上周末被称为加密货币领域最疯狂的周末之一。去中心化交易所 (DEX) 的交易量创下历史新高,Solana 在多个维度上表现突出,同时资金流向也显示了市场的显著变化。

以下通过 10 张图表带你快速了解这一现象背后的数据和趋势。

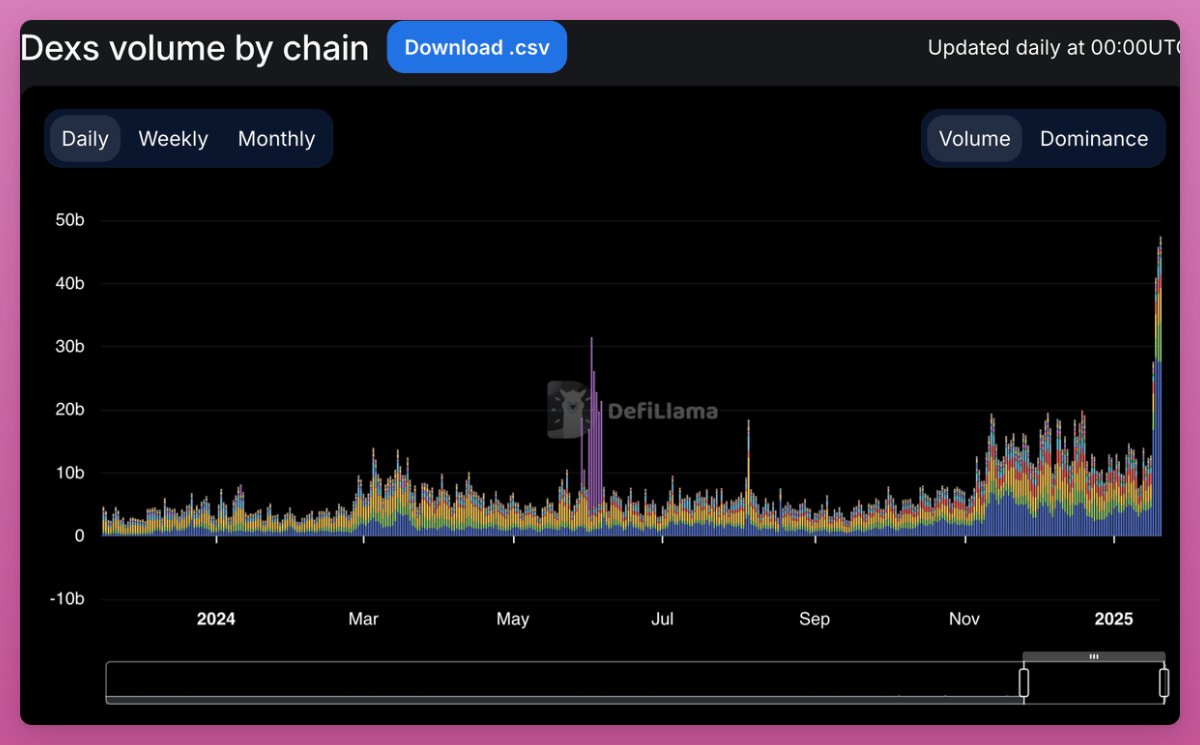

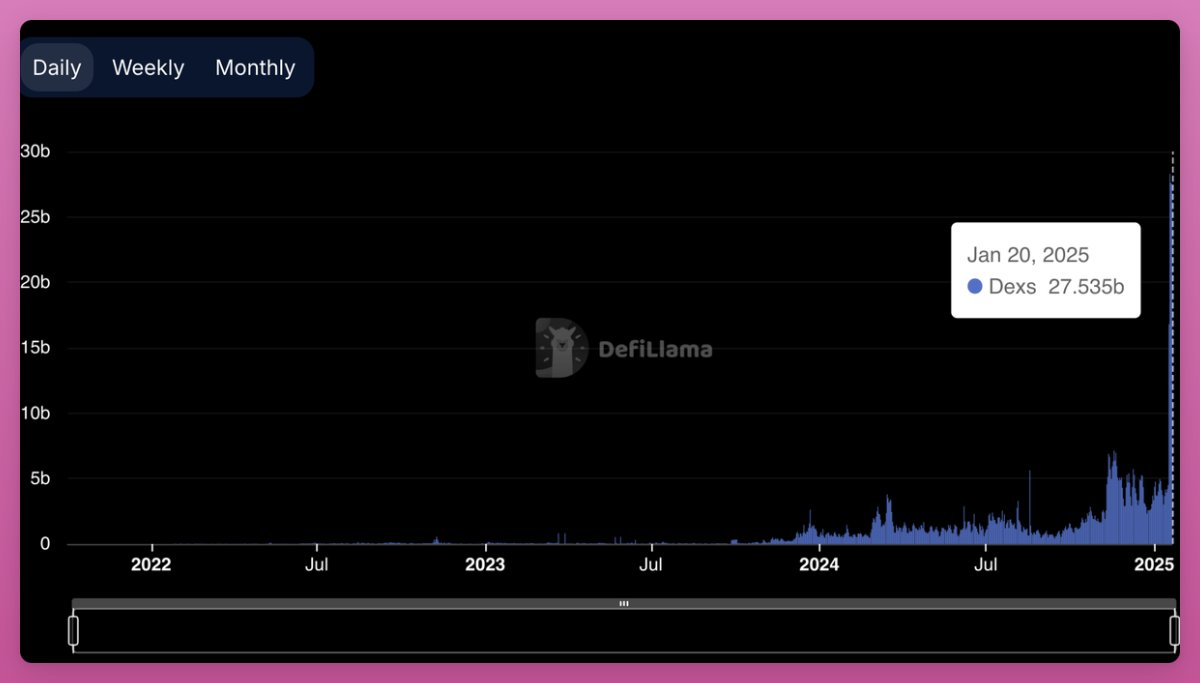

1. DEX 交易量创下历史新高

