Author:Token Terminal

Translation:Saoirse,Foresight News

Ethereum is the core underlying settlement network for on-chain assets, relying on ETH to pay transaction fees and secure the network through staking. Traditional finance suffers from slow settlement, numerous intermediaries, and high counterparty risks, whereas tokenized assets and stablecoins offer on-chain solutions. As relevant regulations mature from 2025 to 2026, institutional deployment of on-chain business formally meets implementation conditions.

Various stablecoins, tokenized funds, commodities, and on-chain stocks are issued and settled on Ethereum, with layer-2 networks diverting transactions before ultimately returning to layer-1 for validation, allowing ETH to continuously accumulate value. By market capitalization, Ethereum remains the world's largest platform for tokenized assets, jointly operated by the Ethereum Foundation and the developer community. Teams like Etherealize specialize in connecting with traditional financial institutions, driving institutional capital inflow. In Q1 2026, the Ethereum ecosystem presented a divergent trend, analyzed in detail below using complete data from Token Terminal.

The market in Q1 2026 displayed a distinct two-sided dynamic: On-chain usage scale reached a historical high—monthly active users, total transaction volume, and throughput all set new records; however, dollar-denominated asset scale and fee metrics contracted simultaneously, with fully diluted market cap, total value locked (TVL), trading volume, and two types of fee data all declining sequentially. Key events this quarter profoundly shaped this unique market condition:

In January, the second round of the Fusaka upgrade cycle, the Blob Parameter Fork (BPO#2), was implemented, significantly enhancing data storage capacity.

In February, the ERC-8004 standard launched on mainnet, becoming the universal standard for AI agent identity and credit ratings.

The Ethereum Foundation finalized the three core goals for the 2026 protocol: scaling, optimizing user experience, and strengthening layer-1 foundational security.

In March, the Institutional Ethereum Forum was held, with participation enthusiasm from traditional financial institutions notably increasing.

Q1 2026 Key Metrics Overview

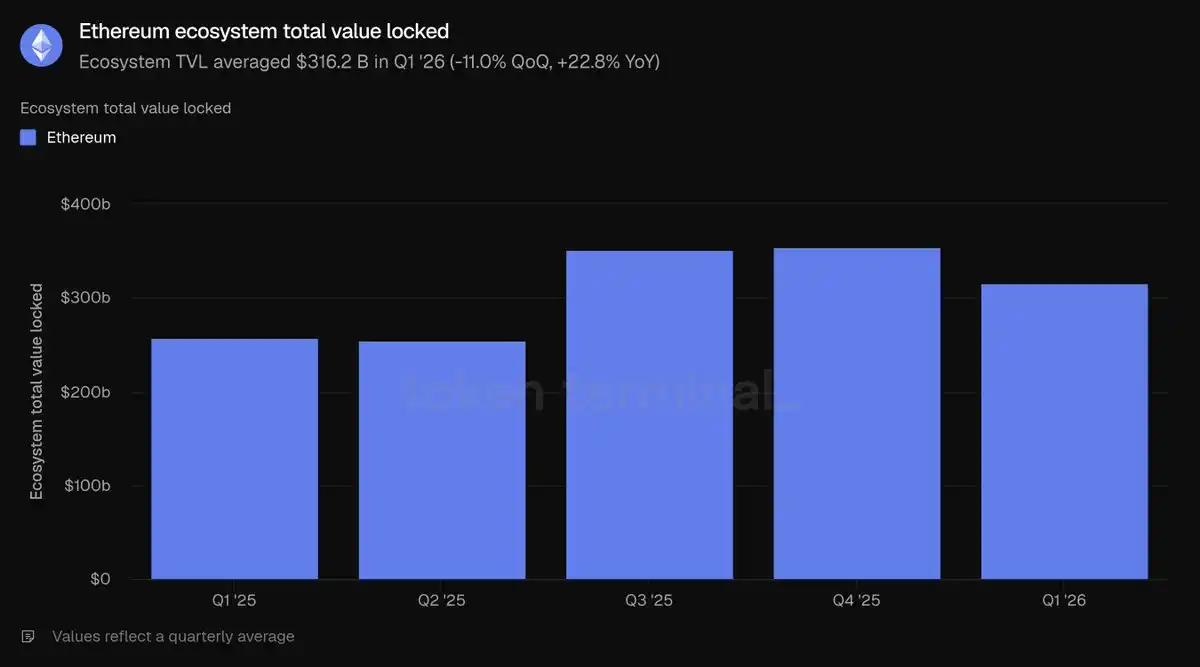

Ecosystem Total Value Locked: $316.2 billion (QoQ -11.0%, YoY +22.8%)

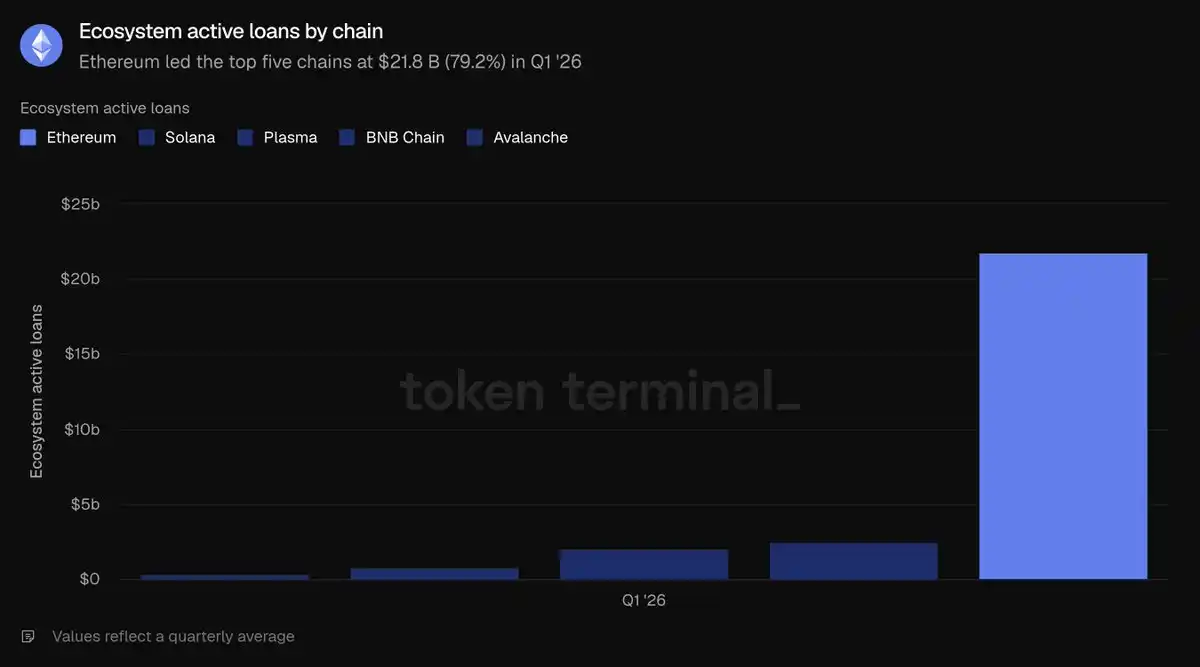

Ecosystem Outstanding Active Loans: $21.8 billion (QoQ -16.6%, YoY +39.0%)

