The Macroeconomic Underpinnings of Africa's Payment Market Landscape

The African payments market, characterized by the world's highest mobile money penetration and fastest-growing cryptocurrency adoption, is not a coincidence but a macroeconomic necessity driven by deep structural factors.

Two key drivers create this landscape: (1) Africa's heavy reliance on commodity exports, trade, and remittances, generating massive cross-border settlement and remittance demand; and (2) chronically underdeveloped financial infrastructure, exacerbated by international bank de-risking, foreign exchange mismanagement, and persistent inflation. This vacuum has allowed mobile money and crypto to thrive. Mobile money platforms replace banks for domestic payments, while cryptocurrencies serve as a store of value against local currency depreciation and a low-cost medium for cross-border exchange.

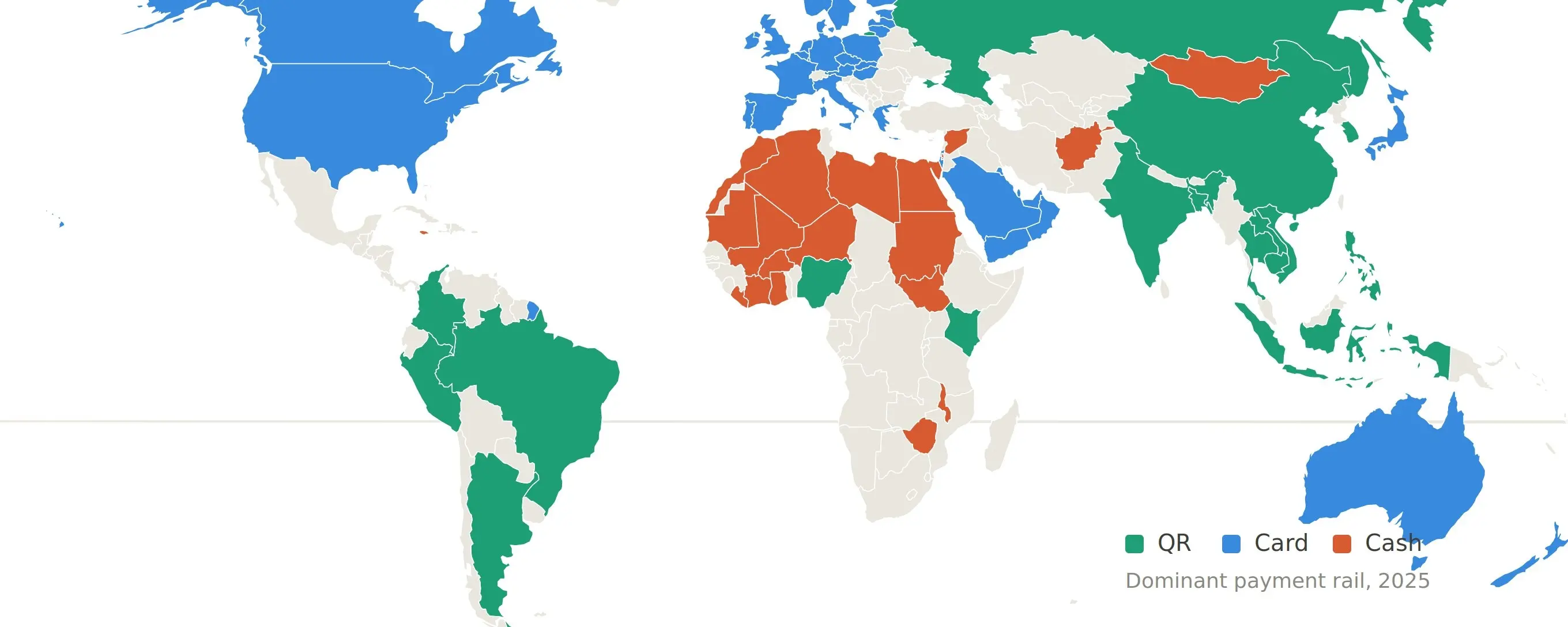

A crucial division lies along the Sahara Desert. North Africa is integrated into the oil-anchored MENA framework, while Sub-Saharan Africa (SSA), plagued by dollar shortages and fragmented currencies, has become a natural, massive market for mobile money and crypto. Nigeria, Kenya, and South Africa are global leaders in adoption.

The SSA economy is deeply dollarized due to currency instability, yet suffers from a severe "dollar shortage" caused by trade deficits and limited export capacity. This creates parallel forex markets and high remittance costs. Cryptocurrencies, particularly stablecoins, fill this gap by providing access to dollar liquidity, cheaper cross-border transfers, and an inflation-resistant store of value, primarily driven by retail users for small-value transactions.

While regional initiatives like PAPSS aim to reduce dollar dependence, the fundamental constraints of commodity reliance, trade imbalances, and shallow financial markets persist. Therefore, mobile money and cryptocurrencies are not niche trends but essential financial infrastructure filling a structural void, and they are likely to remain central to Africa's economic landscape for the foreseeable future.

链捕手06/05 06:12