在加密市场,Meme币的爆炸性涨幅总是吸引无数投资者跃跃欲试,而Moonshot的出现更是让这个领域变得更加炙手可热。凭借极简的操作、法币入金功能,平台严选,以及精准捕捉链上热门Meme币的能力,Moonshot迅速跻身欧美年轻人心目中的加密神器。它被称为“链上小币安”,不仅因为它为用户提供了便捷的交易方式,更因为它打破了加密市场中“最后一公里”的瓶颈,让圈外小白也能轻松参与其中。

本文将深度探讨Moonshot的产品逻辑,分析它为何能在Meme币市场中脱颖而出,以及目前平台的发展趋势。

Moonshot产品概述

Moonshot 是一款专注于Meme币交易的移动应用,它部署于Solana区块链,支持用户通过Apple Pay、信用卡、PayPal等法币入金方式直接购买Meme币。用户无需理解复杂的区块链技术或管理私钥,也无需考虑Gas费用,从而大大降低了交易门槛。作为一个面向Web2用户的Web3平台,Moonshot通过简化加密货币的操作流程,吸引了大量对区块链不熟悉的用户参与Meme币投资。

核心功能:

- 法币入金:通过Apple Pay、信用卡和PayPal等支付方式,用户可以快速进行资金充值。

- 便捷交易:无需钱包管理或Gas费用,所有交易都通过Solana区块链在几秒钟内完成。

- 简易注册:仅需电子邮件或Face ID等常见注册方式,用户可以轻松创建账户,无需管理复杂的助记词和私钥。

- 代币筛选与上币机制:Moonshot严格筛选并快速上架高热度的Meme币,为用户提供潜在的暴利机会。

