Author:Mesh

Compiled by: Deep Tide TechFlow

January 6, 2026

I've been tracking the "wallet to bank" development trend for several months now, and honestly, the pace of progress is astonishing.

By the end of 2025, three projects reached significant transaction volume milestones, achieving what Metamask could not: converting your cryptocurrency into real spending power without touching a centralized exchange (CEX). Superform, Veera, and Tria are no longer just crypto wallets; they are building actual banks.

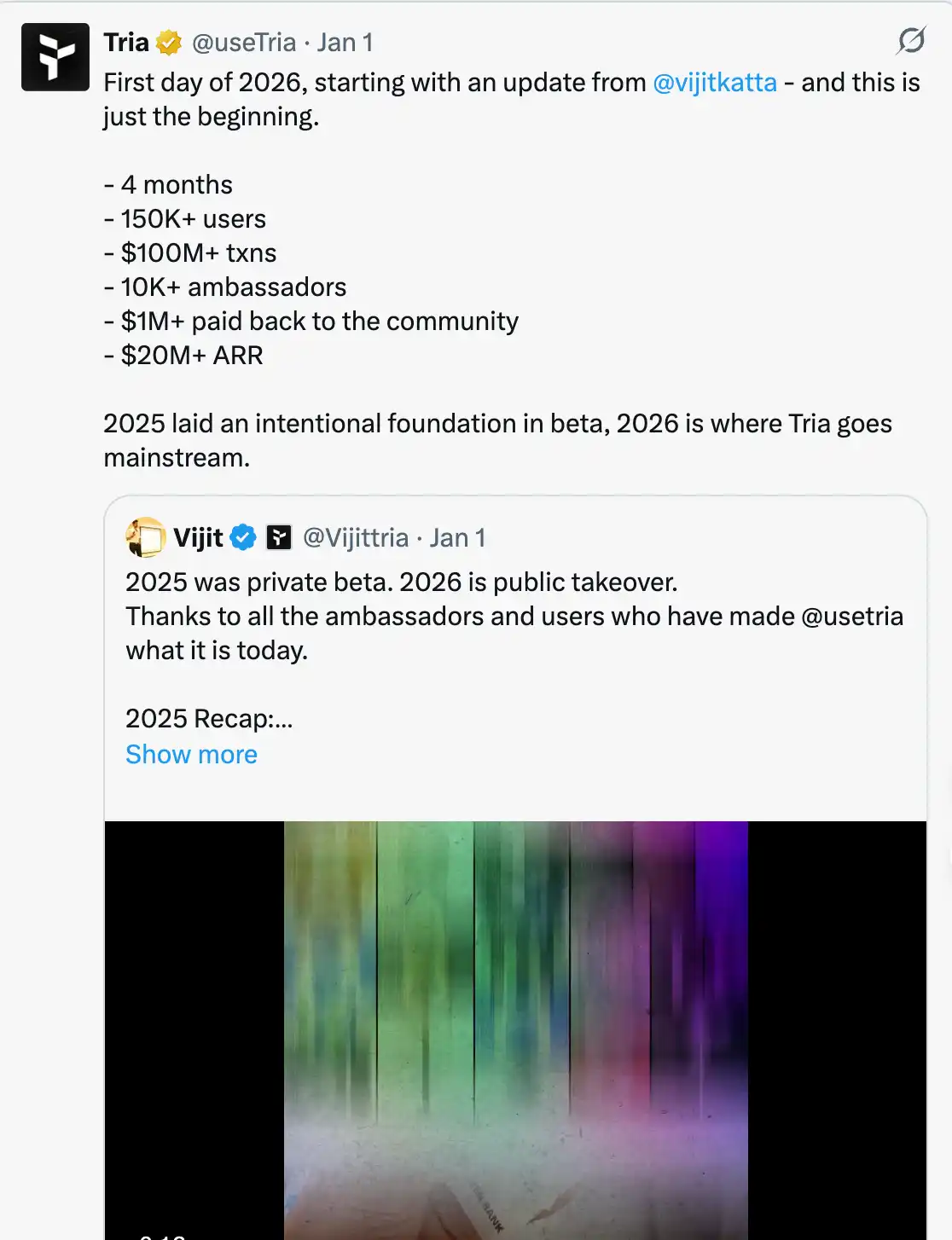

The data speaks for itself. By last November, Tria's daily transaction volume had reached $1 million, with over 150,000 users and an Annualized Run Rate (ARR) of approximately $20 million. Veera expanded to 108 countries, reaching 4 million users. And Superform's Total Value Locked (TVL) surged 300% in just six months, reaching $144 million.

