Original|Odaily Planet Daily (@OdailyChina)

Author|Wenser(@wenser 2010)

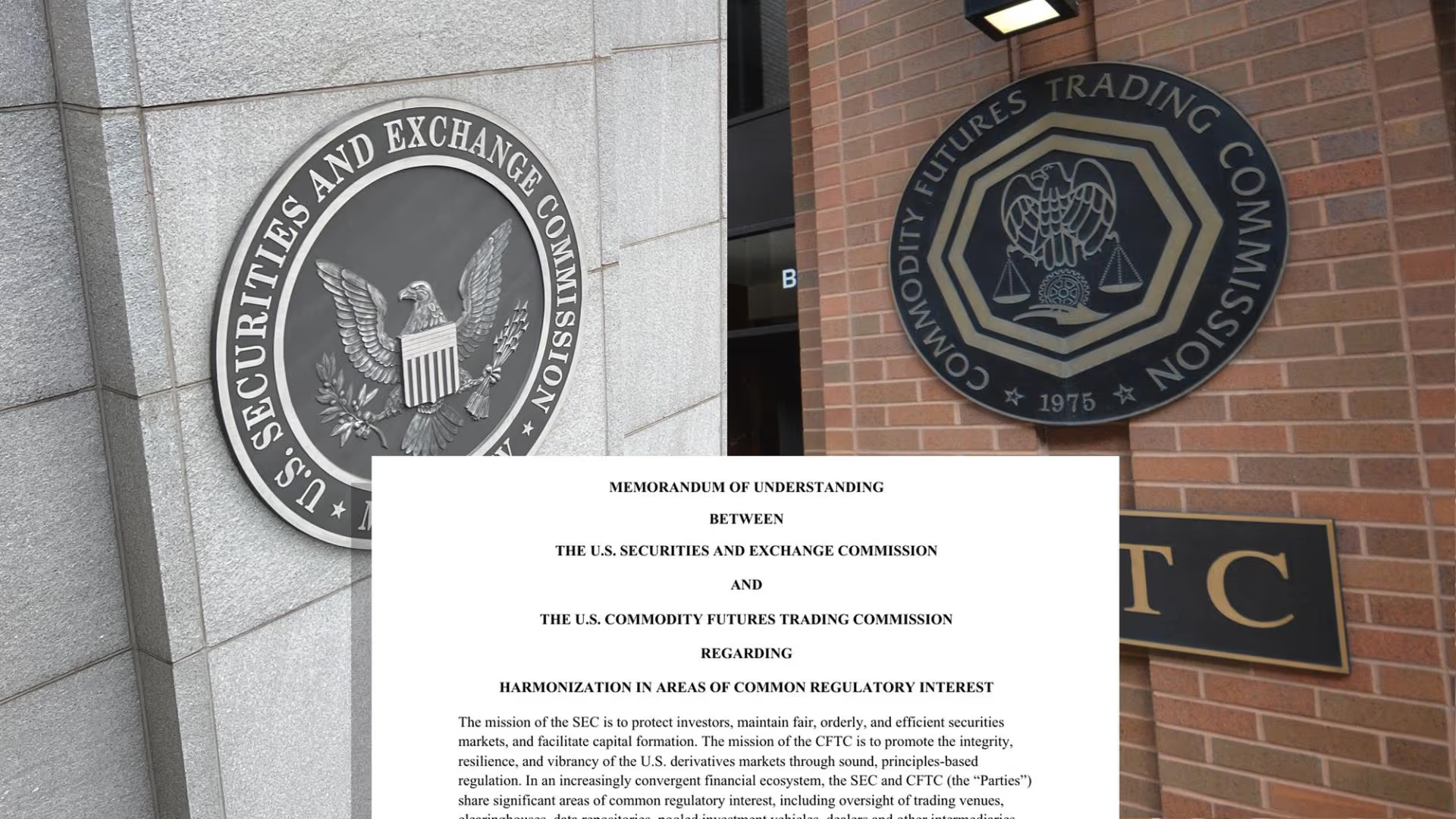

On March 17 local time, the U.S. SEC released its 30th press release this year. In this explanatory document of less than 1,000 words, SEC Chairman Paul Atkins and CFTC Chairman Michael Salinger jointly removed the tight constraint that has been placed on the entire crypto industry for the first time: most crypto assets are not securities but are classified as "digital commodities, digital collectibles, digital tools, stablecoins."

