Author: Nancy, PANews

Recently, the TCG project Collector Crypt forcefully broke into the top 10 of the global revenue rankings and once topped Solana as the highest-earning protocol, sparking widespread discussion in the community.

While most crypto projects are struggling to survive in the bear market, Collector Crypt has become one of the few money printers in the market due to its strong profitability. The tokenized TCG track, represented by Collector Crypt, is moving the fun of collecting and card opening onto the blockchain, rapidly capturing attention in the crypto market.

On-Chain TCGs Are 'Outperforming' NFTs? Solana Takes 80% of the Market

Since last year, TCGs (Trading Card Games), which combine IP, collecting, social, and gaming elements, have entered a new growth cycle, with market enthusiasm continuously rising.

This TCG craze has also begun to migrate on-chain. Since 2025, a batch of tokenized TCG players have emerged in the crypto market, including Collector Crypt, Phygitals, Courtyard, Ready Cards, Beezie, and others.

Compared to traditional physical cards, tokenized TCGs significantly improve liquidity and trading efficiency while reducing risks such as counterfeit cards and theft. This advantage is particularly evident with high-value cards. However, due to their heavy reliance on centralized vaults and custodial systems, they have also raised market concerns—if a platform shuts down or its vault encounters problems, it could lead to asset losses.

To address these issues, some on-chain platforms have begun introducing more robust physical asset anchoring and risk control mechanisms. For example, Collector Crypt has a physical storage vault of approximately 28,000 square feet in Montana, USA, for storing real card assets. It also uses rating systems like PSA for certification and endorsement to enhance asset transparency and user trust.

Benefiting from the continued prosperity of the physical collectibles market and the growing demand for asset tokenization, the on-chain TCG market has entered a rapid growth phase in recent months, becoming one of the more noticeable growth segments in the current crypto bear market.

