下市场上最受欢迎的 Meme 代币启动平台。

随着 Letsbonk.fun 强势崛起,越来越多的人已开始尝试在该平台之上寻找潜在的财富密码,但许多人却忽视了 Letsbonk.fun 数据暴涨后的另一大赢家 —— Raydium。

为什么说 Letsbonk.fun 的崛起会利好 Raydium?故事还要从 Pump.fun 和 Raydium 的恩怨说起。

Pump.fun 的反水,Raydium 的反击

简单概述下,在 Pump.fun 的早期设计中,代币发行需经过“内盘”、“外盘”两个阶段 —— 代币发行后将先进入“内盘”交易阶段,该依赖于 pump.fun 协议自身的 Bonding Curve 进行撮合,待交易量达到 69000 美元时则会进入“外盘”交易阶段,届时流动性将迁移至 Raydium,在该 DEX 上建池并继续开放交易。

然而,Pump.fun 于 3 月 21 日宣布推出自建 AMM DEX 产品 PumpSwap,自此之后 Pump.fun 代币在进入“外盘”时流动性将不再迁移至 Raydium,而是会导向 PumpSwap —— 此举直接截断了 Pump.fun 向 Raydium 的导流路径,进而削减后者的交易量及费用收入。

作为回应,Raydium 于 4 月 16 日宣布已正式推出代币发行平台 LaunchLab,允许用户通过该平台快速发行代币,并在代币流动性达到一定规模(85 SOL)后自动迁移至 Raydium AMM。显然,这是 Raydium 对来势汹汹的 Pump.fun 的直接反击。

那这和 Letsbonk.fun 又有什么关系呢?

价值流向:Letsbonk.fun 、LaunchLab 、 Raydium

虽然 LaunchLab 在代币发行功能方面与 Pump.fun 大同小异,但其最大的特点却不在发行环节本身 —— LaunchLab 的架构支持第三方集成,这使得外部团队和平台能够在 LaunchLab 生态系统内创建和管理自己的启动环境。换句话说,也就是第三方可以依赖于 LaunchLab 的底层技术与 Raydium 的流动性池,推出独立的代币启动前端。

