Автор:Wintermute

Компиляция: Shenchao TechFlow

Введение от Shenchao: Эта статья написана трейдером Wintermute OTC и глубоко анализирует коренные причины оттока розничного капитала с крипторынка. Исторически бычьи тренды на крипторынке часто подпитывались спекуляциями розничных инвесторов, но последние данные показывают, что розничные инвесторы с рекордной скоростью устремляются на фондовый рынок США, в результате чего крипторынок и рынок акций США из режима «роста и падения в унисон» превратились в «качели». По мере снижения волатильности крипторынка, снижения порогов входа и выхода, а также благодаря возможностям анализа на фондовом рынке, которые ИИ предоставил розничным инвесторам, криптовалюты перестали быть их предпочтительным выбором для спекуляций. Понимание этой логики ротации капитала поможет нам пересмотреть рамки мульти-активного инвестирования.

Полный текст:

Активность розничных инвесторов всегда двигала крипторынок. Спекуляции, рефлекторные покупки на падениях и гибкая ротация капитала между различными токенами — розничные инвесторы определяли каждый крупный цикл в истории криптовалют. Но последние данные указывают на то, что отношения между розничными инвесторами и крипторынком меняются.

Мы уже некоторое время предупреждаем, что фондовый рынок США привлекает внимание розничных инвесторов в ущерб ликвидности альткойнов. Новые данные от стратегического подразделения J.P. Morgan, в сочетании с нашими эксклюзивными данными о потоках средств, дополнительно свидетельствуют: акции США и криптовалюты становятся взаимозаменяемыми рискованными активами.

