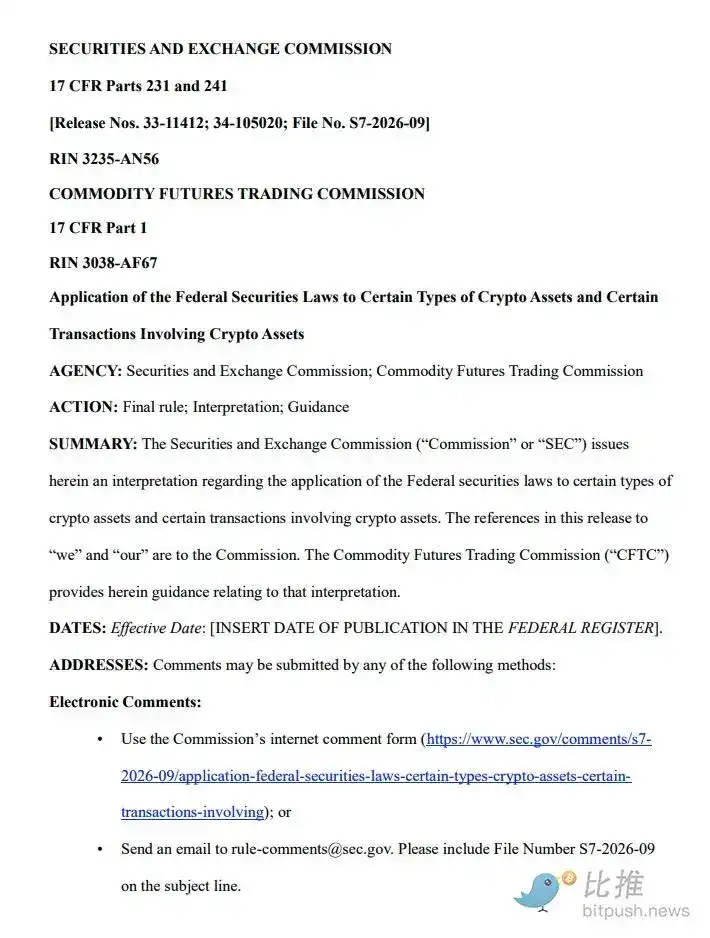

On March 17, 2026, the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) jointly released an interpretive document numbered 33-11412. This 68-page regulatory framework officially declares: U.S. crypto regulation has ended a decade-long era of "regulation by enforcement" and entered a new era of clarity and harmonization driven by "Project Crypto".

This document is not only a rare achievement of regulatory collaboration between the SEC and CFTC but also the most landmark guidance in the history of U.S. crypto regulation. The following is the full interpretation of the essential edition:

I. Background: "Project Crypto" from Conflict to Collaboration

In 2017, the SEC first applied the Howey test to crypto assets through "The DAO Report." For the next decade, regulation primarily relied on enforcement actions to define asset attributes, leaving the market in a state of uncertainty and controversy.

In early 2025, the SEC established the "Crypto Task Force," subsequently launching the "Project Crypto" initiative led by SEC Chairman Paul S. Atkins and CFTC Chairman Michael S. Selig. The initiative aimed to coordinate the authority of the two major regulatory agencies, establish a unified asset classification method, and provide a clear path for crypto innovation to remain in the U.S. In January 2026, the project was officially upgraded to a joint SEC and CFTC action.

II. Asset Classification: The Logic of the "Five-Category Law" for Crypto Assets

Based on asset characteristics,用途, and functionality, the document divides crypto assets into five major categories, providing the market with a clear classification standard for the first time:

-

Digital Commodities

Definition: Refers to those assets whose value stems from the programmatic operation and supply-demand dynamics of a "functionalized" crypto system, rather than relying on the managerial efforts of others.

Core List: The document explicitly names mainstream tokens such as BTC, ETH, SOL, XRP, ADA, DOT, AVAX, LINK, etc., as digital commodities. These assets are not controlled by any single centralized entity and do not possess inherent economic rights that generate passive income.

-

Digital Securities

Definition:即"Tokenized Securities," referring to traditional securities represented in the form of crypto assets, or digital assets possessing the economic substance of securities (e.g., representing enterprise ownership, dividend rights).

Regulation: Whether on-chain or off-chain, as long as they符合 economic substance, they fall under the SEC's regulatory purview.

-

Regulated Payment Stablecoins

Definition: Stablecoins that meet the definition of the 2025 "GENIUS Act" and are issued by authorized institutions.

Qualification: These stablecoins are explicitly excluded from the definition of "securities" and are primarily受 specific legal constraints as payment instruments.

-

Digital Tools

Purpose: Tokens that only have utility functions within specific crypto systems (e.g., access rights or service payments) and are generally not considered securities.

-

Digital Collectibles

Definition: Assets intended to be collected and/or used, representing artworks, music, videos, in-game items, or internet memes, etc.

Examples: CryptoPunks, Chromie Squiggles, WIF, VCOIN, etc.

Qualification: Not securities themselves; their value stems from supply and demand relationships rather than the managerial efforts of others. However, if fragmented and sold, they may constitute securities.

