Paxos Labs выпустила USDG0, мультичейн-расширение своего регулируемого стейблкоина USDG, которое обеспечивает полностью обеспеченную долларовую ликвидность для Hyperliquid, Plume и Aptos с использованием стандарта OFT от LayerZero.

Согласно публикации Paxos Labs в X во вторник, USDG0 расширяет функциональность Global Dollar (USDG) — стейблкоина с долларовым обеспечением 1:1, эмитируемого Paxos и управляемого Global Dollar Network, на новые блокчейны без создания отдельных версий.

Благодаря стандарту OFT от LayerZero, USDG0 может перемещаться между блокчейнами как единый нативный актив при сохранении тех же регуляторных защит и обеспечения, что и USDG в Ethereum, Solana, Ink и X Layer.

Источник: Paxos Labs.

В Paxos Labs отметили, что первоначальный запуск демонстрирует возможности подключения разных сетей к экономике стейблкоина. В Hyperliquid USDG0 будет поддерживать торговлю с доходностью и новые кредитные рынки, в то время как Plume и Aptos планируют использовать его для модульных DeFi, токенизированных доходов и корпоративных платежных систем на основе стейблкоинов.

Во всех трех экосистемах USDG0 позволит приложениям встраивать долларовую ликвидность в свои продукты, получать доходность, привязанную к казначейским эталонам, и передавать стоимость между блокчейнами без использования традиционных мостов.

Компания подчеркнула, что эта инициатива показывает, «как регулируемая инфраструктура сочетается с композабельностью DeFi и как доверенные деньги становятся по-настоящему безграничными».

С 2018 года Paxos обработала более $180 млрд операций по токенизации под надзором глобальных регуляторов. Компания управляет тремя регулируемыми стейблкоинами с долларовым обеспечением: Pax Dollar (USDP), PayPal USD (PYUSD) и Global Dollar (USDG).

Стейблкоины по всему миру

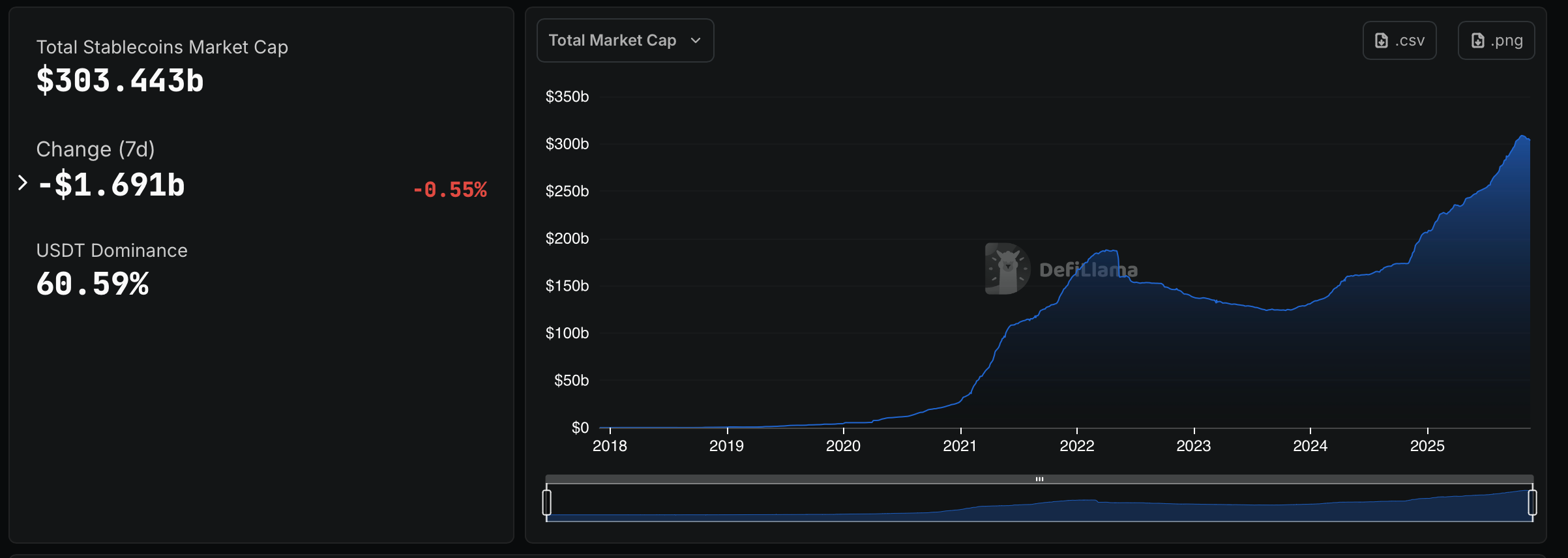

Регуляторная ясность в Соединенных Штатах в соответствии с законом GENIUS и в Европе через регуляторные рамки MiCA способствовала росту использования стейблкоинов. Согласно данным DefiLlama, рыночная капитализация стейблкоинов составляет $303,44 млрд, увеличившись почти на $100 млрд с начала года.

Хотя рынок стейблкоинов продолжает доминировать Tether (USDT) и USD-Coin (USDC) от Circle, несколько новых участников вышли на рынок в этом году из разных стран.

Рыночная капитализация стейблкоинов. Источник: Defillama

В октябре Western Union анонсировала планы по запуску USDPT, стейблкоина, привязанного к доллару США, эмитируемого Anchorage Digital Bank на блокчейне Solana (SOL). Токен предназначен для объединения цифровых и фиатных платежных систем компании и поддержки ее глобальных денежных переводов и казначейских операций.

В том же месяце JPYC, токийская финтех-компания, запустила первый в Японии стейблкоин с иеновым обеспечением — токен с привязкой 1:1 к иене, обеспечиваемый банковскими депозитами и государственными облигациями.

Также в октябре франко-германская банковская группа ODDO BHF запустила стейблкоин, привязанный к евро, в соответствии с регламентом Европейского союза «Рынки криптовалютных активов» (MiCA).

В сентябре европейский консорциум из девяти банков сообщил о планах запуска стейблкоина, привязанного к евро, для конкуренции с растущими стейблкоинами с долларовым обеспечением. Ожидается, что стейблкоин будет запущен во второй половине 2026 года.