Prediction markets are no longer just for fans to trade: now, teams themselves are starting to use them.

Take a simple example: a basketball club promises its head coach a $20 million bonus if the team makes the playoffs. This is a straightforward incentive—if the team wins enough games and enters the playoffs, the bonus is paid out.

But from a financial perspective, this promise is a huge liability. As long as the team makes the playoffs, the $20 million must be paid out, regardless of the team's annual revenue or financial condition.

To manage this risk, teams typically buy insurance. Brokers design policies and find insurance companies willing to underwrite them; insurers may then transfer part of the risk to reinsurers to avoid bearing the full exposure alone. The final price of this protection is negotiated privately among institutions. The premium implicitly reflects the probability of the team advancing, but this number is never made public—it exists only in the quotes given to the team.

Now, there is another solution for the same risk.

The team's probability of advancing is already being priced elsewhere. In prediction markets, this probability is traded daily, visible to everyone, and fluctuates in real time as expectations.

Instead of relying solely on private insurance quotes, the team can refer to the public market probability and use it to hedge part of the bonus risk.

How Sports Insurance Works

To understand how this system operates, let's look at what has happened in the sports industry over the past 20 years.

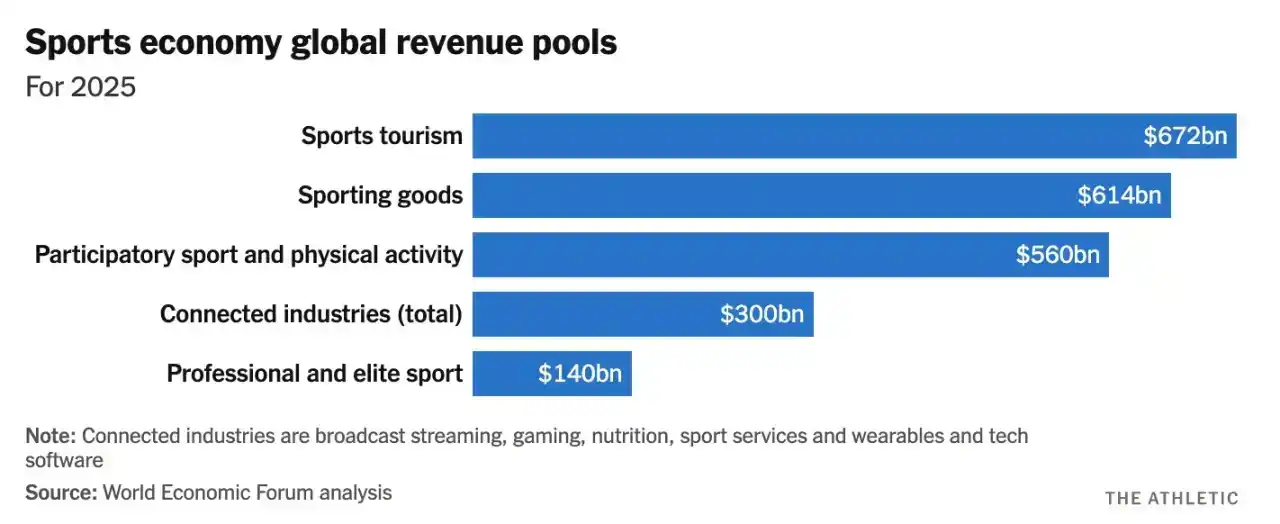

Today, professional sports generate nearly $560 billion in annual revenue, with a growth rate of about 7% per year. Revenue mainly comes from media rights, sponsorships, licensing, streaming platforms, and global business partnerships.

As revenue sources expand, the contracts tied to them have also grown significantly.

Today, team compensation is no longer just base season salaries but also includes numerous performance clauses linked to specific milestones. For example, if a team reaches the conference finals, the head coach may receive an additional $5 million bonus; players can earn extra pay if they achieve 1,000 rushing yards, 25 goals, or meet minimum playing time; some contracts even stipulate that bonuses increase further if the team advances deeper into the playoffs. These clauses are written into contracts as automatically triggered provisions—once conditions are met, the corresponding payments must be made.

Teams manage such exposures through insurance rather than passively bearing the risk and praying that incentives don't trigger en masse. They work with specialized brokers, who then find insurance companies willing to underwrite performance payouts; these insurers often transfer part of the exposure to reinsurers, dispersing the risk into a larger pool of capital. A simple bonus clause in a contract becomes an entire financial chain behind the scenes.

Insurers use a concept called "insurable value" to measure the scale of exposure—simply put, it refers to future income dependent on continuous performance, including salaries, incentives, endorsement income, etc., all of which can be affected if a player is unable to play.

The explosive growth of such exposure is evident in the data. For example, during the 2014 FIFA World Cup, the total insurable value of all participating teams was estimated at about $7.3 billion. But by the 2022 World Cup, this number soared to approximately $25 billion. In less than a decade, the financial value directly tied to performance more than tripled.