Разворот корреляции

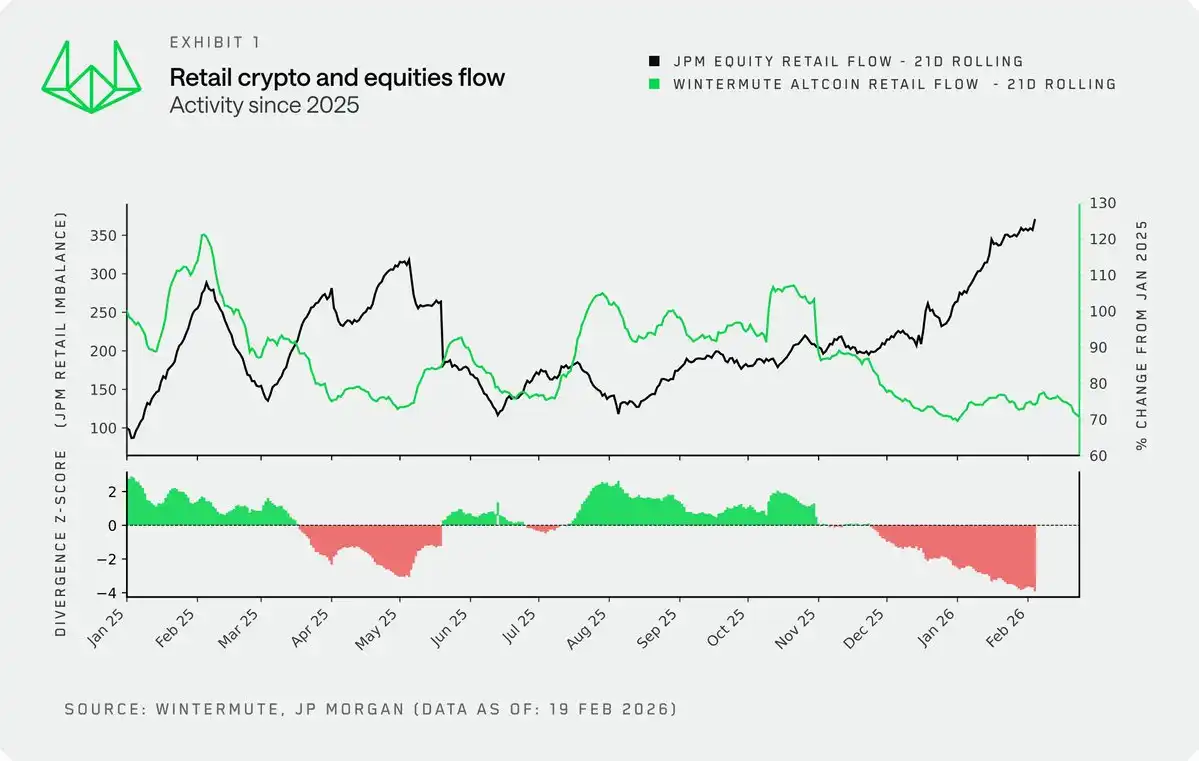

Наложив эксклюзивные данные Wintermute о потоках средств розничных инвесторов в криптовалюты на данные J.P. Morgan о притоках средств розничных инвесторов в акции США, мы получили новый взгляд на отношения между активностью розничных инвесторов на этих двух рынках.

Исторически они обычно двигались синхронно. До конца 2024 года рост аппетита к риску обычно означал покупки на обоих рынках, поскольку в некотором смысле оба они были отдушиной для избыточного капитала (см. данные M2) и риска. Однако с конца 2024 года эта связь разорвалась. Сегодня мы наблюдаем самый серьезный разрыв в новейшей истории: розничные инвесторы с рекордной скоростью идут в акции США, а на крипторынке предпочитают держать монеты и выжидать.

