Author: Chloe, ChainCatcher

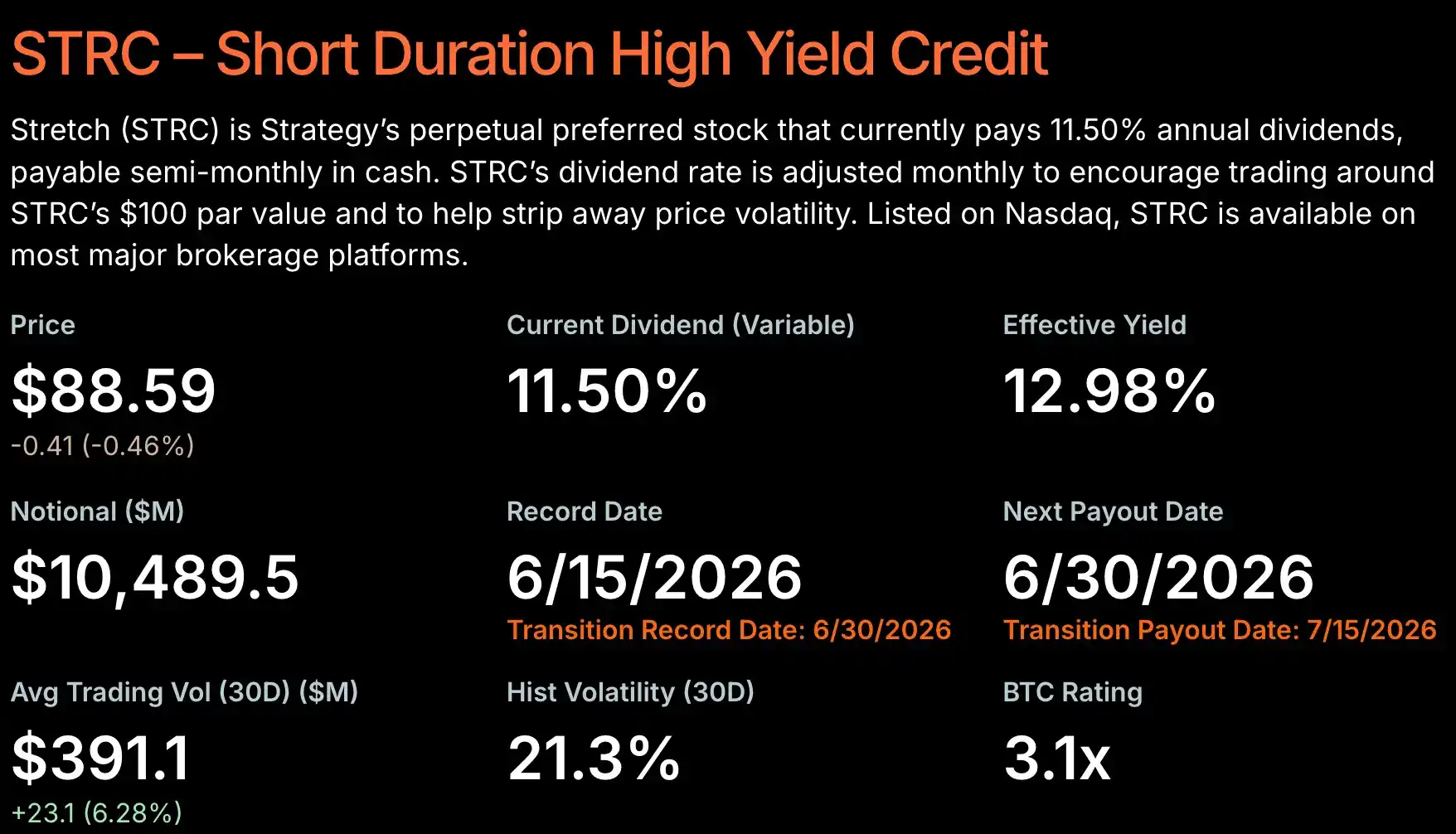

Since the launch of STRC by Strategy at the end of July 2025, Bitcoin has fallen by about 40%, nearly 50%. This preferred share, designed to "trade near a $100 par value," is now deeply discounted: hitting a record low of $82.53 during intraday trading last Thursday, and currently closing at only $88.59, still about 13% below par. As the discount widens, STRC's effective yield has been pushed above 12.9%, approaching 13%.

