Original author: @BlazingKevin_, Blockbooster researcher

On May 14, 2026, the U.S. Senate Banking Committee passed the CLARITY Act with a bipartisan vote of 15-9.

The most important content in this "legislative progress" is Section 404 of the bill text. This section was redrafted in the compromise text released by Senators Thom Tillis and Angela Alsobrooks on May 1st, doing two things the GENIUS Act did not do:

First, it extends the stablecoin yield prohibition to all Digital Asset Service Providers (DASPs) and their affiliates — including centralized exchanges, brokers, dealers, and custodians. When the GENIUS Act was signed in July 2025, it only constrained "stablecoin issuers" (PPSI/FPSI). Compliant workarounds used by Coinbase, Anchorage Digital Neo Ltd., and others to continue offering 3.5%-5% yields to users through "non-issuer payment" paths were all closed by Section 404.

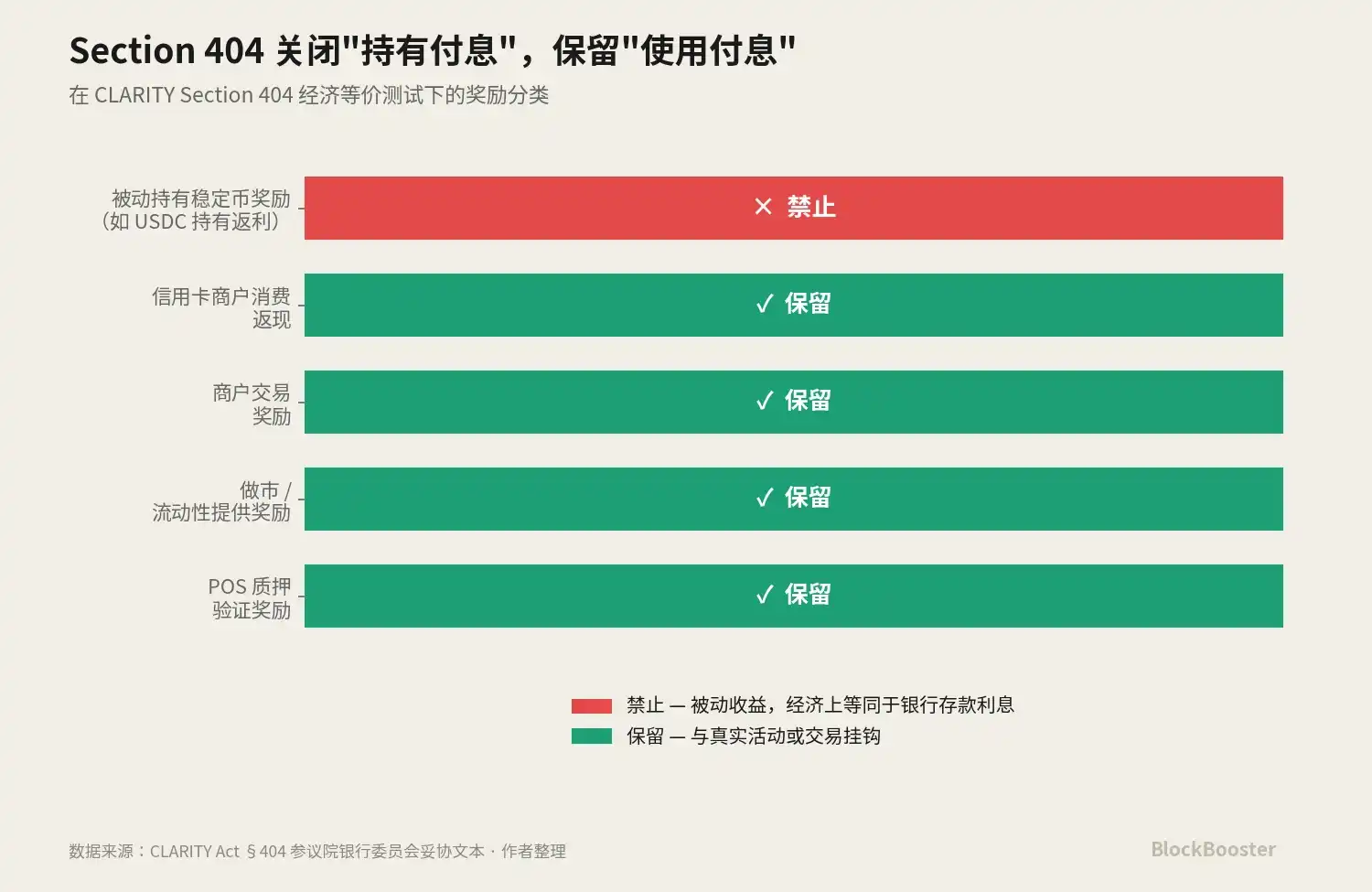

Second, it explicitly introduces the legal dichotomy between "passive yield vs. activity-based rewards." Section 404 prohibits rewards that are "functionally or economically equivalent to bank deposit interest" — i.e., yield generated automatically solely based on holding — but preserves rewards "based on genuine activities or transactions," such as staking, market making, credit card cashback, and merchant transaction rewards.

