Author: Spencer Applebaum & Eli Qian

Compiled by: Deep Tide TechFlow

Over the past two decades, fintech has transformed how people access financial products, but it hasn't fundamentally changed how money moves.

Innovation has primarily focused on cleaner interfaces, smoother user experiences, and more efficient distribution channels, while the core financial infrastructure has remained largely unchanged.

For much of this period, the fintech stack was more about reselling than rebuilding.

Overall, the evolution of fintech can be divided into four stages:

FinTech 1.0: Digital Distribution (2000-2010)

The earliest wave of fintech made financial services more accessible but did not significantly improve efficiency. Companies like PayPal, E*TRADE, and Mint digitally packaged existing financial products by combining legacy systems (such as the decades-old ACH, SWIFT, and card networks) with internet interfaces.

During this phase, fund settlement was slow, compliance processes relied on manual operations, and payment processing was constrained by rigid schedules. Although this period brought financial services online, it did not fundamentally alter how money moved. The change was merely about who could use these financial products, not how they actually worked.

FinTech 2.0: The Neobank Era (2010-2020)

The next breakthrough came from the proliferation of smartphones and social distribution. Chime offered early wage access for hourly workers; SoFi focused on student loan refinancing for graduates with upward potential; Revolut and Nubank served the underbanked globally with user-friendly interfaces.

Although each company told a more compelling story for a specific audience, they were essentially selling the same product: checking accounts and debit cards running on old payment networks. They still relied on sponsor banks, card networks, and the ACH system, no different from their predecessors.

These companies succeeded not because they built new payment networks, but because they reached customers better. Branding, user onboarding, and customer acquisition became their competitive advantages. In this stage, fintech companies became distribution-savvy entities attached to banks.

FinTech 3.0: Embedded Finance (2020-2024)

Starting around 2020, embedded finance rose rapidly. The proliferation of APIs (Application Programming Interfaces) enabled almost any software company to offer financial products. Marqeta allowed companies to issue cards via API; Synapse, Unit, and Treasury Prime offered Banking-as-a-Service (BaaS). Soon, nearly every application could provide payments, cards, or loans.

However, beneath these layers of abstraction, nothing fundamentally changed. BaaS providers still relied on sponsor banks from earlier eras, compliance frameworks, and payment networks. The abstraction layer shifted from banks to APIs, but economic benefits and control ultimately flowed back to the traditional systems.