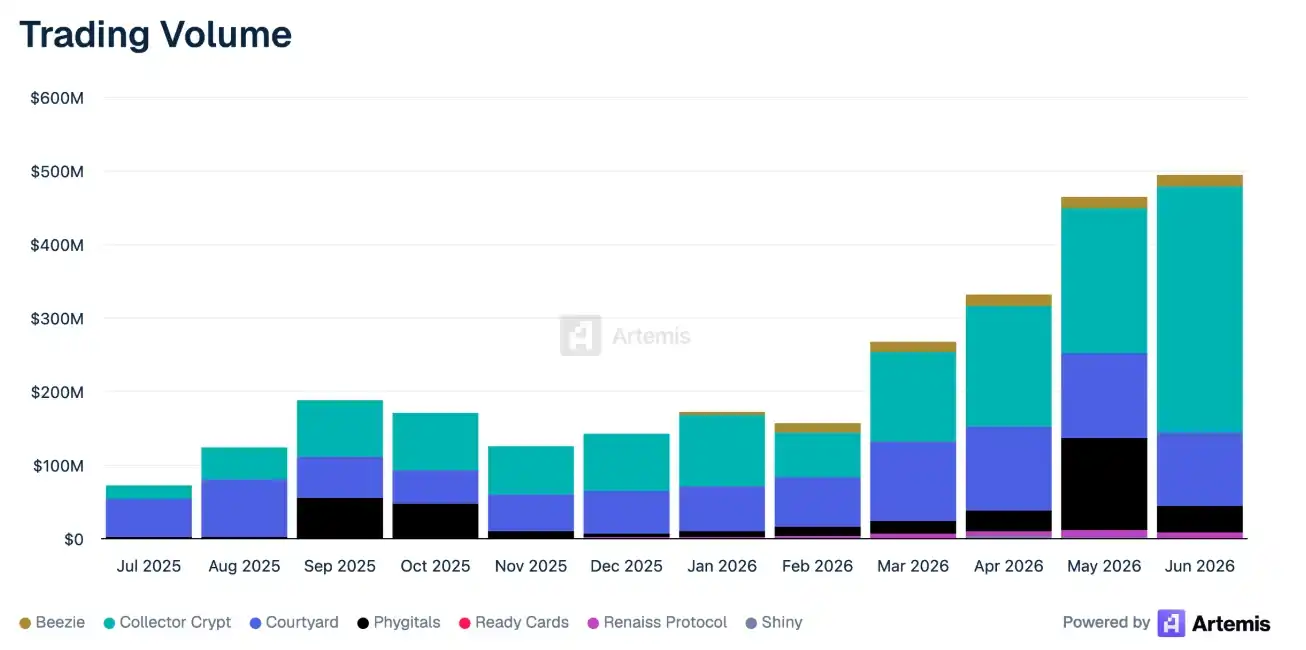

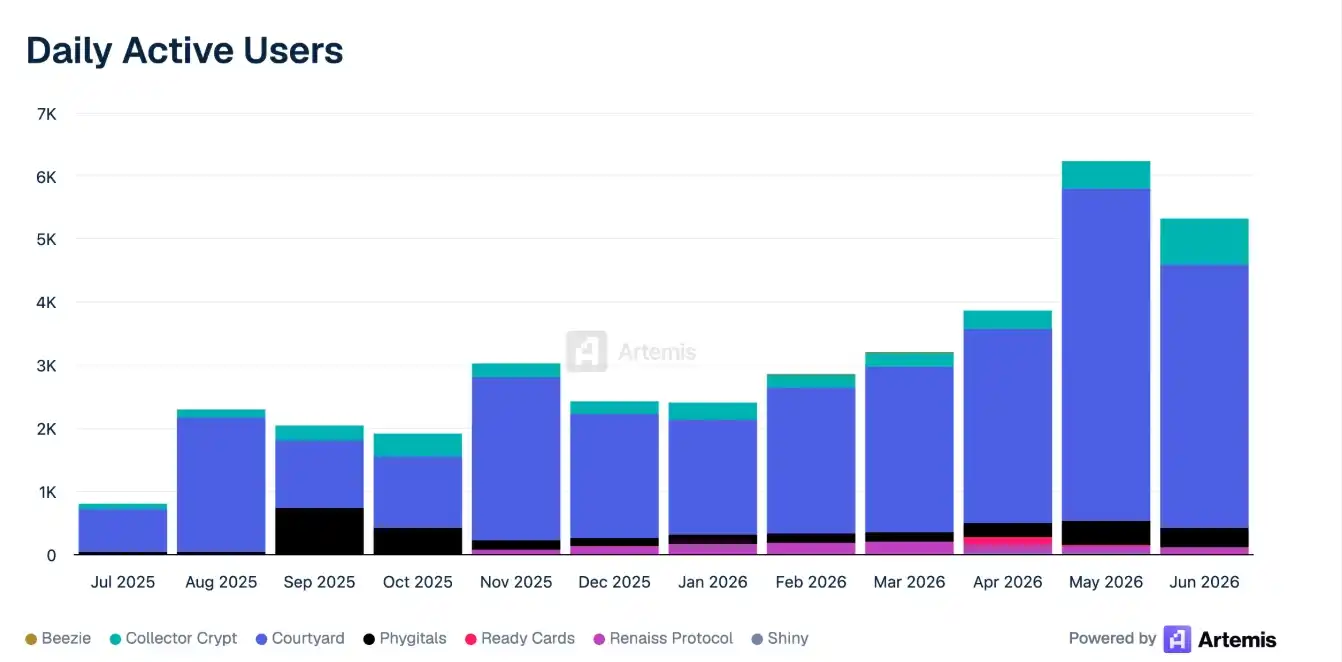

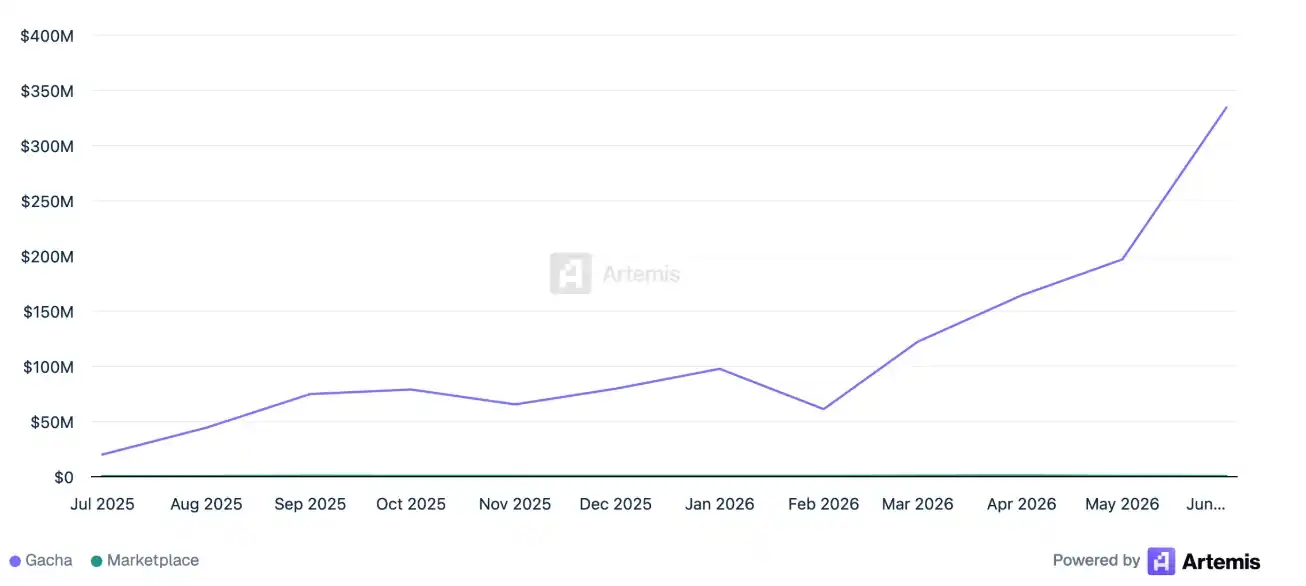

Artemis data shows that in June 2026, the transaction volume of the on-chain TCG market exceeded $490 million, a 7.6-fold increase compared to the same period last year; monthly active users reached approximately 5,300, a year-on-year increase of about 253.3%; and the cumulative monthly revenue of various protocols was about $11.8 million, more than 1.8 times higher than the same period last year.

In contrast, in the NFT sector, CryptoSlam data shows that the transaction volume of the NFT market during the same period was approximately $150 million. Although both belong to on-chain digital collectible assets, TCGs demonstrate higher user willingness to participate and trading activity. The main