Original Title:: : [Issue] No Free Lunch: Reflections on Arbitrum and Optimism

Original Author:Four Pillars

Original Compilation:Ken,ChainCatcher

Key Summary

-

Base announced it would transition from Optimism's OP Stack to a proprietary unified architecture, delivering a strong shock to the market and severely impacting the $OP price.

-

Optimism has fully open-sourced its code under the MIT license and implements a revenue-sharing model for chains joining the "Superchain." Arbitrum adopts a "community source" model, requiring chains built on Orbit that settle outside the Arbitrum ecosystem to contribute 10% of protocol revenue.

-

The debate over open-source monetization in blockchain infrastructure is an extension of recurring issues in the traditional software field (e.g., Linux, MySQL, MongoDB, WordPress, etc.). However, the introduction of tokens as a variable adds a layer of stakeholder dynamics.

-

It is difficult to assert which side is absolutely right. What's important is to soberly understand the trade-offs contained in each model and, as an ecosystem, collectively consider the long-term sustainability of L2 infrastructure.

1. Base's Departure and the Superchain Rift

On February 18th, Coinbase's Ethereum L2 network Base announced it would cut its dependence on the Optimism OP Stack and transition to a proprietary unified codebase. The core idea is to integrate key components, including the sequencer, into a single repository while reducing external dependencies on Optimism, Flashbots, and Paradigm. The Base engineering team stated in an official blog post that this change would increase the annual hard fork frequency from three to six times, effectively speeding up upgrades.

The market reacted swiftly: $OP fell over 20% within 24 hours. This was not surprising, considering the largest chain in the Optimism Superchain ecosystem had just declared independence.