Solana 的去中心化交易所 (DEX) 交易量达到了 270 亿美元,远远超过以太坊的 50 亿美元。

2. Solana DEX 交易量暴增

Solana 的 DEX 交易量从平均约 50 亿美元飙升至 270 亿美元,实现了 5.4 倍的增长。

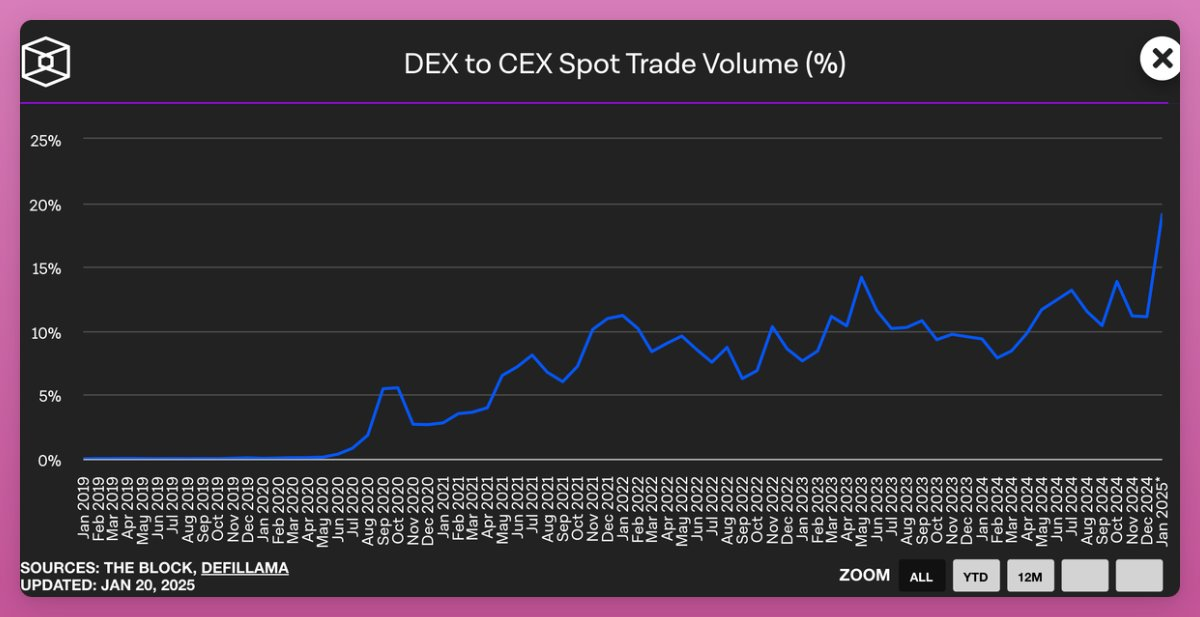

3. DEX 与 CEX 的交易量比达到历史新高

