Автор: Max.s

Оригинальное название: Поглощенная промежуточная зона: Станет ли конечная цель Web3 еще одним игровым столом Уолл-стрит

В течение долгого времени многие аборигены криптомира пребывали в плену грандиозного нарратива: Web3 совершит революцию против Web2, стоит только перенести акции NASDAQ в блокчейн, заменить механизм сопоставления Нью-Йоркской фондовой биржи смарт-контрактами, и в конечном итоге с помощью RWA будет перестроены мировые финансы.

Глядя на постоянно меняющиеся графики на экране, нам следует вспомнить эту дату: 10 ноября 2023 года. В этот день из-за сильных ожиданий одобрения первого спотового ETF на криптовалюты, институциональные средства крупными потоками устремились через регулируемые каналы, что привело к резкому росту открытых позиций на CME и позволило ему обогнать Binance.

Данные CME на тот день: открытые позиции достигли примерно 111,1 тыс. BTC, номинальная стоимость около 4,08 млрд долларов США (на тот момент это составляло около 24,7% от общего объема открытых позиций в сети).

Данные Binance: открытые позиции около 103,8 тыс. BTC, номинальная стоимость около 3,8 млрд долларов США.

Мы должны признать суровую реальность: это будет одностороннее поглощение!

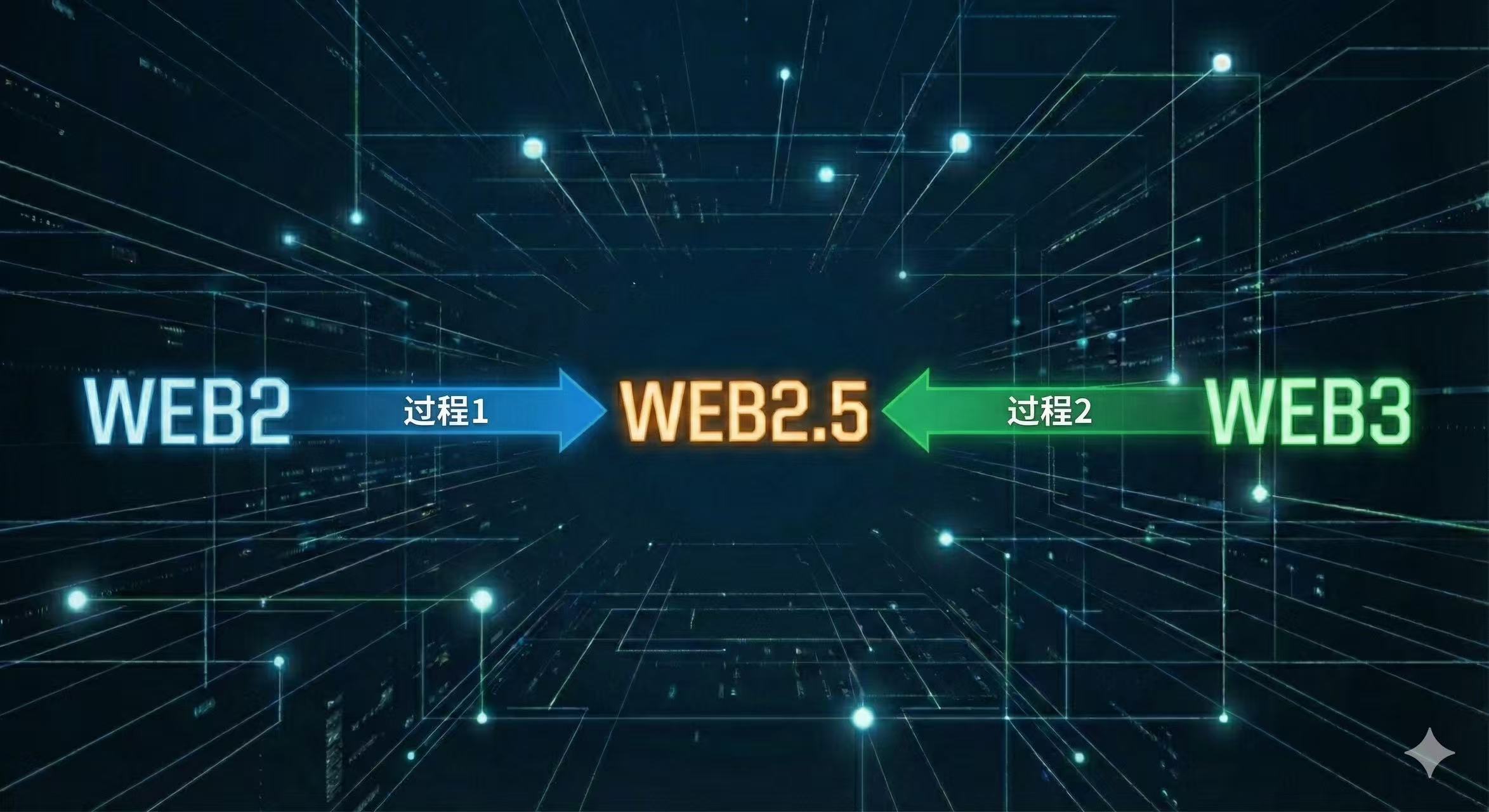

Взгляните на этот график

Процесс 1 на графике — это экспансия традиционных финансов (TradFi) в криптопространство, например, запуск фьючерсов на CME, запуск ETF от BlackRock; процесс 2 — это проникновение криптофинансов в традиционные активы, например, токенизация акций, RWA (реальные мировые активы).

