原文作者:Nancy,PANews

Arbitrum 无疑是数据表现较为强劲的 Layer 2 “优等生”之一,而跌势不止的币价是其“硬伤”,即便流通市值较上线之初已然翻倍。

4 个月新增近 26 亿美元解锁量, 97% 持有者处于亏损状态

与上线之初的 10.2 亿美元初始流通市值相比,如今 Arbitrum 代币 ARB 的流通市值已超 23 亿美元,但持有者却无法摆脱持续“失血”之困。IntoTheBlock 数据显示,Arbitrum 的价格表现疲软,目前有高达 97% 的 ARB 持有者处于亏损状态,仅有 3% 的持有者在当前价格持平,几乎没有持有者盈利。

根据 CoinGecko 数据显示,ARB 在今年 1 月创下 2.26 美元的历史新高,较 2023 年 3 月上线时涨幅达 67.4% ,但随后 ARB 开始一路下跌,并在近期创下历史低点,当前较峰值下跌 69% 。而其流通市值,却仅比高峰期下降 30% 。相比之下,ARB 的竞品 OP 的价格较上线之初的最高涨幅为 235% ,当前价格较峰值下跌超 65.6% ,流通市值则较高点下滑 61.2% 。

Arbitrum 流通市值

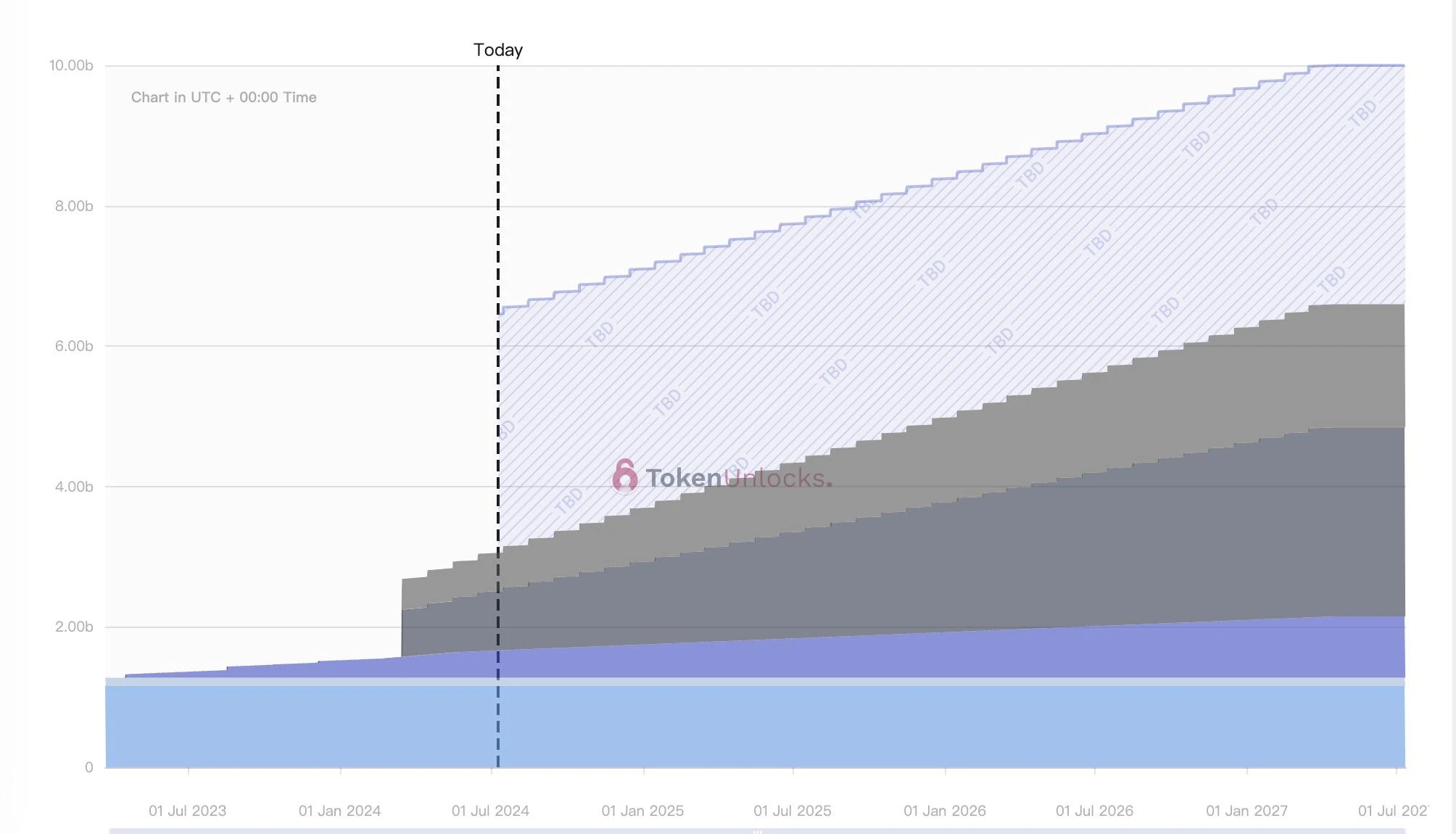

ARB 持续数月的颓废走势与其大额代币解锁有着直接关系,今年 3 月开始 Arbitrum 团队和投资者开始解锁大量 ARB 代币。根据 PANews 统计, 3 月至今,Arbitrum 来自团队和投资者的解锁量已超 13.8 亿枚 ARB,总价值超 25.9 亿美元。

而 Arbitrum 还将在每月 16 日还将面临着更多 ARB 解锁,比如 7 月开始将新增 Arbitrum DAO Treasury 的解锁,价值高达 24.1 亿美元,直至 2027 年 3 月预计增发约 400% 。根据 Token Unlocks 数据显示,截至 7 月 10 日,ARB 的解锁进度暂为 31% 。

若市场流动性持续走低,Arbitrum 持续的巨量解锁无疑会带动其代币价格进一步下探。比如加密分析平台 DYOR 不久前对此表示,鉴于现在的流动性,如果投资机构每个月卖出解锁额度的 5% ,如 ARB 等资产价格将可能下跌 30% 至 70% 。