Taken together, these two changes constitute a paradigm shift. The stablecoin industry is moving from a hold-to-earn market to a use-to-earn market.

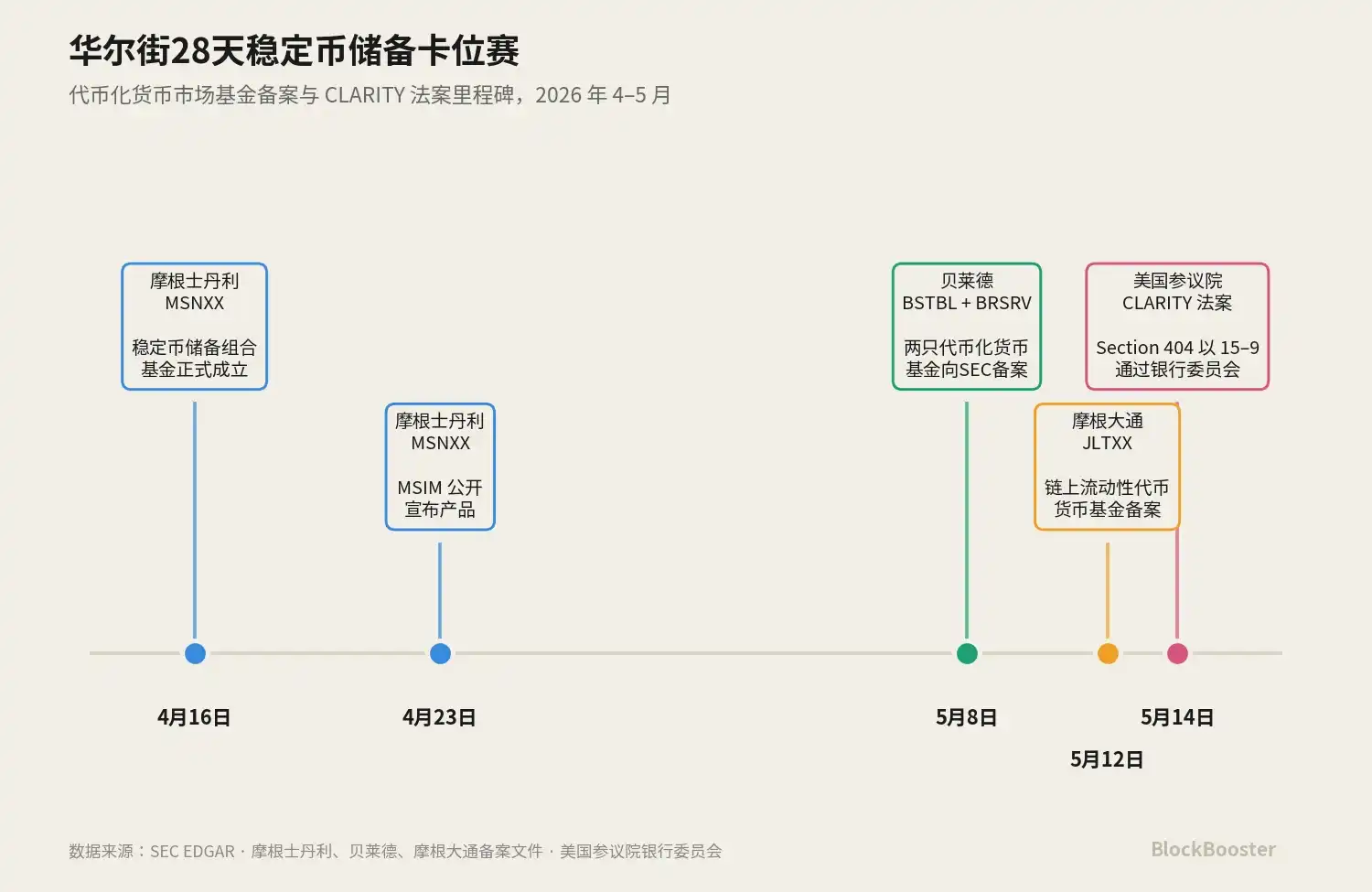

Meanwhile, over the past month, the three largest Wall Street asset managers (Morgan Stanley, BlackRock, JPMorgan) almost simultaneously launched money market fund products tailored for stablecoin reserve requirements. Morgan Stanley's MSNXX was established on April 16th and publicly announced on April 23rd; BlackRock filed for two tokenized funds, BSTBL and BRSRV, on May 8th; JPMorgan filed for JLTXX on May 12th. All three launched highly similar functionally positioned products within a 28-day window.

