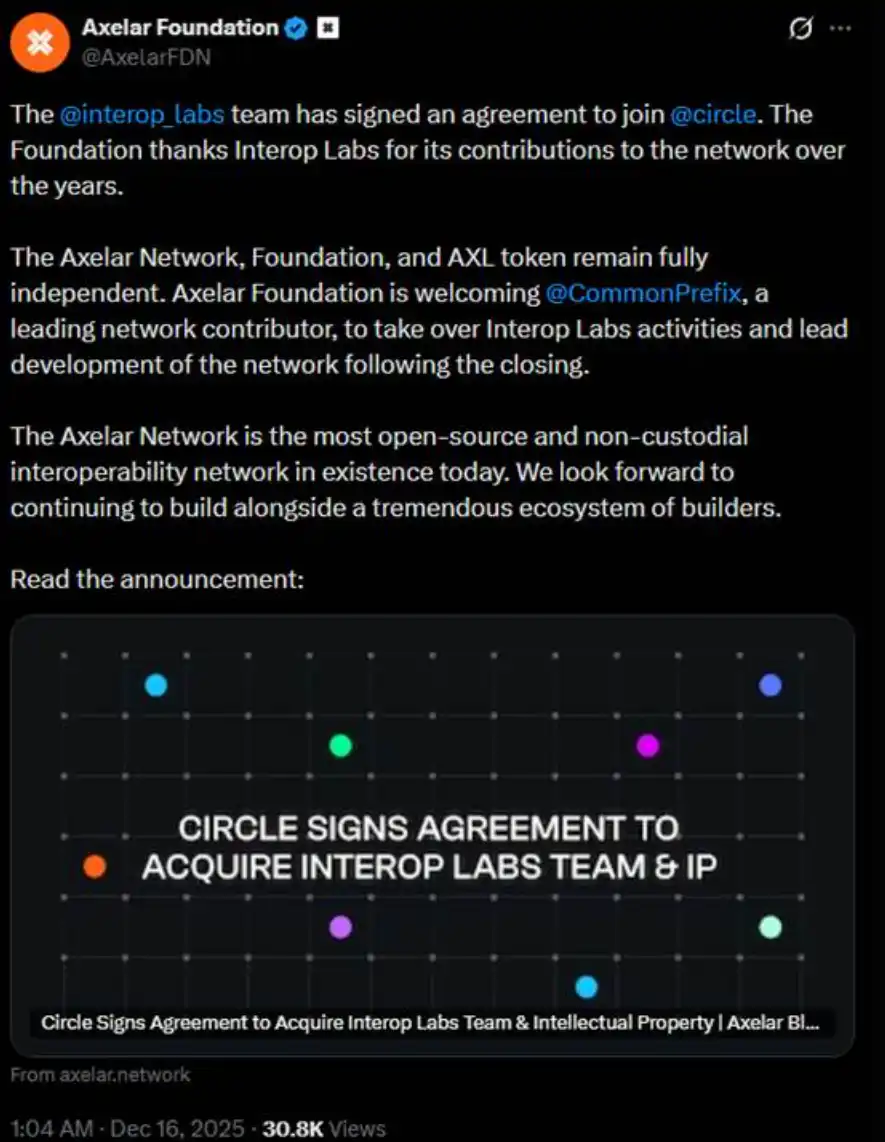

Позапрошлой ночью команда Interop Labs (первоначальный разработчик Axelar Network) объявила о приобретении компанией Circle для ускорения развития своей мультичейн-инфраструктуры Arc и CCTP.

Казалось бы, поглощение — это хорошая новость. Однако дальнейшие разъяснения команды Interop Labs в том же твите вызвали бурную реакцию. Они заявили, что сеть Axelar, фонд и токен AXL продолжат работать независимо, а разработку возьмёт на себя CommonPrefix.

Иными словами, суть сделки заключается в «интеграции команды в Circle» для продвижения USDC в сфере приватных вычислений и регулируемых платежей, а не в полном поглощении сети Axelar или её токенной системы. Команду и технологии забирает Circle. Исходный проект Circle не трогает.