This isn't the so-called DeFi 2.0 hype. This is an infrastructure shift that everyone saw coming, but no one expected it to arrive this quickly.

Let's dive into an analysis of these three projects, along with other potential challengers worth watching.

What is an Onchain Neobank?

Let me break it down for you, as this term is often used loosely.

An Onchain Neobank combines three elements that have traditionally been difficult to merge:

- The Power of DeFi: Includes yield optimization, staking, and cross-chain swaps.

- The User Experience of Traditional Banking: Such as a card you can use at Starbucks, instant payments, and cashback rewards.

- Blockchain Abstraction: Users don't need to deal with Gas fees, cross-chain bridge interfaces, or network switching complexities.

How is it different from Revolut or Coinbase? You control your private keys! How is it different from Metamask? You can spend crypto as easily as fiat, without worrying about which chain your USDC is on.

Simply put, this is the change that comes when DeFi protocols realize that average users don't want to manually bridge assets across chains or calculate Gas fees. They just want a card they can swipe.

One of the Three Titans

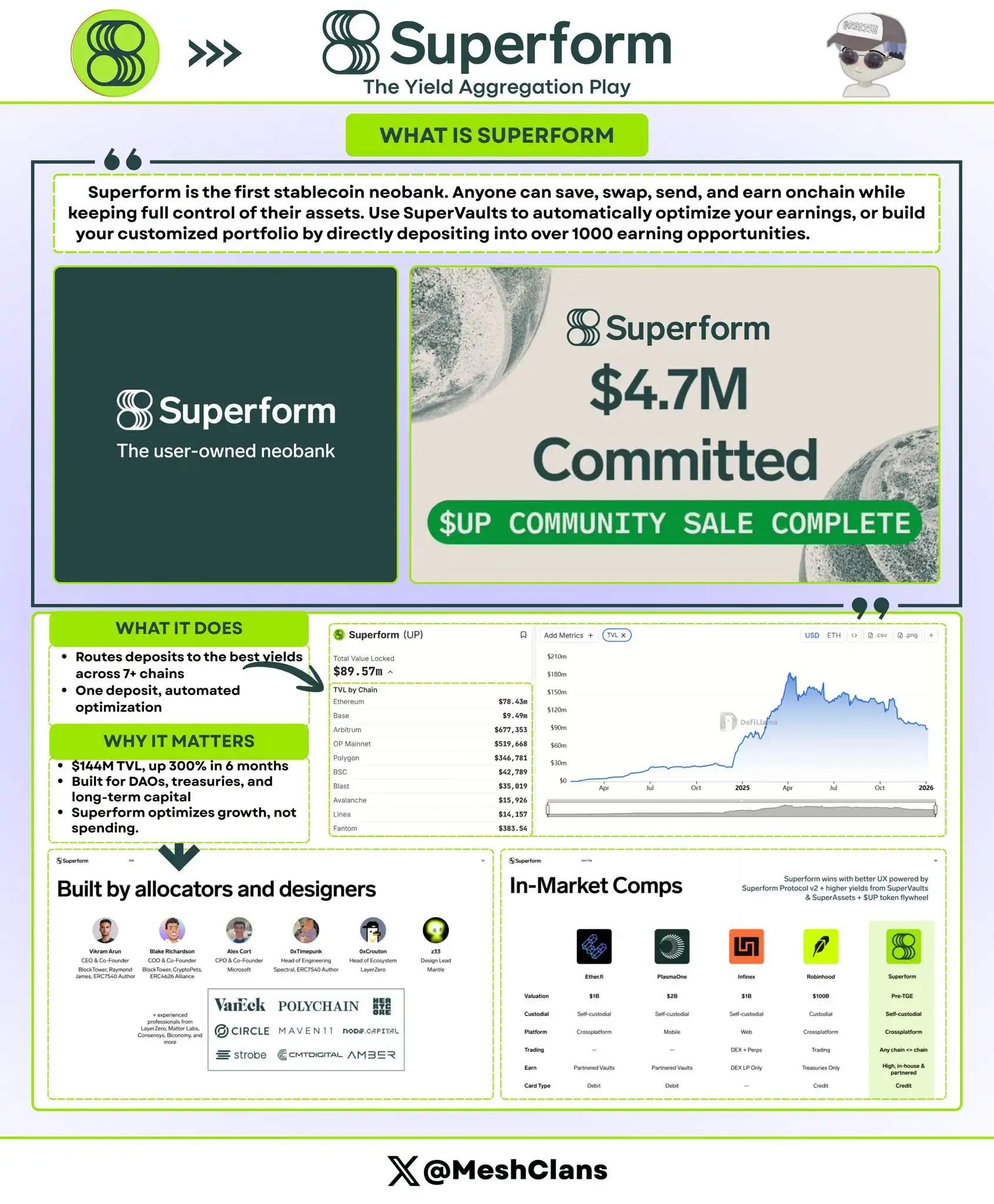

@superformxyz caught my attention around mid-2025, when their primary target users were still institutional investors. Now, they position themselves as the "savings account" for onchain finance.

What are they doing?

Superform's core function is to automatically route your funds to high-yield vaults across 7+ chains. You simply deposit USDC, and Superform finds the best Annual Percentage Yield (APY) for you, whether it's from Aave, Curve, or some protocol-specific yield farm you've never even heard of.

Data Performance (as of end-2025):

- Total Value Locked (TVL): $144 million (300% growth in 6 months)

- Funding: $12.9 million total across Seed, Strategic, and Public rounds

- Fully Diluted Valuation (FDV): ~$90 million

Why is it important?

Superform's SuperVaults v2 launch in Q4 2025 was a game-changer. The "Cross-Chain Instant Deposit" feature allows users to deposit funds on Base, and Superform deploys them to a vault on Arbitrum in the background. No manual bridging, no waiting for confirmations, everything happens automatically.

Previously, yield optimization required significant expertise—tracking APYs, calculating Gas fees, timing bridges. Superform simplifies this to a "one-click" operation.