The Commoditization of FinTech

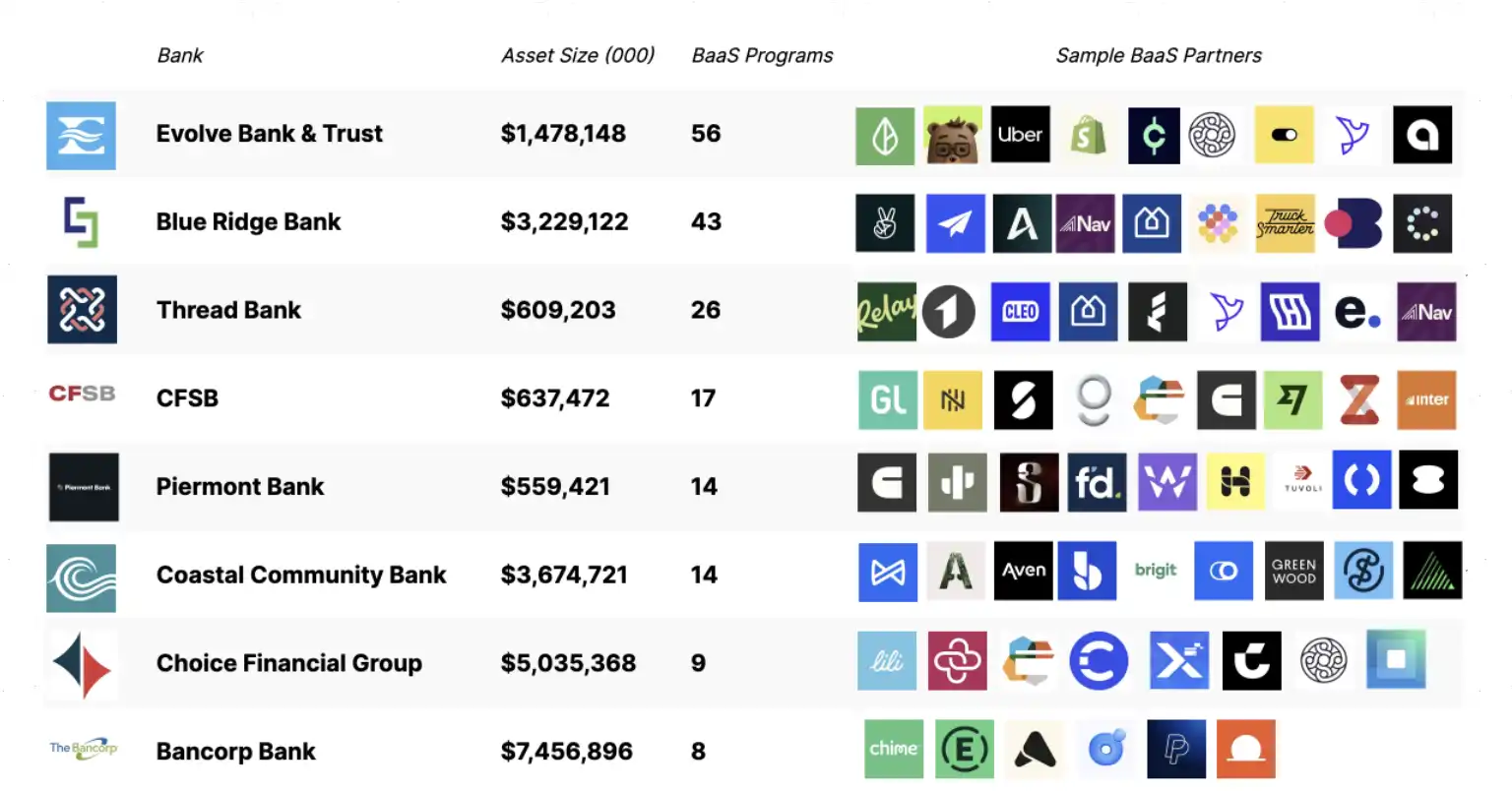

By the early 2020s, the flaws of this model became apparent. Almost all major neobanks relied on the same small set of sponsor banks and BaaS providers.

Source: Embedded

As companies fiercely competed through performance marketing, customer acquisition costs soared, profit margins shrank, fraud and compliance costs surged, and infrastructure became almost indistinguishable. Competition turned into a marketing arms race. Many fintech companies tried to differentiate themselves through card colors, sign-up bonuses, and cash-back gimmicks.

Meanwhile, risk and value control were concentrated at the bank level. Large institutions like JPMorgan Chase and Bank of America, regulated by the OCC, retained core privileges: accepting deposits, issuing loans, and accessing federal payment networks (like ACH and Fedwire). Fintech companies like Chime, Revolut, and Affirm lacked these privileges and had to rely on licensed banks to provide these services. Banks profited from interest spreads and platform fees; fintech companies relied on interchange fees.

As fintech programs proliferated, regulators increased scrutiny on the sponsor banks behind them. Regulatory orders and heightened supervisory expectations forced banks to invest heavily in compliance, risk management, and oversight of third-party programs. For example, Cross River Bank entered into a consent order with the FDIC; Green Dot Bank faced enforcement action from the Federal Reserve; and the Federal Reserve issued a cease and desist order to Evolve Bank.

Banks responded by tightening customer onboarding processes, limiting the number of supported programs, and slowing product iteration. The environment that once supported innovation now required larger scale to justify compliance costs. Fintech growth became slower, more expensive, and more inclined towards launching generic products for broad audiences rather than focusing on specific needs.

From our perspective, the main reasons innovation remained at the top of the stack for the past 20 years are threefold:

- Money movement infrastructure was monopolized and closed: Visa, Mastercard, and the Fed's ACH network left little room for competition.

- Startups needed significant capital to launch finance-centric products: Developing a regulated banking application required millions of dollars for compliance, fraud prevention, fund management, etc.