Ответ, который дает текущий рынок, ясен: процесс 1 продвигается стремительно, процесс 2 — с большим трудом. Ключевое различие заключается не в технологиях, а в «стоимости соответствия требованиям» (compliance cost), которая вызывает снижение размерности ликвидности.

Почему гиганты Уолл-стрит могут так легко вторгнуться в сердцевину криптосообщества, а мы не можем атаковать их крепости?

В экономике все объясняется предельными издержками (marginal cost).

Для CME, CBOE (Чикагской биржи опционов), EUREX (Европейской биржи деривативов) или SGX (Сингапурской биржи) предельные издержки на запуск деривативов на Биткоин практически равны нулю.

Эти финансовые монстры обладают лицензиями на клиринг, которые работают десятилетиями, чрезвычайно зрелыми моделями управления рисками и выделенными сетями, подключенными к крупнейшим хедж-фондам мира. Для них Биткоин — это всего лишь еще один тикер после золота, нефти, соевых бобов. Им не нужно переписывать базовый код, не нужно нанимать новый compliance-отдел, даже не нужно заново обучать клиентов. Им достаточно подать заявку в CFTC (Комиссию по торговле товарными фьючерсами США), изменить несколько параметров — и рождается новый, регулируемый рынок, способный выдержать流动性 в сотни миллиардов.

В противоположность этому, процесс 2, когда криптобиржи пытаются «токенизировать акции», сталкивается с непреодолимой пропастью.

Помните токены акций, которыми так гордился FTX? Это была не только одна из причин его краха, но и первородный грех в глазах регуляторов. Криптоплатформа, желающая на законных основаниях позволить пользователям покупать акции Tesla за USDT, должна получить лицензию брокера-дилера ценных бумаг, клиринговую лицензию, решить проблемы конфликта законов о ценных бумагах в разных юрисдикциях, внедрить чрезвычайно сложные процессы KYC/AML. Комплаенс-издержки здесь не линейные, а экспоненциальные.

Для крипто-нативных компаний это война, которая закончилась, еще не начавшись. Традиционные финансы не просто сами по себе соответствуют требованиям, они — создатели этих требований.

Почему стоимость соответствия так важна? Потому что compliance напрямую определяет безопасность, а безопасность определяет порог входа для капитала.

Розничные инвесторы на крипторынке часто misunderstand источник «ликвидности». Настоящая ликвидность исходит не от нескольких тысяч долларов у розничных инвесторов, а от пенсионных фондов, эндаумент-фондов, суверенных фондов благосостояния и крупных маркет-мейкеров.

Эти гиганты сталкиваются с чрезвычайно строгими фидуциарными обязанностями (Fiduciary Duty). Это объясняет, почему одобрение спотового Биткоин-ETF в 2024 году стало историческим переломным моментом.

До ETF традиционному семейному офису, желавшему инвестировать в Биткоин, требовалось пройти чрезвычайно сложную процедуру одобрения: кто управляет приватными ключами? Что делать, если биржа взломана? Как проводить аудит? ETF и фьючерсы на CME идеально решают эту проблему: не нужно управлять приватными ключами, не нужно доверять офшорным биржам, все делается в рамках обычного брокерского счета для торговли акциями.

Рекордные уровни открытых позиций по фьючерсам на Биткоин на CME — это не результат спекуляций розничных трейдеров, а арбитраж базисного спреда (basis trading) и хеджирование рисков со стороны институтов Уолл-стрит. Высокочастотные трейдеры уровня Jump Trading, Jane Street имеют более низкую задержку в серверных комнатах CME, чем на AWS.

Когда CBOE планирует вернуться на рынок криптодеривативов, когда SGX и EUREX начинают разворачивать регулируемые каналы для деривативов в Азии и Европе, мы видим четкий тренд: право定价 (pricing power) на криптоактивы переходит от офшорных, нерегулируемых бирж (таких как BitMEX на раннем этапе, части офшорных CEX сейчас) к регулируемым традиционным финансовым биржам.

Подобно тому, как фьючерсы на нефть не требуют от владельца фактически перевозить нефть, будущим криптофинансам не потребуется от инвесторов фактически использовать децентрализованные кошельки.

В этом процессе криптовалюты сами по себе лишаются свойства «валюты» как средства платежа, лишаются идеологии «сопротивления цензуре», очищаются до чисто финансового, высоковолатильного актива. Их упаковывают в капсулы ETF, превращают в фьючерсные контракты, вставляют в традиционные портфели активов 60/40.

Вывод, кажется, предрешен: Web3 финансы (особенно часть, связанная с торговлей на вторичном рынке) с большой вероятностью будут поглощены Web2 финансами, став одной из торговых категорий традиционных финансов.

Это может звучать неприятно для крипто-фундаменталистов, но это как раз и есть признак зрелости актива.

Будущая格局, возможно, будет такой: базовые блокчейн-технологии (Web3) по-прежнему будут отвечать за генерацию активов и установление прав собственности, например, майнинг BTC. Но в огромной финансовой надстройке, состоящей из торговли, клиринга, деривативов, Web2-гиганты, обладающие преимуществом низких затрат на compliance, по-прежнему будут занимать главные места за игровым столом.

Для инвесторов крайне важно это понимать. Ликвидность там, где Альфа. А сейчас ликвидность необратимо возвращается к тем, кто носит костюмы.

Twitter:https://twitter.com/BitpushNewsCN

Группа в TG比推:https://t.me/BitPushCommunity

Подписка в TG比推: https://t.me/bitpush