What makes it different?

Superform isn't trying to be your spending app; it's positioned as the savings backend layer for onchain finance. Unlike Tria's focus on capital flow efficiency, Superform is more concerned with efficient capital growth.

Additionally, Superform offers institutional-grade security (audited by Zellic and Omniscia), making it a "safe money" option. Many DAOs and protocol treasuries park capital here, which speaks volumes about the market's trust.

Veera's Trajectory is Fascinating

@On_Veera's growth path is very interesting. Starting as a rewards browser (similar to the Brave model), it evolved into a full financial operating system. It now boasts over 4 million users, active in emerging markets largely overlooked by Western VCs.

Basic Info:

- User Base: Over 4 million users across 108 countries

- Funding: $6 million Seed round from Ayon Capital in February 2024

- Core Markets: India, Southeast Asia, Africa

Product Evolution:

The initial Veera was just a "browse-to-earn crypto" rewards browser. It has now developed into:

- Browser Rewards → Wallet → Staking/Yield → Payment Card (Q1 2026) → Credit Features (Q1 2026)

Their Q2 2026 roadmap also includes a physical debit card and desktop wallet. Their product iteration speed is rapid.

Why does Veera have the makings of a giant?

Traditional banks won't serve users in remote India with only $50 in savings, and companies like Revolut rarely enter most of Africa. Veera solves the distribution problem by meeting user needs: mobile-first, low-balance friendly, and deeply integrated into the daily browsing experience.

Their growth logic is clever: users earn small crypto rewards for normal browsing, then discover they can earn yield through staking or spend via a payment card. The onboarding has almost no friction because users immediately perceive value.

Competitive Angle:

Veera isn't competing with Coinbase; it's competing with local fintechs like Paytm, MTN Mobile Money, and M-Pesa in markets where crypto adoption is rapidly growing but infrastructure is weak.

4 million users in these markets is what most crypto projects dream of. If they execute the physical card launch in Q2, they could scale like Paytm did.

Tria: The Winner in Chain Abstraction

@useTria is one project I actually downloaded and tested in Beta. Its user experience is different and refreshing.

