随着比特币相对于整体加密市场的强势逐步减弱,山寨币的上涨势头正日益增强。这一趋势可能表明,投资者的风险承受能力正在提升,市场中的投机行为也有所回温,尤其体现在对高贝塔资产的偏好上。

在当前阶段,越来越多交易员开始将关注点转向那些具有更大上涨潜力的山寨币。从历史表现来看,当比特币动能减弱时,交易者往往会通过加大对另类加密资产的资金投入,以此对冲风险或捕捉更高的收益机会。

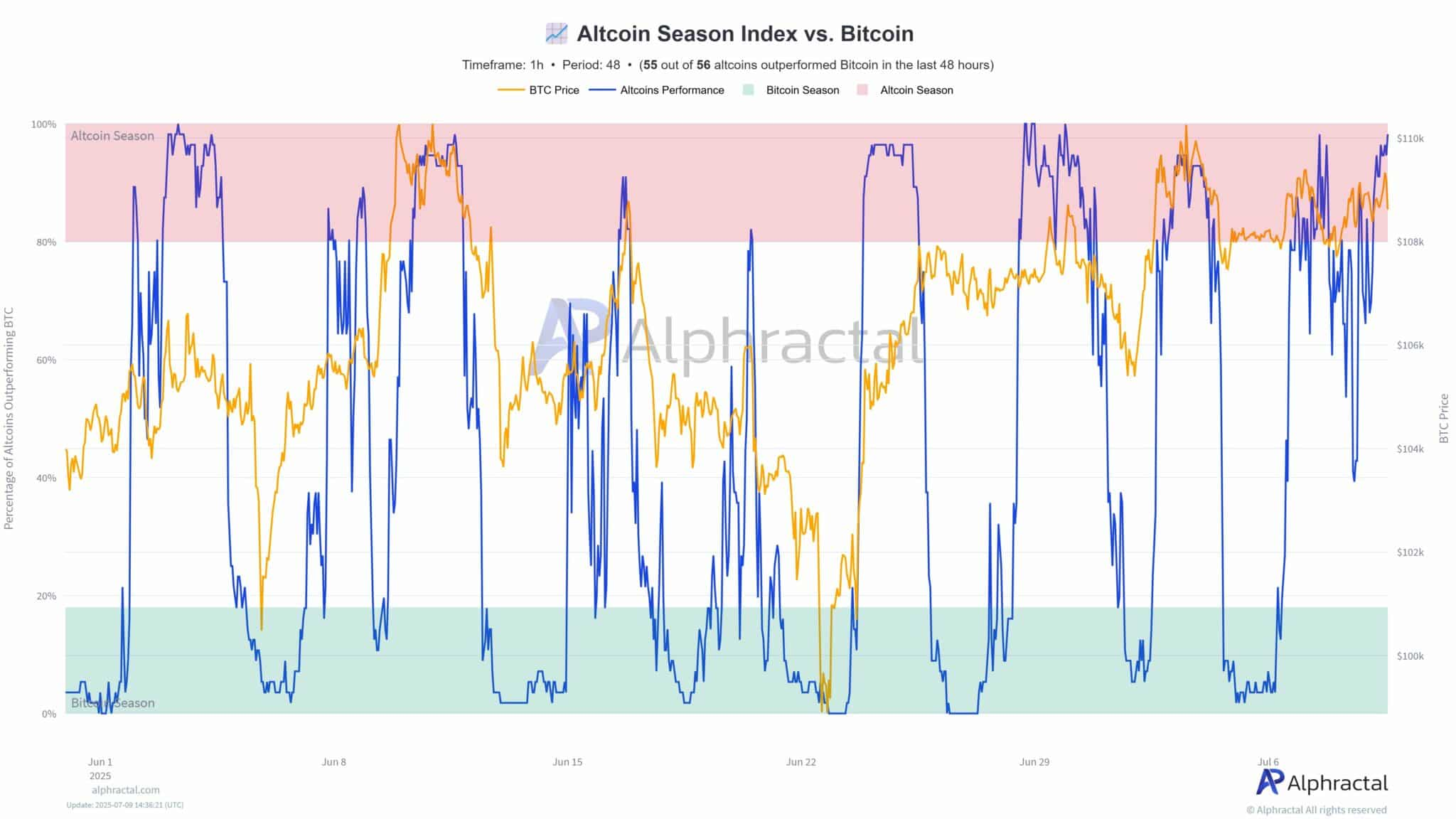

在比特币价格稳定于 11 万至 11.2 万美元区间的同时,山寨币市场却出现了明显的剧烈波动。这种“主稳副动”的行情,往往是山寨币阶段性反弹的典型特征之一。

同时,ETF 的资金流入也在大幅增长。数据显示,比特币的资金净流入达 2 亿美元,而以太坊的流入量则略高,达到 2.11 亿美元。值得一提的是,SOL(Solana)的质押型 ETF 产品也呈现出同步增长的态势。