This timing is certainly not a coincidence. We believe: Anticipation of the impending passage of CLARITY Section 404 is pushing the stablecoin yield economy towards a new paradigm — hold-to-earn pathways are being narrowed, use-to-earn pathways are being preserved, and tokenized money market funds, as the compliant yield-bearing instruments for stablecoin reserves, become the most robustly positioned compliant yield layer in this new paradigm.

The products filed by Wall Street asset management giants in April-May represent an industrial positioning for this paradigm shift. It is crucial to clarify: CLARITY has currently only passed the Senate Banking Committee and remains some distance from a presidential signature, but market expectations are already reorganizing in this direction.

This article will start with a timeline reconstruction, deconstruct the relay-like legal structure of GENIUS and CLARITY, and analyze why the tokenized reserve asset layer has become the most robust compliant yield channel in the new paradigm.

1. A 30-Day Industrial Positioning Race

1.1 April 16th: Morgan Stanley's Opening Move

Let's return to the earliest event.

On April 16, 2026, Morgan Stanley's Stablecoin Reserves Portfolio (ticker: MSNXX) was officially established.

MSIM publicly announced this product on April 23rd.

The product positioning of MSNXX is very precise. The official statement reads: "This fund provides a qualified money market fund option for compliant stablecoin issuers, allowing them to invest the reserve assets required to back circulating stablecoins."

MSNXX is a product tailored for reserve asset requirements — investing in cash, U.S. Treasuries maturing within 93 days, and Treasury-collateralized overnight repos.

But MSNXX is not a tokenized product; it does not trade on-chain. Morgan Stanley's product strategy is conservative — offering only a traditional MMF wrapper, allowing stablecoin issuers to invest through traditional financial channels.

This is the first publicly announced product among Wall Street asset management giants "specifically designed for stablecoin reserve demand." It is not revolutionary in itself, but it sends a clear signal: stablecoin reserve demand has grown large enough for asset management giants to create a dedicated fund for it.

1.2 May 8th: BlackRock's "Dual Filing"

Twenty-two days later, BlackRock simultaneously submitted two registration statements to the SEC: the tokenized version of the BlackRock Select Treasury Based Liquidity Fund (BSTBL) and the BlackRock Daily Reinvestment Stablecoin Reserve Vehicle (BRSRV).

The design of these two products contrasts sharply with MSNXX. BSTBL is the tokenized version of BlackRock's existing Select Treasury-Based Liquidity Fund. It serves traditional institutional cash managers — clients already using this fund, now with an additional on-chain distribution channel.

BRSRV is a newly created tokenized money market fund, distributed via Securitize on multiple chains, targeting only one customer group: stablecoin issuers.

The key difference between BlackRock and Morgan Stanley lies in tokenization. BlackRock chose to issue the same assets (short-term Treasuries + cash + overnight repos) via on-chain shares to stablecoin issuers, giving the reserve assets themselves on-chain composability, 24/7 transferability, and potential for integration with DeFi protocols. This is a product form tailored for crypto-native clients (e.g., Ethena, Jupiter).

The filing of BSTBL + BRSRV represents an expansion of BlackRock's existing product matrix, extending tokenized infrastructure from BUIDL's "DeFi collateral" use case to BRSRV's "stablecoin reserve asset" use case.

1.3 May 12th: JPMorgan's Second Entry

Four days later, JPMorgan submitted the filing for the JPMorgan OnChain Liquidity-Token Money Market Fund (JLTXX) to the SEC.

The fund itself invests in U.S. Treasuries and overnight repurchase agreements collateralized by Treasuries or cash, with underlying assets identical to BUIDL, BSTBL, and BRSRV. The Token Class Shares are dated May 13th.

LTXX is not JPMorgan's first on-chain MMF. As early as December 15, 2025, JPMorgan Asset Management launched the My OnChain Net Yield Fund (MONY) on Ethereum. MONY is a 506(c) private fund, available only to accredited investors.

This means JPMorgan has nearly five months of operational experience in the tokenized MMF lane. JLTXX is not a catch-up product, but the second step in JPMorgan's on-chain MMF strategy — expanding a product originally limited to 506(c) accredited investors into a registered fund for a broader customer base, specifically targeting the stablecoin reserve use case.

