Authors: Jacob Zhao, Jiawei, Turbo

On February 3, 2026, Vitalik published an important reflection on Ethereum's scaling roadmap on X. As the practical difficulty of Layer 2s evolving towards a fully decentralized form is being re-recognized, and the mainnet's own throughput capacity is expected to significantly increase in the coming years, the original assumption of relying solely on L2s for throughput scaling is being revised. L1 and L2 are forming a new 'settlement-service' synergy paradigm: L1 focuses on providing the highest level of security, censorship resistance, and settlement sovereignty, while L2s evolve into 'differentiated service providers' (e.g., privacy, AI, high-frequency trading). Ethereum's strategic focus is returning to the mainnet itself, strengthening its positioning as the world's most trusted settlement layer. Scaling is no longer the sole goal; security, neutrality, and predictability are once again becoming Ethereum's core assets.

Core Changes:

- Ethereum is entering an "L1 First Paradigm": With direct mainnet scaling and continuously decreasing fees, the original assumption that L2s would bear the core role of scaling no longer holds.

- L2s are no longer "branded shards" but a spectrum of trust: The decentralization of L2s is progressing much slower than expected, making it difficult to uniformly inherit Ethereum's security. Their role is being redefined as networks with varying levels of trust.

- Ethereum's core value shifts from "throughput" to "settlement sovereignty": The value of ETH is no longer limited to Gas or Blob revenue, but lies in its institutional premium as the world's most secure EVM settlement layer and native monetary asset.

- Scaling strategy is adjusting towards protocol internalization: Building on continued direct L1 scaling, the exploration of native verification and security mechanisms at the protocol layer may reshape the security boundaries and value capture structure between L1 and L2.

- Valuation framework undergoes structural migration: The weight of security and institutional credibility increases significantly, while the weight of fee revenue and platform effects decreases. ETH's pricing is shifting from a cash flow model to an asset premium model.

This article will analyze the paradigm shift in Ethereum's pricing model and valuation restructuring through a layered approach: facts (technological and institutional changes that have occurred), mechanisms (impact on value capture and pricing logic), and implications (meanings for allocation and risk-return).

I. Return to Origin: Ethereum's Values

Understanding Ethereum's long-term value lies not in short-term price fluctuations, but in its consistent design philosophy and value orientation.

- Credible Neutrality: Ethereum's core goal is not efficiency or profit maximization, but to become a set of credibly neutral infrastructure—rules are public, predictable, do not favor any participant, are not controlled by a single entity, and anyone can participate without permission. The security of ETH and its on-chain assets ultimately relies on the protocol itself, not any institutional credit.

- Ecosystem First, Not Revenue First: Ethereum's key upgrades consistently demonstrate a decision-making logic—actively sacrificing short-term protocol revenue in exchange for lower usage costs, a larger ecosystem scale, and stronger system resilience. Its goal is not to "collect tolls" but to become an irreplaceable neutral settlement and trust foundation for the digital economy.

- Decentralization as a Means: The mainnet focuses on the highest level of security and finality, while Layer 2 networks exist on a spectrum of connectivity to the mainnet with varying degrees: some inherit the mainnet's security and pursue efficiency, while others position themselves with differentiated functionalities. This enables the system to serve both global settlement and high-performance applications, rather than L2s being mere "branded shards".

- Long-termist Technical Roadmap: Ethereum adheres to a slow and certain evolution path, prioritizing system security and credibility. From the PoS transition to subsequent scaling and confirmation mechanism optimizations, its roadmap pursues sustainable, verifiable, and irreversible correctness.

Security Settlement Layer: Refers to the Ethereum mainnet providing irreversible finality services for Layer 2 and on-chain assets through decentralized validator nodes and consensus mechanisms.

This positioning as a Security Settlement Layer signifies the establishment of "settlement sovereignty," marking a shift from a "confederation" to a "federation" for Ethereum—a "constitutional moment" in the establishment of the Ethereum digital nation, and a crucial upgrade to Ethereum's architecture and core.

After the American Revolutionary War, under the Articles of Confederation, the 13 states were like a loose alliance, each printing its own currency and imposing tariffs on each other. Each state free-rode: enjoying common defense but refusing to pay; benefiting from the union's brand but acting independently. This structural problem led to reduced national credit and an inability to conduct unified foreign trade, severely hindering the economy.