由于这一现象,DEX 与中心化交易所 (CEX) 的交易量比例达到了 19% 的历史最高点。

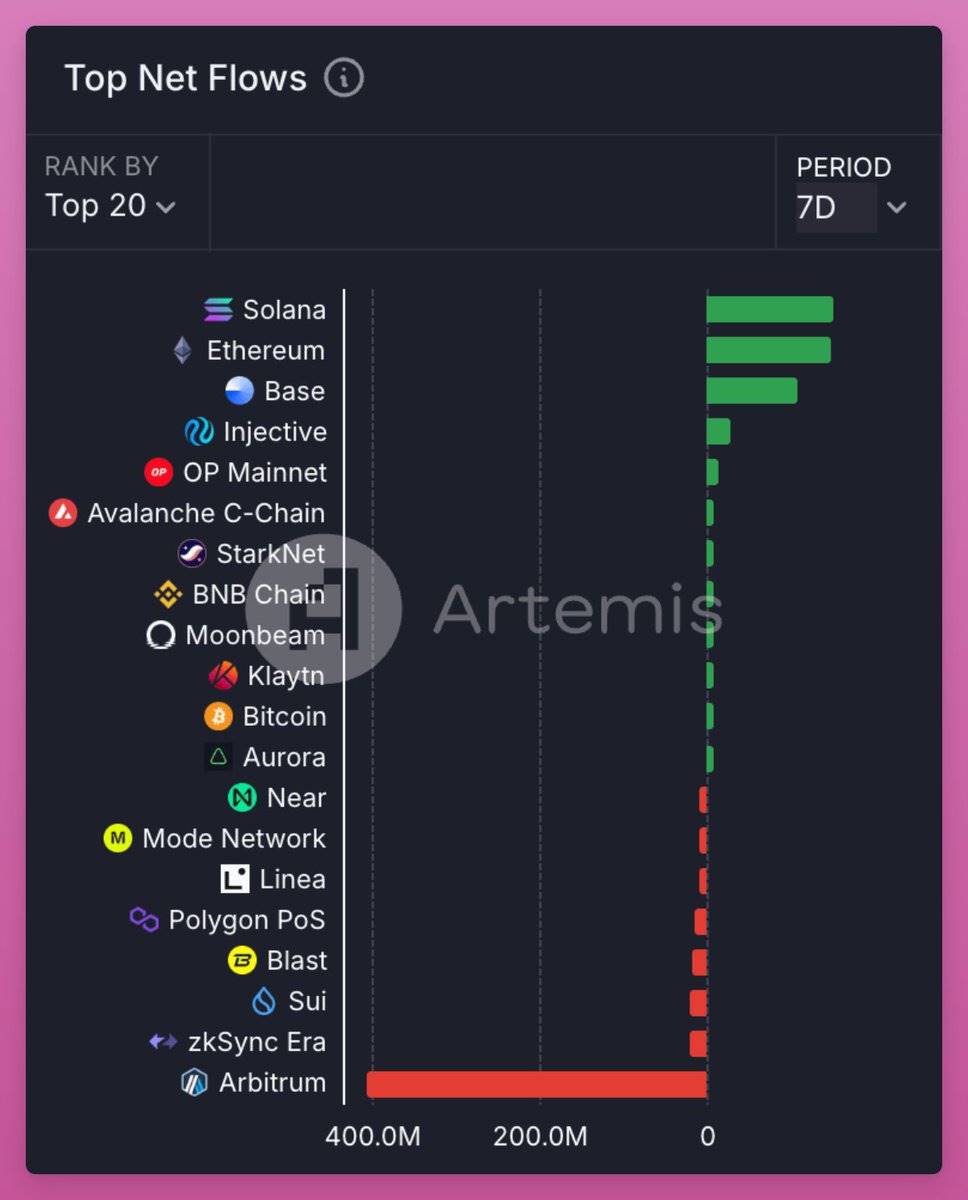

4. 资金从 Arbitrum 流向 Solana、ETH 和 Base

数据显示,Solana 在一周内实现了净流入 1.53 亿美元,而 Arbitrum 则损失了 4.05 亿美元。

(这个情况这是否与 Hyperliquid 的跨链桥有关?)