Moonshot的市场表现与财富效应

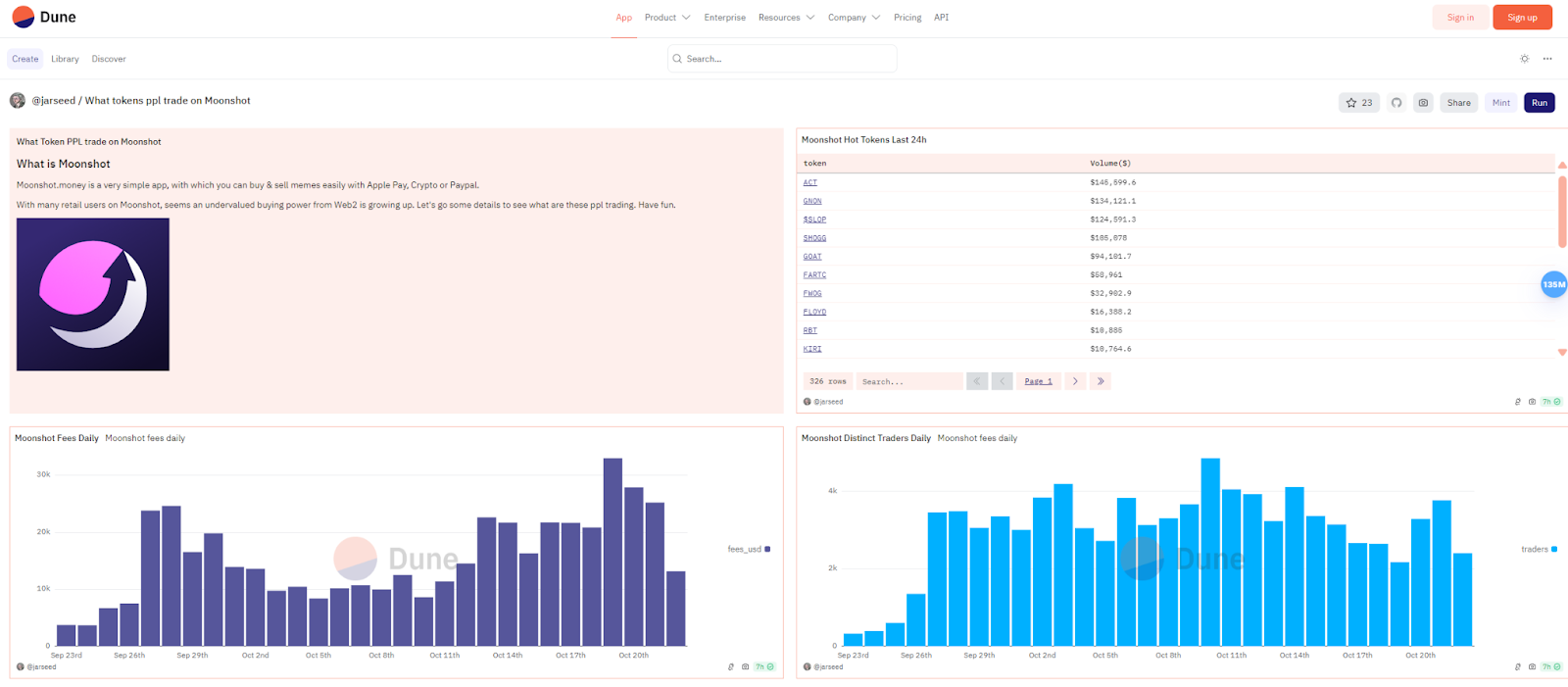

根据Dune数据,Moonshot的每日交易量在最近几周内持续激增,显示出平台强大的用户吸引力和市场活跃度。这种激增不仅仅是由于平台上简化的法币入金流程,还源于其捕捉市场热点的能力,特别是在Meme币爆发期的交易需求上。Moonshot通过便捷的交易方式吸引了大量新手用户,他们无需复杂的区块链知识,就能轻松参与交易。随着用户基础不断扩大,加密市场的资金流动性也在快速增强,推动了平台每日交易量的节节攀升。这一趋势不仅说明了Moonshot在年轻人中的受欢迎程度,还反映了其作为Meme币市场主力平台的地位正在逐步巩固。

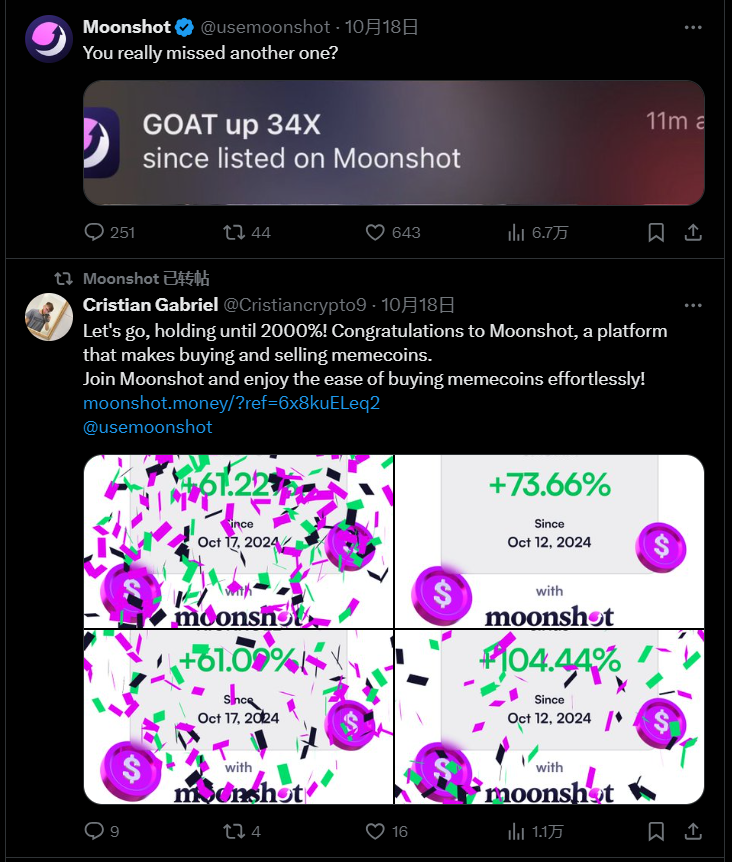

同时,多个Meme币在上线Moonshot后表现出惊人的涨幅,市值暴涨超过数十倍,进一步增强了平台的吸引力。例如,MOODENG和GOAT等代币在上线后不久,分别达到了100倍和30倍的涨幅,吸引了大量投资者争相入场。这些代币通过Moonshot实现了爆炸性的短期增值,平台的上币效应成为市场投机者追逐的焦点。Moonshot凭借其迅速上币机制和高度活跃的市场环境,放大了这些代币的财富效应,成为Meme币投资者的首选平台。这种现象不仅助长了投资者的FOMO情绪,也为平台持续注入了更多的资金和新用户,推动了市场的进一步发展。

如何注册使用Moonshot?