1787 was America's "constitutional moment." The new Constitution granted the federal government three key powers: the power to levy taxes directly, regulate interstate commerce, and issue a unified currency. But what truly brought the federal government "to life" was Alexander Hamilton's economic plan in 1790: the federal assumption of state debts, redemption at face value to rebuild national credit, and the establishment of a national bank as the financial hub. The unified market unleashed economies of scale, national credit attracted more capital, and infrastructure construction gained financing capabilities. The US transformed from 13 small, mutually defensive states into the world's largest economy.

The structural dilemma of today's Ethereum ecosystem is entirely consistent.

Each L2 is like a "sovereign state," with its own user base, liquidity pools, and governance tokens. Liquidity is fragmented, cross-L2 interaction friction is high. L2s enjoy Ethereum's security layer and brand but cannot feed value back to L1. It is short-term rational for each L2 to lock liquidity on its own chain, but when all L2s do this, the Ethereum ecosystem's core competitive advantage is lost.

The roadmap Ethereum is advancing now is essentially its constitution-making and establishment of a central economic system, i.e., establishing "settlement sovereignty":

- Native Rollup Precompile = Federal Constitution. L2s can freely build differentiated functionalities outside the EVM, while the EVM part can obtain Ethereum-level security verification through native precompiles. Not integrating is possible, but at the cost of losing trustless interoperability with the Ethereum ecosystem.

- Synchronous Composability = Unified Market. Through mechanisms like native rollup precompiles, trustless interoperability and synchronous composability between L2s, and between L2s and L1, are becoming possible. This directly eliminates "interstate trade barriers"; liquidity is no longer trapped on isolated islands.

- L1 Value Capture Reconstruction = Federal Taxation Power. When all critical cross-L2 interactions return to L1 for结算, ETH once again becomes the settlement hub and trust anchor for the entire ecosystem. Whoever controls the settlement layer captures the value.

Ethereum is using a unified settlement and verification system to turn the fragmented L2 ecosystem into an irreplaceable "digital nation." This is a historical inevitability. Of course, the transition process may be slow, but history tells us that once this transition is complete, the unleashed network effects will far exceed the linear growth of the fragmented era. The US used a unified economic system to turn 13 small states into the world's largest economy. Ethereum will also transform the loose L2 ecosystem into the largest security settlement layer, and even a global financial carrier.

Ethereum Core Upgrade Roadmap and Valuation Impact (2025-2026)

II. Valuation Misconception: Why Ethereum Should Not Be Viewed as a "Tech Company"

Applying traditional corporate valuation models (P/E, DCF, EV/EBITDA) to Ethereum is essentially a category error. Ethereum is not a company aiming for profit maximization but an open digital economic infrastructure. Companies pursue shareholder value maximization, while Ethereum pursues the maximization of ecosystem scale, security, and censorship resistance. To achieve this goal, Ethereum has repeatedly actively reduced protocol revenue (e.g., through EIP-4844 introducing Blob DA, structurally lowering L2 data publishing costs, and suppressing L1 fee income from rollup data)—akin to "revenue self-destruction" from a corporate perspective, but from an infrastructure perspective, it is sacrificing short-term fees for long-term neutrality premium and network effects.

A more reasonable understanding framework is to view Ethereum as a global neutral settlement and consensus layer: providing security, finality, and trusted coordination for the digital economy. The value of ETH is reflected in multiple structural demands—the rigid demand for final settlement, the scale of on-chain finance and stablecoins, the impact of staking and burn mechanisms on supply, and the long-term, sticky capital brought by institutional-level adoption such as ETFs, corporate treasuries, and RWA.

III. Paradigm Restructuring: Finding Pricing Anchors Beyond Cash Flow

At the end of 2025, the Hashed team launched ethval.com, providing Ethereum with a detailed, reproducible quantitative model collection. However, traditional static models struggle to capture the dramatic narrative shift of Ethereum in 2026. Therefore, we reused its systematic, transparent, and reproducible underlying models (covering yield, monetary, network effects, and supply structure) but reshaped the valuation architecture and weighting logic:

- Structural Restructuring: Map the models to the four major value quadrants: "Security, Monetary, Platform, Revenue," and price by category summation.

- Weight Rebalancing: Significantly increase the weight of security and settlement premium, while weakening the marginal contribution of protocol revenue and L2 expansion.

- Risk Control Overlay: Introduce a macro and on-chain risk-aware circuit breaker mechanism, making the valuation framework adaptable across cycles.

