Written by: BiBi News

In 1999, Elon Musk founded X.com with the ambition to reshape the online payment landscape. A few years later, X.com merged with Confinity and eventually evolved into today's PayPal. Years have passed, and Musk has returned to his roots with unfinished dreams.

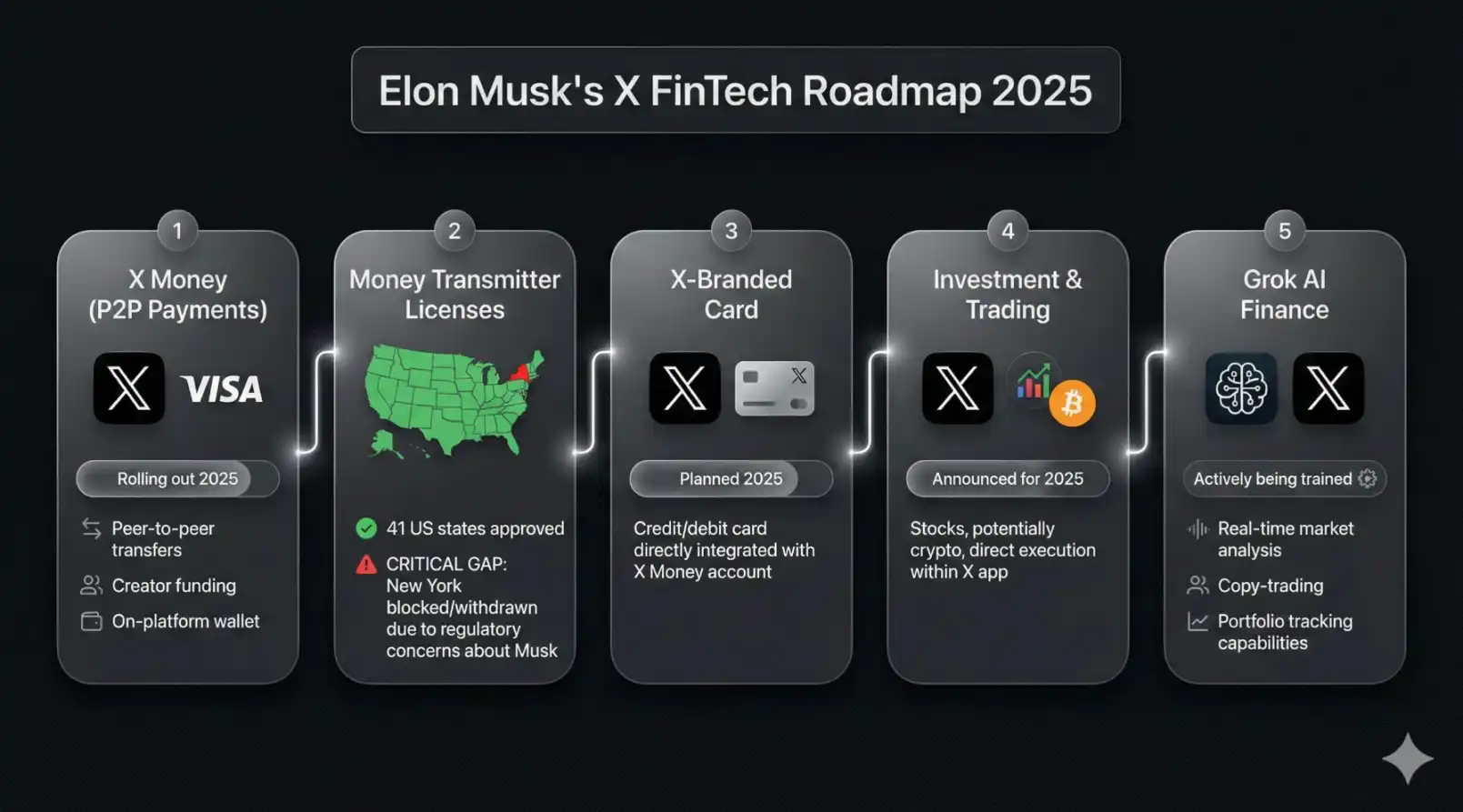

On March 10, 2026, Elon Musk personally announced on the X platform: X Money will begin early public access next month.

This one-line post sent ripples through the crypto community—the cryptocurrency Dogecoin surged in response, media outlets rushed to report, and the U.S. fintech industry began reassessing the competitive threat posed by this social media company.

X Money, a payment product that has been brewing internally for years, is now in the final sprint toward its public debut. But behind the hype, a more fundamental question remains unanswered: Is X Money a genuine financial revolution or another Musk-style narrative marketing stunt?

Musk's Everything App Strategy

X Money did not emerge out of thin air. Shortly after acquiring Twitter, Musk publicly expressed his desire to create an "Everything App" (super app). The goal was to emulate China's WeChat, building a super platform that integrates social interactions, payments, shopping, and travel. Payments are at the core of this vision.

