Пока рынок криптовалют готовится к принятию Закона CLARITY, новое правило в рамках Закона GENIUS вышло на первый план.

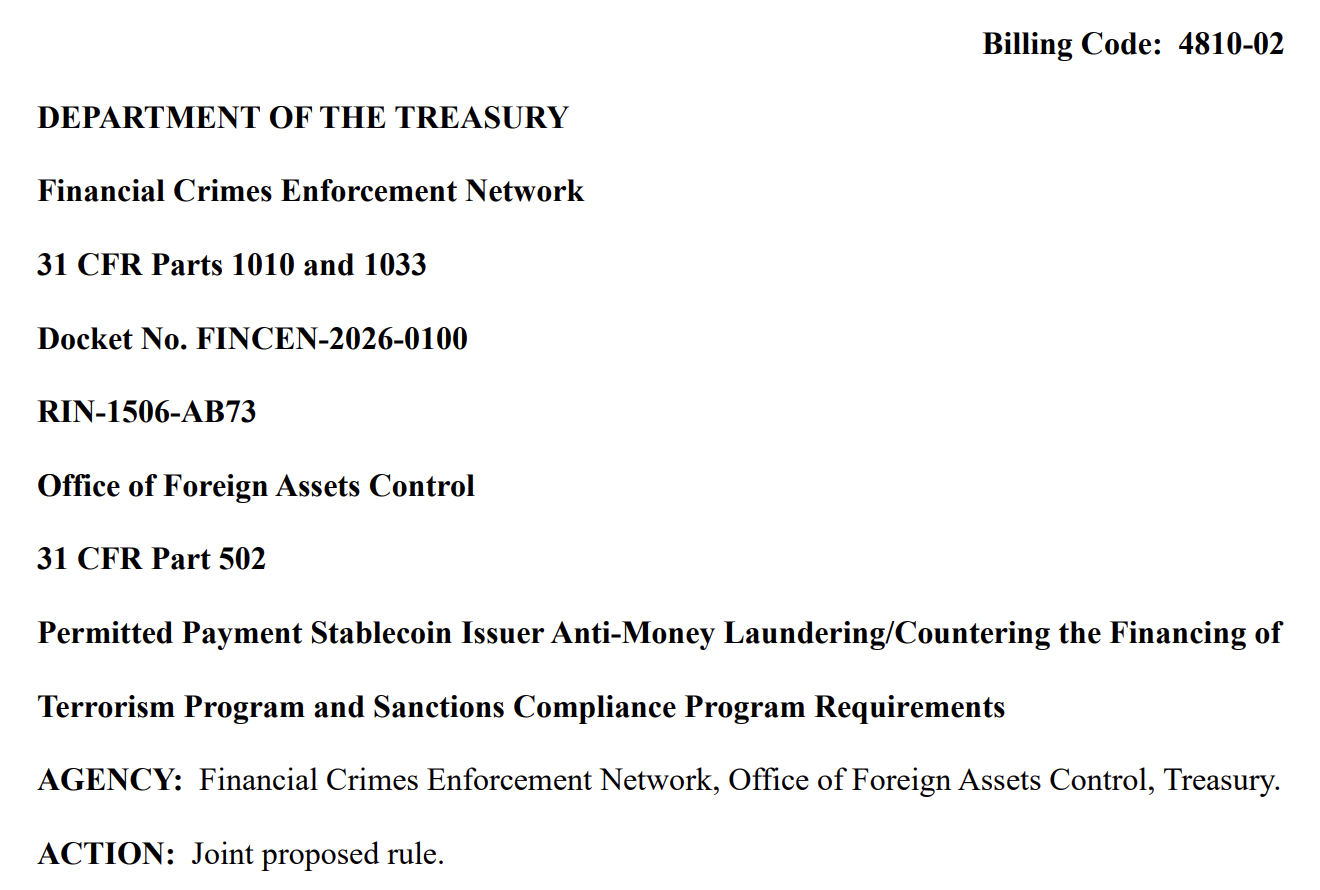

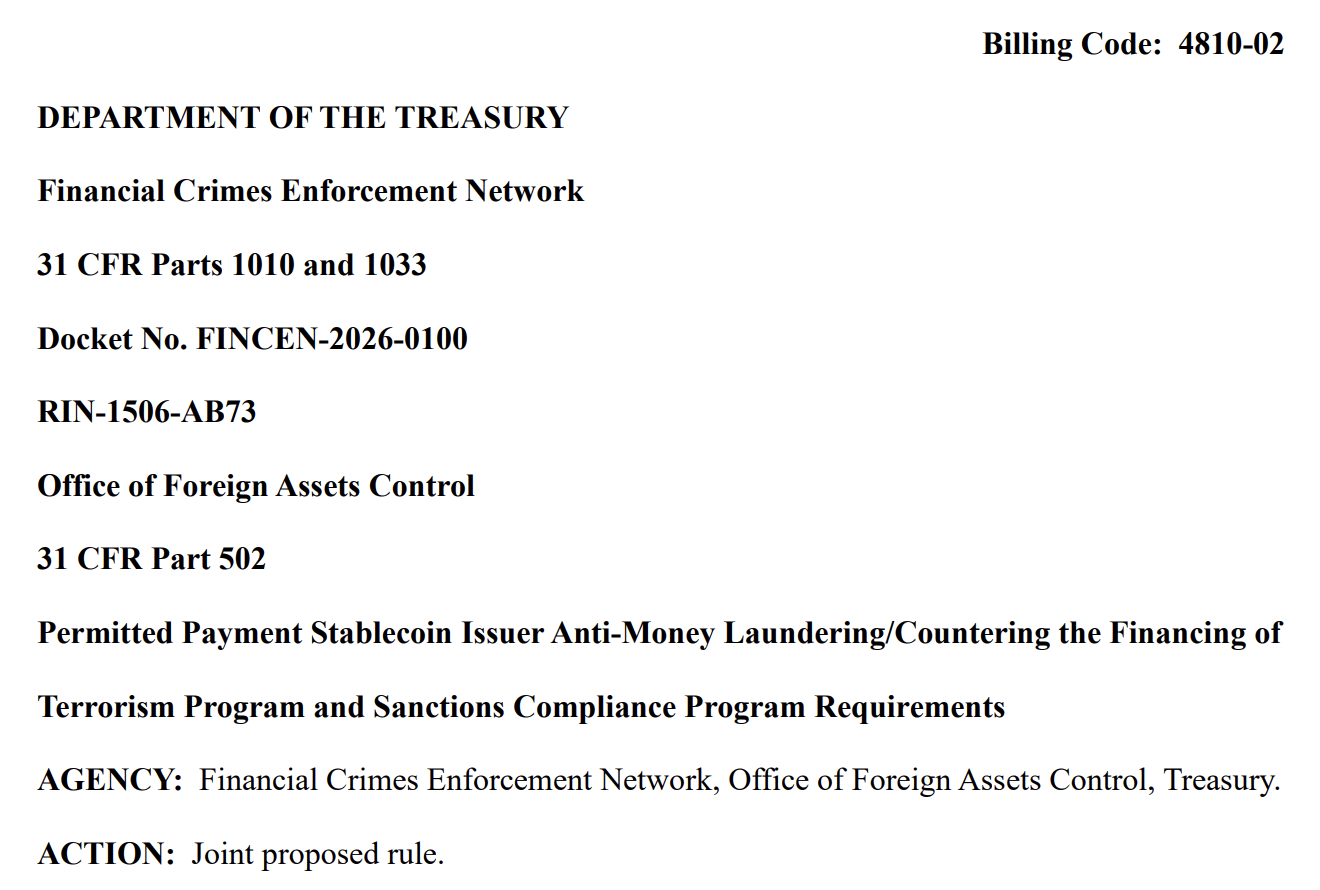

В совместном предложении Сеть по борьбе с финансовыми преступлениями (FinCEN) Министерства финансов США и Управление по контролю за иностранными активами (OFAC) представили правило, которое приравнивает эмитентов платёжных стейблкоинов к банкам.