When so much revenue is tied to performance, uncertainty cannot be left to fate—it must be managed. An entire industry has thus been born. The global sports insurance and reinsurance market is currently estimated at about $9 billion and is expected to double by 2030. Its coverage ranges from event cancellations and athlete disabilities to sponsor guarantees and performance bonuses.

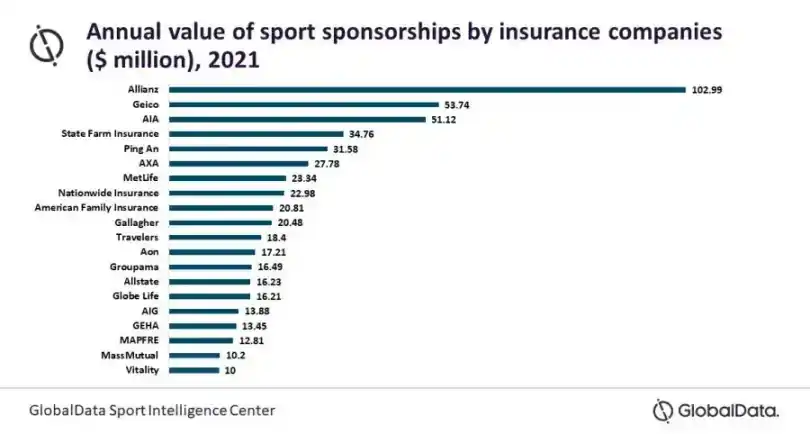

There are specialized brokers like Game Point Capital in the market, handling hundreds of millions of dollars in sports insurance annually; on the other side are underwriting entities like Lloyd's, which writes over $200 million in sports-related accident and health premiums each year, as well as large reinsurance companies that also underwrite catastrophes like hurricanes and aviation accidents. Because playoff bonuses, in pricing logic, fall into the same category of risk as storms and earthquakes.

Thus, the pricing process is cautious and private. Brokers negotiate with insurers, insurers negotiate with reinsurers, each using their own models to estimate the probability of milestone achievement and incorporating it into the premium. Teams only see the cost, not the underlying probability.

Why Private Reinsurance Is More Expensive

The price of sports insurance depends not only on the probability of the team achieving its goal but also on numerous external risks.

Ideally, if a team has a 10% probability of reaching a milestone, the premium should roughly reflect the 10% risk plus a small profit. But the reinsurance market is not an ideal world.

Reinsurers have limited capital. Every dollar invested in playoff bonus insurance is one less dollar available for businesses like hurricanes, aviation, catastrophe bonds, etc. They must continuously balance their portfolios across different regions and risk types. Therefore, when assessing sports risks, they consider: probability, available capital, outcome volatility, and correlation with existing risks.

Another constraint: the sports reinsurance market is highly concentrated. A few global institutions account for most of the underwriting capacity. Whether capacity is available and how much often depends on the reinsurer's own portfolio situation.

All these factors combined mean that the premium ultimately offered to the team includes not only the pure milestone probability but also many costs the team cannot see.

When Probability Is No Longer Hidden in a Black Box

Until now, outcome probability has been integral to every step: reinsurance modeling, broker negotiations, premium finalization. But this number has never been public.

Now imagine: what happens when this probability is priced in a public market? Prediction markets achieve this in a very interesting way.

Platforms like Kalshi have launched contracts for discrete real-world events, one category being sports outcomes. The contract poses a simple question: Will Team X make the playoffs?

Each contract eventually settles at $1 or $0. For example, if the price trades at $0.06, it means the market-implied probability is 6%.

This number isn't decided by an underwriting committee; it's determined by real buyers and sellers trading with real money, continuously adjusting based on their judgments of probability and price.

This mechanism is already in practical use. Game Point Capital, for instance, uses the Kalshi market to hedge basketball-related performance bonuses. In one case, a contract related to the playoffs traded on the exchange at about 6%, while the over-the-counter quote implied a price of about 12-13%. In another case, a second-round advancement contract traded on the exchange at nearly 2%, while the private reinsurance market price was 7-8%.

This is by no means a trivial difference. For a $20 million exposure, the gap between a 6% and 12% implied probability means a difference of millions of dollars in premium costs.

You might ask: these are just numbers clicked by traders—why take them seriously? Why are they more credible than insurance company models?

