Sponsored Content

Crypto occupies a stable place in global finance. A 2024 report from payments firm Triple-A estimates that approximately 562 million people worldwide own digital currencies, accounting for around 6.8% of the global population.

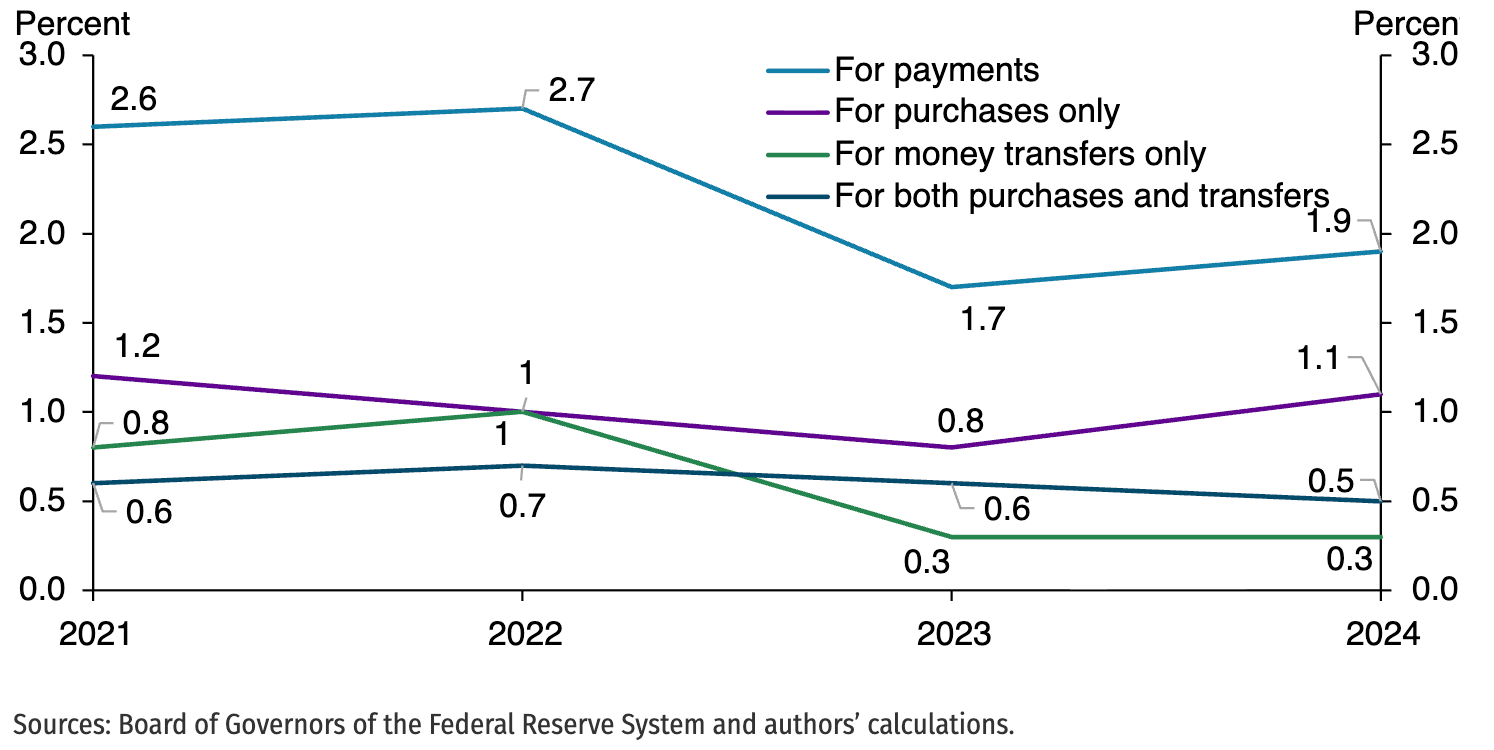

Yet payment behavior grows slowly. Research from the Federal Reserve Bank of Kansas City indicates that less than 2% of US consumers use cryptocurrency for payments, such as purchases or money transfers. Many people hold crypto as an investment or as a way to move value between services, and they still reach for bank cards at the supermarket.

Loyalty programs move in the opposite direction. A 2024 market intelligence report expects the global loyalty market to reach about $151 billion in 2024 and to grow toward roughly $215 billion by 2028.

