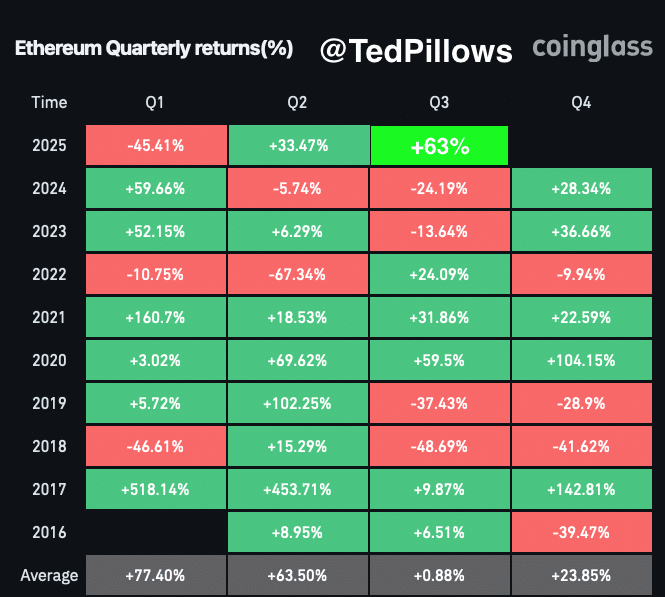

以太坊(ETH)在 2025 年第二季度实现了 33.47% 的强劲涨幅,再次成为市场关注的焦点,并点燃了投资者对 10 月份冲击 4,000 美元的预期。

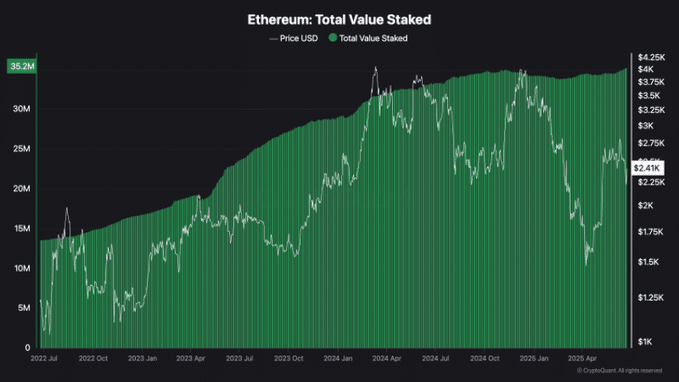

与此同时,ETH 质押量也创下历史新高:目前已有超过 3,500 万枚 ETH 被质押,占总供应量的近 30%。这不仅反映出用户对网络的信心增强,也显示出市场对以太坊长期价值的看好。

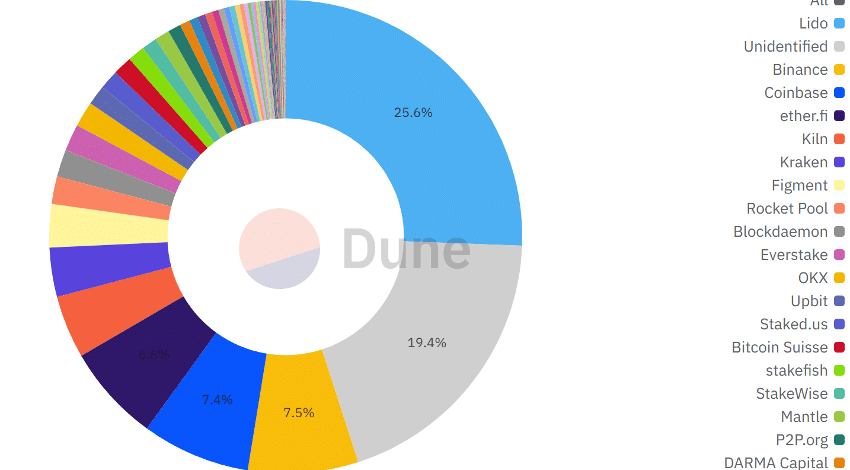

但在涨势和参与度飙升的背后,以太坊验证器的集中化问题也逐渐引发担忧。目前,Lido、Binance 和 Coinbase 共同控制着近 40% 的 ETH 质押量,使去中心化网络的安全性受到挑战。

ETH 的强劲反弹能否持续?

