撰文:0xDecision,链上分析师

编译:zhouzhou,BlockBeats

编者按:本文分析了 SOL、TRUMP、LIBRA 和 MELANIA 等代币对市场的影响,指出这些项目导致了 Solana 生态系统的崩溃。特别是特朗普及其妻子的代币推广和拉盘,给投资者带来了重大损失。此外,预计 2025 年 3 月 1 日 SOL 将解锁大量代币,可能导致价格大幅下跌。文章还提到加密市场面临大量诈骗、黑客攻击等问题,但稳定币指数仍在上升。

以下为原文内容(为便于阅读理解,原内容有所整编):

我花了超过 10 小时分析 SOL 发生了什么,TRUMP、LIBRA 和 MELANIA 摧毁了这条链,目前只有一个决定扭转了市场,这是你在崩盘前保护资金可以采取的措施。

Solana 是一个特别快速的区块链,适用于应用和加密项目。

它专为速度和低成本而建,使交易既快速又便宜。

目前,SOL 因为一些问题而处于困境。

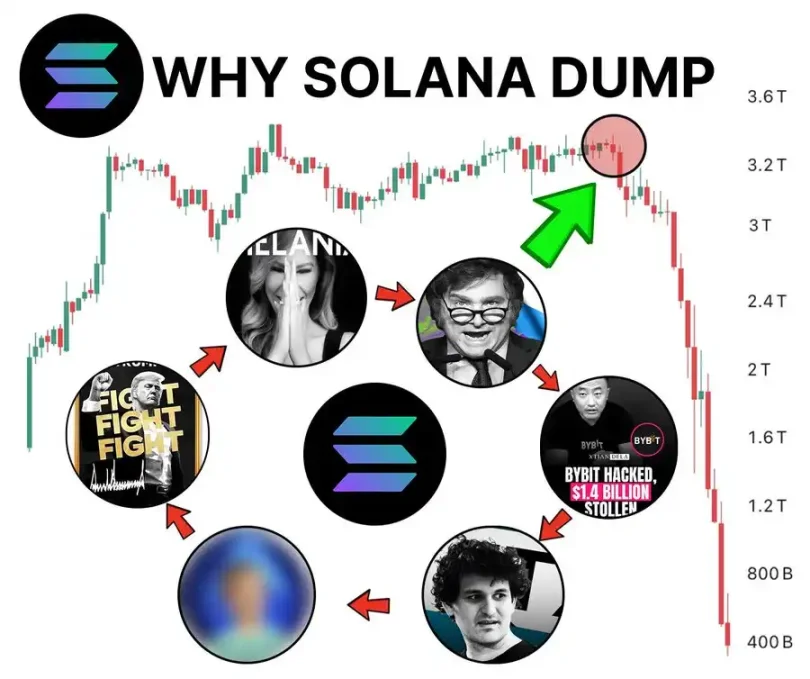

一个月前,SOL 价格大约在 270,现在已经下跌了 30%,这可能是即将到来的大跌的开始。我查阅了所有的事实,结果让我震惊……

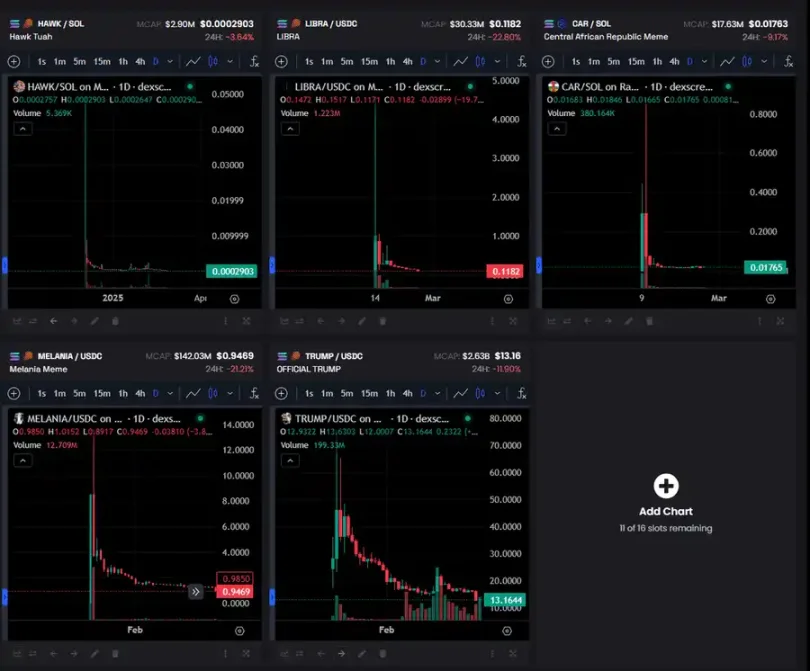

美国总统特朗普推出了 TRUMP 的 meme 币,而 SOL 正创下新高。他的举动伤害了整个市场,引发了混乱。启动后,资金开始从其他 meme 币流向 TRUMP。在 TRUMP meme 币发布的第一周,特朗普的数百个钱包出售了超过 20 亿美元的 TRUMP。这导致了图表崩盘,投资者损失惨重,纷纷撤离,这是引发 Solana 生态系统崩溃的导火索。

看到提款如此轻松后,特朗普的妻子推出了 MELANIA meme 币,这次比 TRUMP 还要糟糕。投资者在前 12 小时内损失了超过 90%,而团队提取了超过 5 亿美元。

2025 年 3 月 1 日,最大的 SOL 代币解锁将发生。约 22 亿美元的代币将被释放,这将导致价格大幅下跌,许多持有长仓的投资者会卖出以锁定利润,从而引发大规模的挤压。

一周前,@JMilei 在 Twitter 上推广了一个巨大的骗局。他还在 Instagram 上多次分享了这个骗局代币的合约地址。该代币的市值在短短一小时内从 1000 万美元飙升至 40 亿美元,但很快又在几小时内崩盘,降至 1 亿美元。

这次周期里从未发生过如此多的诈骗活动,而且现在都这么公开地进行。每三个没钱的名人就有一个在谈论加密货币,并在 SOL 上推出代币。然后,他们在几天内把代币拉盘 -99%,而且是在大家眼皮底下做的,这些事件让人失去了信心。

加密货币历史上最大的黑客攻击导致了 ETH 的大幅下跌。Bybit 被黑客攻击,15 亿美元的 ETH 被盗,这是一个巨大的损失。黑客攻击总是会伤害市场和人们的信心。

另一方面,稳定币指数仍远低于以往周期的水平,这个指数显示了有多少新资金进入加密市场。目前,它才刚刚开始上涨。

从整体来看,情况并不像表面那么糟糕,但事实是:我们现在处于不信任阶段。这样的时刻往往是最好的机会,在市场回暖之前,学习新技能、提升自己,这样你才能成为这个周期结束时的赢家。