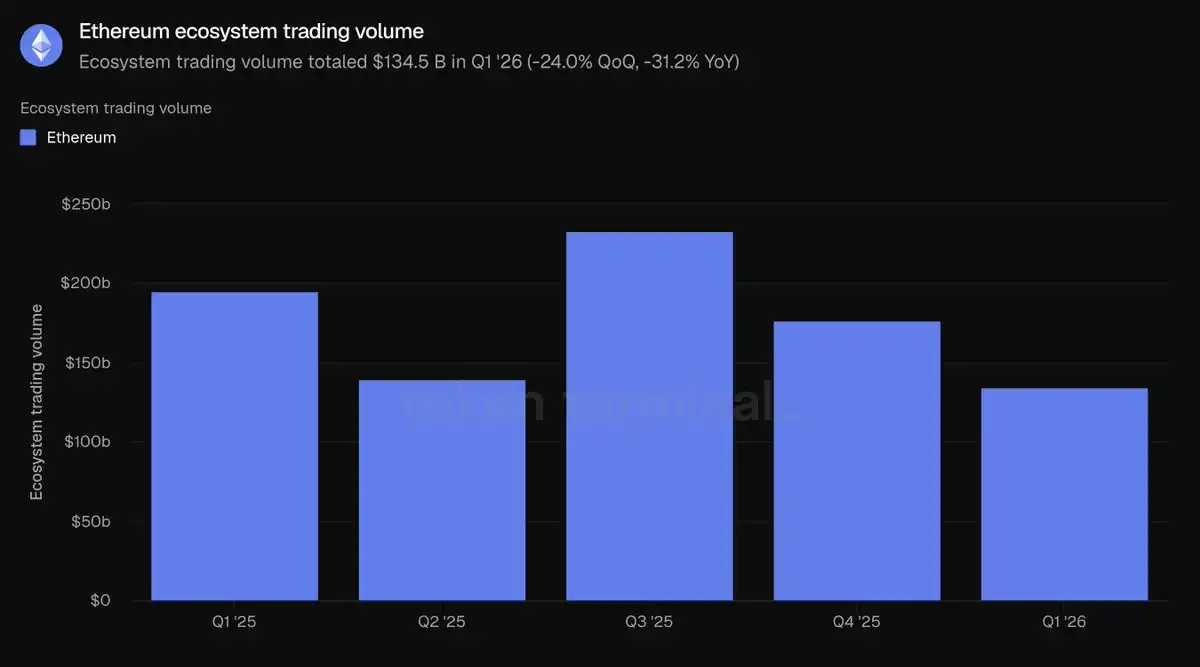

Ecosystem Decentralized Exchange Total Volume: $134.5 billion (QoQ -24.0%, YoY -31.2%)

Full Ecosystem Application Fee Revenue: $2.0 billion (QoQ -16.9%, YoY -7.8%)

On-chain Tokenized Asset Total Market Cap: $203.4 billion (QoQ -0.7%, YoY +42.9%)

Stablecoins: $178.9 billion (QoQ -2.3%, YoY +37.6%)

Tokenized Funds: $19.4 billion (QoQ +4.9%, YoY +73.1%)

Tokenized Commodities: $4.7 billion (QoQ +60.0%, YoY +325.9%)

Tokenized Stocks: $365.1 million (QoQ +16.5%)

Monthly Active User Addresses: 13.2 million (QoQ +53.5%, YoY +85.9%)

Layer-1 Total Transactions: 200.4 million (QoQ +38.0%, YoY +81.5%)

Average Transactions Per Second (TPS): 25.78 (QoQ +41.2%, YoY +81.7%)

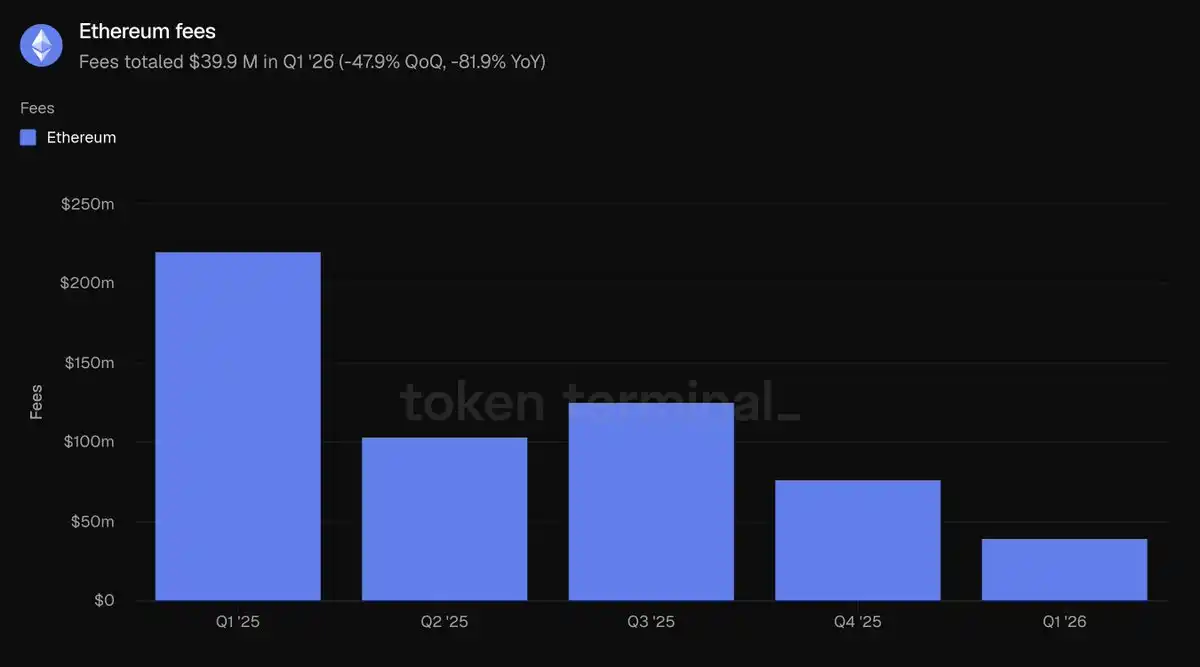

Layer-1 Mainnet Transaction Fee Revenue: $39.9 million (QoQ -47.9%, YoY -81.9%)

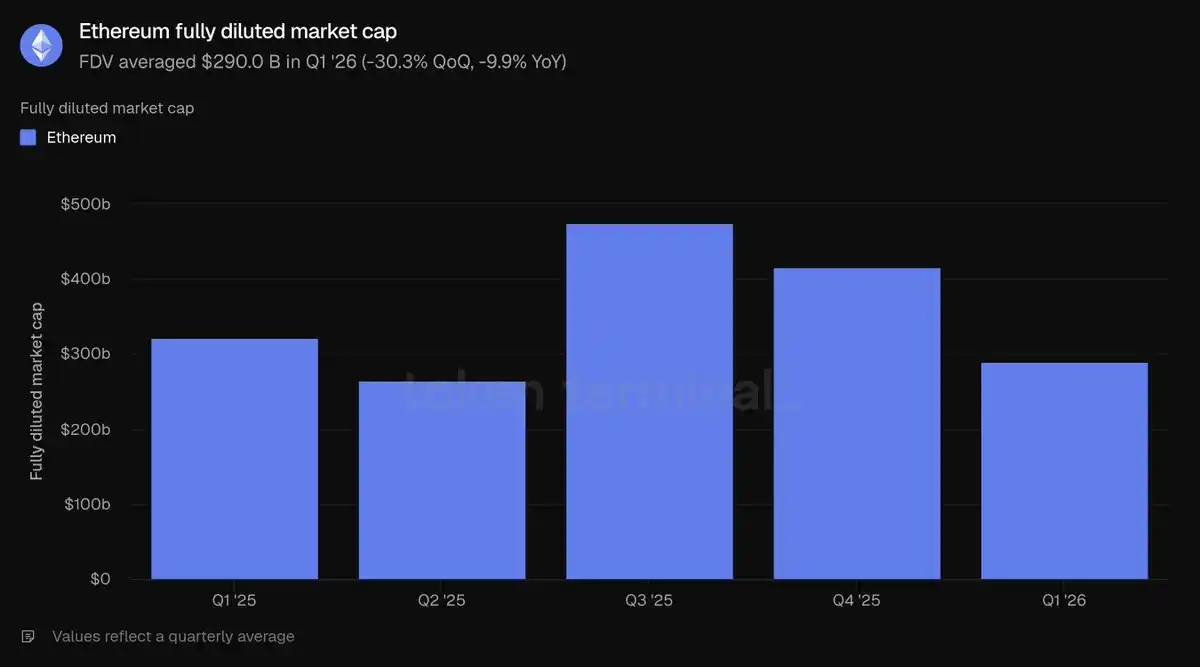

ETH Fully Diluted Market Cap: $290.0 billion (QoQ -30.3%, YoY -9.9%)