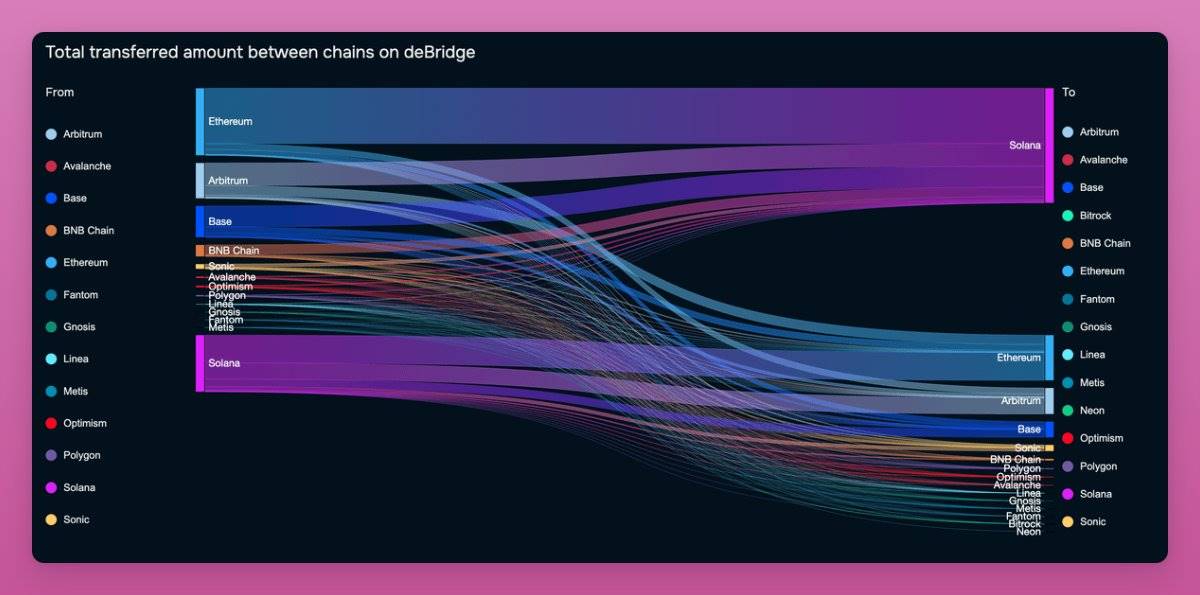

5. 资金流向 Solana 的可视化分析

根据 DeBridge 的数据分析,Solana 在一周内的资金流入达到约 3 亿美元,主要来自 Ethereum、Base 和 Arbitrum。

同时,Solana 的资金流出约为 1.4 亿美元。

6. Phantom 活跃度激增

Phantom 报告显示,其每分钟请求量超过 800 万次。用户通过 Phantom 交易的总量达到 12.5 亿美元,涉及 1000 万笔交易。

按照当前 0.85% 的手续费计算,Phantom 在这一期间的手续费收入达到约 1060 万美元。

@phantom:“交易现在已经恢复顺畅,所有系统运行正常。

尽管面临重重挑战,我们的用户今天依然达成了超过 12.5 亿美元的交易量,并完成了 1000 万笔交易,表现令人瞩目!”