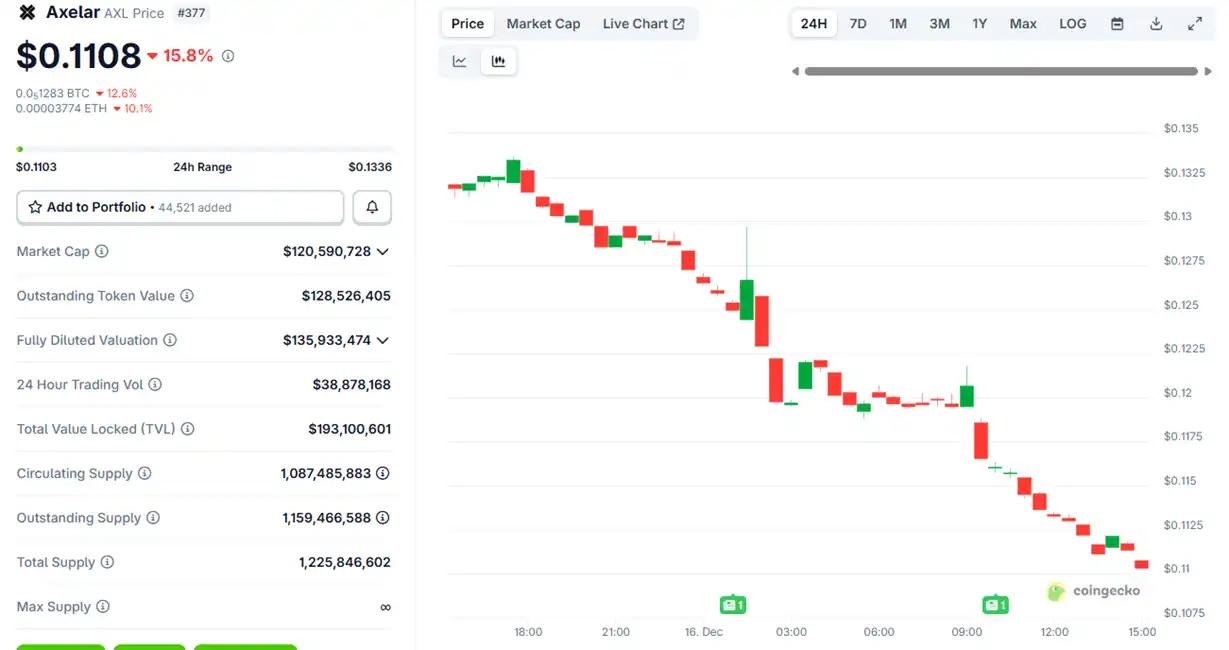

После объявления о поглощении цена токена Axelar $AXL сначала немного выросла, а затем начала падать, к настоящему моменту потеряв около 15%.

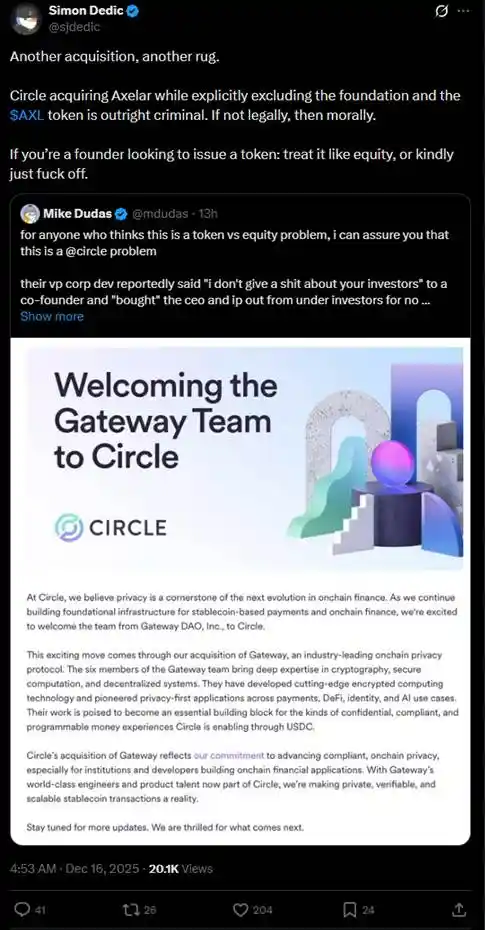

Такое решение быстро спровоцировало в сообществе жаркие дискуссии на тему «токен vs акции». Многие инвесторы выразили сомнения, что Circle, приобретая команду и интеллектуальную собственность, по сути получает ключевые активы, но при этом обходит права держателей токена AXL.

За последний год подобные случаи «забрать команду и технологии, но не токены» в криптосфере происходили неоднократно, нанося серьёзный ущерб розничным инвесторам.

В июле фонд Layer 2 сети Ink, принадлежащей Kraken, приобрёл децентрализованную торговую платформу Vertex Protocol на базе Arbitrum, получив её инженерную команду и торговую технологическую архитектуру, включая синхронизированный стакан заявок, движок перпетуальных контрактов и код денежного рынка. После поглощения Vertex прекратила работу на 9 EVM-чейнах, а токен $VRTX был упразднён. После объявления $VRTX в тот же день упал более чем на 75%, а затем постепенно «обнулился» (текущая капитализация составляет всего 73 000 долларов).

Однако у держателей $VRTX была хотя бы слабая надежда, поскольку во время TGE Ink они должны были получить 1% аирдропа (снепшот уже сделан). Но бывает и хуже — когда токен просто аннулируют без какой-либо компенсации.

В октябре pump.fun объявил о покупке торгового терминала Padre. При этом в сообщении о поглощении pump.fun также заявил, что токен Padre больше не будет использоваться на платформе, и прямо указал, что для этого токена нет будущих планов. Поскольку заявление об аннулировании токена было в последнем ответе ветки, токен мгновенно вырос в два раза, а затем резко упал; сейчас капитализация $PADRE составляет всего 100 000 долларов.