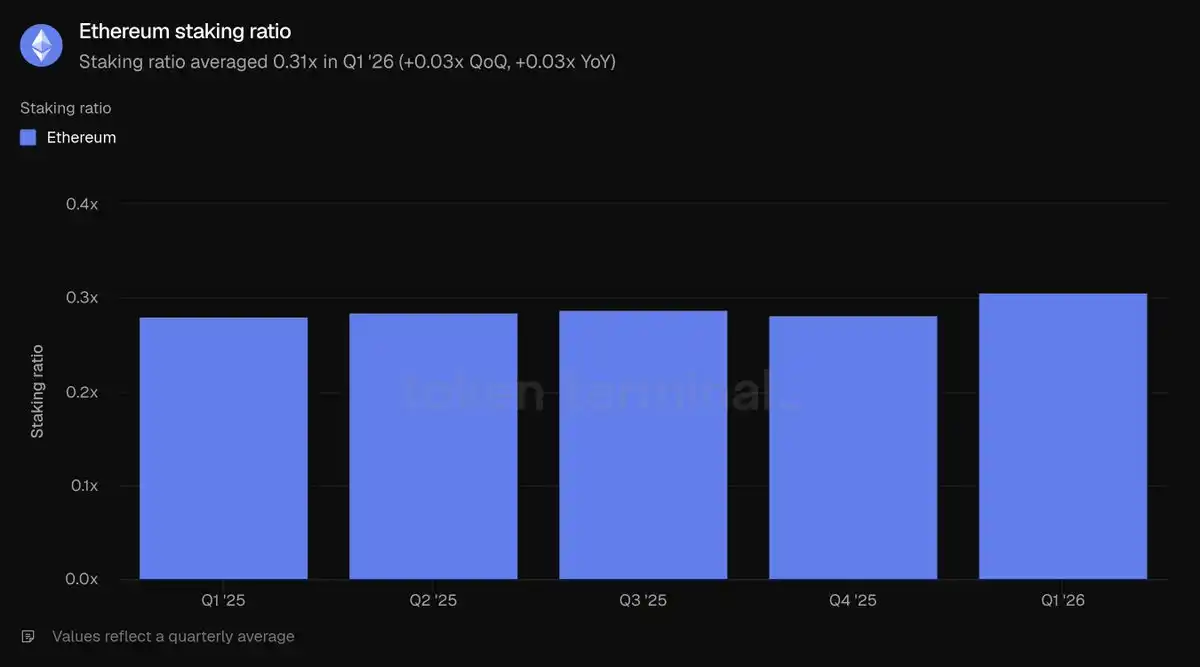

ETH Staking Ratio: 0.31 (Increased 0.03 QoQ and YoY)

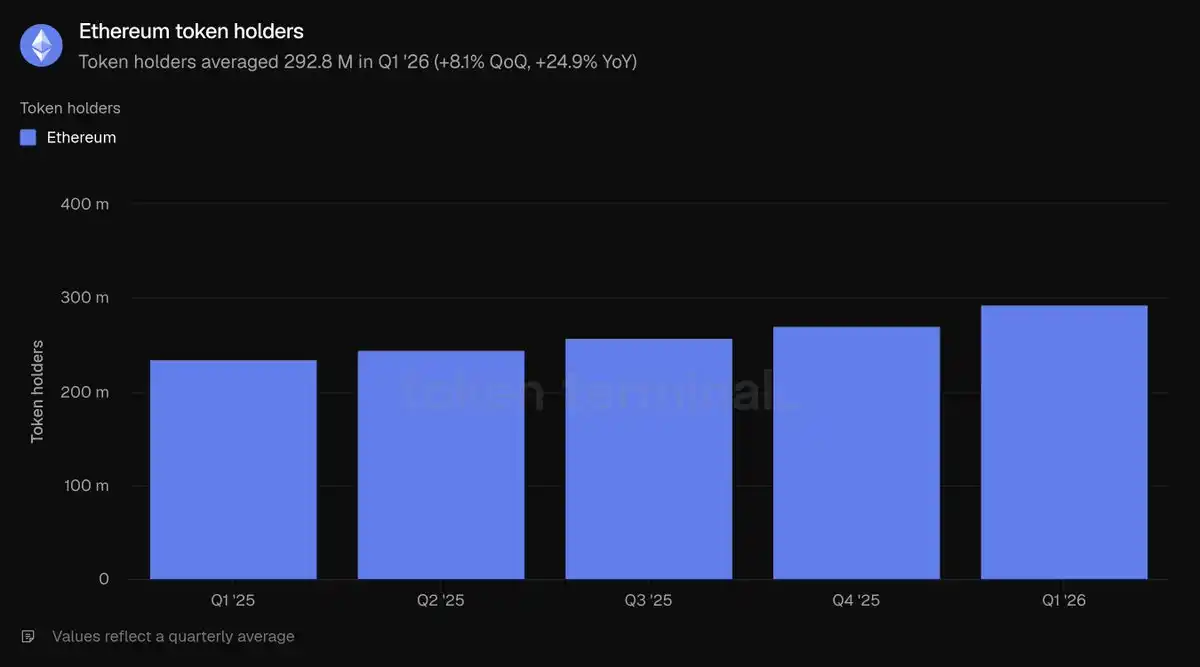

Total ETH Holding Addresses: 292.8 million (QoQ +8.1%, YoY +24.9%)

Note: This report's statistical scope includes only the Ethereum Layer-1 mainnet; layer-2 networks are considered independent blockchains, and their data is not included in Ethereum statistics.

Overall Ecosystem Development

Total Value Locked refers to the total USD value of assets deposited into various on-chain applications, a leading indicator for revenue-generating activities like lending, trading, and staking; here it represents the on-chain, user-withdrawable funds settled across the entire Ethereum ecosystem. In Q1 2026, the average TVL for the Ethereum ecosystem reached $316.2 billion, down 11.0% quarter-over-quarter but up 22.8% year-over-year. The sequential contraction stemmed from a general price correction in crypto assets, while the substantial year-over-year growth demonstrates a real expansion in ecosystem scale compared to the same period last year.