- Regulations limited direct participation: Only licensed institutions could custody funds or move money through core payment networks.

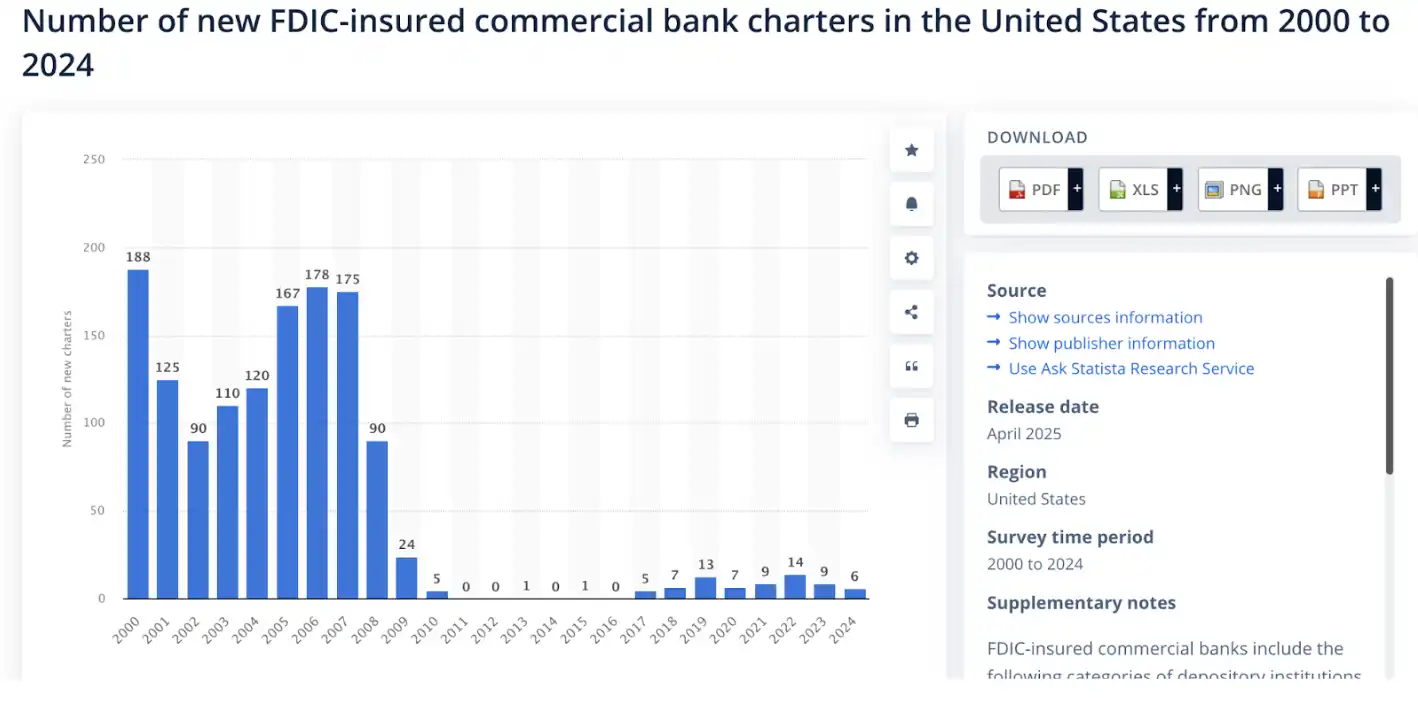

Source: Statista

Given these constraints, it was wiser to focus on building products rather than directly challenging existing payment networks. The result was that most fintech companies ended up as nicely packaged wrappers around bank APIs. Despite two decades of innovation in fintech, the industry saw very few truly new financial primitives. For a long time, there were no practical alternatives.

The crypto industry took the opposite path. Developers first on building financial primitives. From automated market makers (AMMs), bonding curves, perpetual contracts, liquidity vaults to on-chain credit, all were built from the ground up. For the first time in history, financial logic itself became programmable.

FinTech 4.0: Stablecoins and Permissionless Finance

Although the first three eras of fintech achieved many innovations, the underlying money movement architecture changed little. Whether financial products were offered through traditional banks, neobanks, or embedded APIs, money still moved on closed, permissioned networks controlled by intermediaries.