reasons are their combination of real-world value support from physical cards, sustained usage scenarios driven by competitive and gaming attributes, and the high liquidity, asset composability, and global circulation capabilities enabled by on-chain transactions.

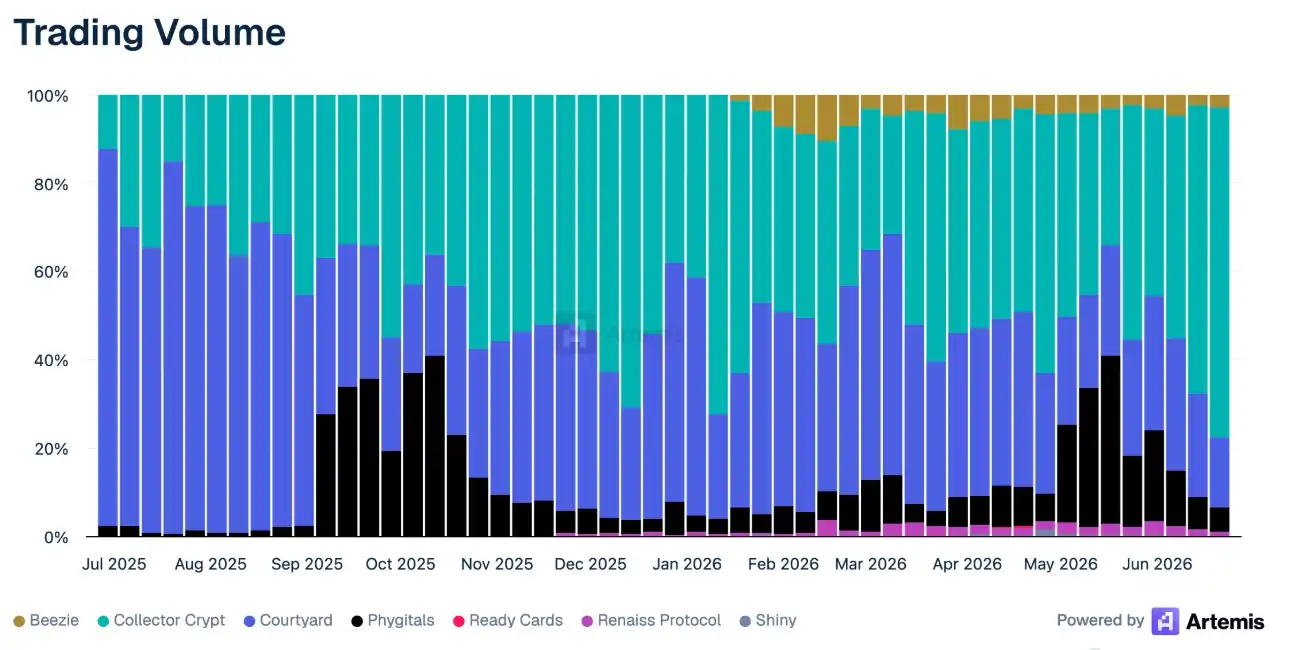

From a public chain ecosystem perspective, current tokenized TCG projects are primarily deployed on mainstream public chains such as Solana, BNB Chain, Polygon, and Base. Among them, Solana, leveraging its technical advantages, first-mover effect, and hit application Collector Crypt, has become the core battleground for tokenized TCGs. According to Artemis data, Solana has captured an 80.8% share of the on-chain TCG market, far exceeding other public chains, making it the most active and liquid ecosystem for tokenized TCGs.