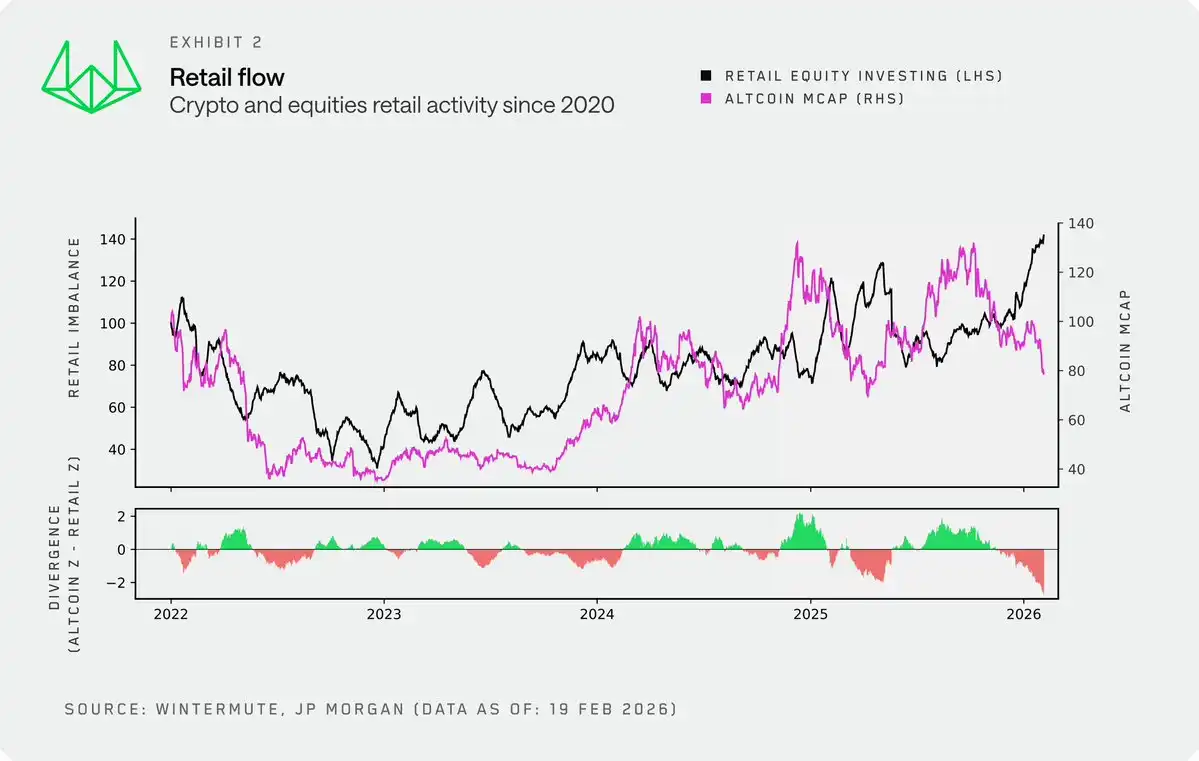

Рассматривая более длительный период, мы используем общую рыночную капитализацию альткойнов в качестве долгосрочного индикатора активности розничных инвесторов в криптовалютах. Она сильно коррелирует с нашими данными о потоках средств и имеет более объективную и длинную историю. С 2022 года до конца 2024 года криптовалюты и акции США в целом двигались одинаково, розничные инвесторы рассматривали оба актива как часть高风险ового инвестиционного портфеля. Но разрыв в конце 2024 года особенно заметен, торговое поведение розничных инвесторов стало более краткосрочным, волатильным и лишенным структуры.

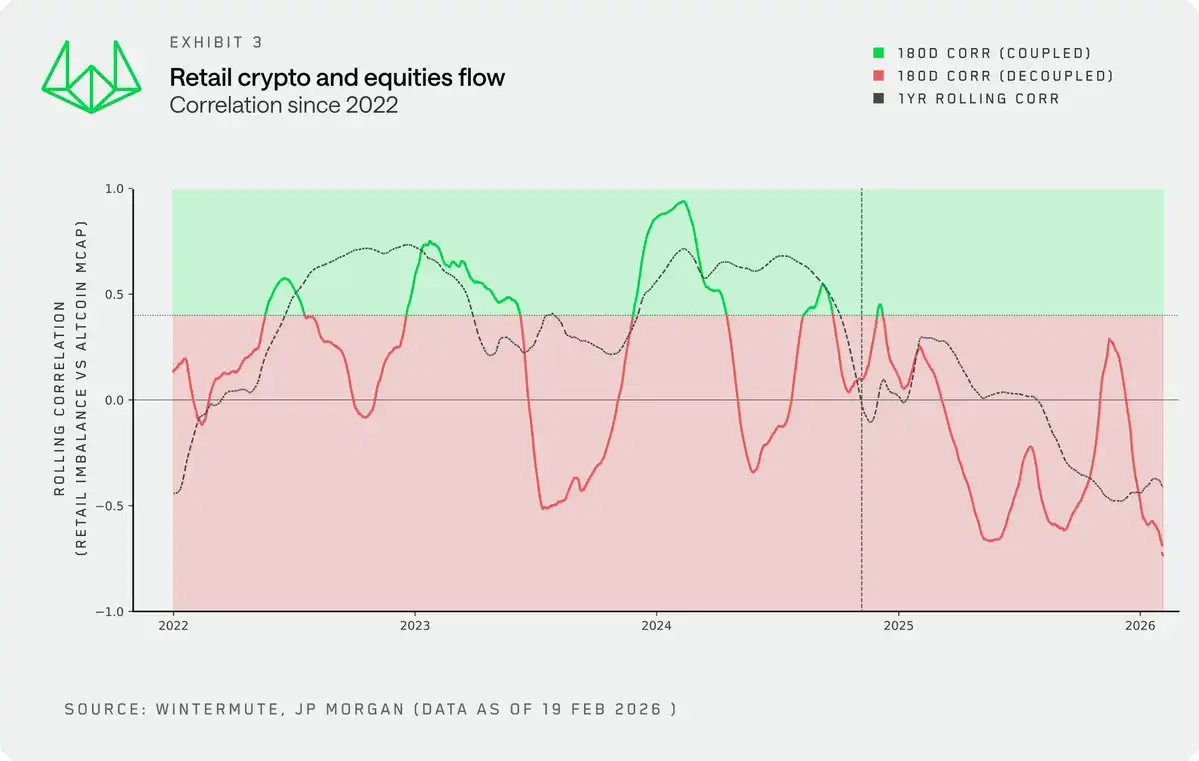

Скользящая корреляция между активностью розничных инвесторов и капитализацией альткойнов подтверждает этот сдвиг. Раньше была волатильная, но в целом положительная корреляция, теперь же она стала отрицательной. Теперь розничные инвесторы распределяют капитал по принципу «или-или», а не покупают одновременно на обоих рынках.