Musk aims to replicate this path in the United States. His logic is straightforward: X already has approximately 600 million monthly active users who spend a considerable amount of time on the platform daily. If payment functionality can be embedded into this ecosystem, X will evolve from a mere attention container into a genuine financial gateway, becoming the central node for all monetary transactions and potentially boosting monthly active users to 1 billion.

X Money's Core Product Strength

Based on the disclosed features, X Money is positioned significantly above traditional P2P tools like Venmo or PayPal.

One of its core highlights is a 6% annual percentage yield (APY). Compared to the普遍less than 0.5% interest rates offered by traditional U.S. savings accounts, X Money's higher yield could serve as a powerful tool to attract early adopters.

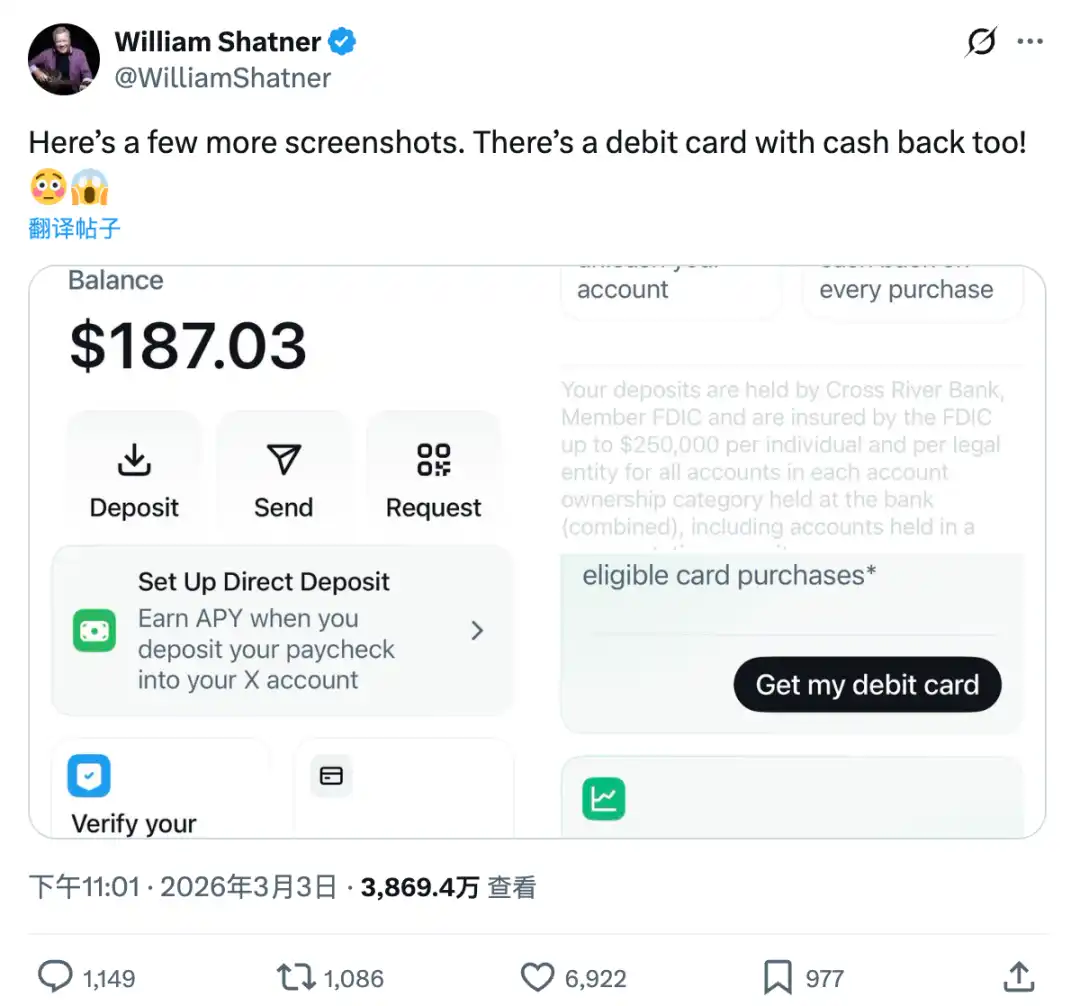

Additionally, the product offers P2P instant transfers, direct deposits, metal debit cards engraved with usernames, cashback rewards, zero foreign exchange fees, and a $25 account opening bonus, among other financial services.

The interface features three main functional tabs: "Account," "Rewards," and "Activity." The overall design resembles a lightweight digital bank account rather than a simple transfer tool, indicating its ambition to build a social ecosystem around financial behaviors, not just serve as a payment utility.

Transaction settlements are facilitated through the Visa Direct network, enabling near-instant fund transfers. In January 2025, X officially announced a partnership with Visa, making the latter X Money's first official payment partner.

The significance of this combination lies in X providing the traffic and场景, while Visa offers global clearing infrastructure. This partnership largely avoids the high barriers of building a payment system from scratch.