However, from the overall market perspective, on-chain TCGs are still in their early stages of development. According to a report by Global Market Insights, the global TCG market size is expected to reach or has already crossed approximately $9.2 billion in 2026, with an estimated market value of $16.9 billion by 2035.

Compared to the vast physical market, the current penetration rate of on-chain TCGs remains limited, indicating significant growth potential in areas such as asset on-chain, trading infrastructure, and global liquidity.

Collector Crypt Dominates, But 97% of Its Revenue Relies on Whales

The explosive growth of the current on-chain TCG track is inseparable from the push from Collector Crypt. As the most dominant project in the track, it has established a clear gap with other platforms in terms of trading volume, revenue capability, and market share.

Artemis data shows that since its launch, Collector Crypt's cumulative transaction volume has exceeded $1.4 billion, and its cumulative protocol revenue has reached $68 million, far surpassing other on-chain TCG platforms.

Looking at its market performance over the past week, Collector Crypt's trading volume was approximately $127 million, accounting for 74.3% of the entire on-chain TCG market. In the same period, other platforms mostly had trading volumes of just a few million dollars or even less. In terms of revenue, Collector Crypt's weekly protocol revenue was about $5.2 million, while other platforms generally earned only tens of thousands of dollars, with some even operating at a loss.

Beyond continuously expanding its leading advantage in the on-chain TCG track, Collector Crypt's profitability has also begun to reach the top tier of the entire crypto industry.

Recently, Collector Crypt entered the top ten of the global protocol revenue rankings alongside protocols like Tether, Circle, and Hyperliquid, demonstrating commercial viability competitive with leading projects in mature sectors like DeFi and stablecoins. Meanwhile, according to DeFiLlama data, as of June 26, Collector Crypt has become the second-highest revenue-generating protocol on Solana, second only to the Meme money printer Pump.fun.

In fact, almost all of Collector Crypt's core operating metrics have entered a rapid growth phase since the beginning of this year.

Artemis data shows that in June this year, the platform's monthly trading volume exceeded $330 million, an increase of about 3.4 times compared to $97.5 million in January; during the same period, monthly active users grew from 276 to 735, an increase of about 2.6 times; and protocol revenue grew from $4.4 million to $13.4 million, an increase of over 3 times.

