Japan's government bond market is experiencing volatility unseen in decades, prompting global asset management institutions to re-examine a long-ignored risk: will Japanese investors, who hold approximately $1 trillion in US Treasury bonds, move their money back home?

According to a recent report by the Financial Times, several investment firms have begun preparing for the potential large-scale repatriation of Japanese capital, betting that Japanese investors will gradually sell US Treasuries and instead buy Japanese Government Bonds (JGBs) with their continuously rising yields.

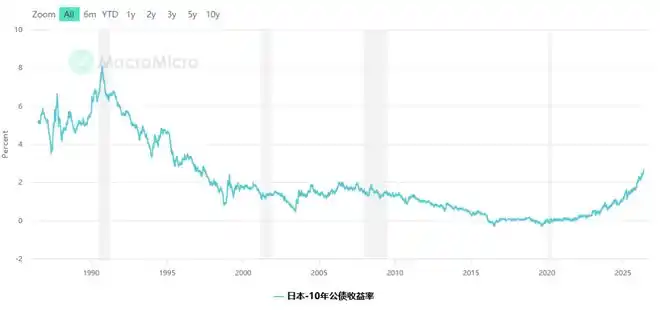

Soaring JGB Yields Hit Multi-Decade Highs

On Friday, Japan's benchmark 10-year government bond yield rose to 2.73% in intraday trading, its highest level since May 1997.

The yield on 30-year JGBs broke through 4% for the first time—a level never reached since these bonds were first issued in 1999. Yields on 5-year and 20-year bonds also hit record highs earlier this week.

Japanese Finance Minister Satsuki Katayama told reporters on Friday that yields on benchmark bonds in major global markets are rising, "These dynamics influence each other, creating a compounding effect."

Analysts expect JGB yields to continue climbing. The Bank of Japan raised its policy rate to 0.75% in December last year, the highest in thirty years, and the market widely anticipates another 25 basis point hike to 1% this June.

The $1 Trillion 'Repatriation to Japan' Logic

To understand this bet, one must first understand why Japanese investors hold such vast assets overseas.

For decades, Japan maintained ultra-low interest rates, offering almost no return on domestic bonds. To seek yields, Japanese institutional investors such as insurance companies, pension funds, and banks went on a massive overseas buying spree, purchasing US Treasuries, European bonds, and various global assets.

Currently, Japanese investors hold roughly $1 trillion in US Treasury bonds, making them the largest foreign holder of US debt, far surpassing other countries.

Now, with Japanese bond yields rising sharply, this logic is reversing. Mark Dowding, Chief Investment Officer at British asset manager BlueBay, directly highlighted this shift. BlueBay just launched its first Japanese bond fund in March this year.

Dowding stated: "New money will not be deployed overseas. It won't go into US corporate bonds, it won't go into US Treasuries; it will come back and be deployed domestically in Japan."

'Trickle' of Capital Repatriation Has Begun

Market data shows signs of capital returning, although the scale is still small.

According to fund tracker EPFR, investors netted about $700 million into Japanese sovereign bond funds in March, setting a record for the largest monthly inflow in the category's history. April saw a net inflow of $86 million, returning to recent normal levels.

Ruffer fund manager Matt Smith offered a more direct assessment. He said: "The pressure is building—long-end domestic yields keep going up, and the signal at an institutional level is 'please bring your money back to Japan'. We think the yen appreciation will happen slowly at first, then all at once."

Smith also said Ruffer currently holds a long yen position as a core hedging tool. "In a market dislocation, particularly one centered around US credit markets, you will get Japanese investors bringing capital back home, and the yen will strengthen."

Large-Scale Repatriation Not Yet Happening, JGBs Have Their Own Concerns

However, analysts caution that Japanese institutional investors are still net buyers of foreign bonds.

RBC Capital Markets Asia macro strategist Abbas Keshvani pointed out that although JGB yields now "superficially offer better compensation for investors," over the past 12 months, Japanese investors have still been net buyers of about $50 billion in foreign bonds.

The reason lies in the uncertainty within the JGB market itself. Japanese Prime Minister Sanae Takaichi won the election this February, with campaign promises including expanded government spending and subsidies to ease inflation pressures. Analysts increasingly warn that the government will be forced to compile a supplementary budget later this year, which would further depress JGB prices and push yields higher.

Keshvani said: "Both supply and demand dynamics point to yields moving higher. As an investor, it's very difficult to have the will to step in now if you know yields will continue to rise."

Previously, the Bank of Japan, through quantitative easing and yield curve control policies, was the market's most significant buyer of JGBs. As the BOJ gradually exits, the market returns to traditional supply-demand logic, leading to noticeably increased volatility in JGB prices.

Implications for the US Treasury Market

The potential scale of Japanese capital repatriation forces the US Treasury market to take this risk seriously.

Japan is the largest foreign holder of US Treasury bonds, with holdings of approximately $1 trillion. If Japanese institutional investors begin systematically reducing their holdings, the impact on the supply-demand dynamics of US Treasuries would be substantial.

Currently, Wall Street's bet is more of a forward-looking positioning rather than a reaction to an established fact. But as Japanese bond yields continue to climb—with analysts viewing a 10-year JGB yield reaching 3% later this year as a realistic target—the logic behind this bet will become increasingly clear.