- Eliminate "Circular Reasoning": Models containing current price inputs (e.g., Staking Scarcity, Liquidity Premium) are no longer used as fair value anchors, retaining their role as indicators for position and risk appetite adjustment.

Note: The following models are not for precise point prediction but for depicting the relative pricing direction of different value sources across different cycles.

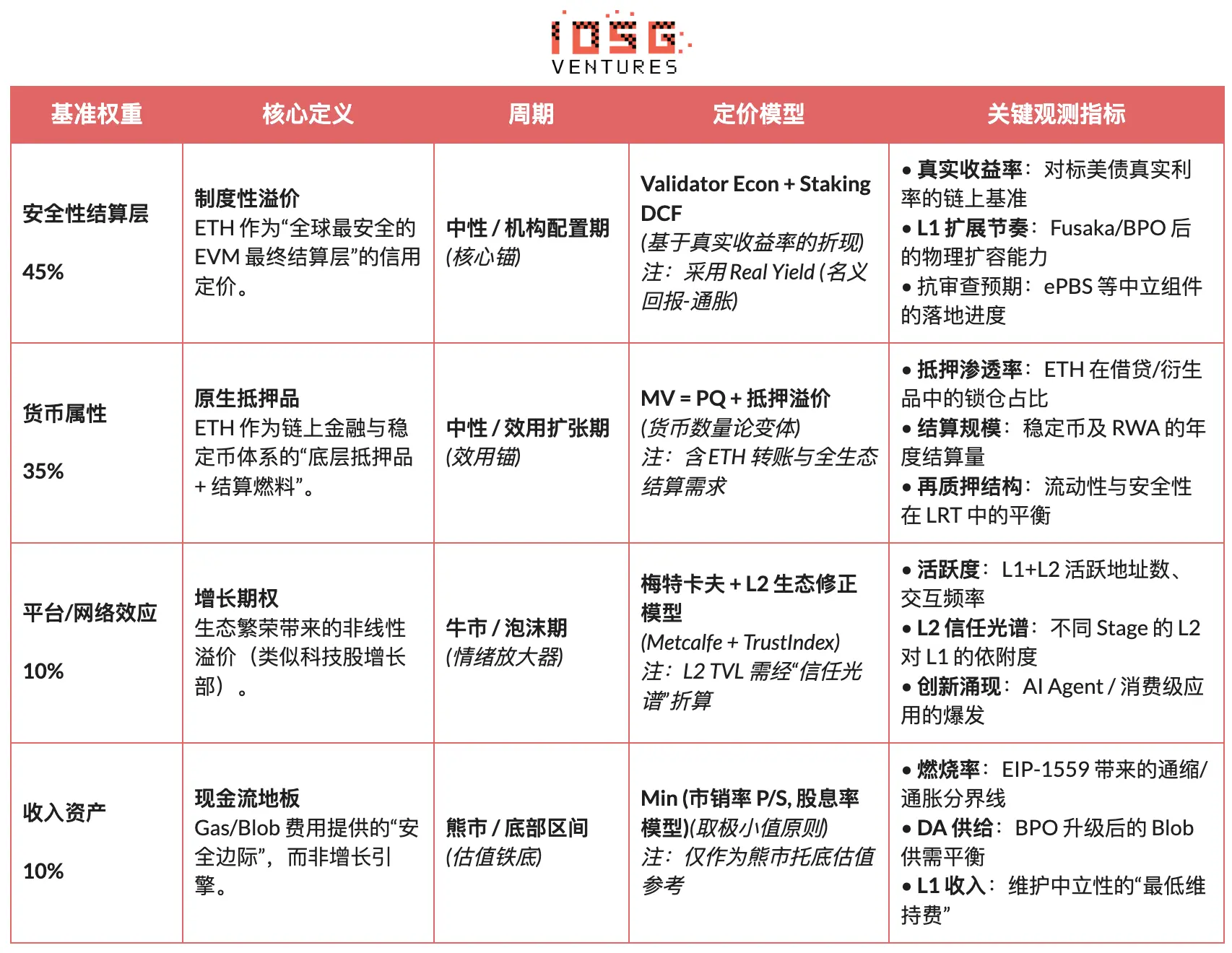

1. Security Settlement Layer: Core Value Anchor (45%, Upweighted in Risk-Off Periods)

We regard the Security Settlement Layer as Ethereum's most core source of value, assigning it a baseline weight of 45%; this weight is further increased during periods of rising macro uncertainty or falling risk appetite. This judgment stems from Vitalik's latest definition of "truly scaling Ethereum": the essence of scaling is not increasing TPS, but creating block space fully backed by Ethereum itself. Any high-performance execution environment relying on external trust assumptions does not constitute an extension of the Ethereum本体 (ontology).

