Background

Ethereum is scheduled to merge to Proof of Stake (PoS)1 on September 15, 2022, and as expected, this has caused speculation around the emergence of a Proof of Work (POW)2 Ethereum (ETHW) fork. While there is precedent for an Ethereum fork3, we’ll explore why it may not be viable this time around and what it could mean for both Ethereum (ETH) and Ethereum Classic (ETC).

Ethereum Classic was born in 2016 after a bug in the code underlying a nascent Decentralized Autonomous Organization, known as “the DAO”, was exploited to allow a hacker to steal more than 3.6 million ETH. While the majority of the community was in favor of a hard fork to amend the network’s transactional record to nullify the attacker’s actions, a subset believed that there should not be any modification to the chain state. The forked version of the network became the Ethereum chain we have today, and the subset of users against the fork continued to host the version of the network in which the DAO’s attacker succeeded, now known as Ethereum Classic.

Since then, Ethereum has developed a robust on-chain ecosystem of decentralized applications (dApps) and users, while Ethereum Classic has largely remained a store-of-value asset. Despite the differences, Ethereum Classic presents a clean-slate, proof of work variant of the Ethereum network that users, developers, and miners could seamlessly transition to should the Ethereum merge result in a hard fork.

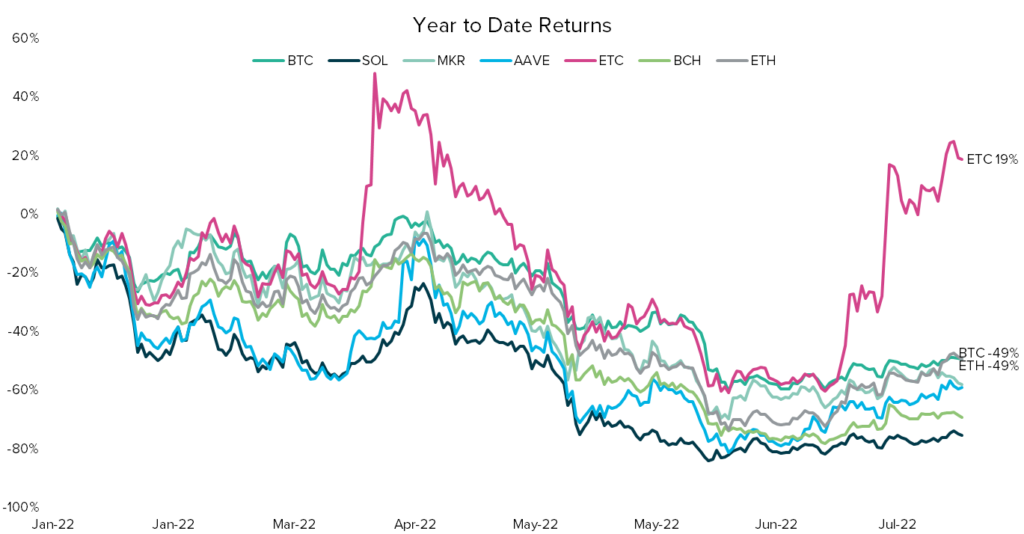

In March 2022, news began to spread of Ethereum miners considering a transition to Ethereum Classic, sending the price of ETC up 103% in 11 days. Despite speculation around a new ETHW fork after the merge, ETC rallied again, gaining more than 198%4 since July 12. Speculation around the merge has made ETC one of the best performing cryptocurrencies of 2022, up 18% YTD, while others like Bitcoin (BTC) and Ethereum (ETH) have shed nearly 50% of their value.

Source: TradingView as of 8/15/2022

Historically, forked assets have been quite profitable, and many of the top tokens by market cap started as forks of Bitcoin and Ethereum. For example, in July 2016 when Ethereum (ETH) forked into ETH and ETC, anyone who held tokens on the original blockchain at the time instantly came into possession of an equivalent amount of the new one. By the end of the year, ETC was the 6th largest coin by market cap at $124 million compared to $697 million for ETH. Today5, Ethereum Classic (ETC) is the 19th largest coin by market cap worth more than $5.6 billion.

Despite a precedent for forks creating value in the past, we’ll explore why this may not be a viable solution to creating a POW

Ethereum is More Than Just Currency

It’s important to distinguish between the Ethereum ecosystem of 2016 (when the network first forked into ETH and ETC) and the far more developed on-chain ecosystem of Ethereum protocols, dApps, and tokens that users experience and interact with today. A PoW fork of the current Ethereum network will bring duplicate instances of all of these tokens, which could present meaningful challenges to developers and market participants. In fact, the sheer complexity of DeFi and the number of asset-backed tokens locked in DeFi protocols poses a catastrophic risk to the price of ETHW due to on-chain positions attempting to be liquidated.