多项数据仍具领先优势,生态补贴打法或难救币价

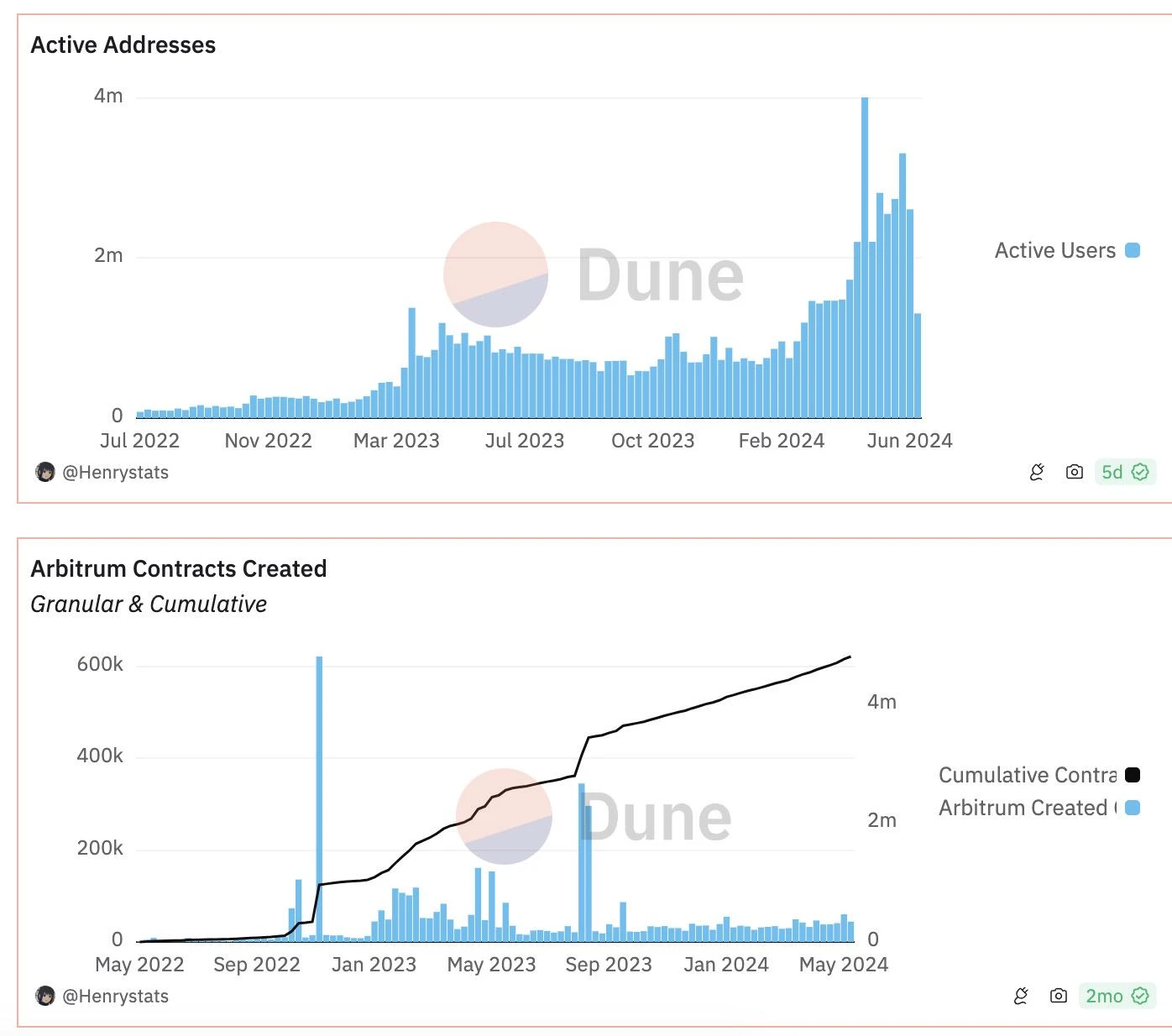

尽管币价表现不尽人意,但从数据来看,目前 Arbitrum 在众多L2中仍处于领先优势。

Dune Analytics 最新数据显示,截至 7 月 10 日,Arbitrum 创建账户总量超 3175.1 万个,交易总数已突破 8 亿笔。Arbitrum 链上桥接总锁仓量 TVB 已突破 300 万枚 ETH,桥接地址总量约 73.7 万个。且L2 BEAT 数据显示,Arbitrum One 以 161.2 亿美元 TVL 稳居第一,市场占比达 40.1% ;Growthepie 数据显示,Arbitrum 稳定币市值突破 40.7 亿美元位居首位,全年涨幅 116% ,超过 Base、OP Mainnet 和 ZkSync Era 等L2;过去 6 个月的活跃地址数增速达 205% ,超过 ZkSync、OP Mainnet 等。

Arbitrum 的生态数据无疑是靠大撒币模式补贴出来的。

一直以来,Arbitrum 不断打补贴这张牌助攻自身生态发展。例如在游戏上,今年 6 月 Arbitrum 批准了 2.25 亿枚 ARB 提案,用于资助 Arbitrum 上的游戏开发,旨在将 Arbitrum 打造成游戏领域的领先区块链,这些资金将在三年内进行分配;在 RWA 上,Arbitrum 拟为 RWA 发展计划分配 3500 万枚 ARB,旨在通过 RWA 生态系统的增长来实现每年 Arbitrum 1% 的财务多元化,现已获得超 99% 的投票支持率。