Under this framework, the value of ETH primarily manifests as the credit premium of a global sovereignless settlement layer, rather than protocol revenue. This premium is supported by structural factors such as validator scale and degree of decentralization, long-term security record, institutional adoption, clarity of compliance path, and protocol-native Rollup verification mechanisms.

For specific pricing, we mainly use two complementary methods: Validator Economics (yield equilibrium mapping) and Staking DCF (perpetual staking discounting), jointly depicting ETH's institutional premium as the "global security settlement layer."

- Validator Economics (Yield Equilibrium Pricing): Based on the ratio of the annualized staking cash flow per ETH to the target real yield, deriving a theoretical fair price:

Fair Price = (Annual Staking Cash Flow per ETH) / Target Real Yield

This expression is used to depict the equilibrium relationship between yield and price, serving as a directional relative valuation tool, not an independent pricing model.

- Staking DCF (Perpetual Staking Discounted Cash Flow): Treating ETH as a long-term asset that can sustainably generate real staking yield, discounting its cash flow in perpetuity:

M_staking = Total Real Staking Cash Flow / (Discount Rate − Long-term Growth Rate)

ETH Price (staking) = M_staking / Circulating Supply

Essentially, this value layer is not对标 (benchmarked against) the revenue capability of platform companies but is similar to the settlement credit of a global clearing network.

2. Monetary属性 (Properties): Settlement and Collateral (35%, Dominant in Utility Expansion Periods)

We regard monetary properties as Ethereum's second core source of value, assigning it a baseline weight of 35%, becoming the primary utility anchor in neutral markets or during on-chain economic expansion phases. This judgment is not based on the narrative that "ETH is equivalent to the USD," but rather its structural role as the native settlement fuel and ultimate collateral asset within the on-chain financial system. The security of stablecoin circulation, DeFi liquidation, and RWA settlement all rely on the settlement layer supported by ETH.

For pricing, we use an extended form of the Equation of Exchange (MV = PQ), but model the usage scenarios of ETH in layers to account for the orders-of-magnitude differences in velocity across different scenarios Layered Monetary Demand Model:

- High-Frequency Settlement Layer (Gas payments, stablecoin transfers)

- M_transaction = Annual Transaction Settlement Volume / V_high

- V_high ≈ 15-25 (referencing historical on-chain data)

Medium-Frequency Financial Layer (DeFi interactions, lending liquidations)

- M_defi = Annual DeFi Settlement Volume / V_medium

- V_medium ≈ 3-8 (based on capital turnover rates of major DeFi protocols)

Low-Frequency Collateral Layer (Staking, restaking, long-term locking)

- M_collateral = Total ETH Collateral Value × (1 + Liquidity Premium)

- Liquidity Premium = 10-30% (reflecting compensation for liquidity sacrifice)

3. Platform / Network Effects: Growth Option (10%, Bull Market Amplifier)

Platform and network effects are treated as growth options within Ethereum's valuation, assigned only a 10% weight, used to explain the non-linear premium brought by ecosystem expansion during bull markets. We use a trust-adjusted Metcalfe's Law model, avoiding equally weighting L2 assets of different security levels into the valuation:

- Metcalfe's Law Model: M_network = a × (Active Users)^b + m × Σ (L2 TVL_i × TrustScore_i)

- Platform/Network Effect Valuation Price: ETH Price(network) = M_network / Circulating Supply

4. Revenue Asset: Cash Flow Floor (10%, Bear Market Support)

We treat protocol revenue as the cash flow floor within Ethereum's valuation system, not a growth engine, also assigned a 10% weight. This layer primarily functions during bear markets or extreme risk phases, used to depict the valuation下限 (lower bound).

Gas and Blob fees provide the minimum operating cost for the network and influence the supply structure through EIP-1559. For valuation, we use Price-to-Sales (P/S) and Fee Yield models, taking conservative values from them, serving only as a bottom reference. As the mainnet continues to scale, the importance of protocol revenue relatively declines, with its core role reflected in the safety margin during downturns.