而本文的主角 Letsbonk.fun 正是 BONK 团队基于 LaunchLab 构架所开发的第三方启动平台。

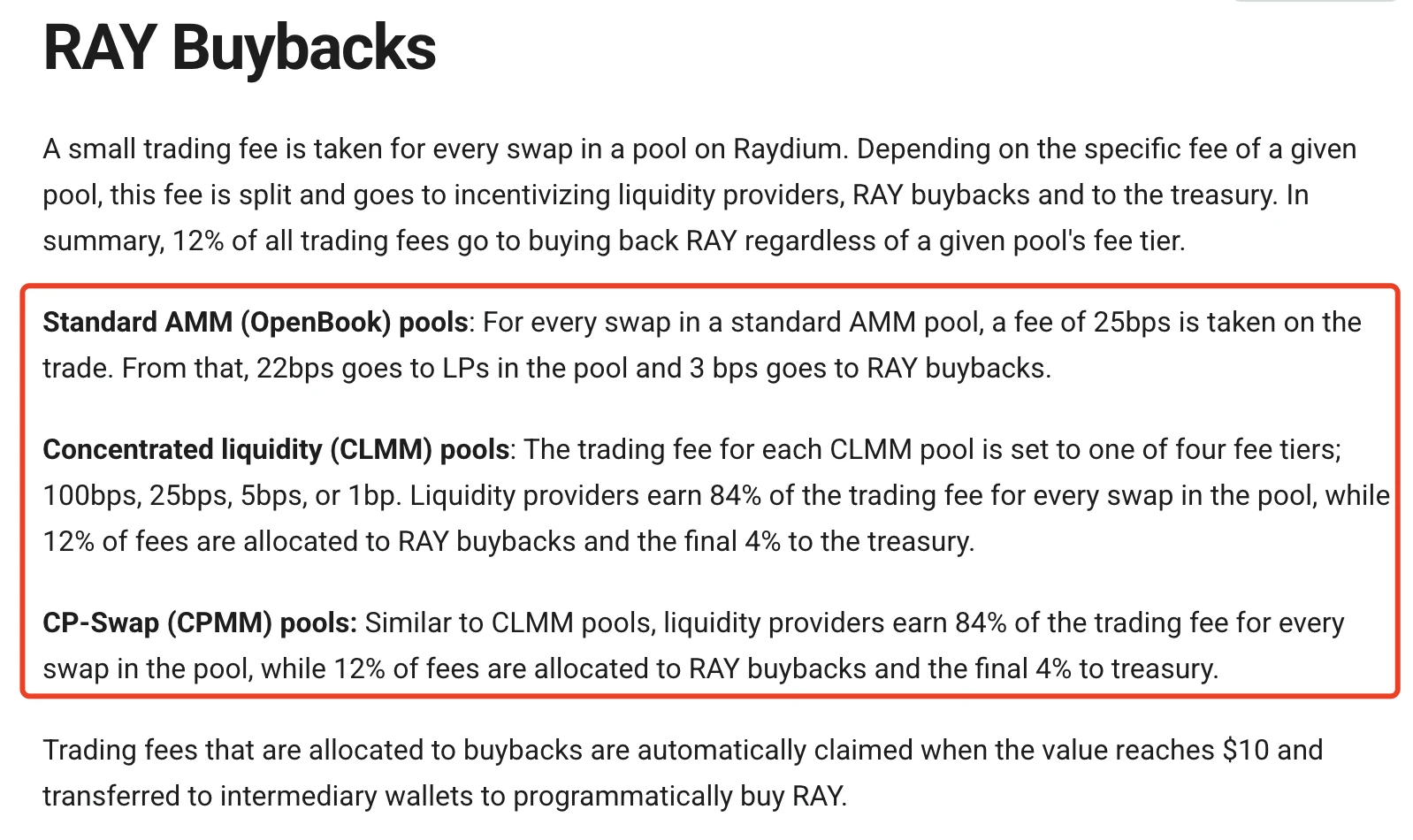

作为基于 LaunchLab 开发的第三方平台,Letsbonk.fun 沿用了 LaunchLab 的费用机制。对于所有基于 Letsbonk.fun 所发行的 Meme 代币,LaunchLab 会收取 1% 的联合曲线发行费用,其中 25% 直接用于 RAY 的回购;此外在代币冲出“内盘”后,Raydium 也将基于流动性池的费用规则进行收费,并将其中部分费用投入 RAY 的回购。