Currently, the product has completed internal closed testing. The external beta phase carries a distinct Musk-style marketing flair—X, through actor William Shatner, initiated a charity auction where donations of $1,000 or more could secure an X Money invitation, with a total of 42 spots released. Shatner himself was among the first to experience the product and shared screenshots on social media.

Ambition to Rival WeChat and the Reality Gap

Musk's reference point has always been WeChat.

The rapid rise of WeChat Pay was largely due to China's unique ecosystem: a near-universal instant messaging tool, a widely integrated merchant system, and a historical window when mobile payments were not yet fully established.

X faces a截然different battlefield. The U.S. payment market is highly mature, with Apple Pay, Venmo, PayPal, and Zelle each holding their ground, and credit card networks deeply embedded in daily consumption scenes.

Although X boasts around 600 million monthly active users, most people are accustomed to using it as an information platform rather than a financial tool. Persuading users to deposit money into a "social app" requires overcoming not just technical barriers but also psychological ones.

From a trust perspective, X platform account suspensions occur from time to time. If users worry about fund security and account accessibility, even high interest rates may not convince them to migrate their financial assets. Meanwhile, past controversies over data usage and privacy issues on X will be further amplified in financial contexts.

Such concerns have already surfaced at the regulatory level. In 2025, a New York State senator sent an open letter urging the state's Department of Financial Services (DFS) to exercise caution when reviewing licenses related to X Money, citing privacy protection and regulatory risks.

In reality, X has been quietly advancing its compliance布局over the past few years. Currently, X has obtained money transmitter licenses in over 40 U.S. states and Washington D.C., and has registered with the Financial Crimes Enforcement Network (FinCEN). Applications in a few markets like New York State are still pending, but the overall compliance framework is largely in place. User funds are custodied with FDIC-insured Cross River Bank, with coverage up to $250,000.

The Potential Role of Cryptocurrency

Among all the discussions about X Money, one topic始终lingers on the periphery—cryptocurrency. On this issue, Musk has chosen to remain silent, at least for now.

Musk's relationship with the crypto world is well-known. Over the past few years, he has repeatedly expressed support for Dogecoin and is also a public supporter of Bitcoin. Consequently, when news of X Money broke, the crypto community immediately began speculating whether the platform would integrate Dogecoin, XRP, or some form of stablecoin.

Based on currently disclosed information, X Money will initially operate on a pure fiat system, prioritizing the U.S. dollar. Officials have never formally confirmed support for Dogecoin or other crypto assets.

But the market clearly sees it differently: After Musk announced X Money's launch timeline, Dogecoin's price surged, community speculation about the "$" symbol button ran rampant, and even rumors about XRP and Ripple's stablecoin RLUSD continued to circulate within the community.

This ambiguity might be part of Musk's shrewd strategy. For Musk, crypto integration is更像a card that can be played at the right moment. Starting with fiat initially allows him to bypass additional regulatory complexities while building a user base and financial data, preserving future possibilities.

User Trust and Habit Barriers

The real challenge may not necessarily come from crypto assets themselves. For X Money, the pressure isn't just from direct competitors like PayPal or Venmo; a deeper obstacle lies in users' entrenched habits. Depositing funds into a social platform account presents a higher psychological barrier than a technical one for most U.S. users.

On the positive side, X's distribution cost is extremely low. Reaching 600 million users requires no additional customer acquisition investment, an advantage Venmo could only dream of when starting from scratch. The 6% APY could serve as a powerful user acquisition tool, especially in a declining interest rate environment. The metal debit card with username engraving also reinforces product identity on a material level.

On the other hand, the logic of a "super app" has its cultural limitations in the U.S. American users are accustomed to using multiple dedicated apps for different needs rather than relying on a single super entry point. The previous failures of Bakkt and Kraken's受阻application for a Federal Reserve account remind us that fintech faces dual阻力from both regulation and user habits in the U.S., and success is not always guaranteed.

The Test of Scaling and Global Expansion

If X Money successfully completes its early public access in April, the real test is just beginning.

First, can it achieve规模化adoption? The 6% APY is an attractive hook, but retaining users' long-term financial behavior depends on the coherence and reliability of the entire product experience.

Second, the global expansion timeline. X plans to expand internationally by the end of 2026, but factors like EU GDPR, various countries' AML/KYC compliance requirements, and local competitive landscapes are variables that cannot be underestimated.

Third, the profit model. X Money免除s many fees for users, so where will the revenue come from? If it relies on deposit interest rate spreads, it faces pressure during periods of declining interest rates; if it turns to value-added services, it needs to build a more complete financial product matrix.

Historically, U.S. internet giants' forays into finance have often ended in setbacks—Facebook Pay折戟, Bakkt's growth stalled, Google Pay underwent repeated restructuring. X Money's path is closer to that of a bank than a tech company, which is both its advantage and its burden.

True financial ambition cannot be replicated overnight. WeChat's success was the product of timing,地利, and人和. Whether X Money can replicate this miracle in the U.S. and globally remains to be seen. The early public access in April will be the first real report card for this ambitious experiment.