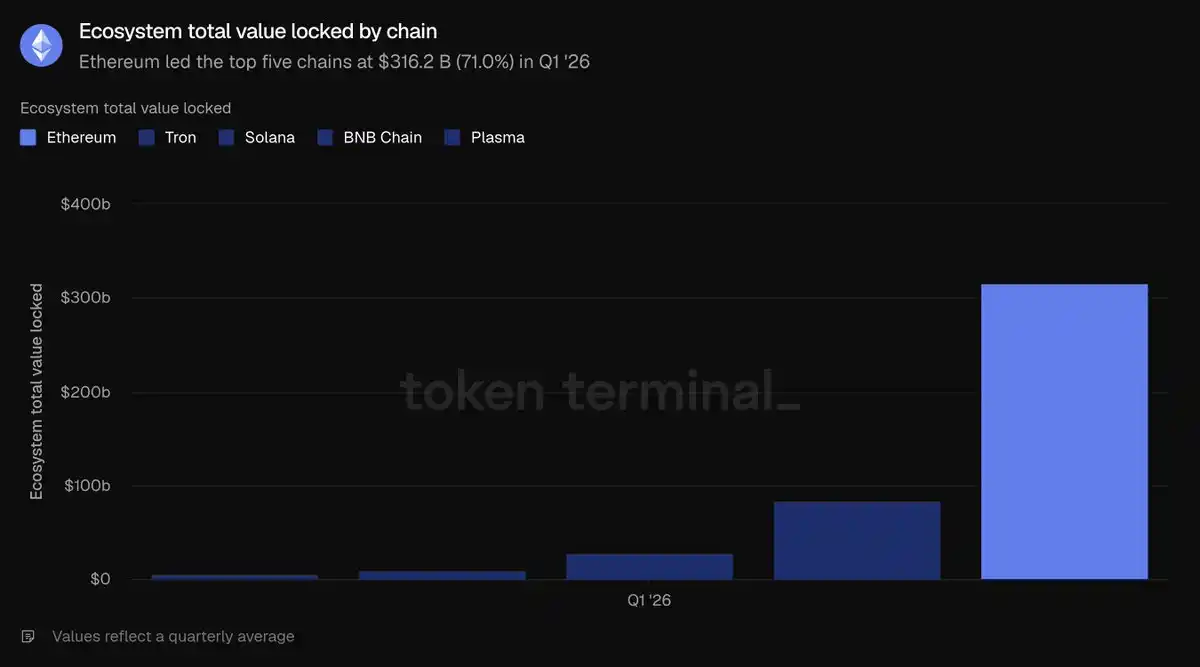

Among the top five blockchains by TVL, Ethereum leads by a wide margin: $316.2 billion far exceeds the sum of Tron ($84.5B), Solana ($28.8B), BNB Chain ($10.3B), and Plasma ($5.7B), accounting for 71% of the total TVL across these five chains. Funds are concentrated in two major sectors: the liquid staking sector led by Lido, and the lending sector centered around Aave; restaking protocols like EigenLayer and ether.fi, as well as synthetic dollar platforms like Ethena and Sky, also hold significant capital. High concentration of funds is Ethereum's most prominent structural advantage.

The Active Loans metric represents the scale of deposits that are lent out and generate interest income, directly reflecting lending business revenue; here it is the total outstanding borrowing across all Ethereum lending applications. In Q1, the average active loan scale in the ecosystem was $21.8 billion, down 16.6% QoQ but up 39.0% YoY. The contraction in loan balances alongside TVL reflects a cooling overall market risk appetite, but the scale remains significantly higher than the same period last year.

Ethereum's lending market is concentrated in a few pools, with Aave dominating: its active loan scale at quarter-end was approximately $13.5 billion, capturing the vast majority of the ecosystem's share; followed by Morpho (~$1.9B), Spark under Sky (~$1.0B), and Maple (~$840M). The contraction this quarter was primarily driven by Aave, as declining crypto asset prices led to cooler borrowing demand, with its total loan volume shrinking by about 24%. Comparing the top five chains, Ethereum's $21.8 billion in active loans significantly leads Solana ($2.5B), Plasma ($2.1B), BNB Chain ($760.8M), and Avalanche ($392.4M), accounting for 79.2% of the total lending volume across these five chains, making this the sector where Ethereum holds its highest share among the measured sectors.

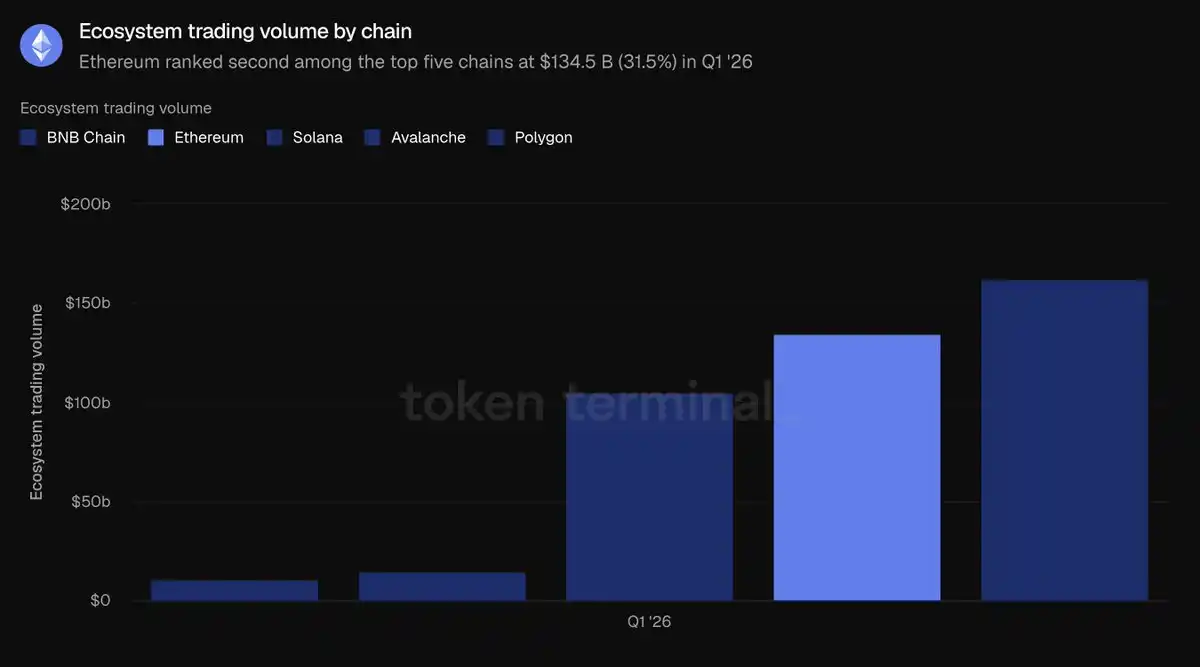

Decentralized Exchange Volume refers to the total transaction value completed on on-chain spot exchanges; traders pay fees during transactions, making volume highly correlated with platform revenue. This data aggregates all DEX trading within the Ethereum ecosystem. In Q1, total ecosystem trading volume was $134.5 billion, down 24% QoQ and 31.2% YoY. The decline in trading volume was steeper than the contraction in TVL, confirming a significant reduction in market risk appetite during this quarter's asset downtrend.

Ethereum DEX trading flow is highly concentrated among leading platforms: Uniswap's Q1 volume was approximately $85.5 billion, accounting for two-thirds of the ecosystem total; followed by Curve (~$22.1B) and CoW Swap (~$12.4B). Trading volume is the only metric where Ethereum does not top the five major chains: BNB Chain's total volume of $162.5 billion exceeded Ethereum's $134.5 billion, followed closely by Solana ($104.9B), with Avalanche ($14.5B) and Polygon ($10.7B) ranking lower. Ethereum's volume constitutes 31.5% of the total across the five chains, second to BNB Chain's 38%.

