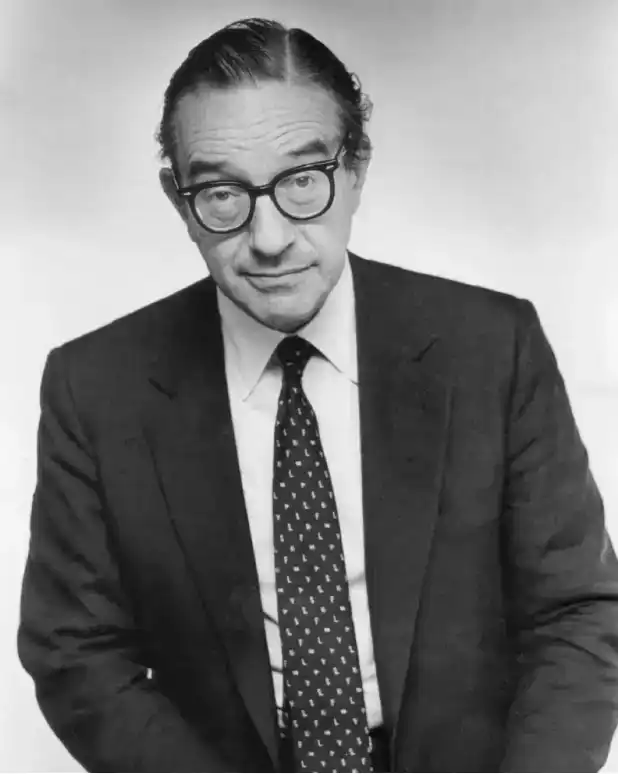

Former US Federal Reserve Chairman Alan Greenspan passed away on Monday at his home in Washington at the age of 100, due to complications from Parkinson's disease. His wife, Andrea Mitchell, NBC News' chief Washington correspondent, announced the news. To global markets, Greenspan was more than just the name of a former central banker: he presided over the Fed for nearly 19 years, witnessing America's journey from the 1987 stock market crash to the internet boom, and later becoming a central figure in the historical questioning surrounding the 2008 financial crisis after leaving office.

His life almost encapsulates the core debates of the US capital markets over the past few decades: whether markets can truly self-regulate, and whether central banks should actively intervene to prevent bubbles.

Presided over the Fed for Nearly 19 Years, Spanning Four Presidents

Greenspan assumed the role of Federal Reserve Chairman in August 1987 and served until January 2006, a tenure of nearly 19 years, making him the second-longest-serving Fed Chair in US history, second only to William McChesney Martin.

This tenure spanned the administrations of Ronald Reagan, George H.W. Bush, Bill Clinton, and George W. Bush, and covered the late Cold War, the internet wave, accelerated globalization, and the expansion of financial innovation. His ability to secure consecutive appointments across partisan administrations itself spoke to his unique position bridging Washington and Wall Street.

At his peak, Greenspan was often referred to as the "Maestro." This title wasn't merely personal acclaim; it represented the strong confidence in technological progress, free markets, and capital market efficiency that characterized the US in the 1990s. During that period of prolonged economic expansion, with inflation remaining moderate and stock markets and productivity rising in tandem, there was a widespread belief that central banks could sustain growth and stability without heavy-handed market intervention.

Greenspan's public persona was also marked by that of a technocrat. He was known for his cautious, often obscure, speech, yet markets would dissect his every word, searching for hints about the direction of interest rates. This era, where "a single sentence from the Fed Chair could sway global markets," reached its zenith during his tenure.

From the 1987 Crash to 9/11, He Was Once Seen as the Crisis Helmsman

Greenspan faced his first major test shortly after taking office. In October 1987, the US stock market experienced "Black Monday," with the Dow Jones Industrial Average plummeting in a single day. The Federal Reserve's swift injection of liquidity to support the markets was seen as a crucial step in stabilizing the financial system.

Thereafter, he navigated the Asian financial crisis, the Russian debt crisis, the Long-Term Capital Management (LTCM) turmoil, and the market shock following the September 11, 2001 attacks. At these junctures, the Fed's liquidity support and rate cuts reinforced Greenspan's image as a "crisis manager."