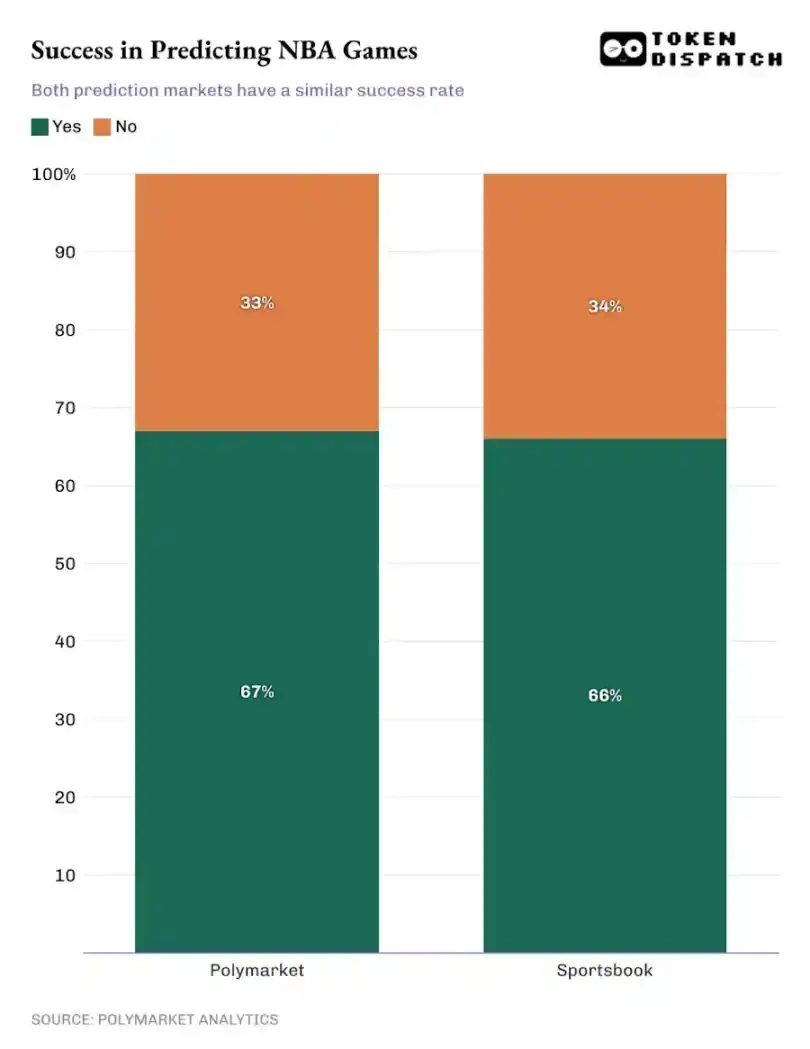

Extensive research shows that market-based odds are strong predictors of real outcomes. Decades of academic research on sports betting markets show that bookmaker odds are highly efficient predictors of game outcomes. More recently, a direct comparison between prediction markets and traditional sports betting: in a study of about 1,000 NBA games during the 2024–25 season, Polymarket's prediction accuracy was almost identical to that of traditional betting platforms.

In games where the market-implied probability exceeded 95%, both had accuracy rates above 90%.

The conclusion is even clearer for election markets. During the 2024 U.S. presidential election, a study comparing Polymarket with traditional polls showed that Polymarket was more accurate in predicting the final outcome, especially in swing states.

When thousands of people continuously update expectations in a real-time market, the collective probability often aligns remarkably closely with reality.

Prediction markets enable continuous price discovery. Any new information entering the system is continuously updated and priced, without waiting for the next review by an underwriting committee.

But to be truly practical, the market must be able to handle scale. In recent major events like the Super Bowl, Kalshi processed about $22 million in trades without significant price fluctuations. This indicates that both long and short sides of the market have real depth, sufficient to support large-scale hedging without impacting prices.

As these markets grow, a whole new set of permissionless financial tools is emerging around prediction markets.

For example, Kalshinomics analyzes event contracts like analysts analyze stocks and bonds, tracking how probabilities change over time, liquidity performance around major events, and whether prices deviate from fundamentals.

There are also platforms like PredictionIndex that aggregate and rank various prediction markets, allowing you to see total trading volume, contract types, blockchains, trading mechanisms, integrating the entire field into one place to visually showcase the market size.

When the probability of an outcome can be priced in real time and effectively absorb capital, it becomes a tool institutions can actually use. Teams can now directly use publicly traded probabilities to hedge performance bonuses, sponsors can hedge risks related to viewership targets, studios can hedge box office milestones. In principle, any income dependent on a specific and verifiable outcome can be transformed into a tradable contract.

Institutions no longer need to negotiate customized insurance contracts; the outcome itself can be publicly traded.

The final piece making this structure truly usable for institutions is identity. Traditional insurance works because counterparties are verified, contracts are enforceable, and exposures are auditable—something public markets have lacked.

Companies like Dflow are now binding real-world identities to trading behavior. This means market participants can be identified, screened, and linked to real entities, rather than being completely anonymous. This also makes contract settlement, exposure management, and incorporating positions into existing compliance frameworks possible.

In practical effect, it is beginning to look less like an ordinary trading venue and more like a functional insurance layer running directly on top of public probabilities.