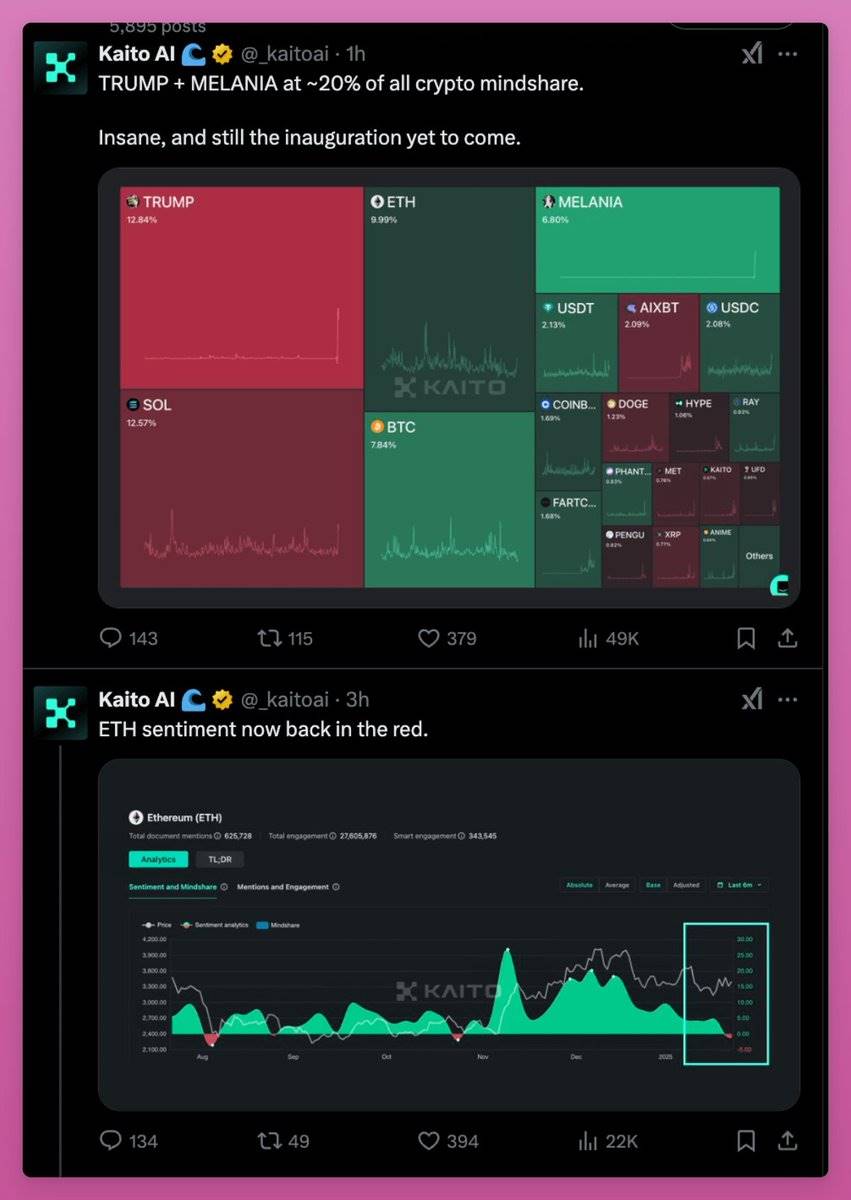

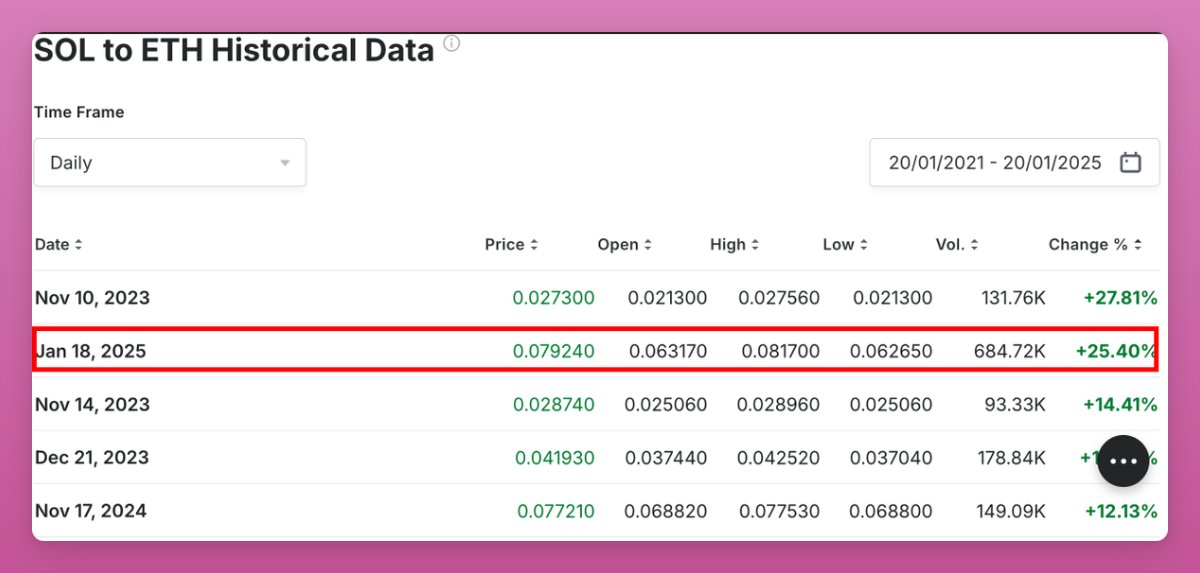

7. $TRUMP 推出当天 SOL 表现亮眼

$TRUMP 代币上线当天,SOL 对 $ETH 的汇率出现自 2021 年以来的最大单日涨幅,高达 25%。

这一重新定价进一步打击了 Ethereum 社区的士气,并加剧了对 Ethereum Foundation 改革的呼声。

SOL 超越 ETH 的可能性已经成为热议话题。