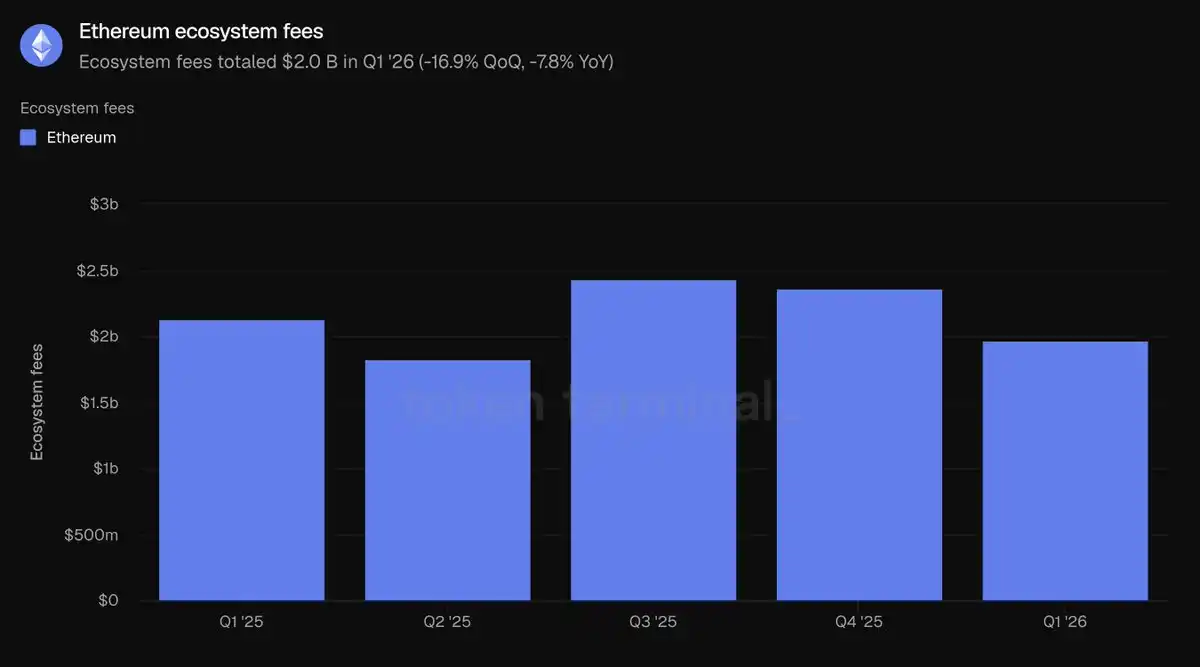

Ecosystem Fees refer to all fees generated by users using various applications, including borrower interest and trader transaction fees, directly reflecting the economic value created by the ecosystem; this sums all application fees across Ethereum. In Q1, total ecosystem fees amounted to $2.0 billion, down 16.9% QoQ and 7.8% YoY, declining alongside reduced trading and lending activity.

Ethereum's $2.0 billion in ecosystem fees far surpasses Tron ($599.3M), Solana ($532.5M), BNB Chain ($231.9M), and Polygon ($38.8M), accounting for 58.4% of the total fees across the top five chains. Even with the Q1 decline, Ethereum remains the number one source of application fees in the industry. Summarizing all indicators in this section: Ethereum leads the industry in TVL, lending scale, and ecosystem fees, trailing only in DEX volume behind BNB Chain.

Tokenized Assets Sector

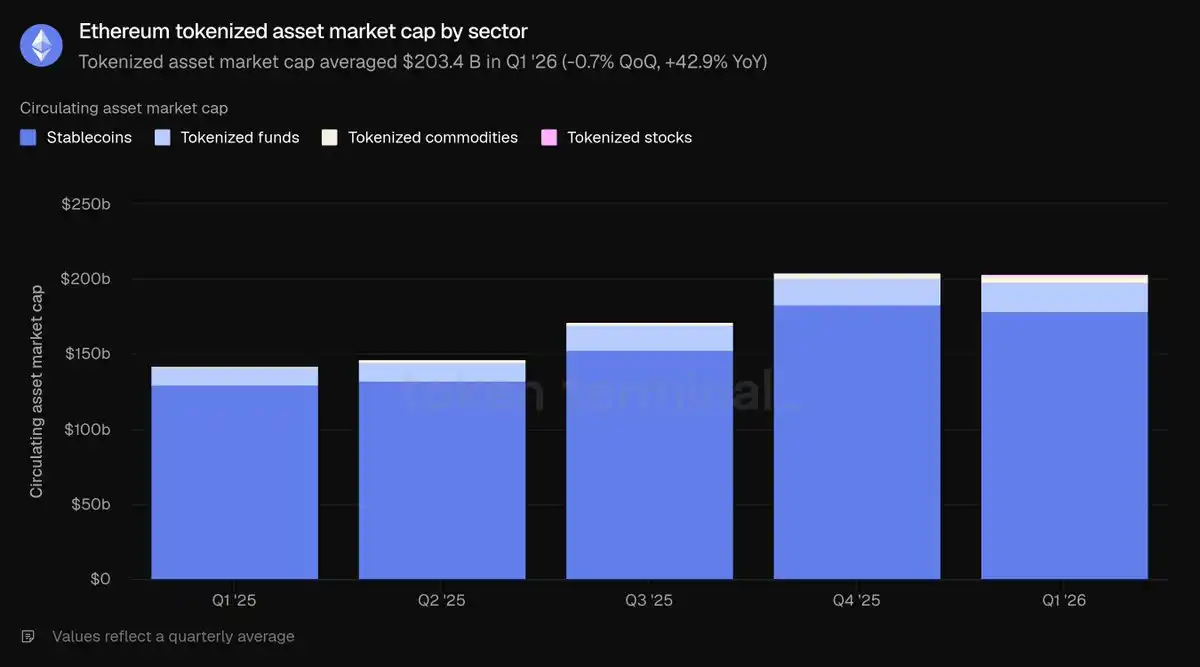

Circulating Asset Total Market Cap refers to the total value of on-chain tokenized assets, calculated as circulating supply multiplied by the daily closing price; for stablecoins, it's the total circulation, for tokenized funds, it's the on-chain assets under management, and for tokenized stocks, it's the total value of issued on-chain shares. This section only counts assets issued on Ethereum.

In Q1, the average total market cap of Ethereum tokenized assets was $203.4 billion, essentially flat QoQ (only down 0.7%), but up significantly by 42.9% YoY. Stablecoins accounted for 87.9% of the total, with the remaining share divided among tokenized funds, commodities, and stocks.

Stablecoins

In Q1, the average Ethereum stablecoin scale was $178.9 billion, down slightly by 2.3% QoQ but up 37.6% YoY, making it the only tokenized sub-sector to contract sequentially this quarter. The market is dominated by two major issuers: at quarter-end, Tether USDT ($94.1B) and Circle USDC ($54.5B) combined held the vast majority of Ethereum stablecoin market cap; other leading products include Sky USDS ($12.4B), Ethena USDe ($5.9B), and PayPal PYUSD ($2.9B); new compliant tokens like Ripple's RLUSD ($1.1B) have also launched. Comparing the top five chains, Ethereum's $178.9 billion stablecoin scale leads Tron ($84.5B), Solana ($14.5B), Arbitrum One ($6.8B), and Base ($4.7B), accounting for 61.8% of the total stablecoin value across these five chains.