This policy style later became known in market parlance as the "Greenspan Put." It wasn't a formal policy but rather a market expectation: when asset prices fell sharply and the financial system was under pressure, the Fed would step in to provide a backstop. For investors, this expectation reduced panic; but from another perspective, it could also encourage higher leverage and more aggressive risk-taking.

Greenspan himself was not simply synonymous with "forever easy" policy. In 1996, he famously warned of stock market excess with the phrase "irrational exuberance," a line that became legendary in financial history. The problem, however, was that the warning did not translate into forceful policy action to suppress the asset bubble. For him, it was difficult for a central bank to accurately judge when a bubble was forming, and equally hard to preemptively burst it without harming the real economy.

This judgment appeared pragmatic during the boom times but became a starting point for controversy after the crisis.

Market-Friendly Philosophy, Re-examined After 2008

The underlying philosophy of Greenspan's policy was market-friendly. He believed market prices aggregated information, that financial innovation dispersed risk, and that excessive regulation would undermine efficiency. He was also a long-term supporter of free trade, deregulation, and technology-driven productivity gains.

This philosophy aligned perfectly with the economic atmosphere of the US in the 1990s. Following the Cold War's end, the expansion of globalization and information technology brought immense optimism. Financial innovation accelerated on Wall Street, with complex derivatives, securitized products, and bank off-balance-sheet activities proliferating. Before the crisis erupted, these instruments were often described as progress that improved capital allocation efficiency and dispersed financial risk.

But the 2008 financial crisis reshaped Greenspan's historical standing.

Critics argued that the Fed maintained low interest rates for too long after the dot-com bubble burst and 9/11, fueling housing market overheating; that regulators were overly tolerant of risk expansion by banks and Wall Street, failing to curb the growth of mortgage-backed securities, leverage, and complex financial products; and that the central bank, aware that asset prices might be deviating from fundamentals, was unwilling to directly confront bubbles.

This criticism does not mean the 2008 crisis can be attributed to Greenspan alone. Its causes were multifaceted, including regulatory structures, institutional incentives, rating systems, housing policies, global capital flows, and more. However, as the preeminent monetary policymaker and a leading proponent of free-market ideology before the crisis, it was perhaps inevitable that he would become a focal point of the debate.

Greenspan defended his policy legacy in his later years. He acknowledged a flaw in his judgment regarding the self-restraint capacity of financial institutions but also emphasized that bubbles are often difficult to accurately identify as they form, and that policymakers cannot possibly grasp the full picture of a crisis in advance.

His Historical Assessment Remains Suspended Between Two Eras

The reason Greenspan's passing still captures global market attention is that the debates surrounding him have not faded with time.

In the eyes of his supporters, he was the central bank helmsman during a prolonged period of American prosperity, maintaining financial system stability through multiple external shocks and helping guide the US economy through a critical transition from high-inflation memories to a low-inflation growth phase. Without the Greenspan era, it would be difficult to understand the optimism of the 1990s US capital markets and the global investor trust in the Federal Reserve.

In the eyes of his critics, he is also an iconic figure of an era of financial permissiveness. Low interest rates, light-touch regulation, and faith in the market's self-correcting abilities ultimately exposed their costs in the housing bubble, subprime crisis, and global financial system imbalances. After 2008, the shift in the Fed and the US regulatory system toward stronger oversight and larger-scale intervention was, in some ways, a reaction against the Greenspan era.

This is precisely the complexity of Greenspan's legacy: he was neither purely a creator of prosperity, nor can he be simply labeled the architect of crisis. He represented an era that believed markets, technology, and financial innovation could continuously improve economic performance; and the conclusion of that era has forced the world to re-examine the boundaries between central banks, regulation, and markets.

For investors today, Greenspan's death is not merely a historical footnote. Whenever markets bet the Fed will pivot to easing in a crisis, whenever rising asset prices coexist with financial stability risks, the questions of the "Greenspan era" resurface: Is the central bank stabilizing the markets, or is it encouraging the next round of risk accumulation? That question still has no definitive answer.