Stablecoins change this model. Instead of building software on top of banks, they directly replace the core functions of banks. Developers can interact directly with open, programmable networks. Payments settle on-chain, and custody, lending, and compliance shift from traditional contractual relationships to being handled by software.

Banking-as-a-Service (BaaS) reduced friction but did not change the economic model. Fintech companies still had to pay sponsor banks, card networks for settlement, and intermediaries for access. Infrastructure remained expensive and restricted.

Stablecoins completely remove the need to rent access. Developers interact directly with open networks instead of calling bank APIs. Settlement happens on-chain, and fees flow to protocols rather than intermediaries. We believe this shift dramatically lowers the cost barrier—from millions of dollars to develop via a bank, or hundreds of thousands via BaaS, to just thousands of dollars via permissionless on-chain smart contracts.

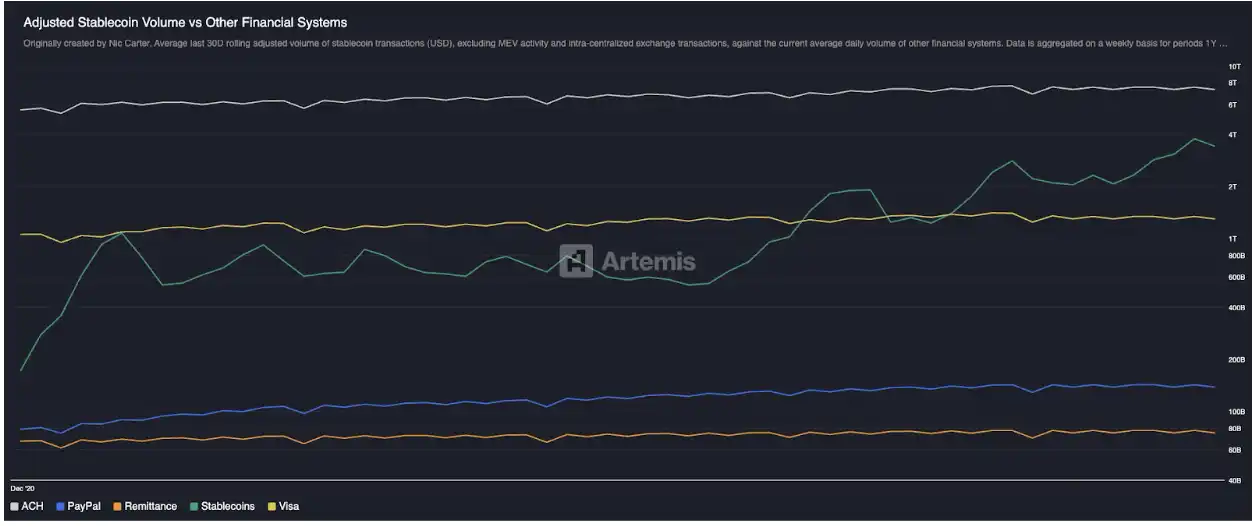

This shift is already evident at scale. The market cap of stablecoins grew from near zero to about $300 billion in less than a decade. Even excluding exchange transfers and maximal extractable value (MEV), the actual economic transaction volume they process has surpassed that of traditional payment networks like PayPal and Visa. For the first time, a non-bank, non-card payment network has truly achieved global scale.