On March 11 this year, the two agencies jointly signed a Memorandum of Understanding (MOU), indicating that they would "clarify product definitions through joint interpretations and rulemaking, and develop modern clearing, margin, and collateral frameworks," among other measures. Now, it appears that this latest explanatory document is the best proof of the two agencies联手 (joining forces) to loosen restrictions on the cryptocurrency market.

It can be foreseen that the impact of this document clarifying the classification of crypto assets goes far beyond this. Subsequent intensive crypto IPOs, airdrops, DeFi mining, staking, and wrapped assets will all usher in new development opportunities. As for whether behind this seemingly convenient door lies an influx of institutional liquidity, countless retail investors, or the hidden scythe of the regulatory machine, perhaps only time will tell.

Detailed Analysis of the 5 Classifications in the SEC Explanatory Document: Most Crypto Assets Are Not Securities

According to the "Fact Sheet" document released by the U.S. SEC, it provides clear regulations for the classification of 5 types of crypto assets:

- Digital Commodities — Non-Securities — Their value is intrinsically linked to the programmed operation of a "functional" crypto system and supply-demand dynamics, rather than arising from the expectation of profits from the core managerial efforts of others.

- Digital Collectibles — Non-Securities — Designed specifically for collection or use, they may represent or convey rights to digital expressions or references of artwork, music, videos, trading cards, game items, or internet memes, characters, current events, trends, etc.

- Digital Tools — Non-Securities — Crypto assets with practical functions, such as memberships, tickets, vouchers, property deeds, or identity identifiers.

- Stablecoins — Stablecoins meeting the definition of the "GENIUS Act" are non-securities, and stablecoin issuers are explicitly prohibited from paying interest or returns to holders in any form (cash, tokens, or other consideration).

- Digital Securities (or "Tokenized Securities") — Are Securities — Financial instruments listed in the definition of "security" presented or represented in the form of crypto assets, whose ownership records are maintained wholly or partly on one or more crypto networks.

In the subsequent more detailed 68-page explanatory document, the U.S. SEC also provided its own definitions for airdrops, DeFi mining, staking, and wrapped assets:

- DeFi Mining (Protocol Mining): Does not constitute a securities offering. (Odaily Planet Daily Note: There is no structure relying on profits from the core managerial efforts of others.)

- Staking: Does not constitute a securities offering. (Odaily Planet Daily Note: If the underlying asset is a digital security, or a non-security asset but has been incorporated into an investment contract, the staking certificate is then classified as a security.)

- Wrapped Assets: Are not securities. (Odaily Planet Daily Note: The custodian of wrapped assets must not misappropriate the underlying assets, and cannot transfer, lend, stake, re-stake, or use them for any other purpose.)

- Airdropped Assets: Are not securities. (Odaily Planet Daily Note: If the issuer proactively announces an airdrop plan and requires users to complete specific tasks to receive the airdrop, creating a clear consideration relationship through active labor in exchange for assets, it may constitute an investment contract risk.)

Simply put, what are not considered securities (stocks) include: Digital commodities, like gold and oil, are tangible things that can be used, with prices determined by market supply and demand. Bitcoin and Ethereum fall into this category; Digital collectibles, like stamp collecting or buying paintings, are for collection or appreciation. Popular online NFT images, game items (including Meme coins) belong to this category; Digital tools, like membership cards, tickets, qualifications, are obtained for use, not for speculation; Stablecoins. Like digital "shopping vouchers," specifically used for payment, with stable value and no volatility. But there is a hard rule: Issuers cannot pay interest to holders. Once interest is paid, the nature changes and it might be considered a stock.

Digital securities, these are essentially stocks, just digitally repackaged, so they remain within the scope of stocks.