Current Data (Early 2026):

- Active Users: Over 150,000

- Beta Transaction Volume: Over $20 million

- Daily Spending: Broke $1 million in November 2025

- Annualized Run Rate (ARR): ~$20 million

- Funding: $12 million raised in October 2025

- Fully Diluted Valuation (FDV): Valuation between $100M - $200M

How does it work?

Tria's "Unchained" infrastructure makes blockchain complexity completely invisible. Users maintain one unified balance across multiple chains. When you spend, Tria's "BestPath" engine:

- Checks your assets on various chains;

- Finds the best liquidity path;

- Executes the swap or cross-chain operation in the background;

- Completes the payment in seconds.

The user experience is seamless: open the app, tap to pay, done. All blockchain complexity is automated away.

Tria's Christmas campaign, Triasmas (their holiday loyalty program), proved that native crypto rewards can rival traditional credit card points. People actually used it for daily spending and got cashback. This shows Tria has found product-market fit.

Why is it important?

Chain abstraction is key to making crypto usable for normal people. Other solutions always make users think about networks, Gas fees, bridges. Tria removes that friction entirely.

$1 million in daily spending validates real consumer demand. This isn't yield farming or speculation; it's real spending—coffee, groceries, bills. Over 150k users and $20M ARR suggest this is more than just beta hype.

Positioning:

In the current crypto landscape, Tria is the closest thing to a traditional bank account. It wins on speed and simplicity, not by flaunting blockchain complexity. This makes it the best candidate for mainstream users, though power users might want more control.