Jesse Myers, Bitcoin Strategy Head at The Smarter Web Company, commented on this, saying, "Strategy is fine," while economist Peter Schiff once again labeled the entire structure a "typical centralized Ponzi."

Thus, those old questions have resurfaced: Will Strategy be forced to sell Bitcoin? Is the flywheel upon which it relies for expansion actually a Ponzi scheme?

Is STRC a Mechanism Designed by AI?

To discuss STRC, we must first address a detail that is easily overlooked but has been reignited during this decline: this structure was conceived by Saylor through conversations with AI.

The controversy stems from a May CoinDesk interview clip that resurfaced on X. In the clip, Saylor admitted to using artificial intelligence extensively in developing Strategy's preferred share product. He said he used AI to design these things when creating Stretch; he couldn't have done it alone. He spent hours discussing and debating back and forth with the AI.

According to his account, he continuously presented the AI with various structural settings, testing whether atypical ideas were legally viable. When he proposed, "I want a preferred share that pays monthly dividends and trades stably at $100," the AI's response was: No one has ever done this in history, but it is completely legal and reasonable.

Interestingly, when STRC fell below par and the market began questioning whether this mechanism could hold, many foreign media outlets simply went back to ask AI—including ChatGPT, Grok, and Claude—whether STRC could return to $100.

Will Strategy Sell More Bitcoin?

Not long ago, Strategy sold 32 BTC, worth about $2.5 million, to meet dividend obligations. This amount is negligible compared to its overall Bitcoin reserves, but it proves one thing: when the financing efficiency led by STRC declines, cash obligations can indeed force limited Bitcoin sales.

More alarming is the freeze in buying momentum. Strategy's pace of increasing Bitcoin holdings has noticeably slowed: in April this year, it spent $2.54 billion in a single week to purchase 34,164 BTC; in May, it added another 24,869 BTC with approximately $2.01 billion. But by June, weekly purchases shrank to around $100 million. As of the week ending June 8th, it bought 1,550 BTC ($101 million); as of the week ending June 15th, it bought another 1,587 BTC ($100 million), bringing total holdings to 846,842 BTC.

Additionally, the widening discount not only pushed up the yield but also suspended the "at-the-market" offering mechanism (ATM, which involves selling new shares into the public market at prevailing market prices in batches to raise cash). This financing channel is a key link supporting the entire Bitcoin flywheel.

However, bulls are not buying this "death spiral" narrative. Jesse Myers believes this round of STRC selling looks more like leverage unwinding than a fundamental deterioration. He estimates that, if conditions remain unchanged, Strategy's current state is sufficient to cover STRC dividends for up to 32 years; and as long as Bitcoin appreciates by about 2% annually, this obligation can be covered indefinitely. Furthermore, the equity issuance tool itself hasn't disappeared. Even though ATM offerings are temporarily halted, Strategy still retains multiple backup financing options, including restarting MSTR common stock issuance and using cash reserves, with selling Bitcoin only as a last resort.

On the bear side, Schiff presents his classic script. He argues that if Saylor raises the yield to 13%, he will have to issue more MSTR at a larger discount to finance it; if he doesn't raise the yield, STRC's price will continue to fall. In his view, the only way to stop this death spiral is to cancel the dividends outright, but that would immediately crush STRC, dragging down MSTR and Bitcoin with it.

Is This Flywheel a Ponzi Scheme?

Schiff's accusation is straightforward: STRC is a "typical centralized Ponzi" because its operation depends on whether Strategy can continue raising new money through successive rounds of share issuance, or simply sell Bitcoin to fulfill its obligations. Even trader DonAlt publicly questioned why STRC's price action after breaking below par "trades like a Ponzi."