Source: Artemis

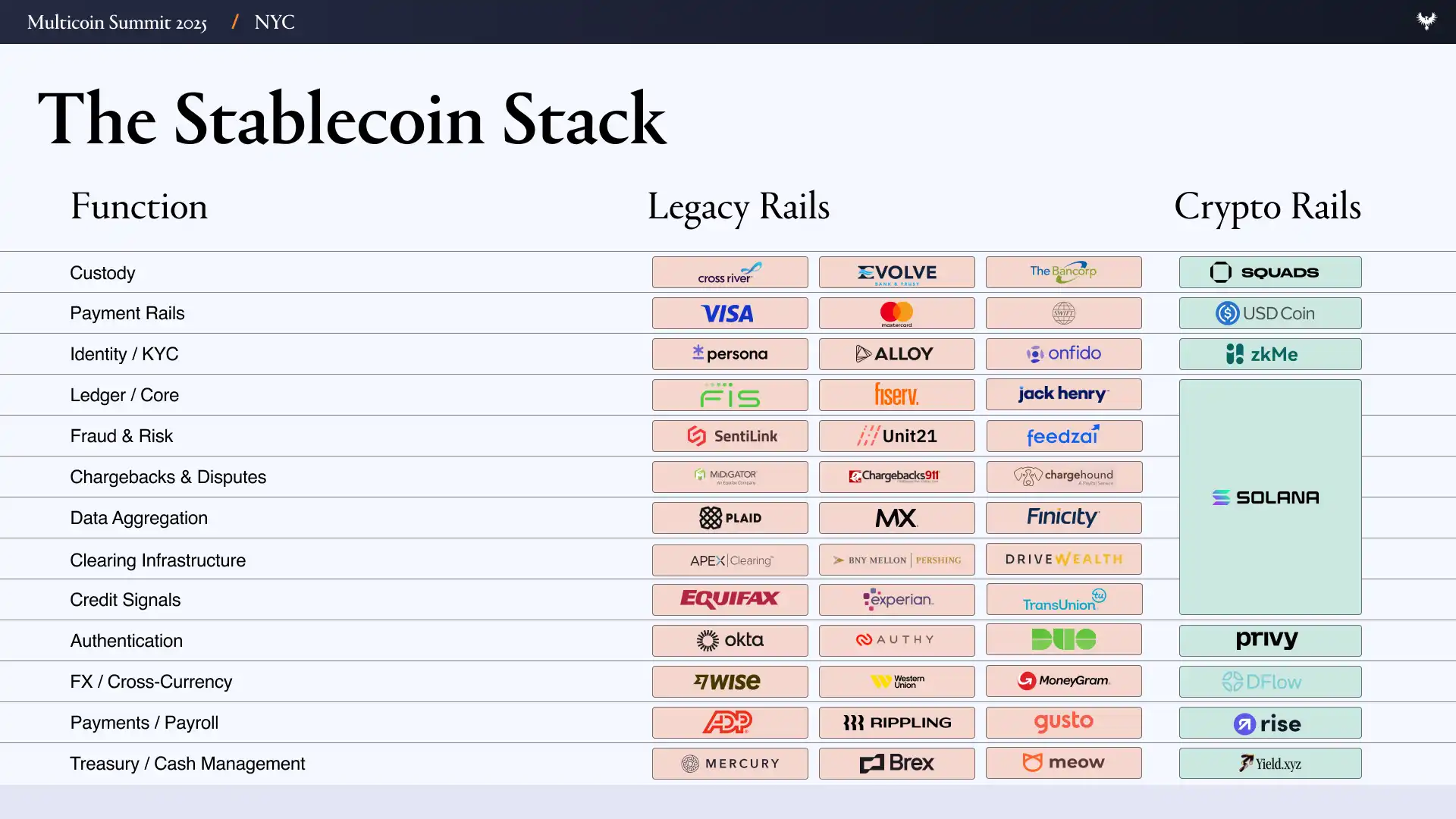

To understand the practical importance of this shift, we need to first understand how fintech is currently built. A typical fintech company relies on a vast vendor stack, including the following layers:

- User Interface/User Experience (UI/UX)

- Banking and Custody Layer: Evolve, Cross River, Synapse, Treasury Prime

- Payment Networks: ACH, Wire, SWIFT, Visa, Mastercard

- Identity and Compliance: Ally, Persona, Sardine

- Fraud Prevention: SentiLink, Socure, Feedzai

- Underwriting/Credit Infrastructure: Plaid, Argyle, Pinwheel

- Risk and Fund Management Infrastructure: Alloy, Unit21

- Capital Markets: Prime Trust, DriveWealth

- Data Aggregation: Plaid, MX

- Compliance/Reporting: FinCEN, OFAC checks

Launching a fintech company on this stack means managing contracts, audits, incentive structures, and potential failure modes across dozens of partners. Each layer adds cost and latency, and many teams spend almost as much time coordinating infrastructure as they do building their product.