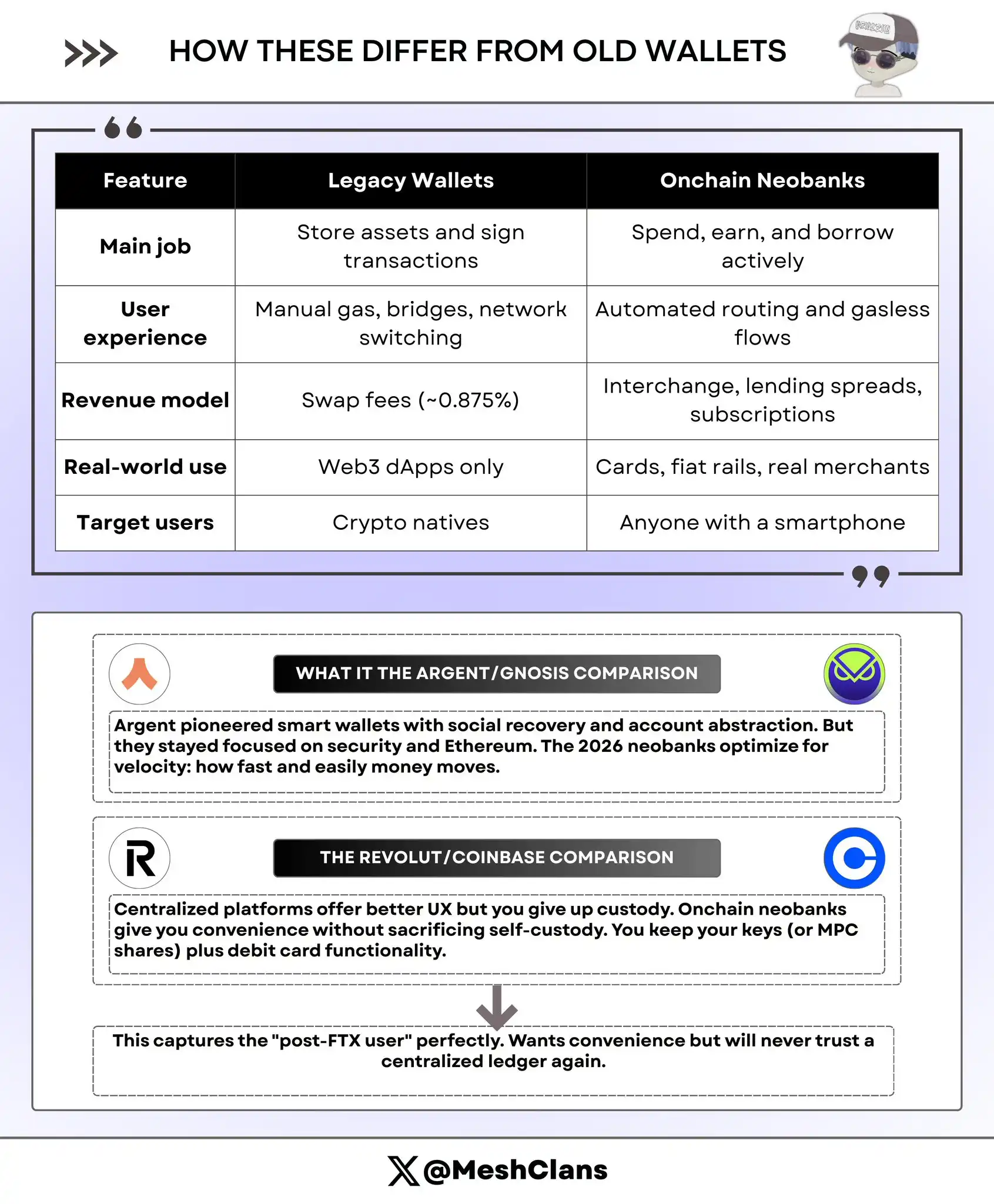

Comparison with Argent and Gnosis:

Argent pioneered smart wallets with social recovery and account abstraction. However, Argent has remained security-focused and Ethereum-centric. The 2026 onchain neobanks focus on the speed and ease of moving money—how to make capital flow faster and easier.

Comparison with Revolut and Coinbase:

Centralized platforms (like Revolut, Coinbase) offer better UX but require sacrificing custody. Onchain neobanks offer the same convenience without sacrificing self-custody. Users keep their keys (or MPC shares) while having debit card functionality.