2025 年第二季度,以太坊反弹 33.47%,成功扭转了第一季度 45.41% 的下跌趋势。这一涨幅是近几年表现最好的季度之一,仅次于 2020 年的 69.62% 和 2019 年的 102.25%。

随着第三季度开启,市场情绪偏向谨慎乐观。社区普遍认为,若基本面持续改善,以太坊在 10 月底前有望重新挑战 4,000 美元关口。

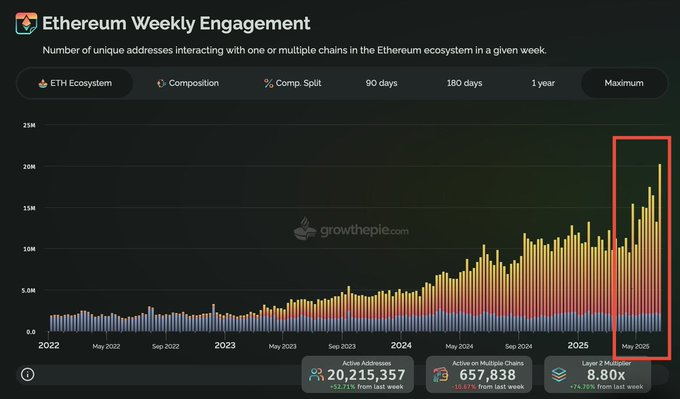

链上活跃度创历史新高,网络参与感显著提升

根据 GrowThePie 数据显示,2025 年 5 月,以太坊每周活跃地址突破 2,020 万,环比增长 52.71%,创下历史新高。链上参与度激增,为网络带来了更多交易、交互和锁仓需求。

以太坊正在“全力运转”,不仅仅是在价格层面,更体现在网络活跃度的深度提升。

超 3,500 万 ETH 被质押,供应逐步收紧

向 PoS 模式转型后,以太坊质押活动进入加速期。截至目前,质押 ETH 总量达 3,520 万枚,占总供应量的 28.3%,按当前价格计算,价值超过 840 亿美元。

仅在 6 月的前两周,新增质押数量就超过 50 万枚 ETH,显示出市场对质押收益和网络安全性的高度认可。

这波质押浪潮在一定程度上受到 美国 SEC 于 5 月发布的指导意见推动,缓解了部分机构的合规疑虑。

同时,长期持有者占比仍维持在约 19%,导致 ETH 在交易市场上的流通量不断减少,进一步推高市场紧张情绪和价格弹性。

骨感现实:集中化风险正在加剧

尽管以太坊网络运行数据令人振奋,但在背后,一个潜在的系统性风险正在悄然积聚:验证器的集中化问题。

据 Dune Analytics 数据,Lido 控制了所有质押 ETH 的 25.6%(约 870 万枚),Binance 和 Coinbase 紧随其后,分别掌握 7.5% 和 7.4% 的质押份额。

三大平台合计控制了将近 40% 的验证算力,一旦其中任何一个受到监管审查或技术故障,都可能影响以太坊新区块的近半生成能力,给网络安全与共识机制带来不小挑战。

流动性质押稀缺,DeFi 借贷成本走高

此外,随着质押代币 stETH 的流动性逐渐收紧,DeFi 平台上用于借贷的流动性资源也在萎缩,导致借贷成本走高,资产灵活性下降。

这进一步放大了以太坊金融生态的风险暴露,尤其在市场波动期,流动性瓶颈可能成为系统性风险的放大器。

总结:上涨之下,以太坊能否保持去中心化的灵魂?

以太坊正在快速重回市场视野,质押、活跃度、价格三线共振构筑出强势基本面。但与此同时,验证节点的集中趋势、stETH 流动性风险以及大型平台对网络算力的控制,都是未来不可回避的挑战。

这一轮上涨,或许能带我们到 4,000 美元,但真正的问题是:去中心化的以太坊,还能走多远?