Tokenized Funds

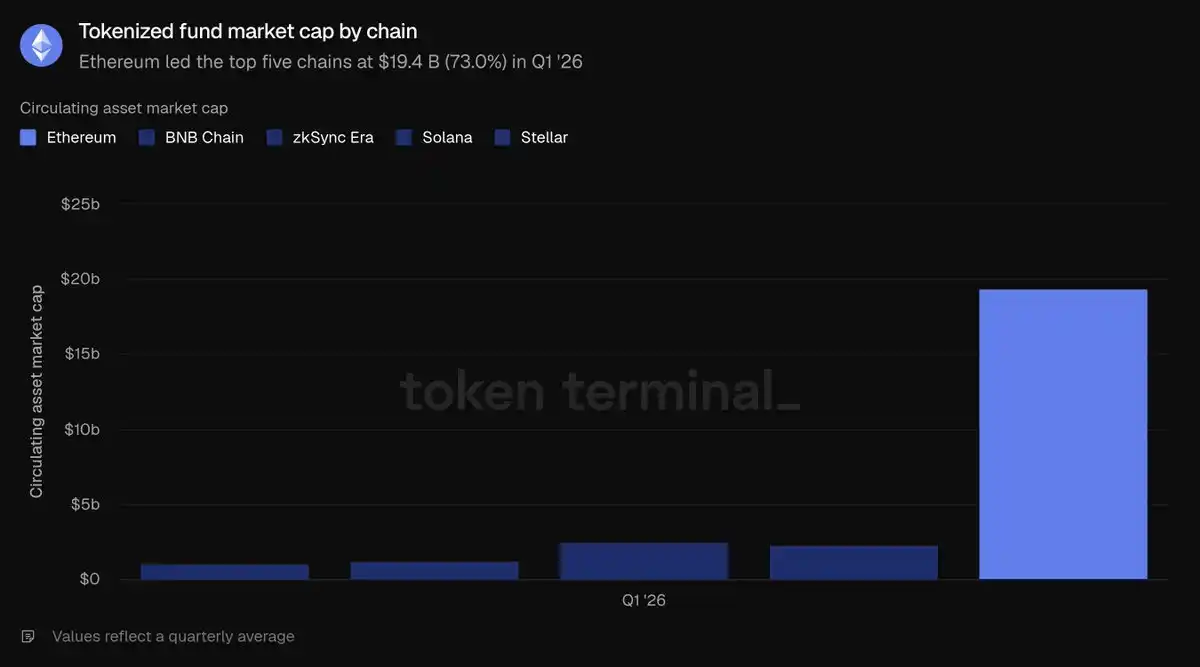

In Q1, the average scale of Ethereum tokenized funds was $19.4 billion, up 4.9% QoQ and surging 73.1% YoY. This sector divides into two main types:

Yield-generating on-chain USD products (largest by scale): Sky sUSDS (~$6.4B) and Ethena sUSDe (~$3.5B);

Traditional finance compliant funds (core vehicles for institutional narrative): BlackRock BUIDL (issued via Securitize, ~$1.0B), WisdomTree Government Money Fund (~$815M), Superstate USTB (~$620M), with Ondo OUSG (~$320M) following closely. Comparing the top five chains, Ethereum's $19.4 billion in tokenized funds significantly leads ZKsync Era ($2.5B), BNB Chain ($2.3B), Solana ($1.3B), and Stellar ($1.1B), accounting for 73% of the total, making this Ethereum's second most dominant tokenized asset sector.

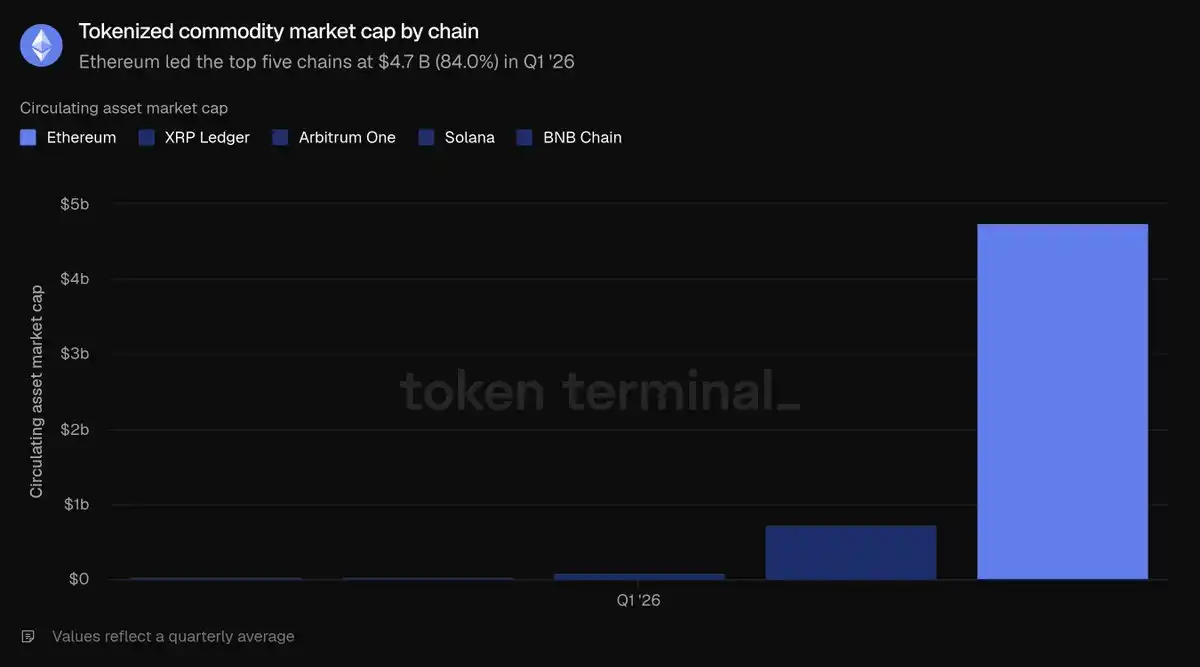

Tokenized Commodities

In Q1, the average scale of Ethereum tokenized commodities was $4.7 billion, up 60% QoQ and soaring 325.9% YoY, making it the fastest-growing tokenized category. This sector is almost entirely composed of on-chain gold: Tether Gold XAUT (~$2.6B) and Paxos Gold PAXG (~$2.4B) together account for nearly all of the sector's share. Comparing the five relevant public chains, Ethereum's $4.7 billion scale far exceeds Ripple ($736.6M), Arbitrum One ($95.9M), BNB Chain ($38.4M), and Solana ($29.8M), accounting for 84% of the total, making this Ethereum's most dominant sub-sector.