В ноябре Coinbase объявила о покупке торгового терминала Solana Vector.fun, созданного Tensor Labs. Coinbase интегрировала технологии Vector в свою инфраструктуру DEX, но это не касается самого NFT-маркетплейса Tensor или прав на токен $TNSR; часть команды Tensor Labs перешла в Coinbase или другие проекты.

Динамика $TNSR — относительно стабильная среди примеров: рост с последующим откатом, текущая цена вернулась к уровню, подобающему токену NFT-маркетплейса, и всё ещё выше минимума до новости о поглощении.

В Web2 поглощение малыми компаниями крупными предприятиями по принципу «забрать команду и интеллектуальную собственность, но не доли» является законным; такая ситуация называется «acquihire». Особенно в tech-индустрии «acquihire» позволяет крупным предприятиям быстро интегрировать优秀 команды и технологии, избегая длительного процесса найма с нуля или внутренней разработки, тем самым ускоряя разработку продукта, выход на новые рынки или повышая конкурентоспособность. Хотя это невыгодно мелким акционерам, это стимулирует общий экономический рост и технологические инновации.

Тем не менее, «acquihire» также должен соответствовать принципу «действовать в наилучших интересах компании». Причины, по которым эти примеры из криптосферы вызывают такую ярость сообщества, заключаются в том, что «мелкие акционеры» в лице держателей токенов совершенно не согласны с тем, что стороны криптопроектов действуют «в наилучших интересах компании» ради лучшего развития проекта при поглощении. Стороны проектов часто мечтают о выходе на американский фондовый рынок, когда проект приносит большие деньги, а затем выпускают токены для заработка, когда всё только начинается или заходит в тупик (самый яркий пример — OpenSea). Заработав на токенах, они тут же ищут себе новое место, а старые проекты остаются лишь в их резюме.

Так что же, розничным инвесторам в криптосфере остаётся только молча глотать обиду? Именно позавчера бывший технический директор Aave Labs Эрнесто опубликовал governance-предложение под названием «$AAVE Alignment Phase 1: Ownership», сделав первый выстрел в защиту прав на токены в криптосфере.

Предложение主张 о том, чтобы Aave DAO и держатели токена Aave чётко завладели核心 правами, такими как IP протокола, бренд, доли и доходы. Представитель поставщика услуг Aave Марк Зеллер и другие публично поддержали это предложение, назвав его «одним из самых влиятельных предложений в истории управления Aave».

Эрнесто отметил в предложении: «Из-за некоторых прошлых событий предыдущие посты и комментарии выражали сильную враждебность к Aave Labs, но это предложение стремится оставаться нейтральным. Оно не implies, что Aave Labs не должна быть контрибьютором DAO или lacks легитимности или способности вносить вклад, но решение должно приниматься Aave DAO».

Согласно интерпретации крипто-эксперта @cmdefi, причиной данного конфликта стала замена Aave Labs интегрированного во фронтенд ParaSwap на CoW Swap, после чего产生的费用 потекли на私人 адрес Aave Labs. Соответственно, сторонники Aave DAO считают это грабежом, поскольку существует governance-токен AAVE, и все выгоды должны в первую очередь流向 держателям AAVE или оставаться в казначействе для решения путём голосования DAO. Кроме того, ранее доход от ParaSwap持续流入 в DAO, а новая интеграция CoW Swap изменила эту ситуацию, что ещё больше убедило DAO в том, что это грабёж.

Это очень прямо отражает矛盾, подобную «собранию акционеров и руководству», и вновь подчёркивает неловкое положение прав на токены в криптоиндустрии. На ранних этапах индустрии многие проекты рекламировались через «захват стоимости» токенов (например, получение вознаграждения через стейкинг или просто прямое распределение доходов). Но с 2020 года enforcement actions SEC (такие как иски против Ripple, Telegram) вынудили индустрию перейти на «utility-токены» или «governance-токены», которые подчёркивают права использования, а не экономические права. В результате держатели токенов часто не могут напрямую делиться прибылью проекта — доход проекта может утекать к команде или акциям, принадлежащим VC, а держатели токенов остаются мелкими акционерами, работающими за идею.

Как в приведённых выше примерах, стороны проектов часто продают команды, технологические ресурсы или доли VC или крупным предприятиям, одновременно продавая токены розничным инвесторам, и в конечном итоге выигрывают владельцы ресурсов и долей, а держатели токенов отодвигаются на задний план или остаются ни с чем. Потому что токены не обладают правами инвестора в юридическом смысле.

Чтобы обойти регулирование «токен не может быть ценной бумагой», токены проектировались всё более «бесполезными». Из-зание регулирования вновь поставило розничных инвесторов в крайне пассивное, незащищённое положение. Произошедшие в этом году种种 случаи уже某种意义上 напомнили нам, что проблема «отказа нарративов» в криптосфере, возможно, заключается не в том, что люди действительно перестали верить в нарративы — нарративы по-прежнему хороши, прибыль тоже неплоха, но когда мы покупаем токены, чего именно мы можем ожидать?