作者:推特大V Murphy

以太坊赫芬达尔指数,用来衡量网络地址在当前供应量中所占的份额,即筹码集中度。指数高表示少数的大持有者正在主导市场,指数低则表示筹码分布更均匀。

在代币刚发行时,早期持有者往往集中了大量的供应,从而导致较高的赫芬达尔指数。随着这些早期持有者的抛售,指数开始下降,反映了代币分布从集中慢慢变得分散。

(图1)

图1就是ETH赫芬达尔指数;可以看到这个指数从2016年2月-2023年3月一直处于持续下降状态,说明在这段周期中ETH的筹码集中度越来越分散。到了2023年3月以后指标开始最走平,说明分散度见底。从2023年3月-2024年12月这段时间始终保持这样的分散程度。

但是,从24年12月后,筹码集中度突然开始上升了,这是从2016年以来从未发生过的事情。那会不会是因为现货ETF的余额增加,导致了赫芬达尔指数上升呢?

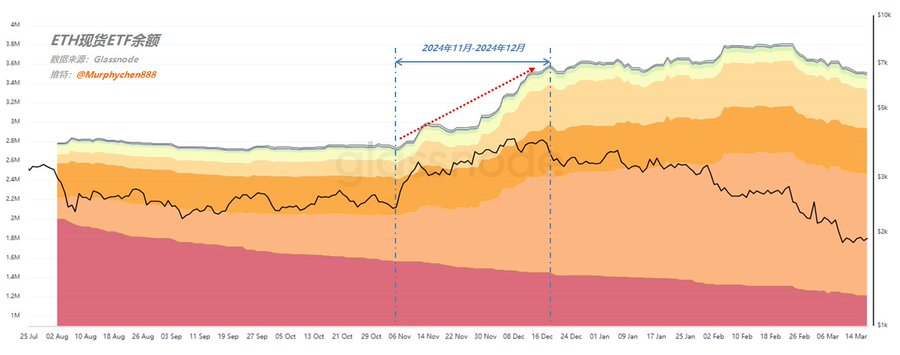

(图2)

图2是ETH现货ETF余额数据。可以看到现货ETF余额增长最快的时候是在2024年11月-2024年12月,期间从273w枚ETH增长到358w枚。12月以后增长速度明显放缓,基本保持平稳。而ETH赫芬达尔指数是在12月以后开始上升的,因此并不是现货ETF余额变化所导致。

说明确实有个别大资金正在积累筹码,使得ETH筹码集中度慢慢上升。

例如,我在3月15日的这篇推文(见引文)中所提到的,在$3,500建仓的大额地址群体,随时ETH跌至$1,900的过程中不断的补仓,从原先的166w枚ETH增加到194w枚;另外,当价格触及一群大户在2年前的建仓成本$1,850时,他们开始将之前高位卖出的部分又买回来平摊成本。从160w枚ETH增加到212w枚;

无论这些鲸鱼们是被动自救式买入还是主动低位加仓,都会让筹码集中度慢慢变高。所以,ETH难道真的是在“换庄”?

但这是一个非常缓慢的过程,因为在此期间也会有其他鲸鱼的筹码继续卖出从而降低集中度。筹码集中度变高有利有弊,有利的一面是当高到一定程度时,价格更容易被控制(容易拉升);不利的一面是在大资本收集筹码的过程中,市场或许会比较痛苦和煎熬。

当初筹码分散(派发)用了7年时间,而现在筹码集中(积累)又需要几年呢......