Beyond the Three Titans

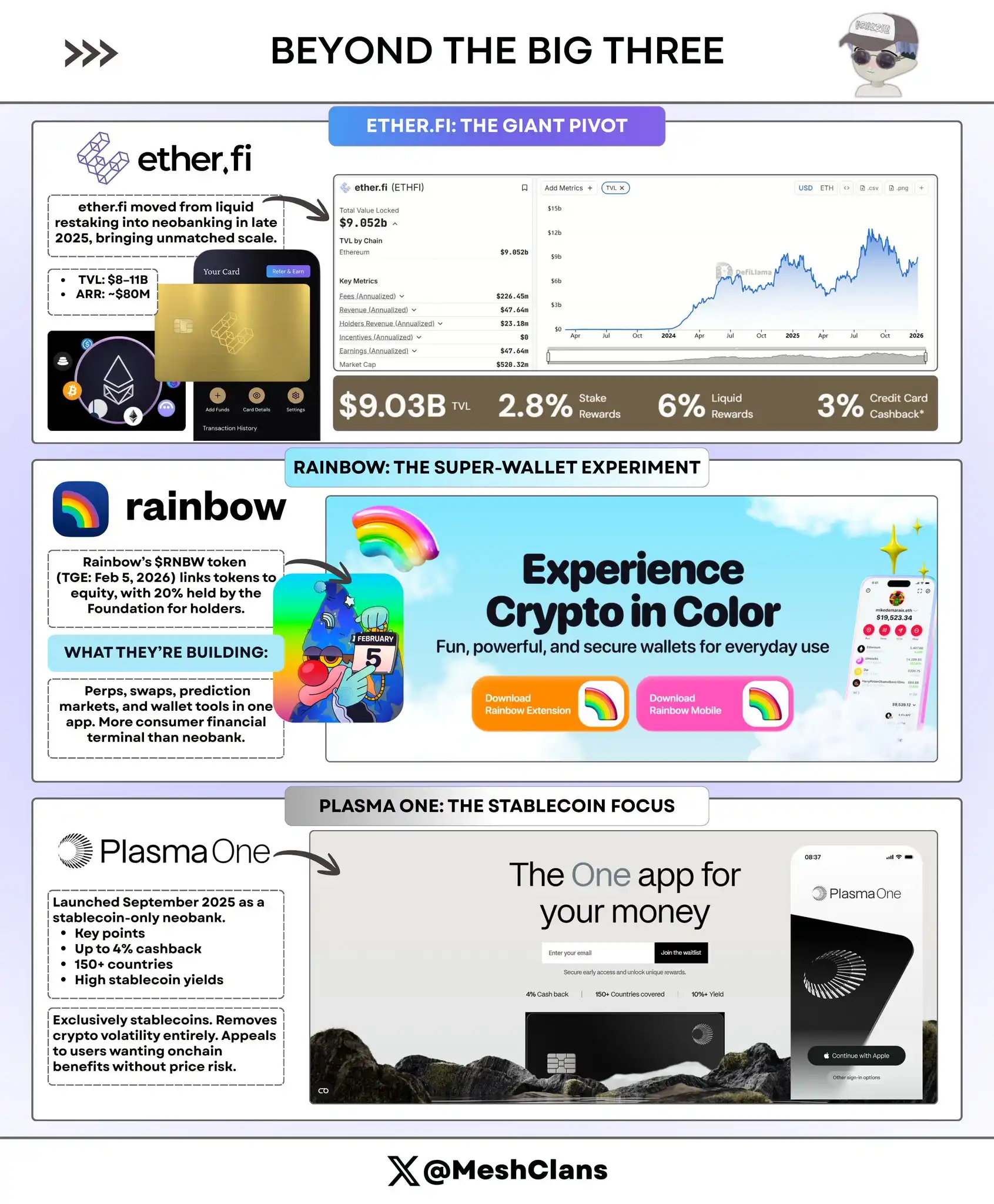

ether.fi: The Titan's Pivot

@ether_fi started as a liquid restaking protocol, but by late 2025, it pivoted heavily into the onchain banking space, on a completely different scale.

Data Performance (Late 2025 / Early 2026):

- Total Value Locked (TVL): $8B - $11B

- Annualized Run Rate (ARR): $80 million

- Product: Cash Card, 3% crypto cashback

Innovation Highlight:

ether.fi's Cash Card lets users borrow against their restaked ETH (eETH) at ~4% APR without unlocking staked assets. This means users continue earning restaking rewards while accessing liquidity for spending.

This model cleanly solves the liquidity problem for yield farmers.

With $8B-$11B TVL, ether.fi is the "Chase Bank" of onchain neobanks. Its scale and liquidity can support serious consumer lending, making it a force in the industry.

Challenge:

Pivoting from DeFi infra to consumer banking isn't easy. ether.fi has capital but lacks Tria's UX polish or Veera's distribution. Execution matters more than TVL here.

Rainbow: The Super-App Experiment

Rainbow is launching its $RNBW token (TGE) on February 5, 2026, with an interesting structure: the Rainbow Foundation will hold 20% of the company's equity to reward token holders.

What are they building?

Rainbow is developing an all-in-one mobile interface including Perps, Swaps, Prediction Markets, and wallet functions. It's more of a consumer "Bloomberg Terminal" than a traditional neobank.

Equity-Token Link:

This equity-linked token structure is an experiment. If successful, other projects may rush to copy it. If it fails, it could be a classic case of over-promising.

Risk:

The risk of feature bloat is high. Trying to do everything might make the product unfocused, struggling to compete with best-in-class single-function apps. The upcoming February TGE will reveal if the market values the equity-link model or sees it as a marketing gimmick.

Plasma One: The Stablecoin-First Contender

Plasma One launched in September 2025, positioning itself as the "first stablecoin-native neobank".

Product Features:

- 4% cashback

- Available in 150+ countries

- High yield on stablecoin balances

Unique Positioning:

Plasma One focuses solely on stablecoins, removing crypto price volatility entirely. This appeals to users who want onchain benefits without price risk.

Core Issue:

The "first stablecoin-native" positioning is more of a marketing angle than a real moat. Any competitor can easily add a stablecoin-only mode. Success will come down to execution, not positioning.

Risks Worth Watching

Sustainability of Yields

Let's be real. High returns like Veera's browser rewards and 15% APYs are mostly subsidized by VC funding and token emissions.

Remember the 20% UST rates from Anchor? We all know how that ended—with the collapse of the entire Terra ecosystem.

The 2026 onchain neobank space faces a core question: what happens when the subsidies run out?

Sustainable onchain banks need real revenue sources: card transaction fees, lending spreads, subscription models. Projects inflating APY by burning token reserves might not survive until the next funding round.