尽管市场仍存在一定的噪音和质疑声音,但这些数据从侧面印证了一个趋势:如同许多交易者预期的那样,一轮更长周期、更广范围的山寨币季节,或许已经悄然开启。

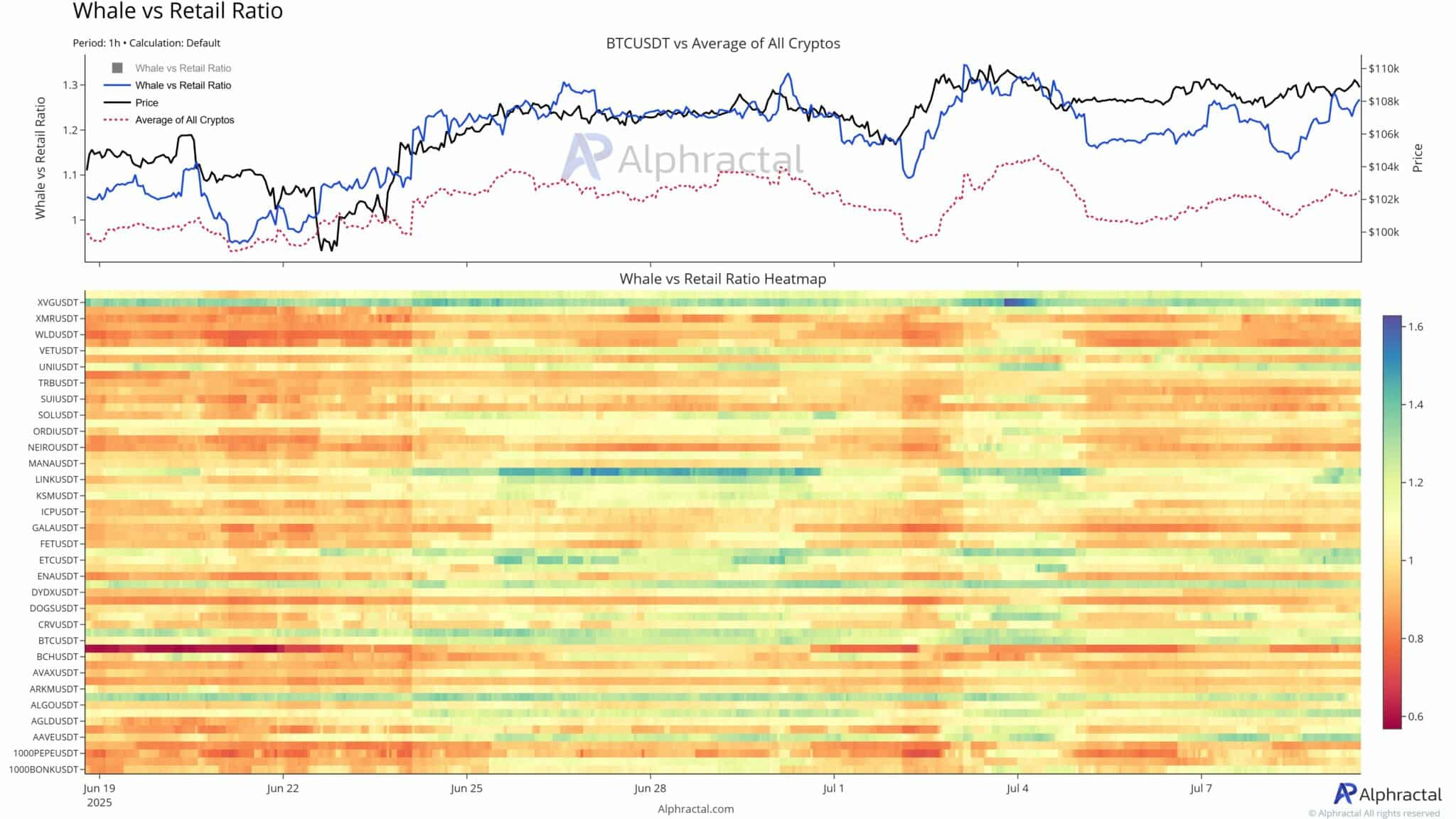

鲸鱼比你先知道行情?

另一个预示山寨币季节来临的重要信号,来自鲸鱼与散户交易行为的分化。

自 6 月底以来,鲸鱼用户的买入力度持续上升,其活跃度与散户之间的比例一直维持在 1.1 以上,意味着鲸鱼的买入规模远超零售用户。这一现象暗示,大资金正在提前布局山寨币市场。

与此同时,比特币价格也在震荡上行,带动部分主流山寨币同步上涨。这种价格联动,以及鲸鱼持续加仓的行为,表明市场正处于一个相对强势的阶段。

根据 Alphractal 的热力图,近期鲸鱼在多个关键山寨币上的活跃度明显增强,涉及项目包括 Algorand(ALGO)、Chainlink(LINK)和 Uniswap(UNI)。相较之下,散户交易行为更为零散,整体结构较为松散。

这种买盘上的不平衡,或许透露出更大的资金迁移信号。在历史周期中,大型鲸鱼的提前布局,往往预示着关键的市场转折点即将到来。

比特币统治力下滑,山寨币迎来窗口?

最后一个值得关注的核心信号是:比特币市场主导地位的转变。

该指标此前形成了一个“等高点结构”,预示市场短期可能出现反转。此后,该形态被打破,主导率开始走低,趋势线出现下破,形成了明显的“更低的高点”。这是一个典型的市场结构松动信号,意味着比特币相对其他资产的强势正在减弱。

数据显示,比特币的主导率已从近期高点的 66% 回落至 64%。虽然幅度看似不大,但足以说明:资金正在从比特币流出,并开始流向更具弹性的山寨币市场。

投机回归?山寨币正在接棒行情主力

随着比特币相对整体大盘的强势走弱,山寨币的热度逐步升温。这种资金转移背后,往往意味着市场的风险偏好正在提升,投资者的投机意愿也在增强,尤其是在高贝塔系数资产上的布局。

当前,交易者正将目光投向那些具备更大上涨潜力的山寨币标的。从历史经验来看,每当比特币动能减弱,市场中的一部分资金就会主动寻求更高波动性资产,以捕捉更大的收益空间。

而现在,这一轮熟悉的节奏,似乎又来了。