On one hand, JPMorgan, along with Bank of America, Wells Fargo, and Citigroup, is exploring the joint issuance of a consortium stablecoin in 2025. On the other hand, through the MONY → JLTXX product matrix, it is deeply positioning itself in the tokenized reserve asset lane. Regardless of how the OCC ultimately rules, JPMorgan has a product in place — this "two-sided bet" is a unique strategic space for JPMorgan as a GSIB bank and asset manager.

1.4 May 14th: CLARITY Act Stamps the Entire Sector

On May 14th, the Senate Banking Committee passed the CLARITY Act with a 15-9 bipartisan vote.

It is worth carefully noting: Morgan Stanley's MSNXX, BlackRock's BSTBL/BRSRV, JPMorgan's JLTXX — all these products began preparation before the CLARITY Section 404 compromise text was made public.

In fact, since CLARITY was first shelved in January 2026, the asset management industry has understood two things: First, the "hold-to-earn" stablecoin reward path will eventually be closed. Second, stablecoin reserve assets must exist, must be compliant, and will necessarily bear yield.

Combining these two points: When the hold-to-earn path is narrowed, one of the most robust "indirect yield" transmission paths is through the reserve asset layer — the stablecoin issuer itself does not pay interest, but its reserve's tokenized money market fund legally pays interest to the issuer, who decides how to pass part of that yield to users within a compliant framework.

The products from asset management giants are the infrastructure prepared for this "most robust compliant yield channel."

2. Why CLARITY is Much More Important than GENIUS

2.1 The Limited Scope of the GENIUS Act

To understand the paradigm-shifting effect of Section 404, one must first precisely understand what it extends — GENIUS Act 4(a)(11).

The GENIUS Act was signed into law in July 2025. Its Section 4(a)(11) stipulates: A compliant stablecoin issuer or foreign stablecoin issuer shall not pay any form of interest or yield to stablecoin holders.

In other words, the GENIUS Act itself does not distinguish between "passive yield" and "activity-based rewards." Any form of interest or yield paid by the issuer to the holder is entirely prohibited.

Second, its constraint targets only the issuer itself, not third parties such as exchanges, wallets, custodians, or affiliates.

This second limitation created a regulatory loophole — known in the industry as "pass-through evasion." Essentially, the entire stablecoin industry in 2025-2026 was innovating within this loophole for compliant spaces:

- Coinbase / Kraken Model: Exchanges distribute rewards. USDC is issued by Circle, but Coinbase provides approximately 4% rewards to USDC holders through its Coinbase One subscription model.

- Gemini Credit Card Model: Triggers rewards through external merchant transactions. GUSD is issued by Gemini Trust Company, but Gemini credit card holders receive GUSD cashback when spending at merchants.

- Anchorage Digital Neo Model: Payment via an independent affiliated legal entity. USDtb is issued by Anchorage Digital Bank, but Anchorage Digital Neo Ltd. (a separate legal entity) pays the rewards.

These three models collectively formed the "indirect yield" ecosystem of the GENIUS era.

But the compliance foundation for all this was the GENIUS Act's limited scope of constraining only the issuer.

2.2 The Substantive Expansion of CLARITY Section 404

The CLARITY Act Section 404 does two things the GENIUS Act did not.

First: Expansion to DASPs and Affiliates

Section 404's constraint no longer applies only to stablecoin issuers but expands to "covered digital asset service providers and their affiliates." This scope explicitly covers centralized exchanges, brokers, dealers, and custodians.

This expansion immediately closes all "non-issuer payment" compliant paths for Coinbase, Kraken, Gemini, Anchorage Digital Neo, and others. As a DASP, Coinbase can no longer distribute hold-only USDC rewards; Anchorage Digital Neo can no longer pay USDtb rewards.

Second: Introducing the "Passive vs. Active" Dichotomy

Section 404 prohibits DASPs from offering rewards that are "functionally or economically equivalent to bank deposit interest," but preserves rewards "based on genuine activities or transactions."

This means any rewards linked to "consumption, transactions, staking, transfers" can survive; any reward that grows linearly with idle balances cannot.

Taken together, these two things constitute a complete paradigm shift. All "indirect yield" templates from the GENIUS era are either closed or need redesigning in the CLARITY era.

The stablecoin industry is moving from a hold-to-earn market to a use-to-earn market.