- Price-to-Sales Model (P/S Floor): M_PS = Annual Protocol Revenue × P/S_multiple

- P/S Valuation Price: ETH Price (PS) = M_PS / Circulating Supply

- Fee Yield Model: M_Yield = Annual Protocol Revenue / Target Fee Yield

- Fee Yield Valuation Price: ETH Price(Yield) = M_Yield / Circulating Supply

- Cash Flow Floor Pricing (take the minimum of both): P_Revenue_Floor = min(P_PS , P_Yield)

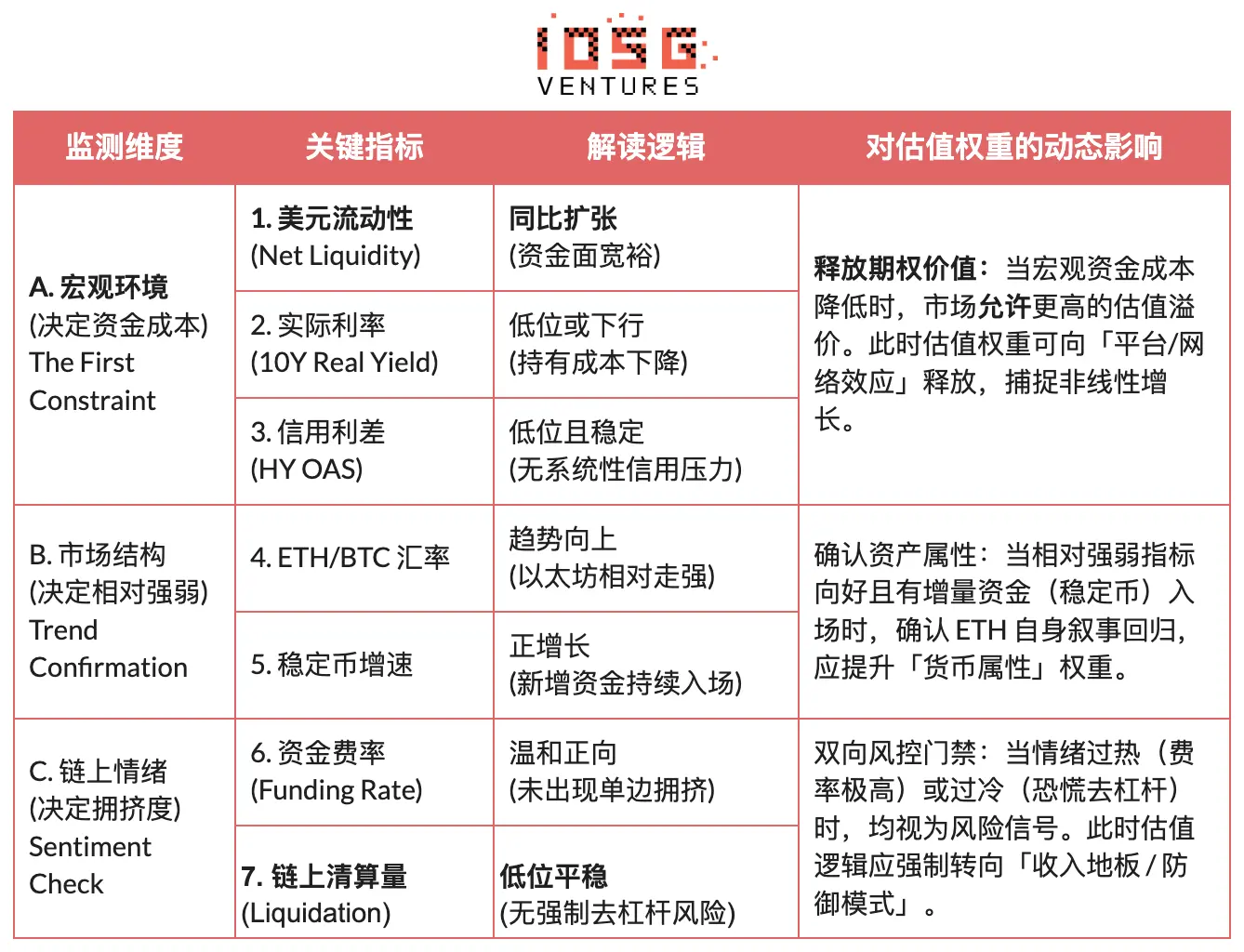

IV. Dynamic Calibration: Macro Constraints and Cycle Adaptation

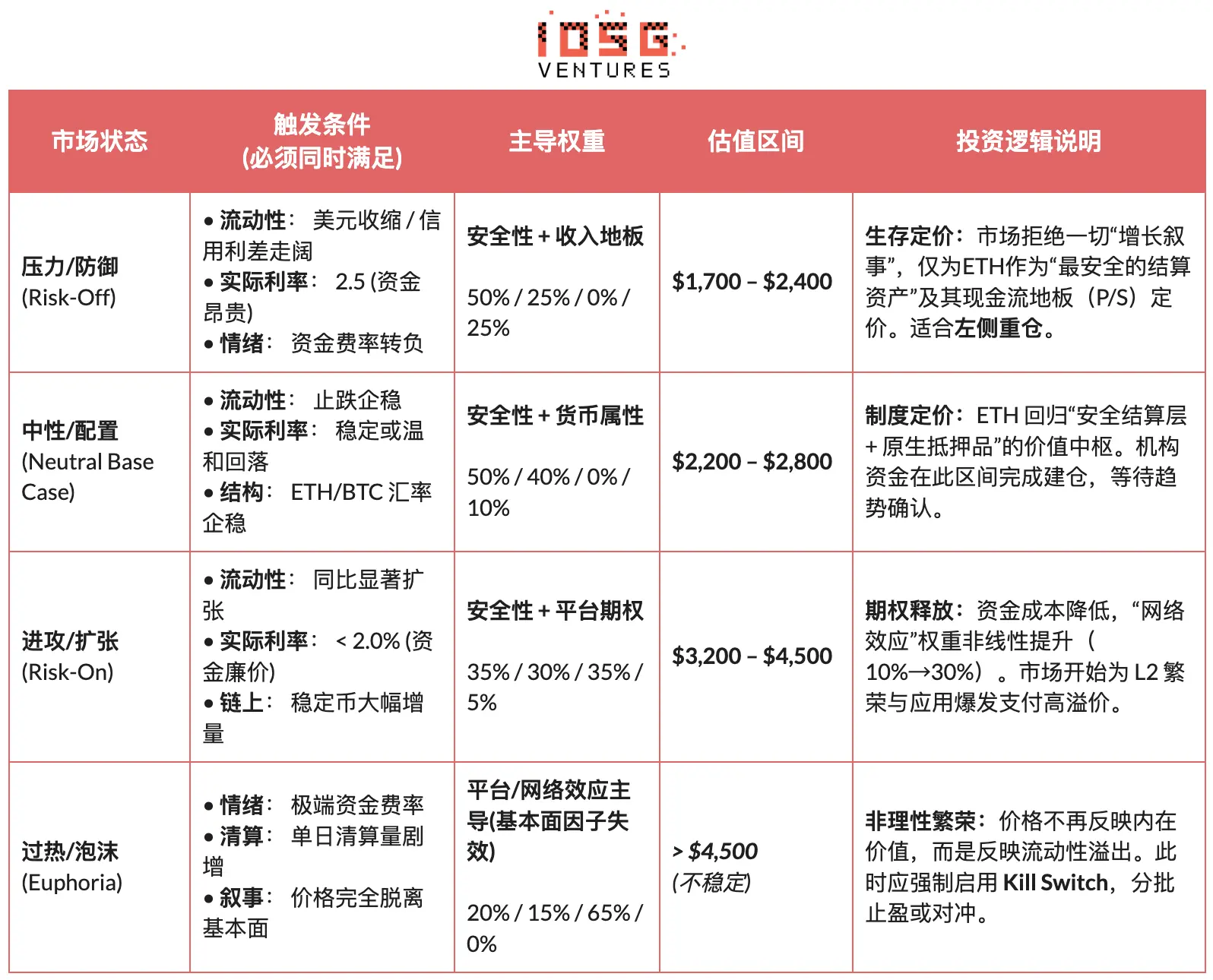

If the previous sections established Ethereum's "intrinsic value center," this chapter introduces an "external environment adaptation system" independent of fundamentals. Valuation cannot operate in a vacuum and must be constrained by three external factors: the macro environment (cost of capital), market structure (relative strength), and on-chain sentiment (crowding). Based on this, we constructed a state adaptation (Regime Adaptation) mechanism, dynamically adjusting valuation weights across different cycles—releasing option premium during宽松期 (loose periods) and retreating to the revenue floor during避险期 (risk-off periods)—thus achieving a leap from static models to dynamic strategies. (Note: Limited by space, this article only presents the core logical framework of this mechanism.)