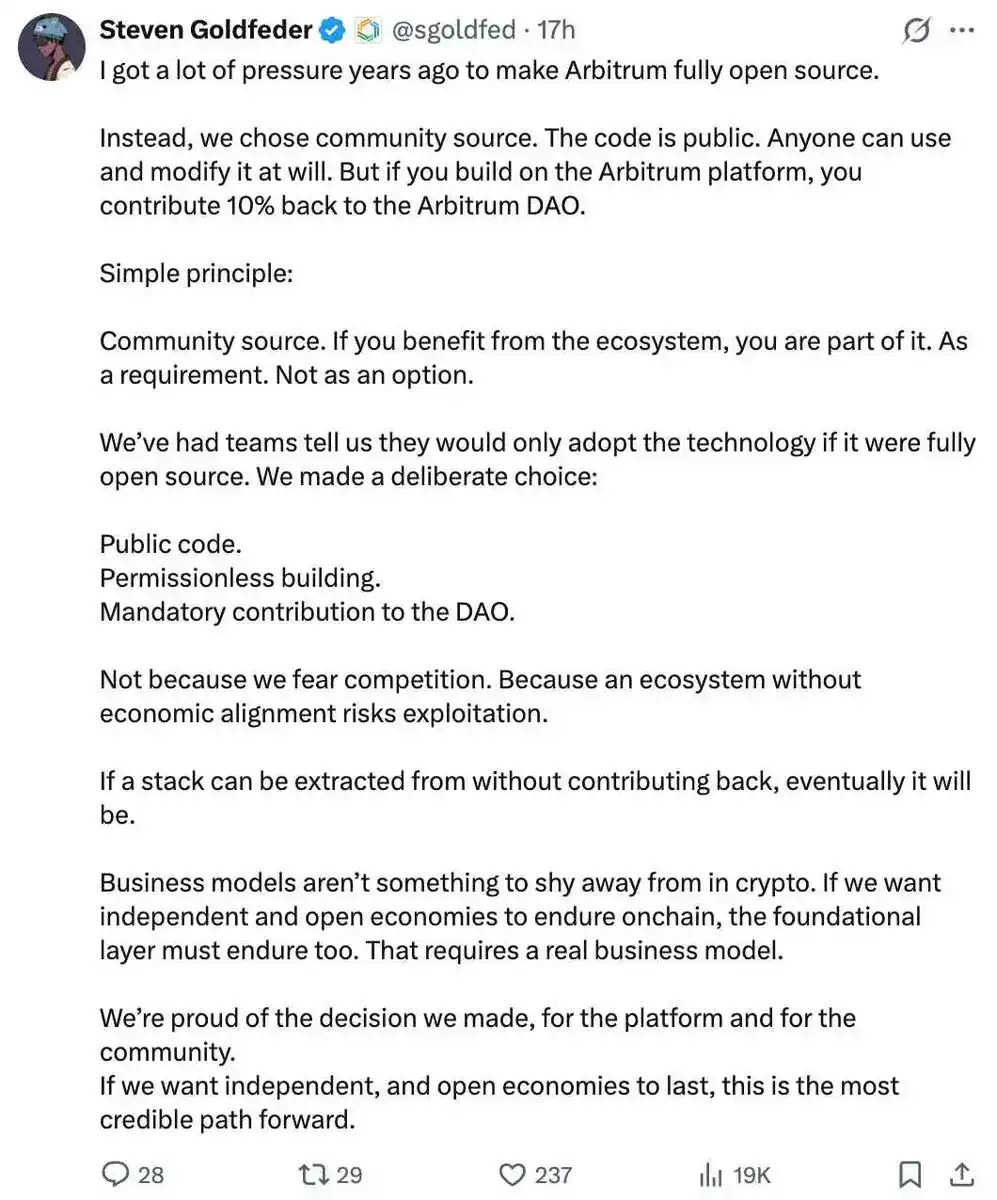

Around the same time, Arbitrum co-founder and Offchain Labs CEO Steven Goldfeder posted on platform X, reminding everyone that his team had deliberately chosen a different path years ago. His core point was that despite pressure to release the Arbitrum code as fully open source, the team insisted on their so-called "community source" model.

Under this model, the code itself is public, but any chain built on the Arbitrum Orbit stack that settles outside the Arbitrum ecosystem must contribute a fixed percentage of protocol revenue to the Arbitrum DAO. Goldfeder issued a sharp warning: "If a stack allows taking value without contributing, eventually this will happen."

Base's departure is more than just a technical migration. This event brings a fundamental question to the forefront: What kind of economic structure should blockchain infrastructure be built upon? This article will examine the economic frameworks adopted by Optimism and Arbitrum, explore their differences, and discuss the industry's future direction.

2. Two Models

Optimism and Arbitrum handle software very differently. Both are leading projects in the Ethereum L2 scaling space, but they diverge sharply in their approach to achieving economic sustainability for their ecosystems.

2.1 Optimism: Openness and Network Effects

Optimism's OP Stack is fully open source under the MIT license. Anyone can take the code, modify it freely, and build their own L2 chain. There are no royalties or revenue-sharing obligations.

Revenue sharing only kicks in when a chain joins Optimism's official ecosystem, the "Superchain." Members must contribute either 2.5% of链 revenue or 15% of net on-chain income (fee revenue minus L1 gas costs), whichever is higher, to the Optimism Collective. In return, they gain access to the Superchain's shared governance, shared security, interoperability, and brand resources.

The logic behind this approach is simple. If countless L2 chains are built on the OP Stack, these chains will form an interoperable network, and the value of the OP token and the entire Optimism ecosystem will rise through network effects. In practice, this strategy has yielded significant results. Major projects like Coinbase's Base, Sony's Soneium, Worldcoin's World Chain, and Uniswap's Unichain have all adopted the OP Stack.

The appeal of the OP Stack for large enterprises goes beyond the licensing model. In addition to the freedom offered by the MIT license, the OP Stack's modular architecture is a core competitive advantage. Since the execution layer, consensus layer, and data availability layer can be replaced independently, projects like Mantle and Celo can adopt modules like OP Succinct for zero-knowledge proofs and customize freely. For enterprise sovereignty, the ability to acquire code without external permission and freely replace internal components is highly attractive.

However, the structural weakness of this model is equally evident: low barriers to entry also mean low barriers to exit. Chains using the OP Stack have limited economic obligations to the Optimism ecosystem, and the more profitable a chain becomes, the more economically rational it is to operate independently. Base's departure is a textbook case of this dynamic.

2.2 Arbitrum: Enforced Alignment

Arbitrum has taken a more complex approach. For L3 chains built on Arbitrum Orbit that settle on Arbitrum One or Nova, there is no revenue-sharing obligation. However, according to the Arbitrum Expansion Program, chains that settle on networks other than Arbitrum One or Nova (whether L2 or L3) are required to contribute 10% of their net protocol revenue to Arbitrum. Of this 10%, 8% goes to the Arbitrum DAO treasury and 2% to the Arbitrum Developers Association.

In other words, chains that stay within the Arbitrum ecosystem enjoy freedom, while those that leverage Arbitrum technology and deploy in external ecosystems must contribute. It's a dual structure.

In the early days, building an Arbitrum Orbit L2 that settled directly on Ethereum required approval through a governance vote by the Arbitrum DAO. When the Arbitrum Expansion Program launched in January 2024, this process transitioned to a self-service model. Nonetheless, the early "permissioned" process and the emphasis on encouraging L3s may have been a barrier for large enterprises seeking sovereign L2 chains. For companies wanting to connect directly to Ethereum, the L3 structure built on top of Arbitrum One introduced additional business risks in terms of governance and technical dependency.