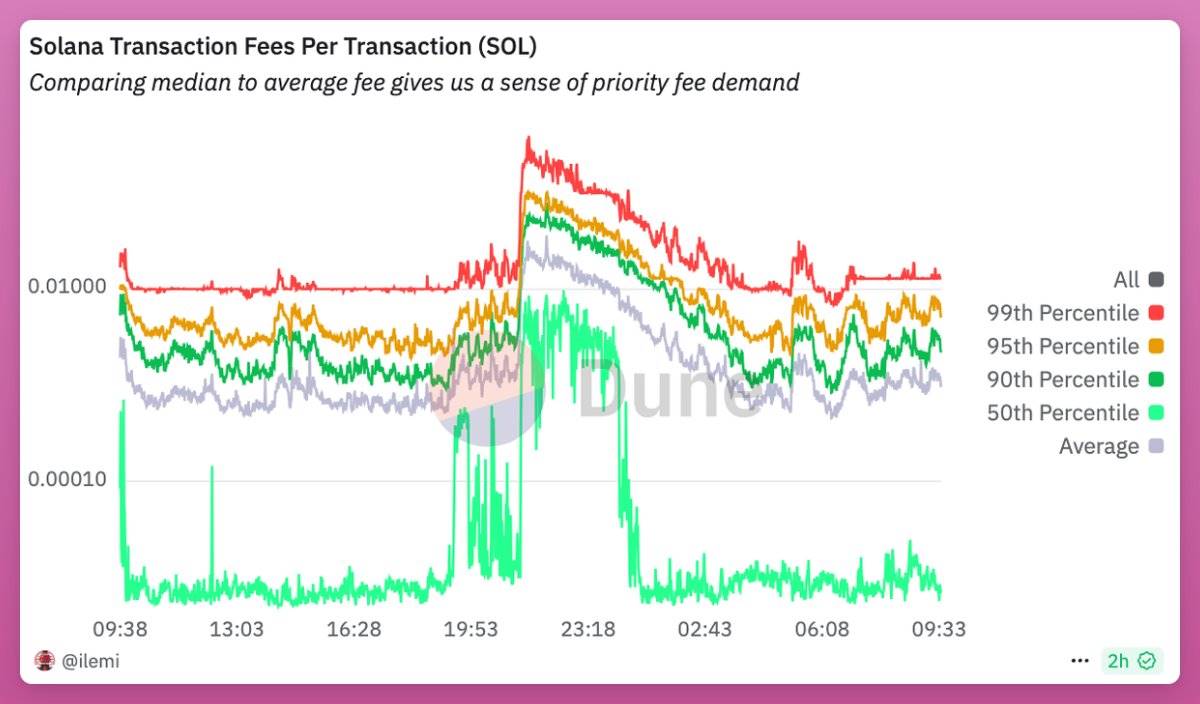

8. Solana 的挑战:手续费飙升

尽管表现强劲,但 Solana 的手续费在此期间平均飙升了 20 倍,许多用户无法成功完成交易。

9. 高手续费对 SOL Staker 的利好

高手续费为 SOL 的质押者带来了收益,总手续费收入达到 5700 万美元。其中,优先手续费 (Priority Fees) 占 3300 万美元,Jito Tips 占 2350 万美元。