Это было в контексте отмывания денег, финансирования терроризма и уклонения от санкций.

Для справки, это предлагаемое правило является частью Закона GENIUS, который был подписан президентом США Дональдом Трампом в июле 2025 года.

Что побудило Министерство финансов выдвинуть такое предложение?

Регуляторы считают, что эмитенты платёжных стейблкоинов могут развивать платёжную систему в США. Однако, учитывая масштабы и размер финансовой системы страны, незаконным деятелям легко «поставить под угрозу национальную безопасность США».

Поэтому для борьбы с такими незаконными финансовыми рисками правило гарантирует, что разрешённые эмитенты платёжных стейблкоинов (PPSIs) будут приравнены к финансовым учреждениям в целях Закона о банковской тайне (BSA).

Само собой разумеется, что это автоматически наложит обязательства по противодействию отмыванию денег (AML), которые ранее относились только к BSA.

Кроме того, предложение также разработано так, чтобы быть «соответствующим цели, помогать правоохранительным органам и минимизировать ненужное бремя». Всё это является частью более широкого плана по «модернизации требований BSA» при постоянных усилиях FinCEN.

Мнение министра финансов Скотта Бессента

Приветствуя такие изменения, внесённые администрацией президента США Дональда Трампа, министр финансов Скотт Бессент отметил:

Президент Трамп укрепляет американское лидерство в области цифровых финансовых технологий.

Он добавил:

Это предложение защитит финансовую систему США от угроз национальной безопасности, не препятствуя способности американских компаний продвигаться вперёд в экосистеме платёжных стейблкоинов.

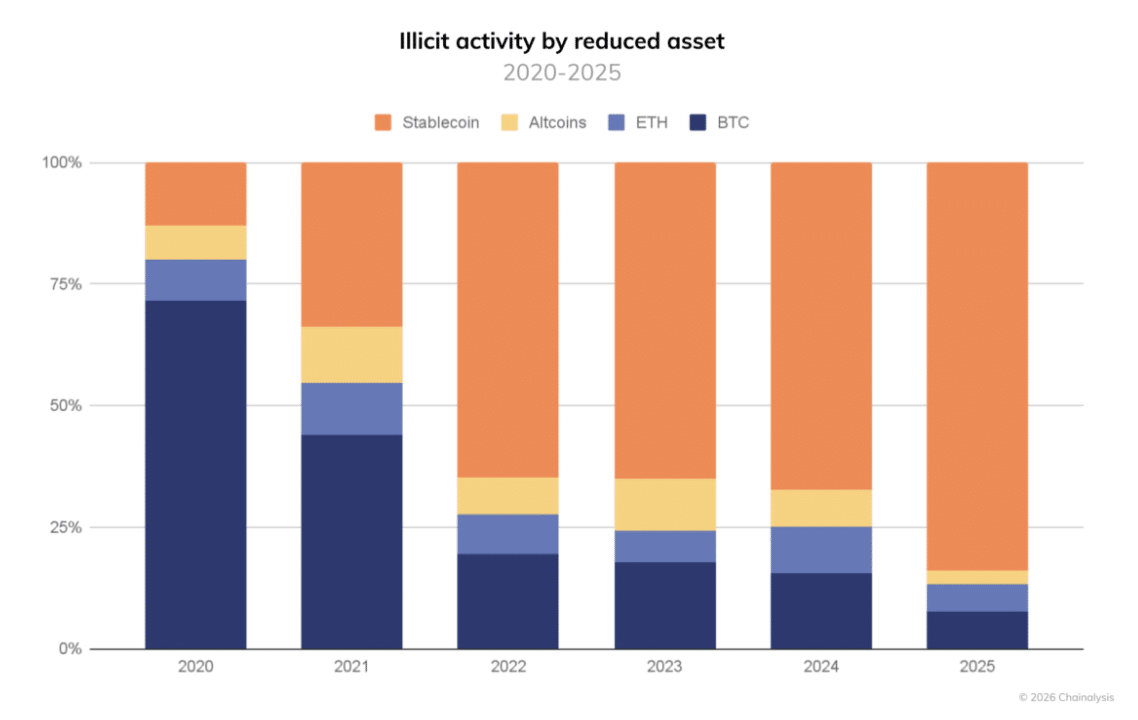

Незаконная деятельность, направленная на стейблкоины в 2025 году и ранее

Это происходит на фоне того, что стейблкоины уже много лет были центром внимания. Например, в июне 2025 года федеральные власти США изъяли 225,3 миллиона долларов в USDT от Tether, связанные с упомянутыми мошенническими схемами.