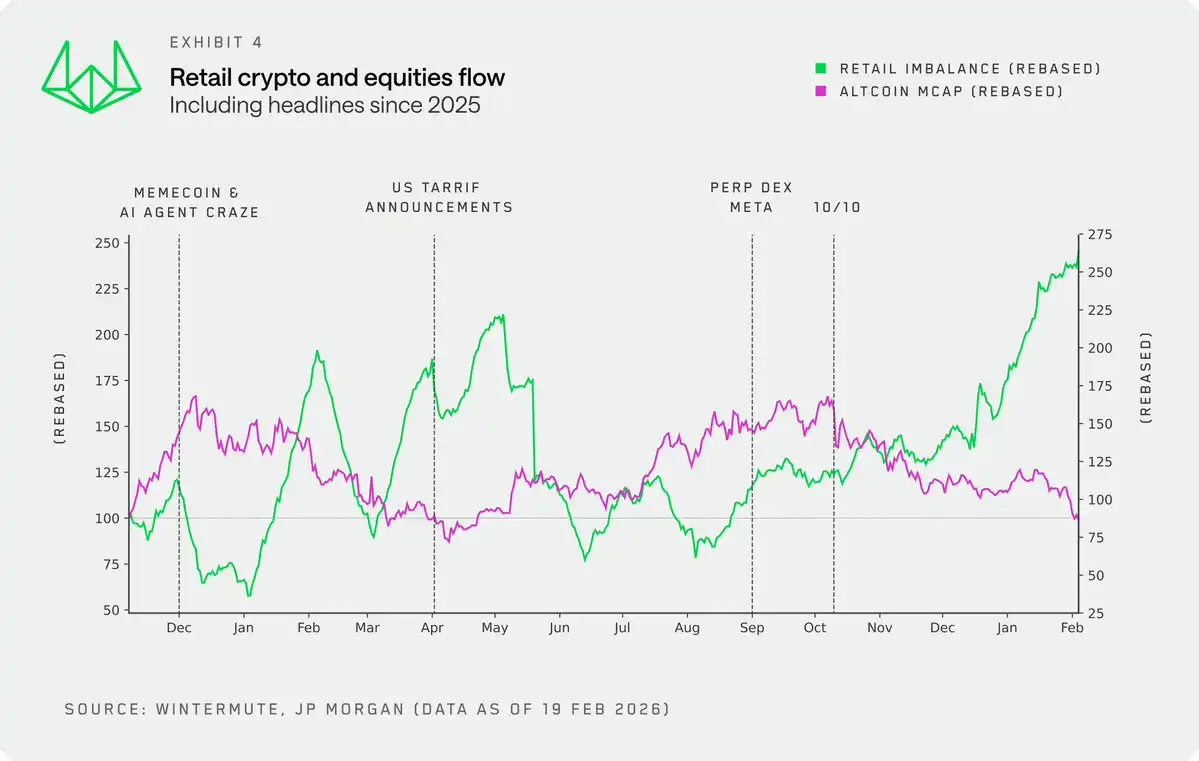

Если сфокусироваться на 2025 годе и ключевых событиях-катализаторах, эта динамика становится еще clearer. Несколько моментов особенно очевидны:

- Когда активность на фондовом рынке США замирала, мемкойны и AI-агенты переживали звездный час, розничные инвесторы переносили спекулятивный спрос в эти области.

- Как во время объявления тарифной политики в апреле 2025 года, так и в последнее время розничные инвесторы продолжали агрессивно покупать акции США на падениях.