2.3 Winning Pathways in the Paradigm Shift

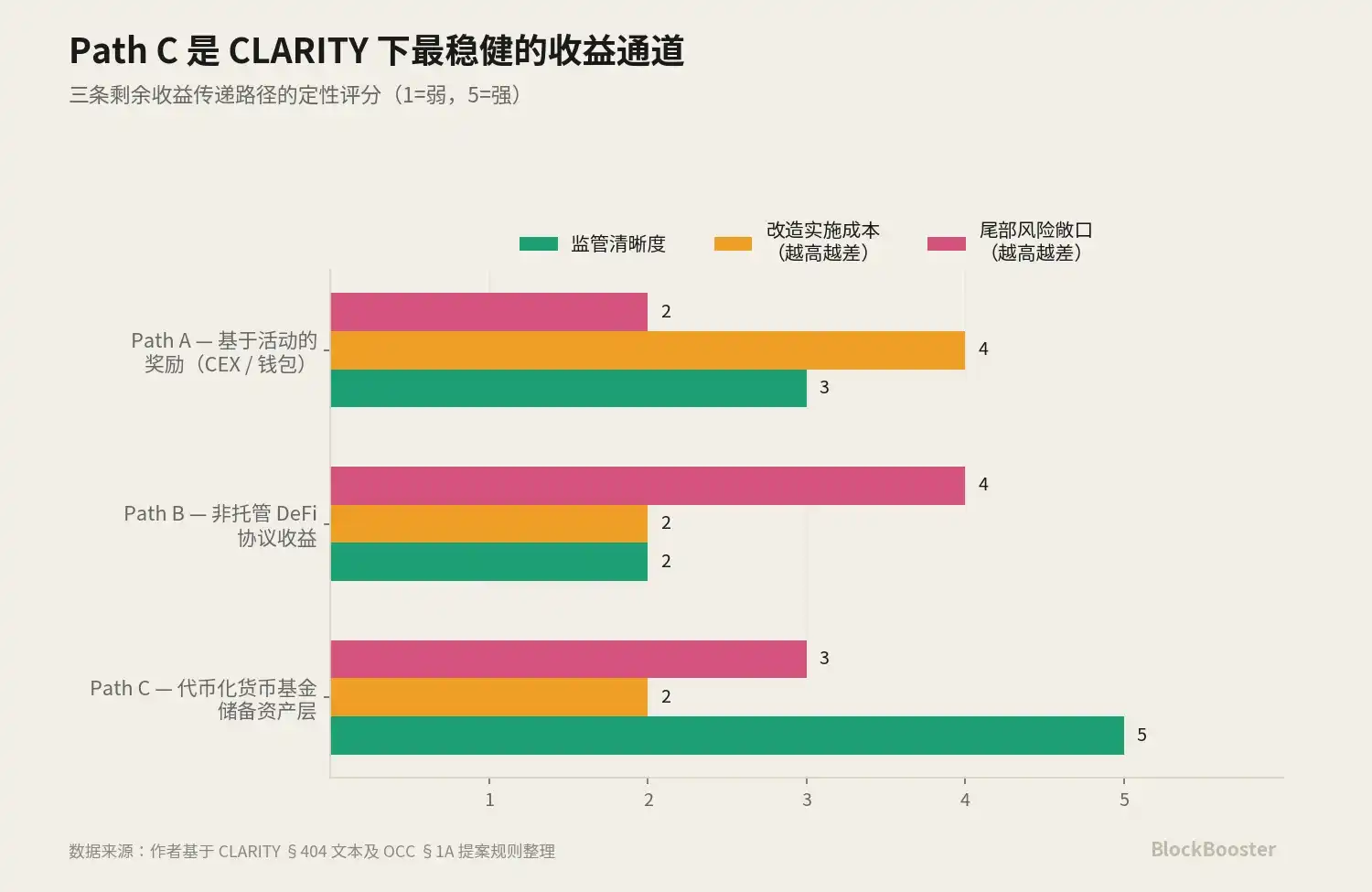

Under the use-to-earn paradigm, there are three possible pathways to pass yield to users.

Pathway A: Redesign Rewards as Activity-Based Rewards

Applicable to: Exchanges, wallets, credit cards. Coinbase could change USDC rewards from "just hold" to "based on transaction frequency/spending amount." Gemini is already using the credit card cashback model.

The key issue is not whether Path A can retain users, but its design cost — Coinbase needs to restructure the entire reward system's legal framework and product UI, with each "active" design subject to factual tests by SEC/CFTC. This restructuring could take 6-12 months, during which user attrition is a real risk. But in the medium term, Path A could fully recover or even surpass the appeal of the hold-to-earn era.

Pathway B: Retain Yield at the Protocol Layer, Passed to Users via Activity-Based Operations

Applicable to: DeFi protocols. Section 404's definition of "covered digital asset service provider" is clearly constructed around centralized intermediaries — yields generated by non-custodial smart contracts (e.g., supplying USDC to Aave for variable interest lending) are not within this definition by design.

This means users depositing USDC into an Aave lending pool to earn variable interest is currently considered compliant in most legal interpretations — CLARITY seemingly, and perhaps unintentionally, leaves a yield pathway for non-custodial DeFi.