Stablecoin-based systems dramatically simplify this complexity. Functions that once required multiple vendors can now be achieved with a handful of on-chain primitives.

In a world centered around stablecoins and permissionless finance, the following changes are occurring:

- Banking and Custody: Replaced by decentralized solutions like Altitude.

- Payment Networks: Replaced by stablecoins.

- Identity and Compliance: Still needed, but we believe this can be achieved on-chain with confidentiality and security through technologies like zkMe.

- Underwriting and Credit Infrastructure: Radically reinvented and moved on-chain.

- Capital Markets Firms: Become irrelevant when all assets are tokenized.

- Data Aggregation: Replaced by on-chain data and selective transparency (e.g., via Fully Homomorphic Encryption FHE).

- Compliance and OFAC Checks: Handled at the wallet level (e.g., if Alice's wallet is on a sanctions list, she cannot interact with the protocol).

The real difference with FinTech 4.0 is that the underlying architecture of finance is finally changing. Instead of developing an application that needs to quietly seek permission from a bank in the background, people are now directly replacing the bank's core functions with stablecoins and open payment networks. Developers are no longer tenants; they become the true owners of the "land."

Opportunities for Stablecoin-Focused FinTech

The first-order effect of this shift is obvious: the number of fintech companies will explode. When custody, lending, and fund transfers become almost free and instantaneous, starting a fintech company will become as easy as launching a SaaS product. In a stablecoin-centric world, there's no need for complex integrations with sponsor banks, no card-issuing intermediaries, no multi-day clearing processes, or redundant KYC (Know Your Customer) checks to slow things down.

We believe the fixed cost of creating a finance-centric fintech product will plummet from millions of dollars to thousands of dollars. As infrastructure, customer acquisition cost (CAC), and compliance barriers disappear, startups will be able to profitably serve smaller, more specific communities through what we call "stablecoin-focused fintech."

This trend has clear historical precedents. The previous generation of fintech companies initially emerged by serving specific customer segments: SoFi focused on student loan refinancing, Chime offered early wage access, Greenlight targeted teens with debit cards, and Brex served entrepreneurs who couldn't get traditional business credit. But this focused model did not become a lasting operating model. Constrained interchange revenue, rising compliance costs, and dependence on sponsor banks forced these companies to expand beyond their original niches. To survive, teams were forced to scale horizontally, adding products users didn't need, just to make the infrastructure viable at scale.

Now, with crypto payment networks and permissionless financial APIs drastically reducing startup costs, a new wave of stablecoin neobanks will emerge, each targeting a specific user group, much like the early fintech innovators. With significantly lower operating costs, these neobanks can focus on narrower, more specialized markets and remain focused, such as Sharia-compliant finance, lifestyle services for crypto enthusiasts, or services designed for the unique income and spending patterns of athletes.

More importantly, specialization also significantly optimizes unit economics. Customer acquisition costs (CAC) decrease, cross-selling becomes easier, and lifetime value (LTV) per customer increases. Focused fintech companies can precisely target products and marketing to niche groups that convert efficiently and benefit from more word-of-mouth within their specific communities. These businesses spend less on operations yet can extract more value from each customer than the previous generation of fintech companies.

When anyone can launch a fintech company in a few weeks, the question shifts from "Who can reach the customer?" to "Who truly understands the customer?"

Exploring the Design Space for Focused FinTech

The most attractive opportunities often arise where traditional payment networks fail.

Take adult content creators and performers, for example, who generate billions in annual income but are often "de-banked" due to reputational risk or chargeback risk. Their income payments can be delayed for days, even held for "compliance review," and typically incur 10%-20% fees through high-risk payment gateways (like Epoch, CCBill, etc.). We believe stablecoin-based payments can offer instant, irreversible settlement, support programmable compliance, allow performers to self-custody income, automatically allocate income to tax or savings accounts, and receive payments globally without relying on high-risk intermediaries.

Consider professional athletes, especially in individual sports like golf and tennis, who face unique cash flow and risk dynamics. Their income is concentrated in a short career span and often needs to be shared with agents, coaches, and team members. They need to pay taxes in multiple states and countries, and injuries can completely interrupt income. A stablecoin-based fintech could help them tokenize future earnings, use multi-signature wallets to pay their team, and automatically withhold taxes according to different regional requirements.