Odaily:Raydium 不同类型流动性池的费用回购比例。

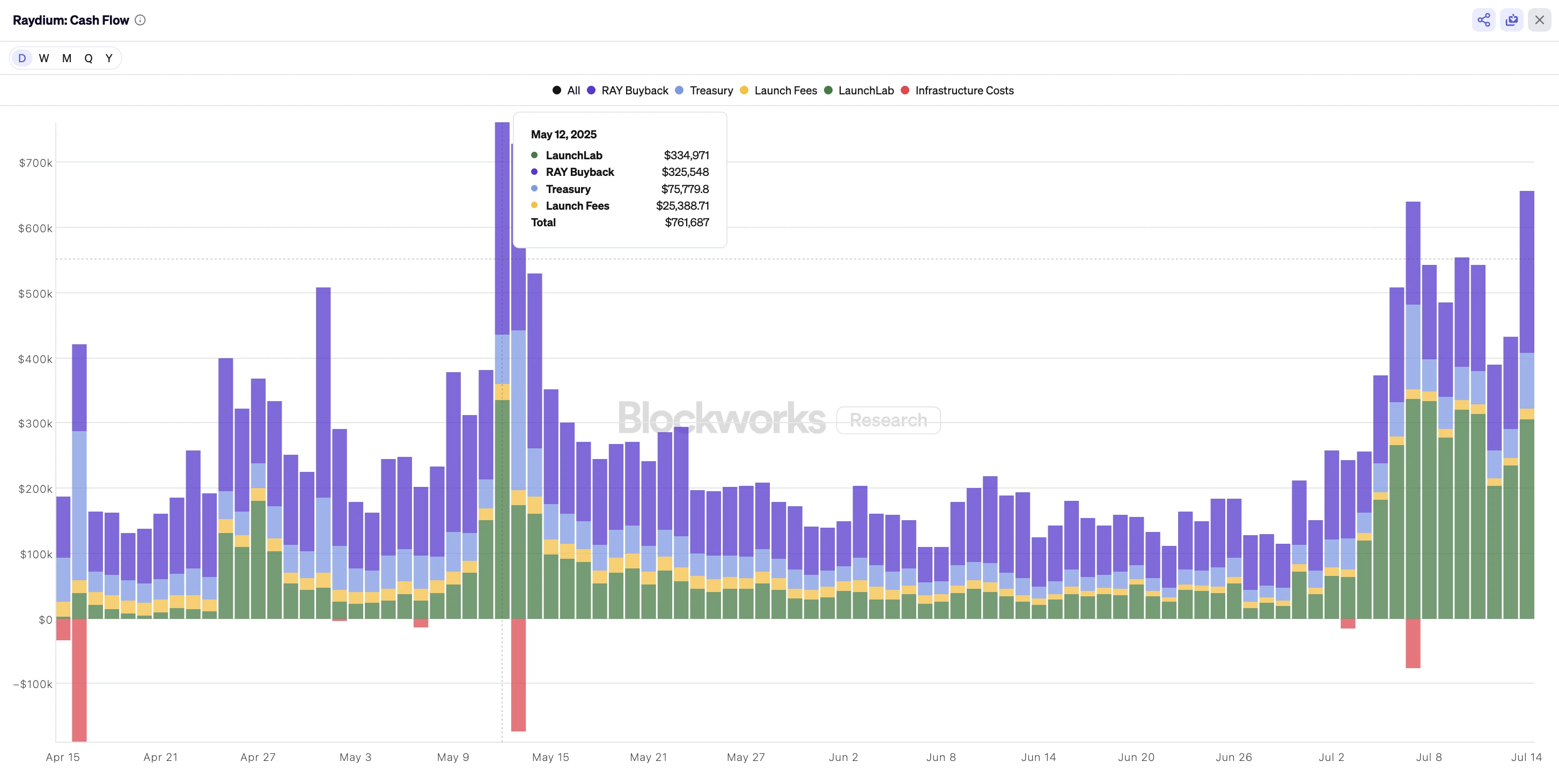

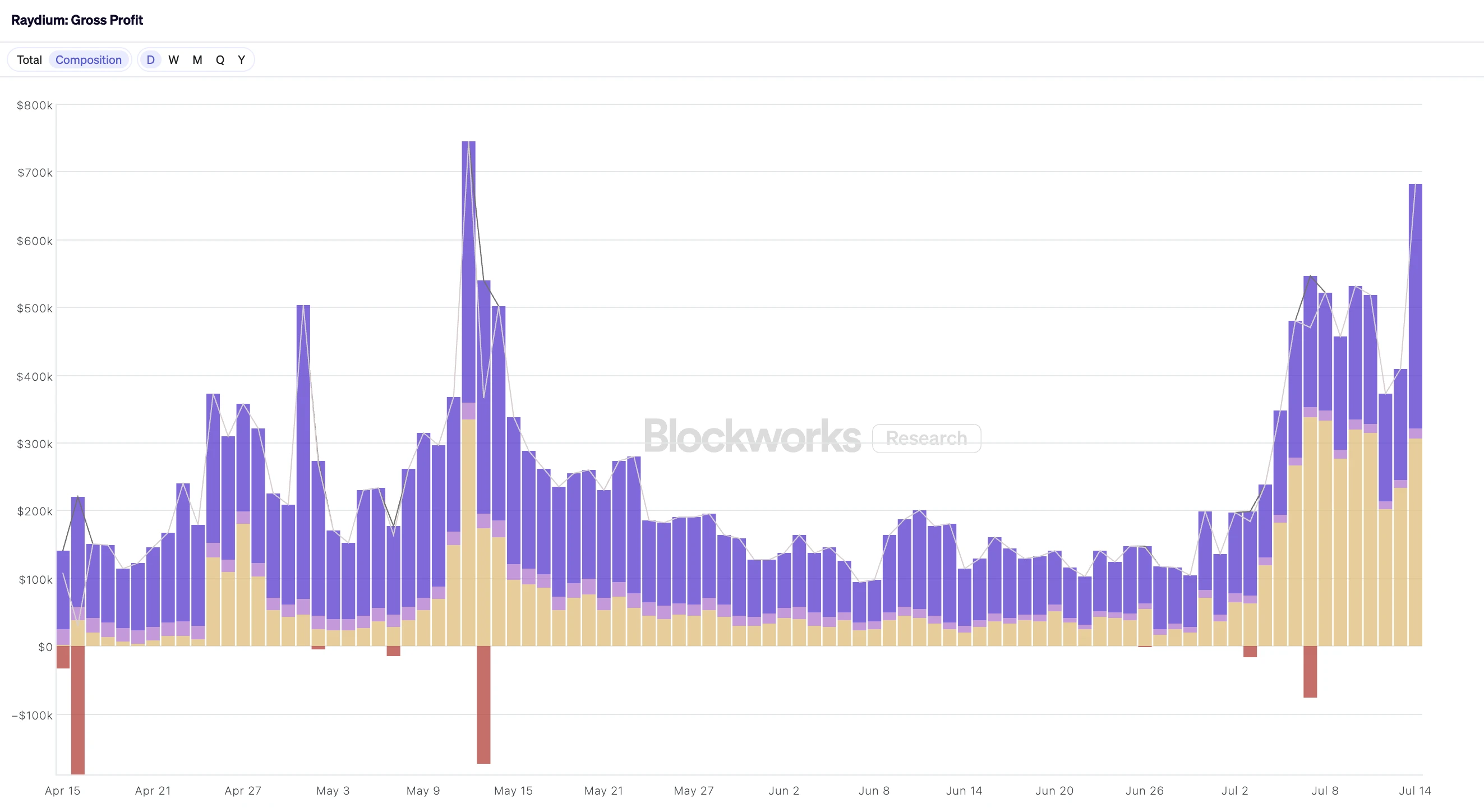

Blockworks 数据显示,自 4 月 16 日 LaunchLab 上线以来,Raydium 的协议收入及 RAY 回购量均已出现明显增长,且其增长轨迹与 LaunchLab 系平台的数据波动高度重叠 —— 5 月 13 日,LaunchLab 系平台在代币毕业数量上首次超越 Pump.fun,当天 Raydium 创下了 32.5 万美元的近期回购峰值;此外随着最近 Letsbonk.fun 的爆发,Raydium 的协议收入及 RAY 的回购量再次出现明显抬头。

更值得关注的是,此前 Raydium 的协议收入主要来源于流动池的兑换费用(下图紫色部分),但近期 LaunchLab 的发行费用收入(下图黄色部分)已逐渐反超,成为了 Raydium 新的主要收入来源,而这些费用的 25% 都将直接用于 RAY 的回购。

以昨日 24.9 万美元的回购数据静态计算,Raydium 每年将可投入约 9088 万美元用于 RAY 的回购,而当前 RAY 的流动市值约为 7.49 亿美元,这意味着每年 RAY 市值的 12% 将会被回购,这将形成巨大的持续性买盘。

Meme 之外,还有美股代币化

除去持续增长的 LaunchLab 费用收入之外,近期同样火热的美股代币化同样有望提升 Raydium 的协议收入。

此前,Kraken 的股票代币化平台 xStocks 已正式上线,并在 Solana 上发行了一系列热门美股的代币化凭证,而这些美股代币大多数都已在 Raydium 部署流动性池。虽然当下交易量规模仍然有限,费用贡献并不明显,但考虑到美股代币化的市场趋势,该板块同样具有较强的收入增长预期。

展望未来,如果 Letsbonk.fun 能够继续保持当下的市场份额(甚至不用考虑 LaunchLab 及其他第三方平台的增长),Raydium 便有望保持当下的协议收入水平及回购力度,再叠加上潜在的美股交易增长预期,该数据有望实现进一步的突破。