Since the outbreak of the US-Iran war, as two commodities highly correlated with geopolitics, crude oil and gold have shown completely different trends: the former has risen sharply, while the latter has fallen slightly. Why is this?

As a natural currency, gold has three major hedging functions: hedging against geopolitical risks, inflation risks, and US dollar risks. The price of gold is simultaneously influenced by these three forces, thus playing varying degrees of hedging roles at different stages.

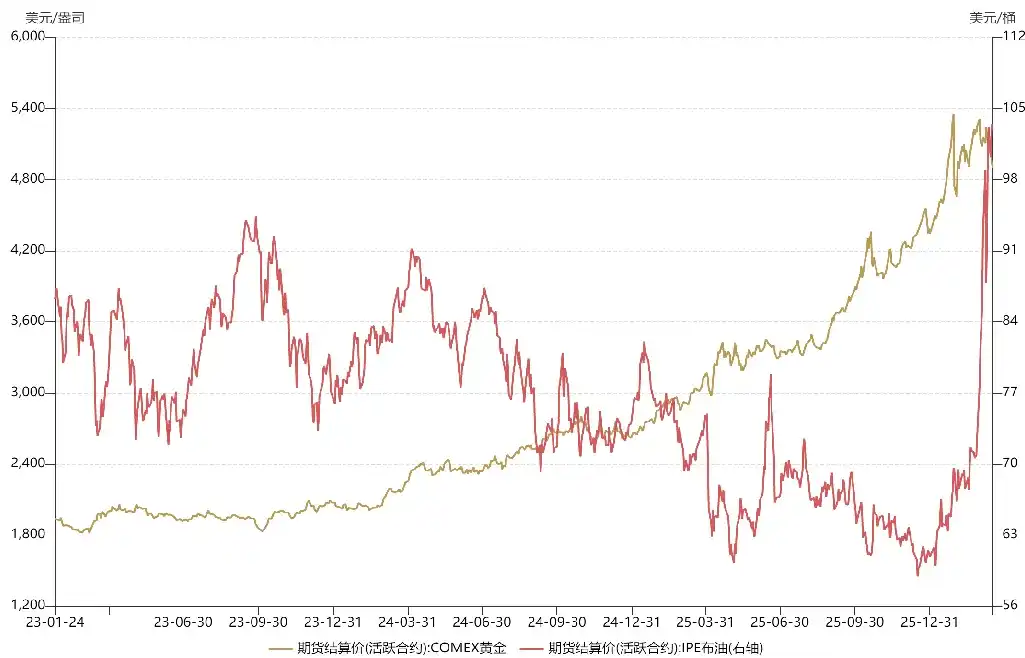

Since the end of 2023, precious metals have experienced a super bull market, with the price of gold soaring from $1,800 to over $5,000. The reason for such strong upward momentum is that gold simultaneously served as a hedge against geopolitical risks, inflation risks, and US dollar risks.

In October 2023, on top of the Russia-Ukraine war, large-scale conflicts broke out between Israel and Palestine, plunging the Middle East into turmoil. In 2024, the Red Sea crisis erupted, and the Bab el-Mandeb Strait was blockaded. In 2025, Trump took office, and the international order became precarious. These are all manifestations of chaotic geopolitical situations, providing strong support for the price of gold.

On the other hand, in 2023, the US economy shifted from overheating to stagflation. By 2024, influenced by political factors, the Federal Reserve boldly initiated an interest rate-cutting cycle before inflation issue was fully resolved, leading to a resurgence of US dollar liquidity. On one hand, there was mid-cycle easing, and on the other, the risk of secondary inflation. Gold simultaneously served as a hedge against US dollar risks and inflation risks, fueling the takeoff of gold prices.

With all three hedging functions in place, how could the price of gold not rise? In addition, benefiting from the Federal Reserve's easing cycle, both emerging and developed markets, whether in A-shares or US stocks, experienced a bull market.