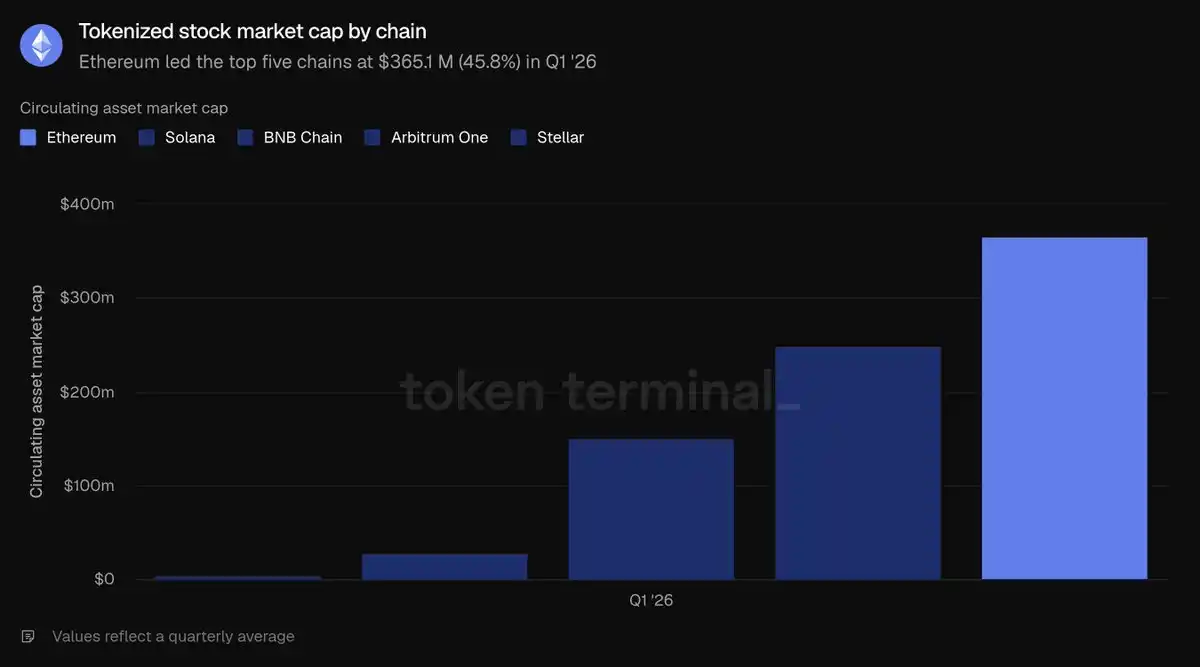

Tokenized Stocks

Tokenized stocks are the smallest sub-category. In Q1, the average Ethereum scale was $365.1 million, nearly zero a year ago, up 16.5% QoQ. This sector is almost entirely monopolized by Ondo Finance, which issues S&P 500, Nasdaq 100 broad-based indices, and dozens of individual stock tokens on-chain, constituting the vast majority of Ethereum's tokenized stock market cap. Comparing the top five chains, Ethereum's $365.1M slightly leads Solana ($249.0M), BNB Chain ($150.5M), Arbitrum One ($29.0M), and Stellar ($4.2M), but only accounts for 45.8% of the total tokenized stock value across these five chains, making it the only tokenized asset sector where Ethereum does not hold an absolute majority share.

Summarizing the tokenized assets sector: Q1 saw a slight decline in stablecoin supply, but Ethereum's monopoly positions in tokenized funds and commodities were further solidified.

On-chain Usage Activity

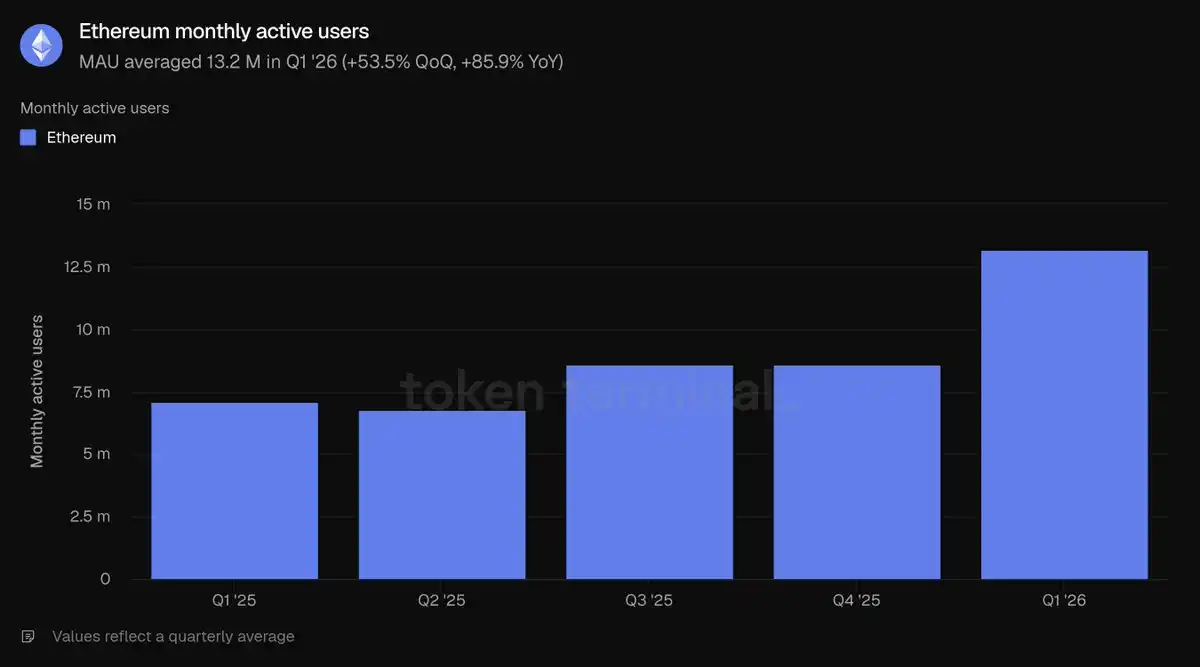

Monthly Active Users are defined as unique addresses that generate revenue-generating on-chain transactions each month; this metric only counts interaction addresses on the Ethereum Layer-1 mainnet. In Q1, the average monthly active users were 13.2 million, surging 53.5% QoQ and up 85.9% YoY, setting a historical record and ending the slow growth trend of previous quarters, with user growth accelerating significantly.

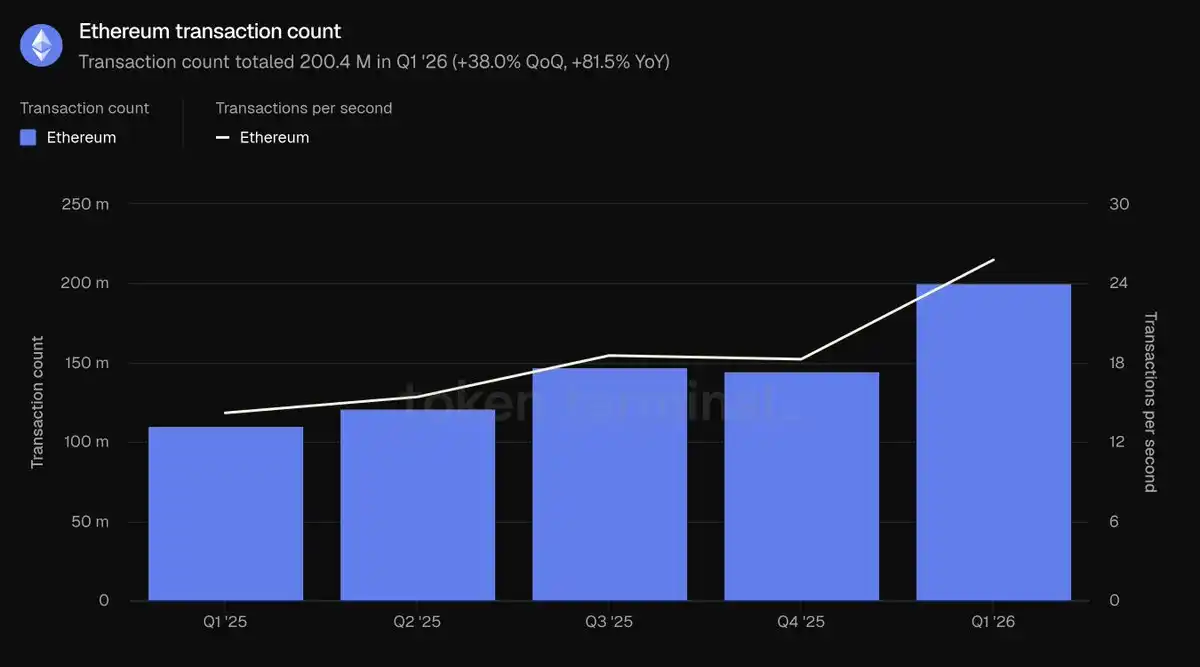

Total Transaction Volume refers to the number of transactions written to and confirmed on the blockchain, reflecting user engagement; Transactions Per Second (TPS) is the average confirmation rate during the period, measuring the network's real-time capacity. Both metrics are for the Ethereum Layer-1 mainnet only. In Q1, layer-1 total transactions were 200.4 million, up 38% QoQ and 81.5% YoY; average TPS increased to 25.78, up 41.2% QoQ. Both data points set new historical highs, proving that user growth has translated into real on-chain business activity increments.