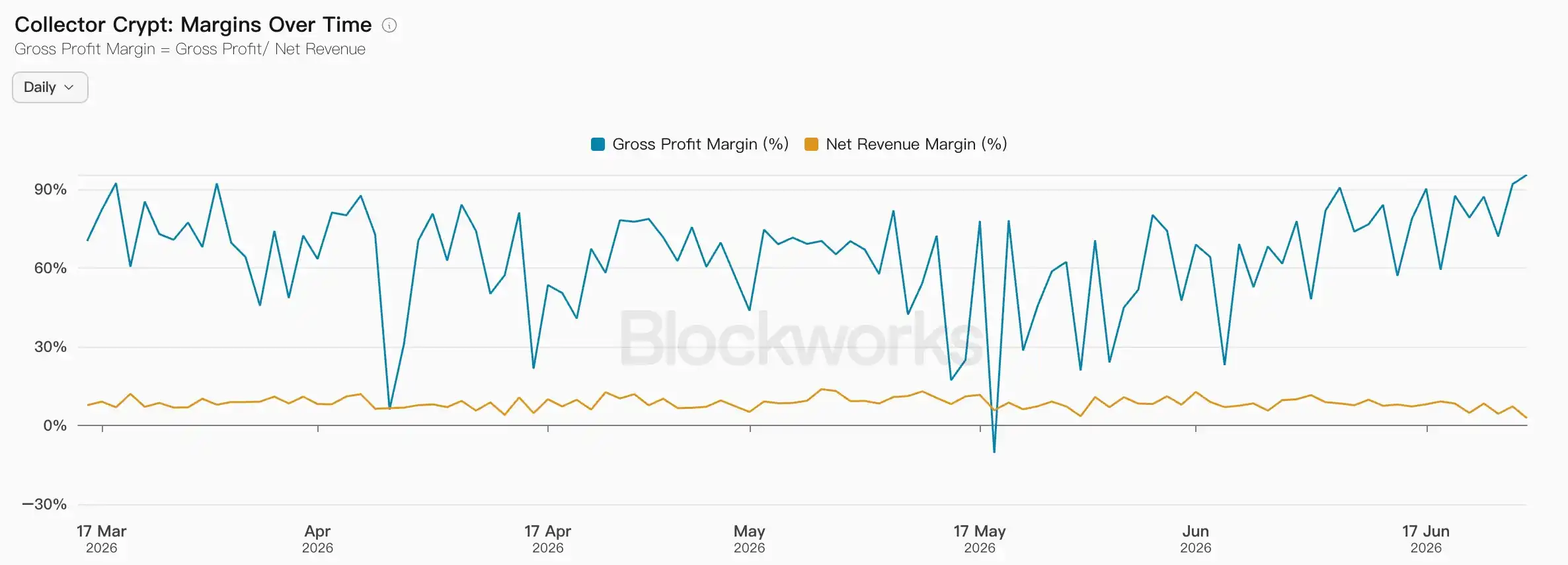

However, alongside its rapid growth, Collector Crypt also faces pressure on profitability. Blockworks data shows that as of June 26, the platform has generated cumulative gross revenue of $707 million, but net revenue is only $46.33 million, with a revenue retention rate of about 6.5%. At the same time, due to factors such as an increasing proportion of high-priced, low-margin card packs and extremely high instant buyback rates, Collector Crypt's platform gross margin has continued to decline, dropping to 2.74% as of June 24, significantly lower than the 6.03% at the beginning of the year.

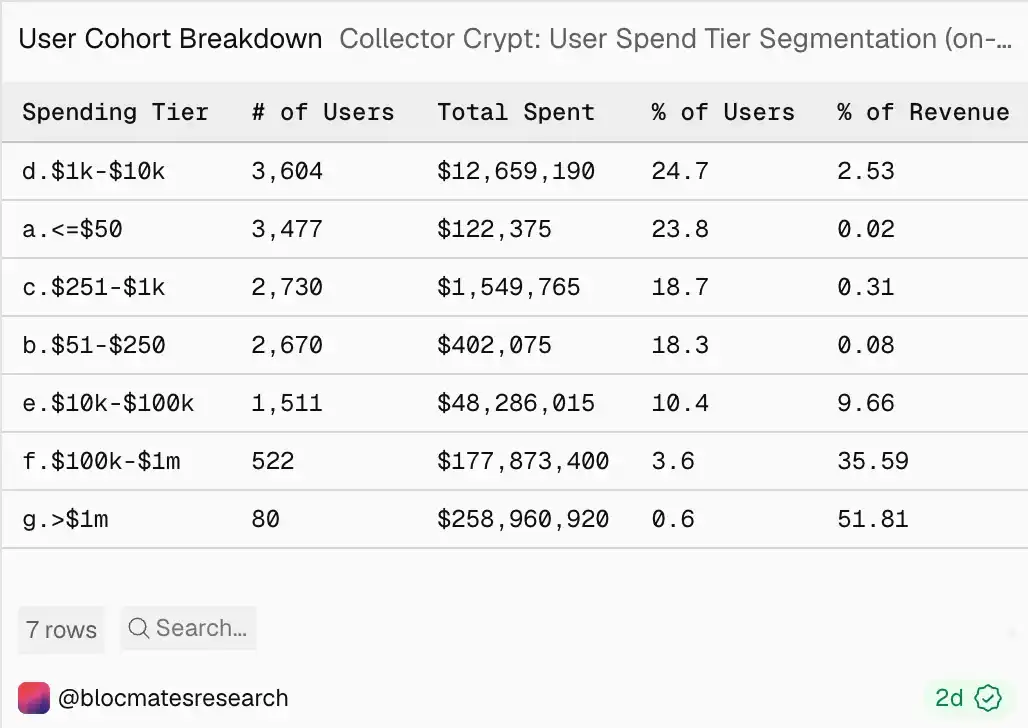

Moreover, from a user structure perspective, Collector Crypt's revenue remains highly dependent on a small number of high-net-worth players, making it a veritable 'whale playground' for on-chain TCGs.