When will the large base of crypto holders and the significant pool of loyalty spend begin to show up as simple weekday payments for groceries, rides and subscriptions?

Why wallet counts hide that answer

Projects usually point to easy success markers. Teams report the number of wallets, the number of cards they have issued and the amount of value in custody. These figures describe potential access, and they look strong on a slide, yet they fail to show whether people treat crypto as everyday money. A single enthusiast can create several wallets, keep balances on multiple exchanges and hold cards from more than one provider.

A tighter group of behavioral metrics gives a clearer view. Time-to-first-spend tracks how quickly new users complete a first successful payment after onboarding. Weekly active payers count people who make at least one payment in a week, and they highlight spending on groceries, transport or subscriptions. Fail and decline rate shows how many attempted payments fail at checkout, and it exposes gaps between onchain balances, offchain settlement and issuer risk rules.

Together, these three metrics form a product brief for builders. The ecosystem needs services that shorten time-to-first-spend, raise weekly active payer numbers and keep decline rates low at the places where people already shop.

What weekday spending looks like

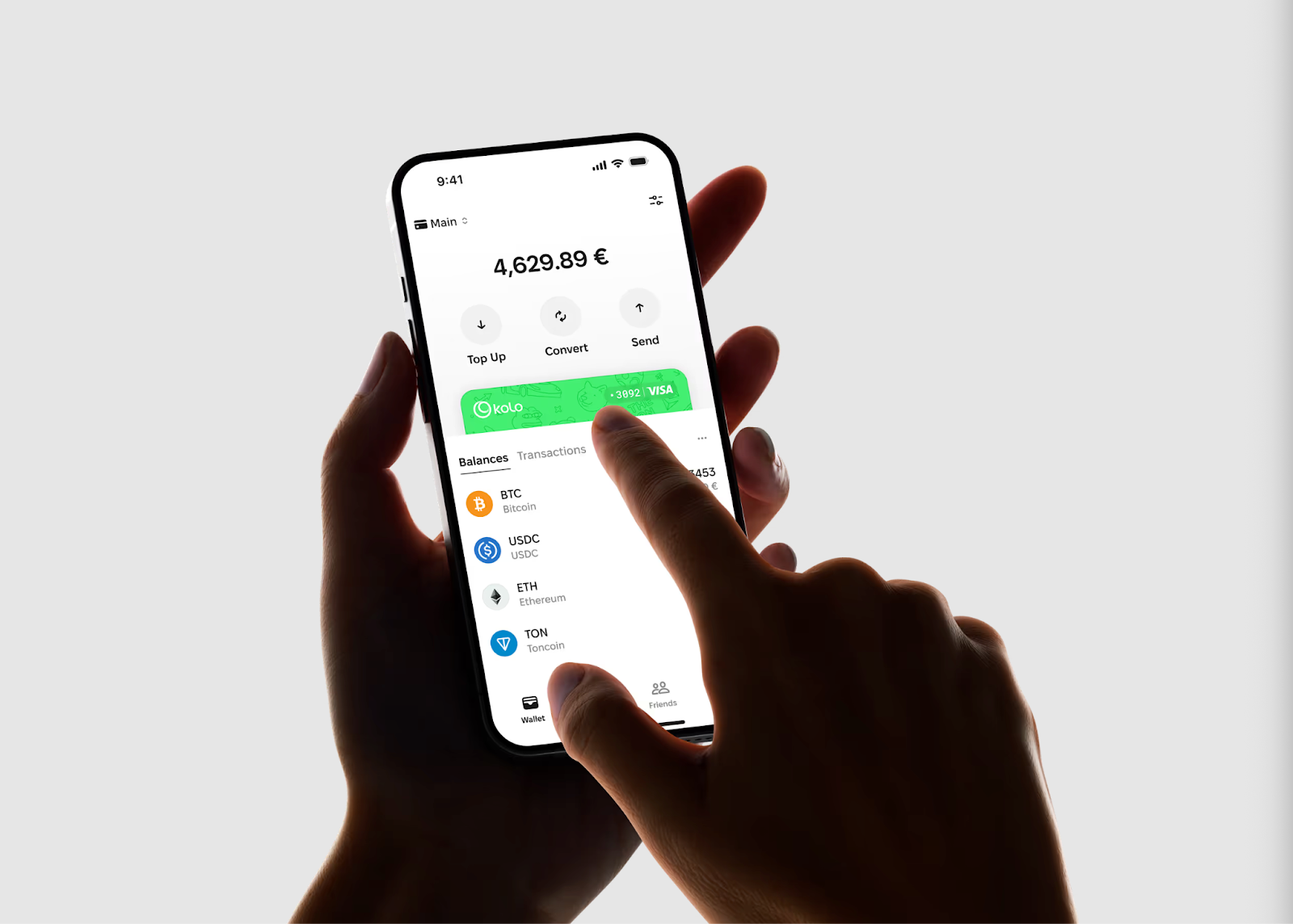

All-in-one crypto app Kolo offers a single solution to that brief. Kolo is a payment layer that bridges digital assets with everyday spending through a multi-network wallet and a Visa card that works with Apple Pay and Google Pay.

The newly launched Kolo Card has introduced a virtual Visa card that allows users to pay with cryptocurrency at millions of merchants and receive up to 5% cashback in Bitcoin (BTC). Users can pay for services such as Amazon, Instagram, Telegram, Netflix or Steam wherever Apple Pay or Google Pay is accepted.

Kolo has more than 100,000 wallets and around 50,000 monthly users. Most Kolo Card transactions fall into familiar spending categories such as restaurants, supermarkets, transport and digital subscriptions, with over 460,000 payments processed.

💳 Kolo Card is LIVE — the first Kolo wallet milestone unlocked!

— Kolo💚 (@KoloHub) May 22, 2025

Spend your crypto for:

🍝 Michelin-star dinners

✈️ Last-minute business-class

🛍 Limited-edition drops

More features are on the way to supercharge you live in crypto! pic.twitter.com/7nFAZPUcU3

The typical Kolo transaction looks like a coffee run, a grocery top-up or a streaming renewal. Users move funds into the wallet, and they see that they can handle routine expenses with crypto in the background. That pattern matches the idea of weekly active payers.

Turning wallets into weekday payments