Fees here specifically refer to the base network cost users pay to initiate transactions on Ethereum Layer-1, distinguished from the full ecosystem application fees in section two. In Q1, layer-1 total transaction fees were $39.9 million, plummeting 47.9% QoQ and down sharply 81.9% YoY. Rising activity paired with drastically falling fees is the quarter's core data paradox: transaction volume increased 38%, yet total fees fell by nearly half. The core reason is that Blob scaling significantly increased block storage capacity, making block space more abundant and thus significantly reducing the cost per transaction.

The core conclusion of this section is that scaling benefits have materialized: users and transaction counts have simultaneously hit record highs, while overall network usage costs have declined. When network throughput expansion outpaces the growth rate of market transaction demand, it results in the characteristic "activity up, fees down."

Native Token ETH Fundamentals

Fully Diluted Market Cap calculation: ETH token price × total supply under the current tokenomics model (including circulating, locked, unlocked, and to-be-issued tokens). In Q1, ETH's average fully diluted market cap was $290.0 billion, down sharply 30.3% QoQ and 9.9% YoY. This is the largest sequential decline among all valuation metrics in the report and the core factor driving the decline in USD-denominated asset scale across the ecosystem.

Staking Ratio: The total value of ETH staked to secure the Proof-of-Stake network, divided by ETH's overall market cap; 0.31 indicates approximately 31% of ETH's market cap is participating in staking. In Q1, the average staking ratio was 0.31, higher than 0.28 in the previous quarter and the same period last year. Despite ETH's overall market cap correcting significantly, the proportion of tokens participating in network security staking increased, indicating stable long-term staking intentions among users even during price downturns.

Token Holder Metric: The total number of unique wallet addresses holding ETH. In Q1, the average number of ETH holding addresses was 292.8 million, up 8.1% QoQ and 24.9% YoY, marking a steady increase for five consecutive quarters. Against the backdrop of a continuously declining fully diluted market cap, the expansion of holding addresses represents a further dispersion of the ETH holder base, with ordinary users' willingness to acquire not cooling with short-term market trends.

Etherealize Team Commentary and Analysis

The quarter's core paradox: Ethereum's Layer-1 mainnet on-chain usage scale hit a historical high, yet network transaction fees declined simultaneously. Ethereum proactively advances network scaling, willingly sacrificing short-term fee revenue. The long-term logic is: cheaper block space will unleash a massive wave of latent market demand, ultimately driving long-term growth in overall network revenue.

Data from Token Terminal's "Ethereum Q1 2026 Report" proves this long-term logic is being realized: on a YoY basis, monthly active users grew 85.9%, total transaction volume rose 81.5%, and network throughput increased 81.7%. This is a typical manifestation of the Jevons Paradox. The team predicts that the long-term increase in total network transaction demand will fully offset the short-term revenue loss from lower per-transaction fees. Drawing an analogy to the semiconductor industry: When Gordon Moore proposed Moore's Law in 1975, industry revenue was limited. Today, industry revenue has grown by several orders of magnitude. Scaling benefits are not yet fully realized: The Glamsterdam upgrade scheduled for Q3 plans to increase the gas limit more than threefold; Ethereum's long-term roadmap envisions achieving tens of thousands of TPS by 2029, building a high-speed Layer-1 blockchain with second-level finality.

The team agrees with BlackRock CEO Larry Fink's view from December last year: The current stage of the tokenization industry is equivalent to the internet in 1996—when Amazon's online book sales were only $16 million. At that time, the market generally believed Amazon was merely surviving on the internet bubble, a continuously loss-making online bookstore. But Jeff Bezos predicted the internet would completely reshape retail, abandoning short-term profits to fully build network effects and scale advantages. Ethereum is now making the same trade-off to solidify its position as the global financial settlement layer.

The development of the internet offers another crucial insight: Open, permissionless networks will ultimately triumph over closed, private networks. In 1995, Bill Gates predicted in "The Road Ahead" that digital commerce would rely on corporate proprietary private networks, "information superhighways," not the open internet. At the time, Microsoft built MSN, and services like America Online, CompuServe, and Prodigy operated closed walled gardens, boasting millions of paying users; France's Minitel terminal system even had more users globally than the entire internet until late 1996. Yet all these closed systems ultimately failed. No major legitimate corporation is willing to build its business on a network controlled by a competitor; more crucially, no single company can perpetually keep pace with the innovation speed of a permissionless, open ecosystem. History repeatedly confirms this pattern: Linux overtaking proprietary Unix systems, the open web replacing corporate intranets, Wikipedia superseding the Encyclopædia Britannica. In each transformation's early stages, proprietary products hold an initial advantage due to more refined features, ample marketing, and business resources. But once the open ecosystem accumulates sufficient development tools, developers, and neutral, trustworthy attributes, the first-mover advantage rapidly erodes.

This industry pattern is now replaying in financial infrastructure, as all data in this report demonstrates that Ethereum has crossed the ecosystem critical point: it holds dominant market share in all core sectors. Institutions choosing Ethereum for tokenized finance is not based on ideological preference, but because ecosystem liquidity, composability, and mature institutional use cases are concentrated here. Report data shows: Ethereum holds 79.2% of DeFi active lending, 61.8% of stablecoins, 73% of tokenized funds, and 84% of tokenized commodities market share among the top five chains. Each new class of tokenized assets further deepens ecosystem liquidity, continuously attracting more institutions. A neutral, unbiased foundation is the only stable equilibrium solution for the industry—major financial institutions will never uniformly choose a competitor's private chain for asset settlement. Moreover, institutions are gradually realizing that private interactions, access restrictions, KYC compliance, and asset transfer controls can all be implemented via privacy-preserving computational environments and permissioned token standards on top of Ethereum, while fully accessing the public network's vast liquidity; conversely, closed private chains cannot tap into the open ecosystem's massive liquidity and diverse applications.

Following the quarter-end, institutional deployment has accelerated further, with multiple significant developments in May alone: Asset Management: BlackRock filed for two additional tokenized funds; JPMorgan issued its second Ethereum on-chain money market fund, JLTXX; Fidelity International launched the Moody's AAA-rated dollar liquidity fund FILQ, launched as an ERC-20 token. Stablecoin Sector: The Japanese Blockchain Association's yen-pegged stablecoin EJPY is set to deploy on Ethereum; a European alliance of 12 major banks (including BNP Paribas, ING, UniCredit, BBVA, etc.) is preparing a compliant Euro stablecoin.

The internet seemed distant in 1990, but by 2005 it had become a societal necessity. If Fink's assessment of the tokenization industry's development stage is accurate, the next few years may be the most opportune period in Ethereum's development history. The team's previous "Efficient Money" report posited a core view: Network fees establish an intrinsic value floor for ETH; the long-term optimistic logic is that, with more robust monetary properties, ETH has the potential to absorb the premium from the combined monetary storage value of gold and Bitcoin, exceeding $30 trillion. Ethereum can establish industry leadership without relying on high transaction fees.