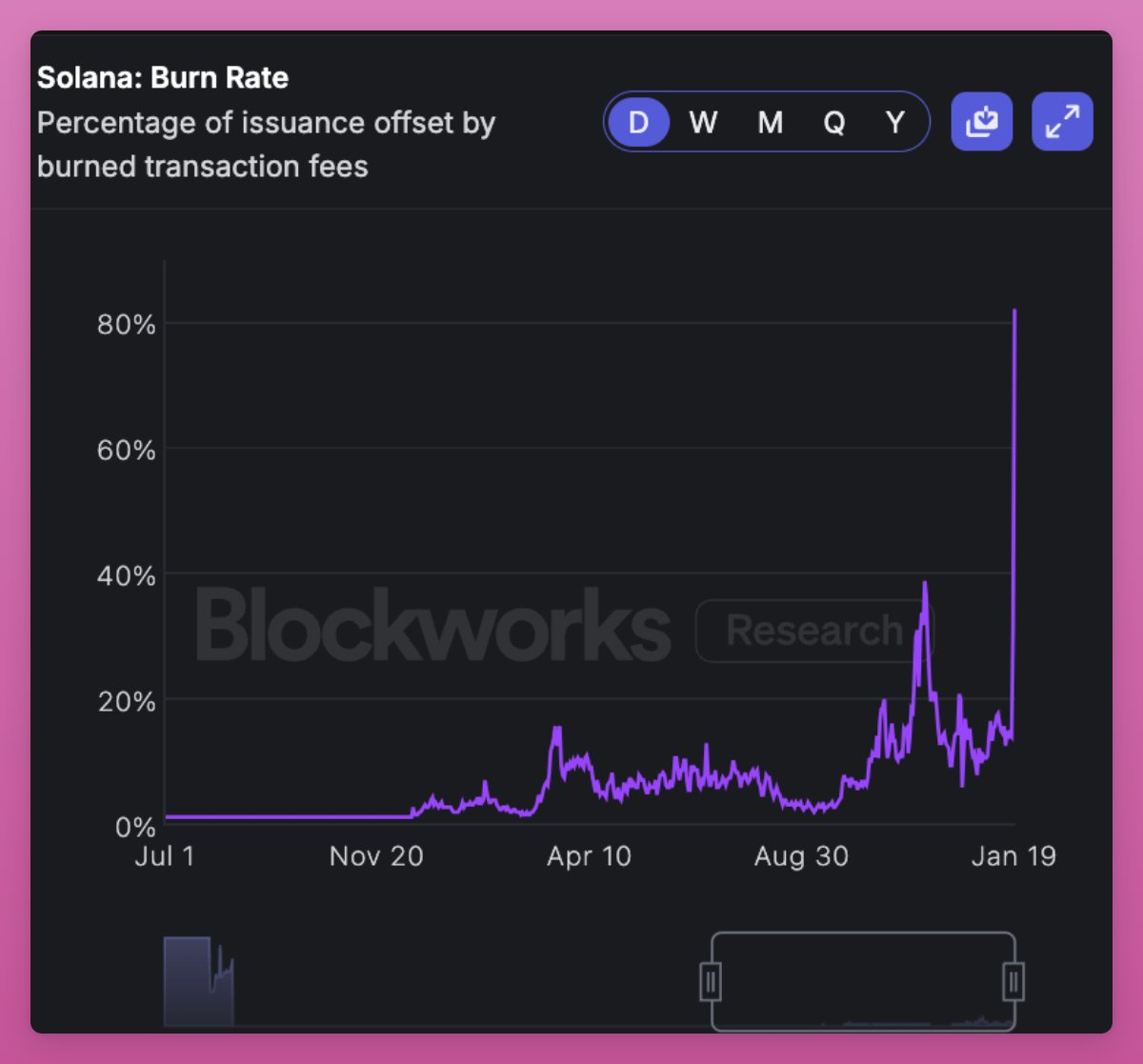

10. 此外,$SOL 的销毁量达到了创纪录的 1670 万美元。

不过,别急着宣传所谓的“超稳健货币 (ultra-sound money)”理论,因为即使是这一天的销毁量,也仅相当于 SOL 当日发行量的 81%。

总结:Solana 的周末

这一周末毫无疑问是属于 Solana 的:$TRUMP、MELANIA 和 $SOL 占据了市场的主要关注点。而与此同时,ETH 的市场情绪再次转为负面。