However, this exemption comes with significant uncertainty. If final rules extend the "economically equivalent" concept to non-custodial DeFi, or define DeFi front-ends as affiliates, the exemption for Pathway B could be substantially narrowed.

Pathway C: Yield via the Reserve Asset Layer

This is the pathway Wall Street asset managers are betting on. Specific mechanism: The stablecoin issuer itself does not pay interest, DASPs do not pay interest, but the stablecoin's reserve assets are tokenized money market funds. The fund legally pays interest to its shareholders (i.e., the stablecoin issuer). After receiving the fund-distributed yield, the stablecoin issuer retains it as corporate profit — or partially passes it to users by designing active behavior rewards.

The key compliance advantage of this pathway: Its yield layer is not at the stablecoin layer, nor the DASP layer, but at the underlying fund layer — independent of stablecoin regulatory frameworks.

These three pathways are not mutually exclusive but will evolve simultaneously.

Pathway A may gain new life with players like Coinbase who have retail brands and distribution channels;

Pathway B may receive an unexpected boost for protocols like Aave, Pendle (but with tail risk of regulatory narrowing in the next 12 months);

Pathway C is the pathway least directly threatened by Section 404, but requires the OCC's 20% cap not to pass as a prerequisite.

Pathway C is the "most robustly positioned" compliant yield layer, but not the "only one positioned."

This is why Wall Street asset management giants filed for tokenized money market funds in April-May. They are providing the compliant yield infrastructure for one of the pathways in the use-to-earn paradigm about to be solidified by CLARITY Section 404. Considering the implementation costs and regulatory uncertainties of Paths A and B, Path C has the strongest risk-adjusted appeal — this is the industrial judgment of the BlackRocks.

2.4 The Collaborative Relationship Between Pathways B and C

There seems to be collaborative potential between Pathways B and C. A complete on-chain yield system could utilize both pathways simultaneously:

- Use BUIDL at the reserve asset layer — ensuring the source of compliant yield

- Use Aave lending or Pendle yield splitting at the user layer — ensuring the "yield" perceived by users comes from active operations

This "BUIDL at the base, DeFi protocols at the surface" two-tier structure could theoretically build a system that is both compliant and user-friendly for use-to-earn. BlackRock clearly did not specifically foresee Section 404 when launching BUIDL, but this product happens to become the optimal base layer for use-to-earn systems under the new paradigm.

3. BlackRock's Three-Tier Product Matrix — Infrastructure Built for the New Paradigm

3.1 Three Products, Three Customer Segments

To understand BlackRock's strategy, one must contrast its three tokenized fund products simultaneously on the table:

BUIDL: Launched in March 2024, natively built on Ethereum. Legal structure is a BVI fund, custody provided by Securitize.

Target Customers: DeFi protocols, crypto-native institutions, on-chain scenarios needing BUIDL as collateral. Accepted as eligible collateral on lending protocols like Aave, minimum investment $5 million.

BSTBL: Filed on May 8, 2026. Legal structure is a U.S. SEC-registered government money market fund, with BNY Mellon Investment Servicing as transfer agent.

Target Customers: Traditional institutional cash managers — clients already using BlackRock funds, now gaining 24/7 trading capability via on-chain shares.

BRSRV: Filed on May 8, 2026. Legal structure is a newly created money market fund, multi-chain distribution via Securitize.

Target Customers: Stablecoin issuers — tailored for compliant reserve demand under the GENIUS Act.

These three products exist simultaneously in the market, but their customer segments hardly overlap. This layered product matrix design: the same underlying assets (short-term Treasuries + cash + overnight repos), packaged differently through distinct legal wrappers, custody structures, and distribution channels, sold to three entirely different customer groups.

More importantly, these three products collectively constitute a complete tokenized reserve asset ecosystem, covering all needs under the use-to-earn paradigm: BUIDL as collateral and composable assets at the DeFi protocol layer; BSTBL as an on-chain cash management tool for traditional institutions; BRSRV as a core target at the stablecoin issuer reserve asset layer. Regardless of the specific design of the use-to-earn system, the required tokenized reserve assets — BlackRock already has corresponding products ready.

4. 90% Concentration — The Overlooked Systemic Risk in the CLARITY Paradigm Shift

Next, we quantify the current concentration risk of BlackRock's BUIDL.

When USDtb launched on December 16, 2024, the official collaboration announcement between Ethena and BlackRock explicitly stated: "BUIDL constitutes over 90% of USDtb reserves. This is the largest allocation to BUIDL by any stablecoin."

After JupUSD launched on January 6, 2026, its reserve structure was 90% USDtb + 10% USDC liquidity buffer.