To contextualize how much higher the stakes are today, let’s look at a key element of the Ethereum ecosystem: stablecoins. In 2016, when Ethereum Classic was forked, stablecoins were only beginning to gain traction. In June of that year, the market cap of Tether (USDT) compared to Ethereum (ETH) was just .65%, compared to 28.34%6 at the time of writing.

Source: CoinMetrics, CoinGecko as of 8/15/2022

Tether and other stablecoin issuers, like Circle (USDC), have stated that only the tokens on the PoS network will be redeemable post-fork. This means all of the variants on ETHW are likely to become worthless, in addition to other “asset-backed tokens,” like wrapped Bitcoin (wBTC) and staked ETH (stETH).

Some of the major use-cases for asset-backed tokens are collateral for loans, providing liquidity, facilitating leveraged trading, and other DeFi applications. In 2016, this ecosystem was effectively non-existent. Today, DeFi on Ethereum consists of more than 530 protocols7 with nearly $40 billion8 of value locked in the smart contracts. Currently, over $25 billion in asset-backed tokens are locked in smart contracts. If the ETHW fork goes live, users of these protocols may attempt to liquidate positions leveraged against formerly-asset-backed tokens into ETHW tokens, while ETH holders simultaneously rush to sell the free ETHW tokens they’ve received for dollars or ETH on centralized exchanges. As a result, we will likely see disproportionate selling pressure on the forked asset.

Source: CoinMetrics as of 8/15/2022

So far, the speculative markets that have emerged for ETHW have not reflected strong support for the fork. The price of ETHW could be considered a proxy for how much support the potential fork may have, which has been trending down since trading of ETH IOU’s began when Poloniex launched support on August 10. ETHW traded at a peak of .08 ETH before continuing a steady down trend to .03 ETH9. While there may be a possibility of short-term relief rallies, the price of ETHW indicates that the support may be driven by speculation rather than true perceived value of the asset. While ETHW has declined more than 50% since launch, ETC has gained ~9% during the same period.

Source: CoinGecko (Ethereum POW on Poloniex) as of 8/15/2022

Unnecessary Complexity for Protocol Teams

An ETHW fork could bring new operational issues for many Ethereum-based protocols, in addition to the non-redeemable asset-backed tokens on the ETHW chain losing value. When the token holders of a protocol vote to deploy on a new blockchain, the circulating supply of the protocol tokens does not change to prevent dilution of value and utility. However, on a PoW fork, the protocol will be duplicated, as will any native tokens. This means they may be likely to trade at a different price than their counterparts on the PoS chain.

As a result, protocols will need to determine how to manage the value tokens held by duplicate treasuries, duplicate tokens, NFT ownership, and more. How will governance rights be consolidated? Could somebody buy the cheaper variant and still have the same amount of voting power? Will duplicate tokens in protocol treasuries be held or sold? Protocol teams may find it much simpler to deploy a fresh instance of the protocol on Ethereum Classic without any issues of token variants.

The Bull Case for Ethereum Classic

The success of an ETHW fork will require not only users, capital, and development work, but also strong support from existing blockchain infrastructure. Major exchanges and DeFi protocols are already making decisions about support for ETHW tokens, though these do not necessarily indicate a preference or endorsement of the ETHW technology.

Now that a potential ETHW fork is gaining traction, miners may play an even more critical role. Post-merge, miners will no longer be able to earn rewards from the Ethereum network and will be looking to divert their resources to a new network. With approximately one month left until the anticipated merge, there is still no documentation or expected timeline for how miners will need to adjust their machines and software to mine the ETHW chain. Meanwhile, Ethereum Classic is fully documented and operationally ready to absorb the hashrate currently mining Ethereum.

Regardless of the success of an ETHW fork, Ethereum Classic will still continue operating as normal. Supporters of continuing a Proof of Work version of Ethereum may find that the complexity of an ETHW fork may not be worth the effort when a stable version of the network exists in Ethereum Classic. While users may be drawn in by the promise of free tokens, the ability to liquidate ETHW tokens for dollars will likely be short-lived as liquidity dries up on exchanges. Once there is no more value left to extract, it is unlikely that users will continue supporting the ecosystem.

Conclusion

An ETHW fork will face significant challenges due to the complexity of DeFi and proliferation of asset-backed tokens. While chances of success are expected to be low, some support for a PoW fork has emerged from miners and exchanges. So far, speculation on the ETHW token has sent the price in a steady decline of more than 50% in value since launch, while the price of ETC has increased in value by approximately 9%.

In addition to declining interest in the ETHW token, major Ethereum protocols and participants, such as Tether and Circle, have signaled support for ETH PoS as the canonical chain – a significant sign of support as the two companies are responsible for nearly $12010 billion in on-chain asset-backed tokens. Should protocols find that token holders do want a variation of the protocol on a PoW variant of Ethereum, it is likely that they will have a preference towards ETC rather than navigating the complexity of the on-chain ecosystem duplicated on ETHW.