- После 10 октября средства почти полностью перетекли в акции США, и эта тенденция сохраняется до сих пор.

Причинно-следственная связь

Важно прояснить: мы не считаем, что масса розничных инвесторов на крипторынке достаточно велика, чтобы оттянуть средства с фондового рынка США. Скорее наоборот, именно высокий ажиотаж розничных инвесторов на фондовом рынке США истощает ликвидность крипторынка.

Новые данные также подтверждают это. Активность розничных инвесторов на фондовом рынке США стала новой переменной, за которой криптоинвесторам следует внимательно следить, чтобы найти окна возможностей, когда средства розничных инвесторов могут обеспечить устойчивые покупки на крипторынке.

Волатильность как продукт

Хотя причин много, но одна из ключевых причин, почему розничные инвесторы были так активны и привлечены крипторынком, — это волатильность этого актива. Волатильность сама по себе является продуктом. Именно это изначально и привлекло розничных инвесторов в криптосферу.

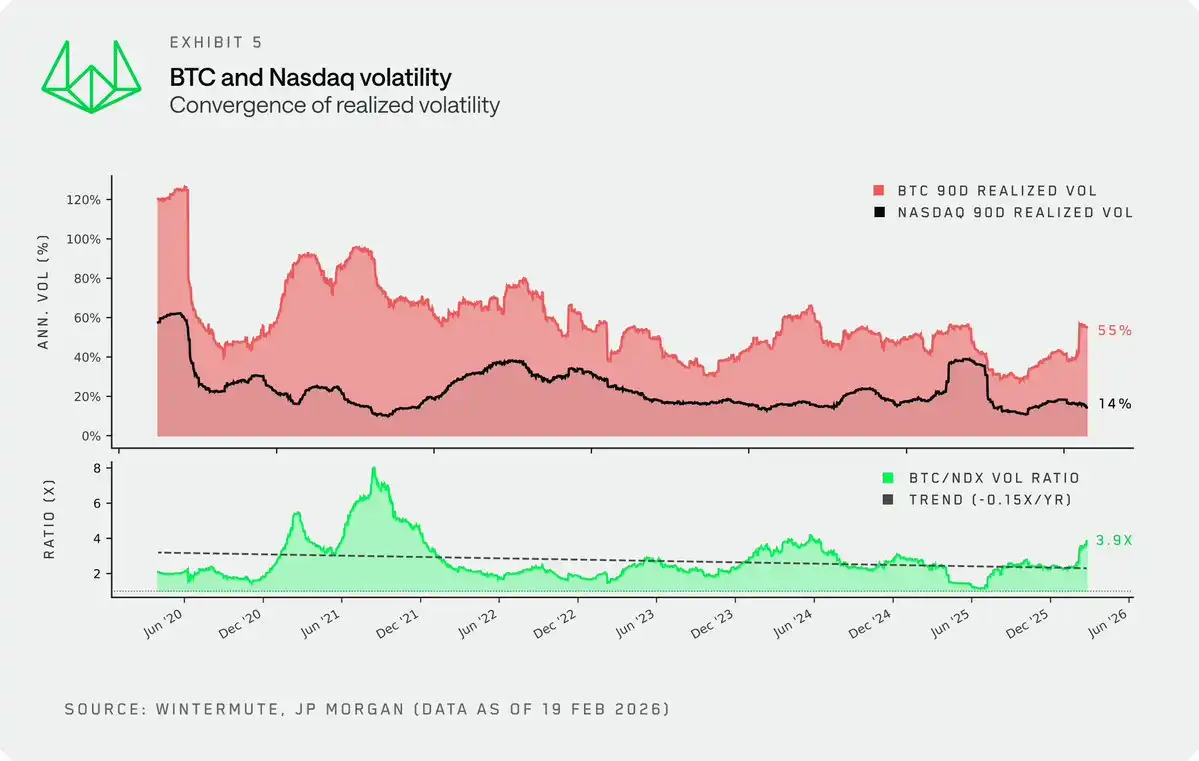

Однако, хотя волатильность крипторынка по-прежнему значительно превышает волатильность фондового рынка США, его реализованная волатильность (realized volatility) подвергается структурному сжатию, и этот тренд трудно обратить вспять. Соотношение волатильности BTC и индекса Nasdaq 100 (NDX) продолжает снижаться, в первой половине 2025 года это соотношение сжалось даже ниже двукратного значения.