与此同时,Arbitrum 还在四处“撒钱”赞助项目,仅在 2023 年就 50 多个项目提供约 1060 万美元赠款,且这一年 Arbitrum 还推出了一项短期激励计划,旨在从 DAO 金库向 Arbitrum 上的活跃协议分配最多 5000 万枚 ARB 资金,有 106 个项目申请首轮资助。而在今年,Arbitrum 也在不断为各类项目资金支持,比如不久前 Open Campus 宣布获得 Arbitrum 基金会的资助,用于推出首个专为教育设计的 Layer 3 区块链 EDU Chain;Pendle 宣布获得 Arbitrum STIP 的 100 万枚 ARB 资助;Synthetix 推出 Arbitrum 流动性激励计划,提供 200 万枚 ARB 奖励来吸引流动性提供者、稳定币流动性和 Perps 交易活动;Curve Finance 声称已收到来自 Arbitrum 超 23.7 万枚 ARB 捐赠,用于向 Arbitrum 链上的 Curve 池提供激励。

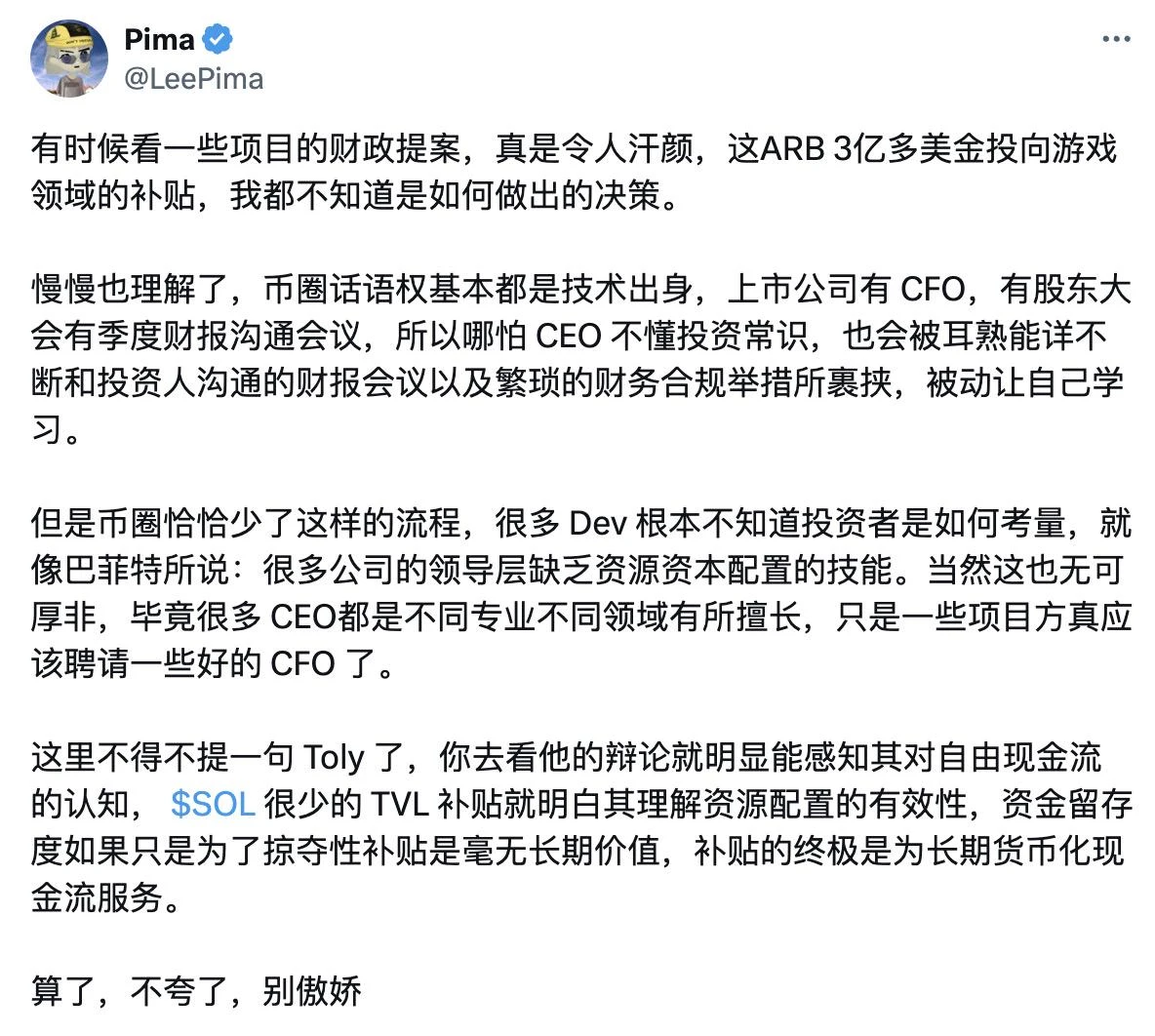

不过,Arbitrum 这种通过代币补贴建设生态的做法也引发不满,在社区看来,这种方式不仅未能给代币赋能,还增加了抛压。例如 Continue Capital 联创 Pima 发文直言,很多公司的领导层缺乏资源资本配置的技能,资金留存度如果只是为了掠夺性补贴是毫无长期价值,补贴的终极是为长期货币化现金流服务。KOL BITWU.ETH 则表示,Arb 是典型“低流通、高排放”的生态补贴打法,最终导致“市值不断增长、代币趋势波动”。说白了,这种方式就是不断牺牲二级市场,更适合趋势交易者,不是那种死拿就获得巨额赔率的币,这些币的价值早就被机构挖掘完了,得到了充分的估值,未来只有贝塔收益,没有阿尔法收益。