Goldfeder's decision to call this model "community source" is intentional. It positions itself as a third way between traditional open source and proprietary licensing. Code transparency is preserved, but commercial use outside the Arbitrum ecosystem must contribute back to it.

The strength of this model lies in aligning the economic interests of ecosystem participants. For chains settling externally, there is a tangible cost to exit, ensuring a sustainable revenue stream. Reportedly, the Arbitrum DAO has accumulated around 20,000 ETH in revenue, and Robinhood's recent announcement that it will build its own L2 chain on Orbit further validates the model's potential for institutional adoption. The Robinhood chain testnet recorded 4 million transactions in its first week, indicating that Arbitrum's technical maturity and regulatory-friendly customization capabilities offer meaningful value to certain types of institutional clients.

2.3 Trade-offs of Each Model

The two models optimize for different values. Optimism's model maximizes the speed of initial enterprise adoption through the unconditional openness of the MIT license, modular architecture, and the strong proof-of-concept represented by Base. An environment where code can be acquired without permission, components freely replaced, and mature reference cases exist offers the lowest barrier to entry for business decision-makers.

Arbitrum's model, on the other hand, emphasizes long-term ecosystem sustainability. Beyond superior technology, its economic alignment mechanism requires external users to contribute revenue, ensuring a stable funding base for infrastructure maintenance. Initial adoption speed might be slower, but for projects building on unique features of the Arbitrum stack, such as Arbitrum Stylus, the cost of exit could be significant.

That said, the difference between these two models is not as extreme as often portrayed. Arbitrum also offers free and permissionless licenses within its ecosystem, and Optimism requires revenue sharing from Superchain members. Both exist on a spectrum between "fully open" and "fully enforced," distinguished by degree and scope rather than nature.

Ultimately, this difference is the blockchain version of the classic trade-off between growth speed and sustainability.

3. Lessons from Open Source History

This tension is not unique to blockchain. The debate over open-source software monetization models has seen extremely similar arguments over the past few decades.

3.1 Linux and Red Hat

Linux is the most successful open-source project in history. The Linux kernel is fully open under the GPL license and has penetrated almost every area of computing: servers, cloud, embedded systems, Android, etc.

However, the most successful commercial enterprise built on this ecosystem, Red Hat, does not profit from the code itself. It profits from the services built on top of the code. Red Hat sells technical support, security patches, and stability guarantees to enterprise customers and was acquired by IBM for $34 billion in 2019. The code is free, but professional operational support is paid. This logic bears a striking resemblance to Optimism's recently launched OP Enterprise.

3.2 MySQL and MongoDB

MySQL introduced a dual-licensing model: an open-source version under the GPL license, and a separate commercial license sold to enterprises that wanted to use MySQL for commercial purposes. The code was visible and free for non-commercial use, but generating revenue from it required payment. This concept is similar to Arbitrum's community source model.

MySQL succeeded with this method, but not without side effects. When Oracle acquired Sun Microsystems in 2010 and随之 gained ownership of MySQL, concerns about MySQL's future led its original creator, Monty Widenius, and community developers to create the fork MariaDB. While the direct catalyst was the change in ownership structure rather than licensing policy, the possibility of forking is an ever-present risk in open-source software. The parallels to Optimism's current situation are evident.

MongoDB provides a more direct example. In 2018, MongoDB adopted the Server Side Public License. The motivation was to address a growing problem: cloud service giants like AWS and Google Cloud were using MongoDB's code, offering it as a managed service, without paying anything to MongoDB. Actors who take the value of open code without giving anything in return: this is a pattern that repeats itself throughout the history of open source.

3.3 WordPress

WordPress is fully open source under the GPL license and powers about 40% of websites globally. The company behind WordPress, Automattic, generates revenue through WordPress.com hosting services and various plugins, but charges nothing for the use of the WordPress core itself. The platform is completely open, with the logic that the growth of the ecosystem itself enhances the platform's value. This is structurally similar to Optimism's Superchain vision.

The WordPress model has clearly been successful. But the "free rider" problem was never fundamentally solved. In recent years, a dispute erupted between WordPress founder Matt Mullenweg and the major hosting company WP Engine. Mullenweg publicly criticized WP Engine for extracting huge revenues from the WordPress ecosystem while contributing insufficiently in return. The paradox of the biggest beneficiaries of an open ecosystem contributing the least: this is the exact same dynamic that occurred between Optimism and Base.