Moonshot之所以被年轻一代所追捧,除了其市场敏锐度和财富效应之外,还在于其简单易用的操作流程。以下是如何注册和使用Moonshot的详细指南:

1. 下载与安装

Moonshot 是一款移动应用,用户可以在 App Store 或 Google Play 商店中下载该应用。安装完成后,打开应用准备开始注册流程。

2. 注册账户

Moonshot 提供了非常简便的注册流程,用户只需通过以下几步即可完成:

选择注册方式:Moonshot 支持通过电子邮件、Face ID 或 Touch ID 注册。选择合适的方式后,用户只需输入电子邮件地址,点击确认即可。

无需助记词和私钥:Moonshot并不要求用户管理区块链钱包中的私钥或助记词,这对不熟悉加密技术的用户极为友好。注册过程结束后,平台会为用户自动生成一个钱包地址,用户无需任何额外操作。

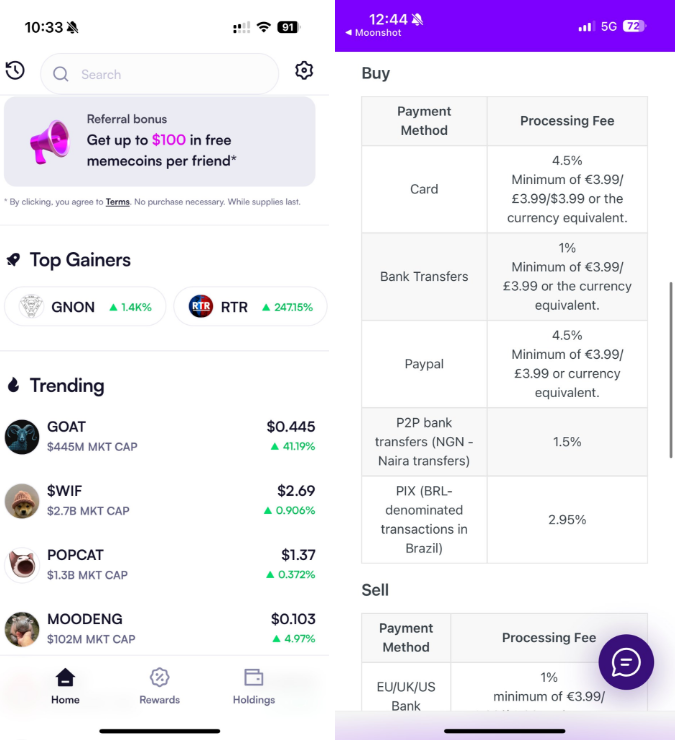

3. 法币入金

与传统的加密交易平台不同,Moonshot 支持法币直接入金。用户可以选择以下几种方式:

Apple Pay:通过 iOS 系统内置的 Apple Pay 功能,用户可以快速充值资金。

信用卡:平台支持使用 Visa 或 MasterCard 进行充值。

PayPal:对于偏好电子支付的用户,Moonshot 也支持 PayPal 进行资金转移。

资金到账通常只需几分钟,用户可以迅速开始进行Meme币交易。这一法币入金功能大大缩短了用户从法币到加密货币的操作流程,是Moonshot吸引大量新用户的关键所在。

4. 购买Meme币

完成入金后,用户可以浏览Moonshot上架的各种Meme币项目,选择想要交易的代币。交易流程非常简单:

选择代币:在首页或搜索框中输入感兴趣的Meme币名称,点击进入该代币页面。

输入购买金额:选择你想购买的金额,系统会自动计算你将获得的代币数量。

确认交易:确认购买后,系统将在后台自动完成交易结算。由于Moonshot依赖于Solana公链,交易速度非常快,用户通常可以在几秒钟内看到交易结果。

5. 提取收益

在交易获利后,用户可以通过MoonPay快速提现,Moonshot 支持将资产转化为法币并返回到用户的银行账户中。整个提现过程极为便捷,用户无需担心复杂的审查流程,通常几分钟内即可完成出金。

这种快速、高效的交易体验让Moonshot成为了年轻人眼中的“财富神器”,特别是在充满波动的Meme币市场中,Moonshot为用户提供了更便捷的操作体验与更大的盈利机会。

为什么Moonshot能成为年轻人的加密神器?