Dune data shows that over the past six months, the platform had about 14,594 on-chain paying users, contributing nearly $500 million in trading volume. Among them, only 80 players (0.6% of total users) spent over $1 million, contributing 51.8% of the revenue; 522 users (3.6%) spent between $100,000 and $1 million, contributing 35.6% of the revenue; and users spending between $10,000 and $100,000 (10.4%) contributed 9.7% of the revenue. In contrast, users spending less than $250, who account for over 42.1% of the total user base, contributed only about 0.1% of the revenue. This means that currently, about 14.6% of Collector Crypt's users contribute about 97.1% of the platform's revenue.

This highly concentrated revenue structure, on one hand, reflects that Collector Crypt's high-net-worth users possess strong payment capabilities and consumption stickiness, bringing considerable profitability to the platform, though wash trading cannot be entirely ruled out; on the other hand, it also means that for the platform to achieve sustainable and scalable growth, it still needs to expand its user base and reduce dependence on a few whale transactions.

With Fewer Than 1,000 Daily Active Users, How Did Collector Crypt Make It into the Top 10 in Revenue?

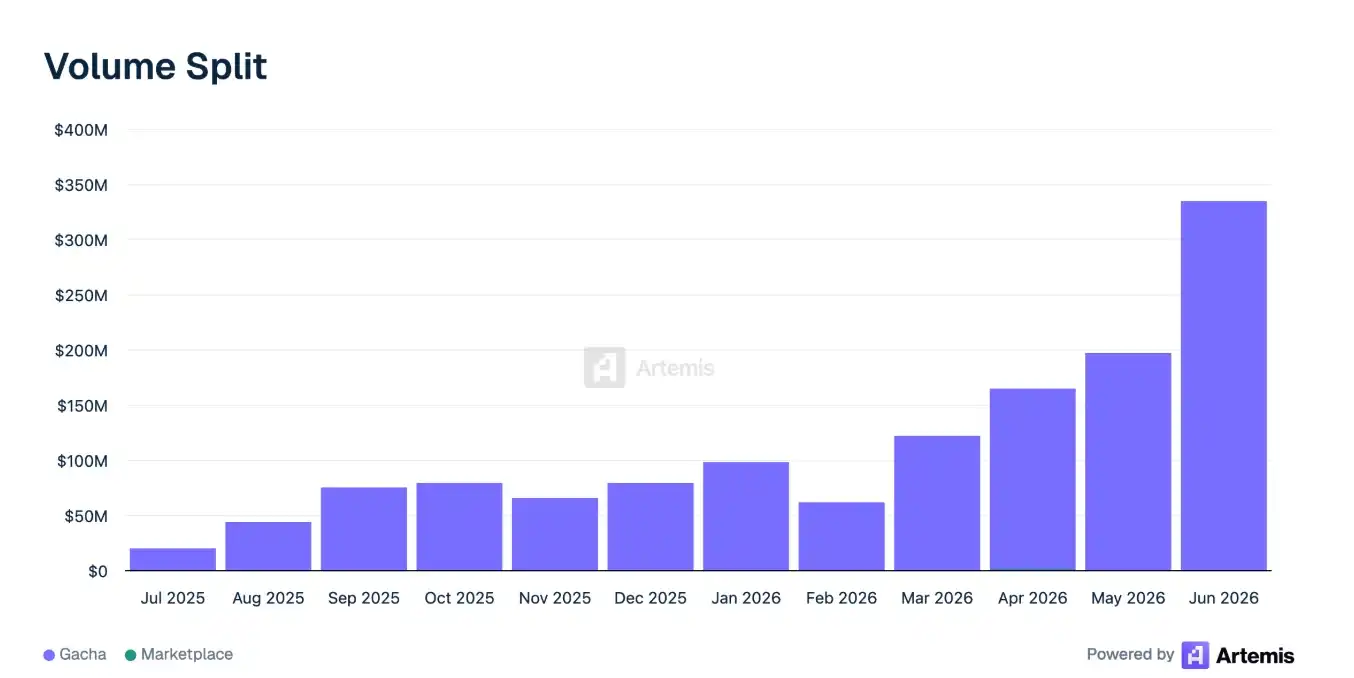

One of the key drivers behind Collector Crypt's trading explosion is the on-chain Gacha mechanism introduced by the platform. This model draws inspiration from the traditional TCG card-opening gameplay, amplifying players' anticipation and repeat purchase willingness through random rewards, scarce cards, and instant feedback, becoming the core engine for the platform's trading growth.

Currently, Collector Crypt has become the largest on-chain Gacha market on Solana, holding approximately 87.4% of the market share.