Tria's $20M ARR provides a template: real revenue from real transactions, not token incentives.

Watch for: Projects being transparent about revenue sources, clearly distinguishing organic income from token subsidies. If they aren't transparent, that says something.

Regulatory Uncertainty

2025 discussions around the Stablecoin Act created much uncertainty. If US regulations require self-custody "banks" to implement KYC, the industry could see a major split:

- Compliant Hybrids (with institutional backing and regulatory infrastructure) will thrive in the US market.

- Pure Self-Custody Apps (like Tria, Superform) might be forced to geo-block US users or add compliance layers, potentially breaking their core value proposition.

Europe's MiCA regulations in 2024-2025 provided some clarity. Clear rules help legitimate projects but raise the barrier to entry.

Key Question: Can these protocols adapt to regulation while keeping their decentralized core intact?

The Metamask Threat

Metamask has 30 million MAUs and immense brand recognition. For Veera or Tria to reach 10 million users, they need to be significantly better than Metamask, not just marginally.

Chain abstraction is a feature, not a moat. Metamask could launch gasless transactions and unified balances within six months. If that happens, the competitive edge of onchain banks shrinks to payment cards and yield optimization.

Defenses:

- Tria's Play: Payment networks (hard to copy quickly).

- Superform's Play: Yield optimization algorithms (more sustainable).

- Veera's Play: Focus on markets Metamask ignores (geographic moat).

Time will tell who wins.

2026 Outlook

Most Likely to Hit 1M DAU First: Tria

Tria's UX is already polished. $1M daily spending and 150k+ users show strong consumer demand. If the rumored Q1 Mastercard payment network integration happens, Tria could run away with it.

Chain abstraction matters most to mainstream users who don't care about blockchain. They just want to buy coffee with crypto, not understand the tech.

$20M ARR suggests Tria has found real product-market fit, not just beta hype.

Safest for Sustained Growth: Superform

Yield optimization survives every market cycle. Even if consumer-facing neobanks struggle, institutional users (DAOs, protocols, treasuries) will still park capital in optimized vaults.

Superform's focus on "safe money" means lower volatility and more stable growth. Less "sexy," but highly sustainable.

Most Likely Dark Horse: Veera

4 million users in India and Southeast Asia is a distribution most crypto projects can't touch. If Veera executes the physical card launch in Q2, it could become the "Paytm" of crypto.

It achieved massive scale in markets Western VCs largely ignore. The upside is huge.

Most Likely Acquisition Target: ether.fi

$8B-$11B TVL and $80M ARR make ether.fi a prime acquisition target for Coinbase, Kraken, or TradFi banks looking to enter crypto. Expect consolidation by end-2026, as giants choose to buy proven infrastructure rather than build from scratch.

What These Onchain Banks Share

These three projects are essentially building a new kind of financial super-app: combining DeFi's power with everyday banking UX, all self-custodied and onchain.

Common DNA:

- Non-Custodial Core: Users control keys and assets, avoiding freeze/confiscation risks of centralized platforms.

- Unified Operating System: Yield, spend, trade across chains in one app, vs. traditional wallets requiring constant dApp switching.

- Focus on Mass Adoption: Replaced "read 47 docs on liquidity pools" with "earn more, do less".

- Timing is Right: These projects emerged in late 2025, marking the next phase post-"DeFi 2.0". Better L2s, account abstraction, and real-world spending needs converged.

Different Paths, Same Goal

- Superform: Yield optimization & institutional-grade infra

- Veera: Global credit & yield OS

- Tria: Consumer payments & spending

Together, these projects are building a new category. People are starting to see "onchain neobanks" as an industry, not just individual projects. This narrative momentum matters for funding, partnerships, and market mindshare.

Final Take

Self-custody is becoming convenient. These three projects represent different paths to solving the same problem: making crypto as easy as traditional banking, while keeping self-custody at the core.

Who will dominate?

Likely, all three will thrive, serving different user segments. The crypto economy is vast enough for multiple financial operating systems.

The real challenge: can they cross the chasm from crypto-natives to mainstream adoption?

Late 2025 data suggests yes:

- Tria: $20M ARR

- Veera: 4M users

- Superform: $1.44B TVL

These numbers suggest sustainable growth, not just speculative hype.

2026 will be the year this space proves its potential.