Moonshot能够在Meme币市场脱颖而出,成为年轻一代用户的加密神器,背后有着一套清晰的产品逻辑,这些设计准确抓住了年轻用户的核心需求:便捷性、快速获取财富效应,以及极简操作体验。

1. 降低技术门槛:便捷的法币入金与简化操作

Moonshot最核心的逻辑是大幅降低加密货币交易的技术门槛。传统的加密货币交易平台往往要求用户拥有加密钱包、管理私钥、设置Gas费等复杂操作,这对不熟悉区块链技术的新人来说无疑是巨大的门槛。

Moonshot通过极简的注册流程和法币入金渠道,让那些从未接触过区块链的用户也能轻松参与到Meme币市场中。用户只需通过电子邮件或Face ID完成账户注册,整个过程无须助记词和私钥的管理。更重要的是,用户可以通过Apple Pay、信用卡、PayPal等熟悉的支付方式直接入金,无需额外兑换加密货币或管理Gas费用。这种无缝对接Web 2支付方式的设计,大大降低了用户的学习成本,让他们能够快速进入交易状态。

2. 抓住短期财富效应:上币与爆发增长机会的放大器

Meme币市场的短期暴利特性是吸引投机者的重要原因。Moonshot通过快速上架热门Meme币,帮助用户在Meme币的市场情绪高涨时抓住短期的投资机会。许多代币在Moonshot上线后实现了大幅增长,MOODENG和GOAT等代币在短时间内都创造了数倍甚至数十倍的收益。

Moonshot 的上币效应极大放大了Meme币的短期财富效应。平台通过对代币的严格筛选,保持较低的上币频率,这不仅为用户提供了更多的短期机会,也使每次上架的代币更具爆发力。正是这种短期财富效应,使得Moonshot成为了年轻人眼中的“财富引擎”,他们通过平台捕捉到一个又一个“百倍币”的机会。

3. 极简体验与年轻人社交化投资的完美契合

年轻人已经习惯了移动支付和即点即买的互联网消费体验,他们对于复杂的技术和繁琐的流程并不感兴趣。Moonshot通过极简的操作流程和快速的法币入金功能,让年轻用户能够像在App Store中购买应用一样轻松交易Meme币。这种极简操作的体验让用户能专注于市场机会,而不必为技术操作烦恼。

更重要的是,Moonshot还结合了年轻人偏好的社交化投资体验。用户通过平台的邀请机制,能够拉动更多好友加入交易,形成一个具有高度互动性的社区。在这个社区中,用户不仅分享投资经验,也通过上币推送迅速抓住市场机会,形成了平台内部的社交化投资氛围。

这种基于社交的投资逻辑,使Moonshot不仅仅是一个工具型平台,而是一个让年轻人分享财富故事、相互学习的社交场所。这大大增强了平台的用户黏性和活跃度。

挑战与未来发展

尽管Moonshot在Meme币市场中取得了巨大成功,但平台的未来发展仍面临几个关键挑战。

1. 短期财富效应的风险

Meme币市场本质上高度投机,尽管Moonshot的上币效应能够在短期内带来巨大的财富机会,但许多Meme币在市场情绪消退后,价格会迅速回调甚至归零。这种风险可能导致用户在短期暴利后迅速失去兴趣,平台需要通过进一步的工具和机制帮助用户管理风险,例如提供市场风险提示功能,帮助用户在波动较大的市场环境中做出更理性的决策。

2. 用户增长与竞争压力

目前,Moonshot每天新增的用户数量已超过1万,但随着Prerich等竞争对手推出相似的法币入金服务,平台面临的竞争压力逐渐增大。为此,Moonshot需要通过引入更多新兴资产类别,如NFT和GameFi代币,增强平台的多样性和吸引力,并进一步提升用户体验,保持其竞争优势。

3. 监管与安全挑战

随着Moonshot在全球范围内的用户数量增加,平台在合规性和安全性方面的要求也日益提升。特别是在欧美等市场,Moonshot需要确保其运营符合KYC(客户身份验证)和AML(反洗钱)等金融法规。此外,平台需要进一步强化安全防护,保障用户资金和数据的安全,避免因简化操作而带来的潜在安全隐患。