原文作者:Murphy,链上数据分析师(X:@Murphychen 888)

挖矿成本对 BTC 价格下限的影响有多少?

有些小伙伴对「挖矿成本是否影响 BTC 价格」有误解,他们认为在当前资本时代,矿工手上的 BTC 在整个流通市场的占比很小,因此矿工抛售与否并不影响 BTC 的价格走势。

这里可以谈谈我的个人观点。首先,挖矿成本对 BTC 的价格「上限」没有影响,这是毋庸置疑的;但却会在很大程度上影响 BTC 的价格「下限」。这其中的逻辑并非是矿工到了成本价会抛售或不抛售手上的筹码,而是在于市场需求端的心理因素。

当 BTC 的价格低于挖矿成本时,投资人会认为此时在二级市场买入 BTC,要比动辄投入千万资金费时费力通过挖矿获得 BTC 要划算的多。类似于一种「占便宜」的心态,占了矿工的便宜,从而引发市场更多的需求。好比我们买东西,当发现物品的生产成本和价格持平甚至高于价格,我们会买的更加「心安」,就是觉得自己占便宜了(买不了吃亏买不了上当)。

其次,当 BTC 的价格下跌到一定程度,矿工无法覆盖成本便会选择退出部分算力,从而难度下降。难度下降让挖矿成本降低,「占不到便宜」市场需求减弱,从而价格继续下跌,算力继续退出...... 这就进入了死亡螺旋。强大的算力是 BTC 去中心化及系统安全的重要保障。在极端情况下,无人打包、矿场倒闭、矿机卖不掉甚至资产安全受到威胁,这不符合所有人的利益。

因此,挖矿成本一定会在某种条件下影响 BTC 的价格下限!

那么如何正确地衡量挖矿成本?我们可以借助一个简单的计算模型进行推演:

挖矿成本主要包括 2 个方面:购买矿机和后期运维。其中后期运维成本又主要包括电费及其他(人工、厂房、维修、贷款等)运营成本。我们假设电费成本占比 70% ,其他成本占比 30% ,再加上购买矿机的成本,便组成了矿工的主要成本。

算力价格是指每天每 E 算力(1 E = 100 w T)所能产生的 BTC 的数量(包括出块奖励和手续费收入),当前是 0.809 ;

单位电价按$ 0.053 ,我选取了目前市场上存在的 5 款矿机作为样本,其中 S 19 XP Hyd 是上轮周期的主力矿机,T 21 是本轮周期的主力矿机,而 S 21 目前官网销售的是期货,理论上还未大量部署。所有矿机参数和价格均采集于比特大陆官网。

以上表格便是根据上述模型进行测算得出的结果。可以看到当 BTC 价格在 42, 000 美元时,主力矿机T21的利润率为负。意味着此时在二级市场买入 BTC 要比挖矿更划算。

巧合的是, 42, 000 这个极限值与我在 6 月 23 日发表的《从链上数据分析,本轮牛市 BTC 价格回撤的极限值是多少?》一文中用 STH-MVRV 和 TMMP 测算的回撤极限值将不低于 43, 000-44, 000 这一观点非常接近。

当 BTC 价格低于 56, 500 美元时,T21的回本周期需要 48 个月。通常来说,一台矿机的最大使用寿命在 3-4 年左右, 3 年后即便矿机不出故障,由于落后的能效比也会被新款矿机所取代。届时老款矿机剩余残值几乎为零,只能给电费成本极低甚至免费电的矿主继续发光发热,要不就得按废铁称斤卖掉。因此,对于 48 个月才能回本的 T 21 来说,这个价格太不友好了。假设未来 BTC 价格不涨,相当于辛苦 3 年刚刚回本的矿工又要面临被淘汰,试问这样的生意谁愿意做?