V. Conditional Path for the Institutionalization Second Curve

The previous analyses were all based on the internal logic of the crypto system—technology, valuation, and cycles. This chapter discusses a different level of problem: when ETH is no longer priced solely by crypto-native capital but is gradually incorporated into the traditional financial system, how will its pricing power, asset attributes, and risk structure change? The institutionalization second curve is not an extension of existing logic but a redefinition of Ethereum by exogenous forces:

- Change in Asset Attributes (Beta → Carry): Spot ETH ETFs solve compliance and custody issues, essentially仍是 (still being) price exposure; whereas the future advancement of Staking ETFs introduces on-chain yield into the institutional system for the first time through compliant vehicles. ETH thus transitions from an "interest-free, high-volatility asset" to a "configurable asset with predictable yield," potentially expanding its buyer base from trading capital to yield- and duration-sensitive pensions, insurance, and long-term accounts.

- Change in Usage Mode (Holding → Using): If institutions no longer see ETH merely as a tradable asset but begin to use it as settlement and collateral infrastructure. Whether it's JPMorgan's tokenized funds or the deployment of compliant stablecoins and RWA on Ethereum, it indicates that the demand for ETH is shifting from "holding demand" to "operational demand"—institutions not only hold ETH but also use it to complete settlement, clearing, and risk management.

- Change in Tail Risk (Uncertainty → Pricing): As stablecoin regulatory frameworks (like the GENIUS Act) are未来 (future) gradually established, and Ethereum's roadmap and governance transparency improve, the regulatory and technical uncertainties most sensitive to institutions are being systematically compressed, meaning uncertainty begins to be priced in rather than avoided.

The so-called "institutionalization second curve" is a change in the nature of demand, providing a source of real demand for the "Security Settlement Layer + Monetary Properties" valuation logic, pushing ETH to transition from an emotion-driven speculative asset to a foundational asset carrying both allocative and functional demand.

VI. Conclusion: Anchoring Value in the Darkest Hour

Over the past week, the industry has experienced a severe deleveraging洗礼 (baptism), with market sentiment freezing over. This is undoubtedly a "darkest hour" for the crypto world. Pessimism is蔓延 (spreading) among practitioners, and Ethereum, as the asset最能代表 (best representing) the crypto spirit, is also at the eye of the storm of controversy.

However, as rational observers, we need to see through the fog of panic: what Ethereum is experiencing is not a "collapse of value" but a profound "migration of the pricing anchor." With direct L1 scaling推进 (advancing), L2s being redefined as networks with varying trust levels, and protocol revenue actively yielding to system security and neutrality, ETH's pricing logic has structurally shifted towards "Security Settlement Layer + Native Monetary Properties."

Against the backdrop of high macro real interest rates,尚未宽松 (not yet loose) liquidity, and on-chain growth options not yet allowed to be priced by the market, ETH's price naturally converges to a structural value range supported by settlement certainty, verifiable yield, and institutional consensus. This range is not an emotional bottom but the value center after剥离 (stripping away) platform-type growth premium.

As long-term builders in the Ethereum ecosystem, we refuse to be "mindless bulls" on ETH. We hope to rigorously argue our predictions through a严谨的 (rigorous) logical framework: only when macro liquidity, risk appetite, and network effects simultaneously meet the trigger conditions of the market state will higher valuations be重新计入 (repriced in) by the market.

Therefore, for long-term investors, the key question is no longer anxiously asking "can Ethereum still rise?", but to清醒地认识到 (clearly recognize)—in the current environment, which layer of core value are we buying at "floor price"?

Disclaimer: This article was created with the assistance of AI tools such as ChatGPT-5.2, Gemini 3, and Claude Opus 4.5. The authors have尽力 (made their best effort) to proofread and ensure the information is true and accurate, but疏漏 (omissions) may still occur. Please understand. It is特别提示 (specially noted) that the crypto asset market普遍存在 (commonly exhibits) a disconnect between project fundamentals and secondary market price performance. The content of this article is for information integration and academic/research exchange only, does not constitute any investment advice, and should not be regarded as a recommendation to buy or sell any token.