此外,Arbitrum DAO 还考虑借鉴科技巨头的做法实施并购来实现生态扩张。Arbitrum DAO 在今年 5 月批准了 Areta 公司的创始合伙人 Bernard Schmid 提出的一项为期八周的并购试点计划,营销公司、业务开发、基础设施提供商、稳定币发行人和零知识技术是最具吸引力的潜在收购目标。如果试点成功,Schmid 计划提出一个更加雄心勃勃的提案:建立一个拥有 1 亿至 2.5 亿美元资金池的并购部门,并在两年内识别和收购潜在目标。DeepDAO 数据显示,Arbitrum 财库持仓价值为 26 亿美元,其中 97.4% 为代币 ARB,较峰值下降了超 65.7% 。

值得一提的是,Arbitrum 还尝试在产品和治理等方面进行迭代更新来优化开发者和用户体验,例如今年 4 月,Arbitrum 基金会拟更改 Arbitrum 扩展计划,以允许在任何区块链上部署新的 Orbit 链;上月底 Arbitrum 基金会提议采用新交易排序策略 Timeboost,来增强网络交易的效率和公平性;Arbitrum 宣布将推出结合零知识证明和 Stylus MultiVM 的功能等。

在治理提案中,对代币有直接刺激作用的是,Arbitrum 提出的新 ARB 质押奖励提案,拟使用 50 %排序器费用奖励质押,从而增强 DAO 的经济安全性并降低资金库遭受攻击的风险。DeFi 研究员@DefiIgnas 对此表示,在此计划中,使用未来剩余排序器费用的 50% 来奖励 ARB 代币质押者,假设年度费用为 12, 000 ETH,且 ARB 价格为 1 美元,这将转化为 7% 的 APY,这种与代币持有者分享收入的机制对于处在下跌状态的 ARB 来说是个明智的提案。

从目前来看,面对巨量解锁压力,Arbitrum 的生态补贴打法尚未对 ARB 价格起到明显提振作用,而随着市场对低流通高 FDV 玩法的争议愈演愈烈,Arbitrum 将面临更大挑战。