因此,从这个角度看 56, 500 以下的 BTC 同样具有一定的性价比,尤其比较适合喜欢定投的小伙伴。

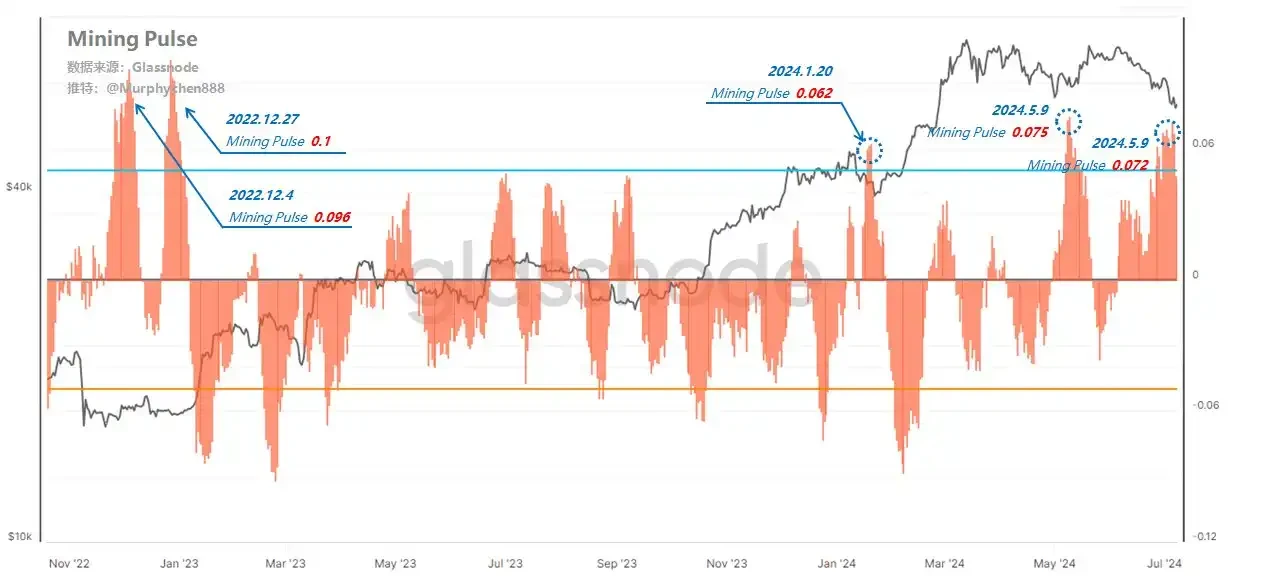

更新:Mining Pulse 是一个衡量矿工挖矿速度的指标。它主要反映了 14 天平均出块间隔时间与目标时间(10 分钟)的偏差。具体来说,Mining Pulse 可以帮助我们理解以下几点:

1、偏差表示速度差异:

负值表示实际区块时间比目标时间更快,正值表示实际区块时间比目标时间更慢。

2、负值表示:

· 更快的区块时间:如果 Mining Pulse 显示负值,意味着区块被挖出的速度比预期更快。

· 哈希率增长:这通常发生在网络哈希率增长速度超过难度上调速度时。也就是说,更多的算力(矿工)正在加入,导致区块生成时间变短。

· 网络扩展:表明网络的哈希算力正在扩展。

3、正值表示:

· 更慢的区块时间:如果 Mining Pulse 显示正值,意味着区块被挖出的速度比预期更慢。

· 哈希率下降:这通常发生在网络哈希率下降速度超过难度下调速度时。即一些矿工可能关闭了设备(算力退出),导致区块生成时间变长。

· 矿工下线:表明一部分矿工正在离线,减少了网络的总哈希算力。

如上图所示,正值越大表明当前 BTC 的价格越接近矿工的挖矿成本线,导致矿工投降的范围越大。在本轮周期,从熊市底部到目前为止,一共发生了 5 次 Mining Pulse 超过+ 0.05 的情况。

第 1 和第 2 次发生在 2022.12.27 和 2022.12.4 ,当时正值熊市最底部,BTC 价格在 16, 000-16, 500 美元左右。Mining Pulse 达到 0.1 ,即区块被挖出的速度比预期要慢 10% 左右,大面积的矿工投降,行情进入严冬期;通常这也是底部即将出现的特征。

第 3 次是 24 年 1 月 ETF 通过后,BTC 价格回调到 39, 450 美元;第 4 次是 BTC 突破 7 万美元大关后大量中短期筹码获利了解,价格回调到 58, 200 美元;第 5 次就是现在,Mining Pulse 已经达到 0.072 ;

回看历史数据,如果每次都在挖矿成本线附近买入 BTC,相当于以比矿工还低的成本获得了 BTC,从中长期角度说获得收益的确定性要大于承担风险的不确定性。

注:以上计算模型并非精准挖矿成本统计,存在一定程度的误差,但会比大家在网上看到的「关机价」更加贴近真实成本(关机价通常只计算了电费)。如有疏漏之处,欢迎专业矿工提出指正!