Размышления о некоторых ключевых драйверах:

- Созревание рынка. Растущее число зрелых инвесторов в сочетании с появлением новых инструментов ликвидности, таких как ETF и DAT, подавляет типичную для ранних циклов волатильность, вызванную рефлекторными действиями.

- Размер рынка. При текущей общей капитализации крипторынка в 2,3 трлн долларов, даже с откатом на 40% от исторических максимумов (ATH), для роста рынка сейчас требуется гораздо больше капитала, чем пять лет назад.

По мере сжатия волатильности ослабевает и ключевое торговое предложение криптовалют для розничных инвесторов. Те резкие взлеты и падения, которые определяли бычий цикл 21-22 годов и привлекли целое поколение розничных инвесторов, остались в прошлом. Для розничных инвесторов, ищущих волатильность, фондовый рынок США становится все более привлекательным.

Технологические драйверы

Помимо структурных изменений на самом крипторынке, технологические драйверы также ускоряют эту ротацию капитала, и этому аспекту уделяется недостаточно внимания на рынке.

- Интеграция инвестиционных каналов. Интеграция торговли криптовалютами в платформы финтеха и традиционных брокеров (или интеграция торговли акциями США на крипто-нативных платформах) действительно снизила порог входа, но ее более глубокое влияние проявляется в «оттоке средств». В предыдущих циклах сложные процессы ввода и вывода средств фактически запирали капитал внутри крипторынка после его попадания туда, что способствовало органической ротации между различными токенами. Сегодня же такие же плавные каналы ввода-вывода означают, что средства могут свободно перемещаться между криптовалютами и акциями США без каких-либо препятствий.

- Познавательное преимущество (The edge). Розничные инвесторы, похоже, все больше привлекаются фондовым рынком США отчасти потому, что благодаря ИИ они получают совершенно новое преимущество. Большие языковые модели (LLM) значительно повысили аналитические возможности розничных инвесторов, создав у них иллюзию возможности на равных конкурировать с институциональными игроками.

Но на крипторынке такого ощущения нет. Хотя вы также можете анализировать криптопроекты на основе данных, в криптосфере отсутствуют консенсусные frameworks оценки и механизмы захвата стоимости токенов, а количество инвестиционных активов продолжает бесконечно расширяться, что makes it difficult for розничным инвесторам найти здесь это чувство «преимущества».

Заключение

Розничные инвесторы когда-то были самым надежным источником рефлекторного спроса на крипторынке, но теперь их аппетит к риску все чаще удовлетворяется в других местах. Фондовый рынок США предлагает highly конкурентную волатильность, предоставляет розничным инвесторам不断增强ющее аналитическое преимущество, и через одно и то же приложение на телефоне средства можно seamlessly переключать между крипторынком и акциями США. Криптовалюты по-прежнему занимают свое место в инвестиционных портфелях розничных инвесторов, но теперь они лишь один из многих инструментов для игры, а не предпочтительный носитель для спекуляций.

Этот сдвиг также должен изменить视角, через которую инвесторы смотрят на рынок. Некоторые проверенные индикаторы перестали работать. Для криптоинвесторов, стремящихся к успеху, уже недостаточно просто искать опережающие индикаторы аппетита к риску и сочетать их с крипто-нативными frameworks. Инвесторам все чаще необходимо рассматривать криптовалюты через призму мульти-активного инвестиционного портфеля, как это уже давно стало стандартной практикой на рынках акций США и fixed income.