Strategy has not directly responded to such accusations, continuing to position STRC as a preferred share backed by its Bitcoin DAT strategy. A more concrete action was changing STRC's dividend payment from monthly to semi-monthly, meaning payouts twice a month.

The core argument from the opposing side is "leverage unwinding." Myers points out that the problem lies not in the structure itself, but in the fact that STRC traded around $99 to $100 for an extended period, enticing investors to take on heavy leverage. Many assumed the instrument would remain firmly above $95; once the price slipped, margin calls and forced liquidations amplified and accelerated this decline.

Analyst Scott Melker offers another perspective: the discount might instead attract yield-seeking buyers. Because STRC's dividend is calculated based on the $100 liquidation preference, not the market price. With an 11.5% dividend rate, someone buying at $90 effectively gets a yield of about 12.8%; someone buying at $85 gets about 13.5%. The deeper the discount, the higher the effective yield, which is itself an incentive.

So, the question of "whether it's a Ponzi" ultimately depends on which explanation the market believes. One narrative is that this mechanism inherently can only keep turning by continuously bringing in new money, with money from later entrants used to pay earlier entrants—a characteristic of a Ponzi scheme. The other narrative is: the instrument itself is fine; it's just that people previously thought it was stable and borrowed heavily to amplify their positions. When the price slid this time, these people were forced to sell at a loss, amplifying the decline—a one-time washout, not a problem with the instrument itself.

Semi-Monthly Dividends Officially Take Effect, Answers May Come in June?

Looking back at what was mentioned above, since this mechanism was designed by Saylor using AI, many foreign media outlets simply posed the same questions to AI: Can STRC return to $100, and what should Strategy do to restore market confidence? The common answer from ChatGPT, Grok, and Claude was, "Returning to $100 requires conditions."

ChatGPT believes returning to $100 is still possible, but requires stronger market confidence, sustainable dividend coverage, and a recovery in Bitcoin price—all three together. It emphasizes that the fastest path to repair is making investors believe again that dividends can be maintained without relying on selling assets. If more Bitcoin sales are needed later, confidence could worsen further.

Grok is the most reserved, bluntly stating, "Maybe, but it would be extremely difficult." In its view, the market is essentially asking: Can the engine that fuels this Bitcoin-buying machine still run? It believes a sustained Bitcoin rally would be the most effective catalyst; conversely, prolonged weakness would weigh on both STRC and MSTR.

Claude notes that preferred shares can often recover from a discount to par, but the prerequisite is that investors regain confidence in the issuer's ability to fulfill long-term obligations. "Recovery is possible, but the market needs to see evidence that this structure can operate even in adversity, not just when Bitcoin is rising."

So, is there a problem with this strategy? Whether it's bearish Schiff, bullish Myers, or top-tier AI models, they all point to the same decisive variable: Whether Strategy can continue fulfilling dividend obligations without selling Bitcoin.

The current flywheel hasn't stopped, but it's clearly slowing: ATM offerings are paused, Bitcoin buying speed has shrunk from tens of billions per week earlier this year to about $100 million per week in June; the sale of those 32 BTC further proves that when share issuance falters, the door for "selling Bitcoin to pay dividends" is already open. As for whether it's a Ponzi or a one-time leverage washout, it depends on whether STRC can return to par and what Strategy actually uses to pay dividends.

The most specific observation point falls on June 30th: that day, STRC's change to semi-monthly dividends officially takes effect. But the real focus is on the rule that automatically adjusts the dividend rate based on price: if the monthly average price is below $95, a rate increase is recommended; it only stops when it reaches above $99. Currently, it is mired below $95, almost guaranteeing another rate hike. The dividend rate has already climbed from 9% in August 2025 to 11.5%.

This is the core of Schiff's death spiral: the lower the price, the more the mechanism automatically pushes the dividend rate higher, creating a larger cash bill, which ultimately can only be filled by issuing more shares or selling more Bitcoin. Whether this mechanism is a "stabilizer" or an "accelerator," the answer lies in the coming price and rate movements.