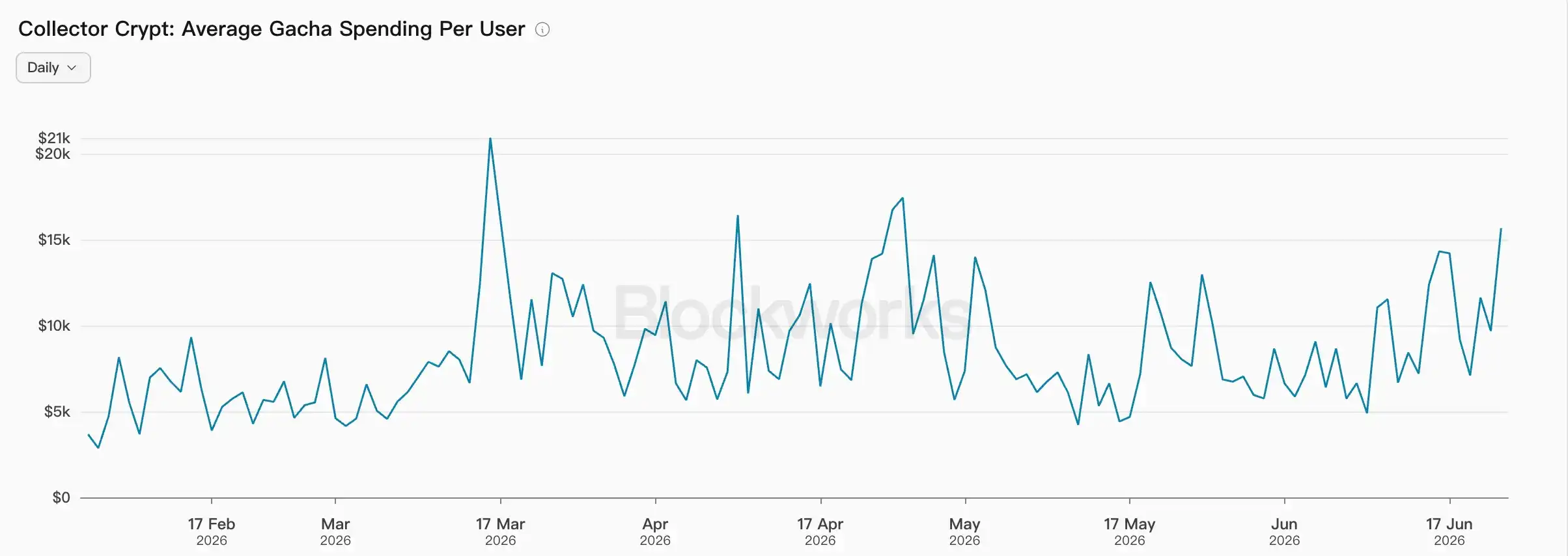

Blockworks and Artemis data respectively show that in June alone, the platform's Gacha transaction volume reached $127 million, contributing almost the entire platform's trading volume; during the same period, the cumulative value of opened packs exceeded $100 million, nearly doubling compared to the beginning of the year. At the same time, the number of participants continued to increase. As of June 23, the platform's daily active Gacha users had reached 811, whereas in previous months, it was typically below 300.

It is worth noting that Collector Crypt's high trading volume is not only due to increased activity but also largely attributed to the substantial spending continuously contributed by the aforementioned whale users. Blockworks data shows that the average Gacha spending per user is as high as $7,829, and in recent months, it once rose to $9,858.

In addition to the Gacha mechanism, the Pokémon IP and token economic model have also become important drivers for Collector Crypt's sustained growth.