Calculated concentration: The single BUIDL fund supports approximately 90% of USDtb's reserves, and indirectly supports approximately 81% of JupUSD's reserves (90% of USDtb × 90% of JupUSD).

USDtb's historical peak circulation was around $1.2 billion (June 2025 data), and JupUSD has grown rapidly since its January 2026 launch. This means the health of the single BUIDL fund directly determines the solvency of at least two significant stablecoins. If BUIDL experiences large-scale redemption pressure, the reserve assets of downstream USDtb and JupUSD would simultaneously become impaired.

The CLARITY paradigm shift further amplifies this concentration risk.

5. The OCC's 20% Reserve Asset Cap Game — Deciding Which Pathway, A, B, or C, Prevails

5.1 The Cap Proposal and Opposition

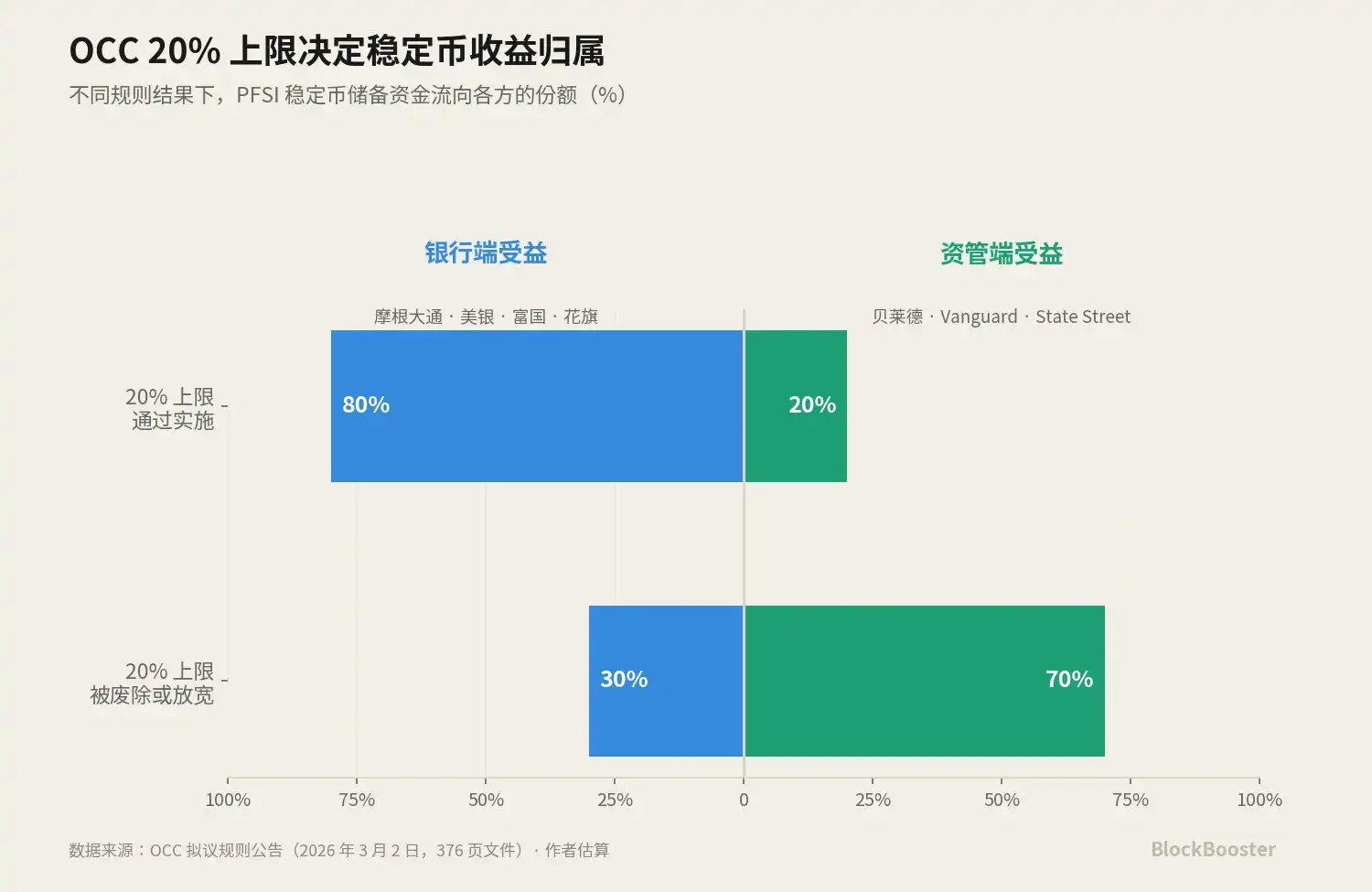

On March 2nd, the U.S. Office of the Comptroller of the Currency (OCC) published a 376-page proposal in the Federal Register as part of the GENIUS Act implementation rules. One proposal sparked industry-wide discussion: as a possible alternative threshold, the OCC explored whether to set a 20% cap on the proportion of "tokenized assets" within the reserve assets of federally chartered stablecoin issuers (PFSIs).