Kolo aligns its experience with these behavioral metrics. The product aims to help new users move from signup to the first successful payment in one flow and to keep using the card every week for familiar purchases. During checkout, the cryptocurrency is converted to the local currency with a single tap on the phone or smart watch of the user.

Key features include:

A digital wallet across 11 networks

Kolo Card for Apple Pay and Google Pay at millions of merchants

One-minute Know Your Customer (KYC) that unlocks the card and payment features

More than 15 different payment methods, including PIX, MPESA and many others

Up to 5% Bitcoin cashback that grows a BTC balance on every purchase

This structure aims for a short time-to-first-spend. A user can download the app, complete KYC in about a minute, receive a Kolo Card and start using it in under two minutes. They no longer need to move funds through multiple intermediaries.

Compliance and infrastructure sit at the core of that journey. Kolo operates with MiCA alignment and Travel Rule compliance, and it includes Anti-Money Laundering (AML) protections. These foundations help the team lower fail and decline rates because the card, the wallet and the back-end settlement share the same rules and risk view.

“For everyday users, stablecoins’ rise as a universal way to store and move value simply removes friction. Digital money finally exists in a digital form that feels natural,” said Pavel Luchkovskyi, CEO of Kolo, adding:

“Kolo just connects to this new layer: if someone holds a digital dollar or any virtual asset, they should be able to use it for regular payments as easily as tapping a card. And once that becomes normal, that’s when real adoption shows up.”

Kolo also uses rewards to reinforce everyday behavior. The Bitcoin cashback model links offchain payments to onchain savings. Users pay for ordinary purchases at physical or digital merchants, and they grow a BTC stack in parallel.

Rethinking success in the age of crypto payments

The story of crypto adoption often highlights wallet milestones and price charts. Another picture emerges when teams track how many people tap a phone on a Tuesday morning and complete a smooth crypto-backed payment.

Time-to-first-spend, weekly active payers and fail or decline rates give that picture structure. These metrics encourage builders and investors to treat UX, on-ramp design and merchant coverage as central levers for growth.

Kolo shows how this mindset looks in a live product. The company brings together a hybrid wallet, a globally accepted card, a variety of payment rails and Bitcoin rewards in one experience that fits existing payment habits. Cryptocurrency runs behind the scenes while users focus on their everyday lives.