4. Why Crypto is Different

These debates are commonplace in traditional software. So why has this issue become particularly acute in blockchain infrastructure?

4.1 Tokens as Amplifiers

In traditional open-source projects, value is relatively dispersed. When Linux succeeds, no specific asset's price directly rises or falls as a result. But in a blockchain ecosystem, tokens exist, and tokens reflect the incentives and political dynamics of ecosystem participants in real-time through price.

In traditional open-source software, free riding leads to a shortage of development resources, which is serious but the consequences are gradual. In blockchain, the departure of a major player triggers an immediate and highly visible result: the token price plummets. The more than 20% drop in $OP following Base's announcement illustrates this clearly. Tokens are both a barometer of ecosystem health and a mechanism that amplifies crises.

4.2 The Responsibility of Financial Infrastructure

L2 chains are not just software. They are financial infrastructure. Billions of dollars in assets are managed on these chains, and maintaining their stability and security requires significant ongoing costs. In successful open-source projects, maintenance costs are often covered by corporate sponsorship or foundation support, but most L2 chains today are barely breaking even just running their own ecosystems. Without external contributions in the form of sequencer fee sharing, it is difficult to ensure the resources needed for infrastructure development and maintenance.

4.3 Ideological Tension

The crypto community has a strong ideological belief that "code should be free." Decentralization and freedom are core values tightly interwoven with the industry's identity. In this context, Arbitrum's fee-sharing model can cause resistance among some community members, while Optimism's open model is ideologically appealing but faces the practical challenge of economic sustainability.

5. Conclusion: No Free Infrastructure

Admittedly, Base's departure is a blow to Optimism, but it is too early to conclude that the Superchain model itself has failed based on this.

First, Optimism is not sitting idle. On January 29, 2026, Optimism officially launched OP Enterprise, an enterprise-grade service for fintech companies and financial institutions, supporting the deployment of production-ready chains in 8 to 12 weeks. While the original OP Stack is MIT-licensed and can always be converted to a self-managed mode, Optimism's assessment is that for most teams without blockchain infrastructure expertise, partnering with OP Enterprise is the more rational choice.

Base will also not cut ties with the OP Stack overnight. Base itself has stated that it will remain a core support services customer of OP Enterprise during the transition and plans to maintain compatibility with the OP Stack specification throughout the process. This separation is technical, not relational. This is the official position of both parties. On the other hand, Arbitrum's community source model also has a gap between ideal and reality.

In practice, the approximately 19,400 ETH in net fee revenue accumulated in the Arbitrum DAO treasury comes almost entirely from sequencer fees and Timeboost MEV auctions on Arbitrum One and Nova themselves. Fee-sharing revenue contributed by ecosystem chains through the Arbitrum Expansion Program has not been publicly confirmed at any meaningful scale. There are structural reasons for this. The Arbitrum Expansion Program itself was only launched in January 2024, most existing Orbit chains are L3s built on Arbitrum One and thus exempt from revenue-sharing obligations, and even the most prominent independent L2 eligible under the program—the Robinhood chain—is still in the testnet phase.

For Arbitrum's community source model to truly carry weight as a "sustainable revenue structure," the ecosystem needs to wait for large L2s like Robinhood to go live on mainnet and for Expansion Program fee-sharing revenue to actually start flowing. Demanding that 10% of protocol revenue be handed over to an external DAO is not an easy ask for large enterprises. That an institution like Robinhood still chooses Orbit speaks to the value proposition on other dimensions, namely customization potential and technical maturity. But the economic rationale of the model remains unproven. The gap between theoretical design and actual cash flow is a challenge that Arbitrum still needs to address.

The two models offered by Arbitrum and Optimism are, ultimately, different answers to the same question: how to ensure the sustainability of public infrastructure?

What matters is not which model is correct, but understanding the trade-offs each one brings. Optimism's open model enables rapid ecosystem expansion but carries the inherent risk that its biggest beneficiaries may leave. Arbitrum's enforced contribution model builds a sustainable revenue structure but raises the barrier to initial adoption.

Whether talking about Optimism or Arbitrum, OP Labs, Sunnyside Labs, and Offchain Labs employ world-class research talent working to scale Ethereum while maintaining decentralization. Their continued development input is indispensable for the technological advancement of L2 scaling, and the resources to fund this work must come from somewhere.

There is no free infrastructure. As a community, our task is not blind allegiance or knee-jerk resentment, but to start an honest conversation about who bears the cost of this infrastructure. Base's departure can be the starting point for this conversation.