Mining, using computers to help the network keep accounts and earn coins, is not issuing stocks; Staking, locking up coins to help maintain network security and earn some rewards, is not issuing stocks. But if the locked coins are inherently stock-like, that's a different story. Wrapping, converting one coin into a form usable on another network, like changing change, is not issuing stocks. Airdrops, platforms giving away coins for free, are not issuing stocks. But if the platform requires you to complete tasks first, then it becomes more like an "employment relationship," and the nature might be different.

It is worth noting that the document acknowledges for the first time that an "investment contract" can be terminated. This also means that even if a token was initially issued through financing (ICO), as long as it later achieves decentralization or acquires utility attributes, it can cease to be considered a security.

Although these are currently still at the "explanatory document" level and not yet specific statutory law条文 (legal provisions), they have initially clarified the previously chaotic crypto asset classification system, providing some evidential support for future regulation and enforcement. Subsequently, the potential impact of this document may bring market benefits in the following aspects.

Non-Security Classification for Crypto Assets Released, 3 Potential Benefits May Drive Market Recovery

Currently, the explanatory document jointly issued by the U.S. SEC and CFTC seems more like a "New Crypto Development Manifesto," which will directly promote the explosive development of prediction markets, crypto IPOs, and DeFi protocols.

New Interpretation Clears Obstacles for Polymarket Airdrop, Crypto IPOs and Token Launches to Proceed Together

After the release of the latest U.S. SEC crypto asset interpretation, crypto KOL @harrysew posted that this framework might "give the green light" to the POLY token launch and airdrop, significantly reducing regulatory uncertainty. On one hand, Polymarket can leverage its real-time data prediction function, with the POLY token becoming a utility token; on the other hand, mining, staking, and wrapping assets can also proceed smoothly, further expanding the application scenarios of the POLY token.

Thereby, Polymarket is expected to grow from an "illegal gambling den" previously denounced by local regulators into a "global truth machine" that predicts the future and verifies the direction of event development.

New Interpretation Facilitates Crypto Exchange IPOs in the US, Platform Tokens No Longer Negative Assets

For exchanges like OKX and Kraken that aspire to conduct crypto IPOs in the U.S. stock market, this explanatory document is like receiving a pillow when drowsy.

Previously, exchanges were often limited by their资产负债表 (balance sheet) constraints, unable to clearly define and conduct compliant audits on包括 (including) platform tokens and assets held by the platform, because they feared regulators would label "cryptocurrencies as stocks."

Now, with this explanatory document, the audit obstacles before an IPO have been swept away at once, and the former platform tokens are no longer obstacles in front of the IPO.

New Interpretation Benefits DeFi Protocol Development, Massive Liquidity May Pour In

For many DeFi protocols, this explanatory document is also a "get-out-of-jail-free card."

Previously, many DeFi protocols, including Uniswap, have received "regulatory subpoenas" from the U.S. SEC. Now, staking, wrapped assets, and spot holdings are explicitly not securities. In view of this, various institutional funds can also enter and use DeFi protocols in a compliant, large-capacity manner.

Of course, regarding liquidity mining, governance tokens promising returns, and yield aggregation protocols, asset management giants like BlackRock and Fidelity still cannot seamlessly enter.

Conclusion: The Era of Crypto Wild West Ends, Market Accelerates into the "Great Co-optation Era"

Of course, just like the two sides of a coin, as the legal boundaries defined by the U.S. SEC and CFTC become clearer, the "ambiguity红利 (dividends)" and "gray areas" within the cryptocurrency industry will also face清算 (liquidation/settling accounts) simultaneously. To some extent, the crypto industry, like the banking and credit industries before it, is gradually being co-opted by the regulatory system and compliance framework. New crypto projects need to invest more human and material resources in regulatory compliance, airdrop distribution, staking design, etc., which to some extent will also affect crypto innovation.

But无论如何 (in any case), for the current liquidity-starved crypto market, every detailed explanation from regulators is an invitation ticket to the mainstream financial field. Although the ideal of decentralization is moving further away from us, more importantly, the connection between the crypto industry and the mainstream population is becoming closer, so its vitality and living conditions can be guaranteed to a certain extent.

Between disappearing in silent high pressure and living with restrictions, I think most people would choose the latter.