III. Innovation: "Separation" and "Dynamic Conversion" of Security Attributes

This is the most groundbreaking legal innovation in the document—the SEC首次承认: The "security attribute" of a crypto asset is not permanent.

"Separation" Mechanism

-

Principle: A project may be considered a security (investment contract) during its initial financing phase if it meets the Howey test. But when the project completes its roadmap, achieves autonomous operation of open-source code, and decentralizes network power, the asset can be "separated" from the investment contract.

-

Judgment Standard: When investors no longer reasonably rely on the issuer's "essential managerial efforts" to obtain profits, but instead rely on the system's own operation and market supply and demand, the asset transforms from a "security" to a "digital commodity."

-

Separation Timing: Can occur immediately upon delivery of the asset to the purchaser, or at a future date.

Three Scenarios for Separation

-

Issuer Fulfills Promises: After completing the essential managerial efforts, even if non-essential maintenance continues, the asset is no longer bound by the investment contract.

-

Issuer Abandons Project: If publicly宣布放弃 development and no longer fulfills promises, the asset脱离 securities law jurisdiction (but the issuer may still bear legal liability for fraud).

-

Secondary Market Trading: If subsequent purchasers no longer reasonably expect to rely on the issuer's efforts for profit, the transaction does not constitute a securities transaction.

Transparency Recommendation

The SEC encourages project parties to publicly disclose roadmap progress and milestone achievements to facilitate market identification of the "separation point."

IV. Qualification of On-Chain Activities: "Demining" for Decentralization

Regarding long-disputed activities such as staking, mining, wrapping, and airdrops, the document provides extremely detailed and favorable explanations:

Protocol Mining

-

Qualification: PoW mining is an "administrative or ministerial" activity that ensures network security and verifies transactions.

-

Conclusion: Whether solo mining or joining a mining pool, it does not involve securities issuance.

-

Mining Pool Operation: The activities of mining pool operators are administrative and ministerial, not constituting essential managerial efforts.

Protocol Staking

-

Qualification: Staking is an administrative activity for maintaining network operation.

-

Coverage: Includes solo staking, delegated third-party staking, custodial staking, and liquid staking.

-

Custodial Staking: If a custodian stakes on behalf of users, as long as it does not involve re-lending of assets, leverage, or discretionary trading, it does not constitute a securities activity.

-

Ancillary Services: Slash insurance, early unstaking, flexible reward distribution, asset aggregation, and other auxiliary services are all administrative and ministerial.

Staking Receipt Tokens

-

Qualification: If the underlying asset is a non-security commodity and not subject to an investment contract, the receipt itself is not a security.

-

Principle: The receipt merely exists as a "receipt," does not generate income; income stems from the underlying staking activity.</极速赛车开奖极速赛车开奖直播历史记录直播历史记录

Wrapping Tokens (Wrapping)

-

Definition: Users deposit crypto assets with a custodian or跨链桥, obtaining 1:1锚定的 redeemable wrapped tokens.

-

Qualification: If the underlying asset is a non-security commodity and not subject to an investment contract, wrapping tokens are considered an "administrative function" aimed at enhancing interoperability and do not constitute a securities transaction.

-

Key Restriction: The custodian must lock the assets and cannot lend,抵押, or re-stake them.

Airdrops

-

Qualification Breakthrough: As long as the recipient does not provide money, goods, services, or other consideration, it does not meet the "investment of money" element of the Howey test.

-

Applicable Scenarios:

Airdropping to wallets holding specific tokens, without prior announcement

Rewarding early testnet users

Airdropping to eligible users based on application usage

-

Red Line: If recipients need to provide services (e.g., social media promotion) in exchange for the airdrop, it may constitute securities issuance.

V. Consolidation of U.S. Leadership

The document analyzes its economic significance in detail at the end:

-

Eliminate "Chilling Effect": By providing legal clarity, reduce business stagnation caused by compliance opacity and encourage crypto innovation to return to the U.S.

-

Reduce Compliance Costs: Clear classification and separation paths significantly reduce corporate legal consulting and regulatory应对 costs.

- Enhance Market Transparency: The new framework requires more detailed disclosure during the "investment contract" phase, better protecting investors.

-

Promote Competition and Innovation: Clear rules will attract more issuers and entrepreneurs to enter the market.

-

Improve Pricing Efficiency: Reduce price distortions caused by uncertainty.

VI. Historic Breakthrough in Regulatory Collaboration

Structurally, the document establishes a clear analytical path: first classify the asset, then judge the transaction structure, and finally analyze whether the investment relationship持续存在.

More importantly, this is a rare result of coordination between the SEC and CFTC on crypto regulatory issues. Previously, the two agencies had long-standing differences in defining "securities vs. commodities," and this joint framework实质上 divides the归属 of major asset categories, marking a shift in U.S. crypto regulation from the stage of "inter-agency jurisdictional competition" to a "division of labor system based on unified rules."

This 68-page document not only ends a decade of regulatory chaos but also establishes the U.S.'s leadership position in the global crypto regulatory field. For practitioners, it is a must-read "industry constitution"; for investors, it is a clear "rights protection guide"; for entrepreneurs, it is a clear "compliance roadmap".

The "Wild West" era of crypto assets has officially ended.

Original Link