Кроме того, в июле 2025 года Министерство юстиции рассекретило информацию о цифровых активах на сумму примерно 2 миллиона долларов, связанных с палестинским бизнесом по обмену денег. В ноябре 2024 года также было изъято 5,5 миллиона долларов в стейблкоинах в рамках операции по борьбе с наркоторговлей.

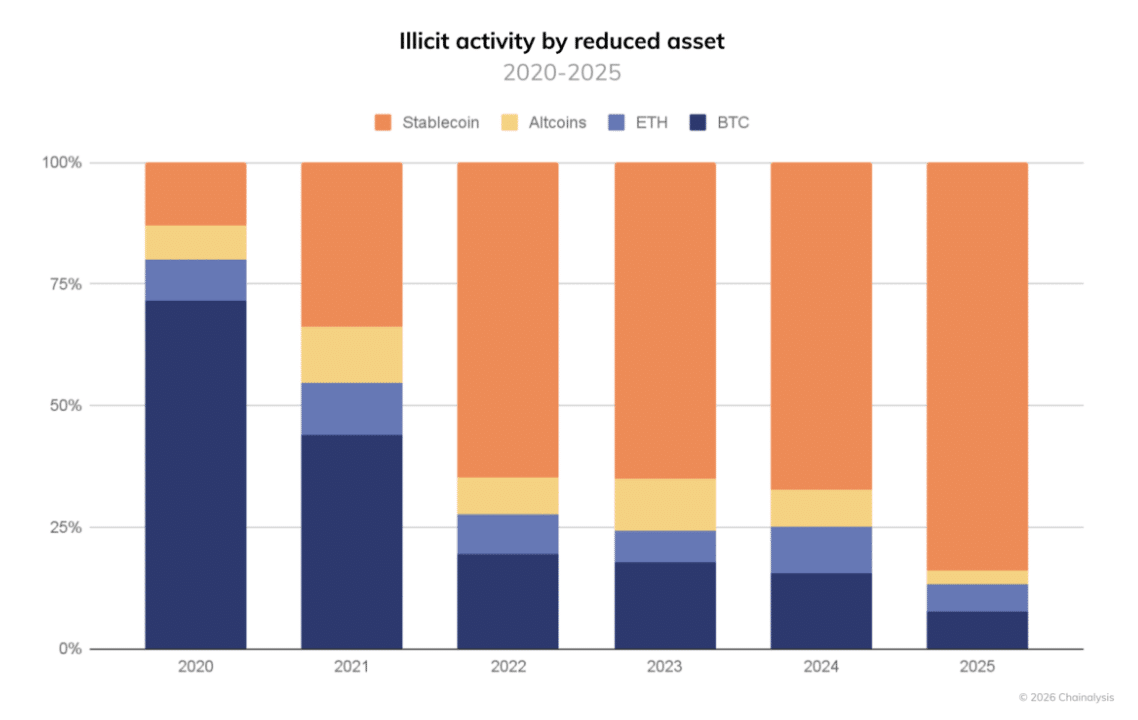

Недавний отчёт Chainalysis further подтвердил эти данные, подчеркнув, что в 2025 году на стейблкоины пришлось «84% всего объёма незаконных транзакций».

Итоговое резюме

- Совместные усилия по внесению предлагаемого правила для решения проблемы незаконной деятельности на рынке стейблкоинов подчёркивают важность Закона GENIUS, принятого в июле 2025 года.

- Учитывая миллионы, изъятые и конфискованные Министерством юстиции, это было необходимое правило, которое должно быть принято для лучшего развития криптоинноваций в США.