Now, regarding oil prices, last year's average oil price was significantly lower than the previous year. This was because after Trump took office, he persuaded OPEC to significantly increase crude oil production in an attempt to force Russia to make concessions at the negotiating table. This strategy initially worked, with Putin repeatedly softening his stance on peace talks. If not for the US-Iran war, it was expected that Russia and Ukraine would sign a ceasefire agreement in the first half of this year.

Since the outbreak of the Middle East war, the prices of gold and oil have experienced multiple fluctuations, with their trends diverging due to different causes.

For gold, in mid-to-late January (half a month before the war), as the probability of a US-Iran conflict continued to rise, the price of gold increased, reflecting its geopolitical hedging attribute. According to the market's mainstream expectations at the time, this conflict might be similar to last year's "Midnight Hammer" operation, with a short duration, making it more of a temporary trend.

After the US carried out a "decapitation" strike on Iran, the price of gold rebounded briefly but soon plummeted. This was because the main force shifted from gold to crude oil. Due to the excessive concentration of gold holdings earlier, the main funds chose to sell gold to obtain liquidity for going long on crude oil. In other words, the "position switching" from gold to crude oil led to a fall in gold and a rise in oil.

On the other hand, as overseas markets began to price in a prolonged US-Iran war, risk assets such as US stocks came under pressure, triggering a wave of redemptions. The US financial market faced a liquidity crisis, and as an asset with liquidity second only to cash, gold was heavily sold. In other words, the selling pressure on gold in early March was not because international investors were bearish on gold but rather a self-preservation strategy amid the liquidity crisis.

If it were just a liquidity crisis, the price of gold would often form a "deep V" trend, providing buying opportunities. However, the more troublesome part came later. Since mid-March, overseas expectations for the US-Iran conflict have become more pessimistic, with concerns not only about the potential long-term blockade of the strait but also about the possibility of warring parties launching large-scale attacks on each other's energy facilities. This would keep oil prices at relatively high levels for an extended period, dealing a devastating blow to the global economy and even causing the collapse of the international order. In such a scenario, the Federal Reserve might delay its interest rate-cutting pace or even restart a rate-hiking cycle as it did in 2022. Based on this expectation, the price of gold plummeted, with the extent of the correction breaking the highest record in recent years.

In other words, gold's geopolitical hedging function is still at play, but the current sharp decline in gold prices is driven by expectations of a reversal in the Federal Reserve's monetary policy. The US dollar anti-hedging attribute of gold has overshadowed its geopolitical and inflation hedging attributes, becoming its main driver. Compared to previous declines, the fundamentals of gold have changed. It is no longer a liquidity crisis or profit-taking but rather overseas concerns about the tightening of the Federal Reserve's monetary policy. These concerns are also reflected in risk assets such as A-shares and US stocks, as no one is spared when disaster strikes.

Since the outbreak of the US-Iran war, oil prices have also experienced twists and turns. The reason for this volatility is that overseas investors' perception of geopolitics has deviated. After the "decapitation" strike, oil prices continued to rise, reaching nearly $120 per barrel. However, in early March, as Trump hinted that "the war will end soon," the market began executing "TACO" trades, believing that the Iran situation might ease, and oil prices once plummeted by 30%. However, unlike tariff issues, the initiative in a geopolitical crisis does not lie with Trump. He cannot extricate himself easily while the strait is blockaded. Eventually, the market corrected its expectations for oil, and prices returned to an upward trend.

On geopolitical issues, the market sometimes makes misjudgments, but such pricing deviations are not necessarily bad. A drop in oil prices can反而 provide opportunities to add positions, making it easier for latecomers to enter the market.

Looking ahead, the trends of gold and oil prices will depend on the pace of the US-Iran conflict. If it evolves into a prolonged war like the Russia-Ukraine conflict, gold may lack配置 value in the first half of the year, and in the short term, one might focus on the energy chain. However, the situation could still reverse. The US-Iran war may reach a critical turning point, which will determine whether the Strait of Hormuz can be unblocked in the short term. It all depends on Trump's choice.