Although this is merely a possible option raised by the OCC for discussion during the comment period, market participants already view this alternative threshold as a strong signal of regulatory intent.

If this cap were implemented, it would mean: PPSIs could place at most 20% of their reserve assets in tokenized funds (e.g., BUIDL, JLTXX, BRSRV), with the remaining 80% in traditional non-tokenized assets.

If the 20% cap passes, it would directly hinder the scaling capability of the tokenized reserve asset layer.

5.2 A Zero-Sum Game Deciding Pathway Victory

The true meaning of the OCC's 20% cap is: This is the key variable in the CLARITY paradigm shift that determines whether Pathway C can scale among the three yield channels A, B, and C.

Supporting the cap are JPMorgan Chase, Bank of America, Wells Fargo, Citigroup — which announced in 2025 they were exploring the possibility of jointly issuing a stablecoin. If the 20% cap passes, 80% of PPSI reserve assets must reside in traditional assets, meaning most reserve funds would flow back to the bank deposit system. The biggest beneficiaries would be these four banks.

Opposing the cap are asset management giants like BlackRock, Vanguard, State Street. If the cap is removed or significantly relaxed, PPSIs could place 100% of their reserve assets in tokenized money market funds (including BUIDL, BSTBL, BRSRV). The biggest beneficiaries would be these asset managers. Pathway C fully opens.

5.3 Changes in the Game After CLARITY's Passage

The May 14th passage of the CLARITY Act by the Senate Banking Committee adds a key variable to the OCC 20% cap game.

The CLARITY Act provides clear legal status for tokenized securities — indirectly weakening the OCC's argument that "tokenized assets pose special risks requiring additional restrictions." If CLARITY gives tokenized funds legal status, the OCC's use of "the tokenized form itself carries special risks" as a restriction reason becomes less tenable.

Once CLARITY + GENIUS form a complete framework, the OCC is expected to have to adjust its 20% alternative threshold. The most likely outcome: the threshold is abolished or significantly relaxed. This is a partial victory for the "principles-based" route favored by BlackRock.

But a question must be confronted directly: The scaling victory of Path C and the systemic concentration risk discussed in Part 4 are two sides of the same coin. If the OCC's 20% threshold is relaxed, BUIDL-type funds could rapidly absorb hundreds of billions, even a trillion dollars, in stablecoin reserve assets, validating the industrial value bet by BlackRock and others. But simultaneously, BUIDL's single-point-of-failure risk, reflexive stampede risk, and the "pyramid-style concentration" risk for the crypto-dollar economy would all be magnified.

In other words, Path C's victory is a win for BlackRock in industrial terms, but the birth of a new type of concentration risk in systemic terms.

Traditional finance uses SIFMU designation, CCAR stress tests, DTCC disaster recovery mechanisms to manage such scaled concentration. The on-chain tokenized reserve asset layer currently has no equivalent mechanisms. Therefore, if Path C's victory arrives, it will be accompanied by a time window — the window for regulatory frameworks to catch up with concentration risks. Whether FSOC begins intervening in this concentration issue in 2027-2028 is a policy variable worth tracking.

Conclusion

The entire stablecoin yield economy is being forcibly reset from "hold-to-earn" to "use-to-earn," with tokenized money market funds as the underlying reserve assets becoming one of the most robustly positioned compliant yield infrastructures in the new paradigm.

The product layout of Wall Street asset management giants — MSIM's MSNXX, BlackRock's BSTBL/BRSRV, JPMorgan's JLTXX — represents an industrial positioning for this paradigm shift.

The true protagonists of this direction are the tokenized money market fund providers at the very bottom of the industry chain. Visa and Mastercard do not directly face consumers, but they built a high-margin, high-growth, strong-moat business model by charging ~0.1-0.3% network fees per transaction — with a combined market cap exceeding $1 trillion, far surpassing most credit card issuers.

Tokenized reserve asset providers (BlackRock, JPMorgan, Morgan Stanley) are now playing a similar role within the crypto-dollar economy.

What we are witnessing is a regulation-driven changing of the guard in the financial infrastructure layer. The CLARITY Act closed the "indirect yield" paths of the GENIUS era, but it did not close yield itself — yield has been forcibly relocated to the reserve asset layer. The new world's Visa and Mastercard are already in position.