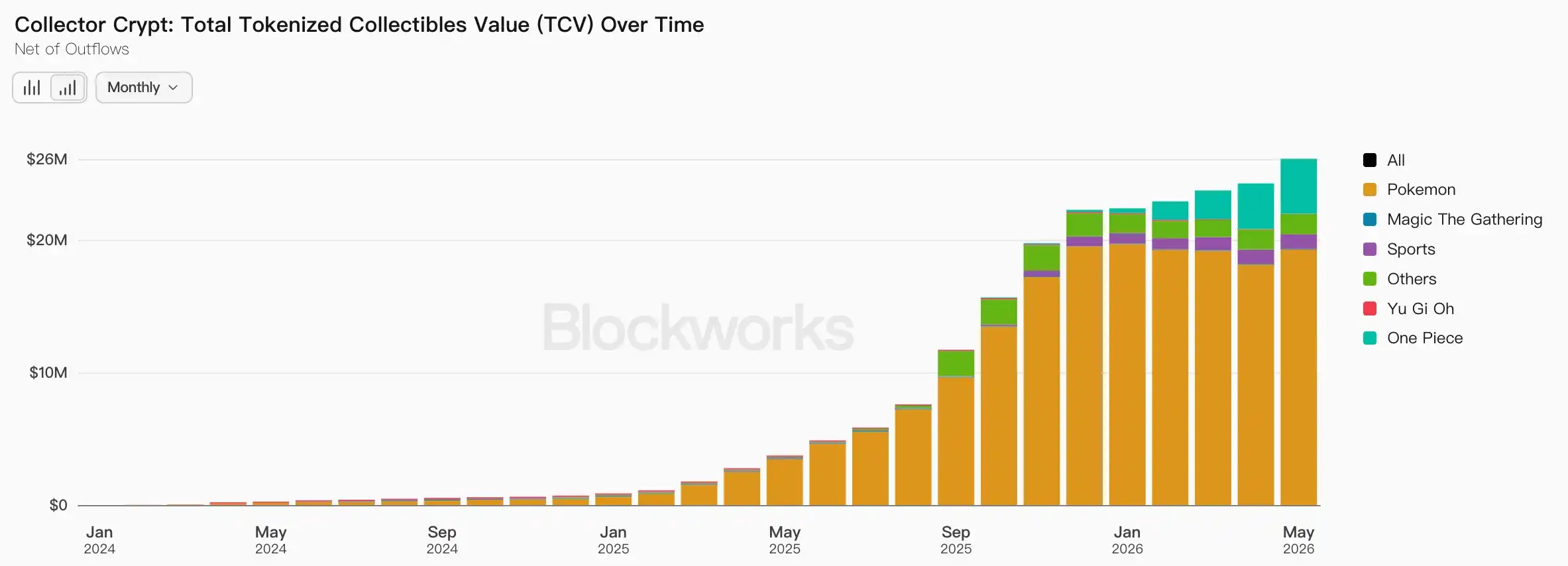

Among them, the Pokémon IP is the platform's most critical traffic source. Blockworks data shows that in June this year, the Tokenized Collectible Value (TCV) on the Collector Crypt platform reached $26.1 million, of which about 73.8% came from Pokémon cards. Among the popular card pack products, about 76% are Pokémon series packs, with the $1,000 Pokémon bundle accounting for nearly half of all packs opened. In other words, high-quality IP remains a crucial foundation for driving user consumption and trading.

On the other hand, the CARDS token has constructed a growth flywheel for the platform. Since its launch, Collector Crypt has cumulatively distributed 4.75% of the CARDS token supply to the community. This includes a 2.5% initial airdrop at the TGE stage and three quarterly airdrops, each releasing 0.75%. The most recent quarterly airdrop was valued at approximately $4 million.

Compared to simple airdrop incentives, Collector Crypt has also established a dual buyback mechanism: on one hand, it conducts instant buybacks for card assets, providing continuous liquidity for trading; on the other hand, it uses protocol revenue to continuously buy back CARDS tokens to enhance the token's value support.

As platform trading continues to grow and protocol revenue increases accordingly, the scale of CARDS buybacks also expands. The rising token price further stimulates user participation in trading, card opening, and holding, thereby creating a flywheel effect.

Influenced by this, CoinGecko data shows that the CARDS token has accumulated an increase of over 412% since the beginning of this year, with its current FDV reaching $510 million. Recently, in a research report, Arthur Hayes' family office, Maelstrom, even set a $4 target price for CARDS by the end of summer, further boosting market attention.

It is worth mentioning that, according to a report by Maelstrom Fund analyst Lukas Ruppert, wallets related to Collector Crypt's operational center have cumulatively realized $45.7 million in USDC.

It is important to note that the CARDS token will face continuous unlocks. Currently, Collector Crypt has completed approximately 23.6% of its token unlocks, with the remaining tokens locked until November 2027. Among them, the next unlock is scheduled for June 29, expected to release about 28.84 million CARDS, valued at approximately $7.46 million. Additionally, the official recently disclosed that an early Pre-Seed round investor has sold about $1.5 million worth of CARDS tokens to a liquidity fund via an over-the-counter (OTC) transaction.

As operational funds flow out, tokens continue to unlock, and early investors begin to realize profits, the circulating supply in the market will gradually increase. Investors need to continuously monitor potential short-term market selling pressure.

Overall, the rise of Collector Crypt validates the viability of the on-chain TCG business model and has propelled this track into a rapid development phase. However, on-chain TCGs are still in the early stages of development, with significant room for growth in areas such as user expansion, asset supply, and infrastructure.