Luxury and watch dealers are another market poorly served by traditional financial infrastructure. These businesses often move high-value inventory across borders, typically through wire transfers or high-risk payment processors for six-figure transactions, while waiting days for settlement. Their working capital is often locked up in inventory in safes or display cases rather than bank accounts, making short-term financing expensive and difficult to obtain. We believe a stablecoin-based fintech could directly address these issues: instant settlement for large transactions, credit lines collateralized by tokenized inventory, and programmable escrow with built-in smart contracts.

When you examine enough of these cases, the same limitations appear repeatedly: traditional banks do not serve users with globalized, irregular, or non-traditional cash flows. But these groups can become profitable markets through stablecoin payment networks. Here are some theoretical examples of focused stablecoin fintech that we find attractive:

- Professional Athletes: Income concentrated in a short career; frequent travel and relocation; may need to file taxes in multiple jurisdictions; need to pay coaches, agents, trainers, etc.; may want to hedge injury risk.

- Adult Performers and Creators: Excluded by banks and card payment processors; global audience.

- Unicorn Company Employees: Cash-poor, net worth concentrated in illiquid equity; face high taxes when exercising options.

- On-Chain Developers: Net worth concentrated in highly volatile tokens; face fiat off-ramp and tax issues.

- Digital Nomads: Banking without a passport, automatic forex exchange; automated tax handling based on location; frequent travel and relocation.

- Prisoners: Difficult and expensive for family or friends to deposit money through traditional channels; funds often don't arrive timely.

- Sharia-Compliant Finance: Avoid interest-based transactions.

- Gen Z: Light-credit banking; gamified investing; social features.

- Cross-Border SMEs: High FX fees; slow settlement; working capital frozen.

- Crypto Degens: Use credit card bills to pay for high-risk speculative trading.

- International Aid: Aid funds move slowly, are restricted by intermediaries, and lack transparency; significant funds lost to fees, corruption, and misallocation.

- Tandas / Rotating Savings Clubs: Cross-border savings for globalized families; pooled savings for yield; can build on-chain income history for credit assessment.

- Luxury Dealers (e.g., Watch Dealers): Working capital locked in inventory; need short-term loans; conduct large, high-value cross-border transactions; often transact via chat apps like WhatsApp and Telegram.

Conclusion

Over the past two decades, fintech innovation has mostly focused on distribution, not infrastructure. Companies competed on branding, user onboarding, and paid acquisition, but the money itself still moved through the same closed payment networks. This expanded access to financial services but also led to homogenization, rising costs, and razor-thin margins that were hard to escape.

Stablecoins promise to radically change the economics of financial products. By turning custody, settlement, credit, and compliance into open, programmable software, they dramatically lower the fixed costs of launching and operating a fintech company. Functions that once required sponsor banks, card networks, and a vast vendor stack can now be built directly on-chain, with drastically reduced operational costs.

When infrastructure gets cheaper, focus becomes possible. Fintech companies no longer need millions of users to be profitable. Instead, they can focus on small, well-defined communities that are poorly served by one-size-fits-all products. Groups like athletes, adult creators, K-pop fans, or luxury watch dealers already share common cultural contexts, trust bases, and behavioral patterns, allowing products to spread more naturally through word-of-mouth rather than relying on paid marketing.

Equally important, these communities often share similar cash flow patterns, risks, and financial decisions. This consistency allows products to be designed around how people actually earn, spend, and manage money, rather than abstract user profiles. Word-of-mouth works not just because users know each other, but because the product genuinely fits how the group operates.

If this vision materializes, the economic implications are profound. As distribution becomes more community-aligned, customer acquisition costs (CAC) will fall; and as intermediaries are removed, profit margins will improve. Markets that once seemed too small or uneconomical will transform into sustainable and profitable business models.

In such a world, the advantage in fintech will no longer rely on simple scale and high marketing spend, but shift to a deep understanding of user context. The success of the next generation of fintech will lie not in trying to serve everyone, but in serving specific groups exceptionally well, based on how money actually moves for them.