Автор: Prathik Desai

Компиляция и редактирование: BitpushNews

Более года назад для многих компаний, стремящихся повысить стоимость своих акций, стать казначейством цифровых активов казалось легким решением.

Некоторые акционеры Microsoft собрались, чтобы потребовать от совета директоров оценить преимущества включения биткоина в их баланс. Они даже упомянули Strategy (ранее MicroStrategy), крупнейший публичный биткоиновый DAT.

В то время существовал финансовый маховик, который привлекал всех следовать.

Покупайте много BTC/ETH/SOL. Наблюдайте, как цена акций превышает стоимость этих активов. Выпускайте больше акций с премией. Используйте эти деньги, чтобы купить еще больше криптовалюты. Повторяйте цикл. Этот финансовый маховик, поддерживающий публично торгуемые акции, казался почти идеальным, достаточно соблазнительным для инвесторов. Они платили более двух долларов, чтобы получить косвенное воздействие на биткоин стоимостью всего в один доллар. То были безумные времена.

Но время проверяет даже лучшие стратегии и маховики.

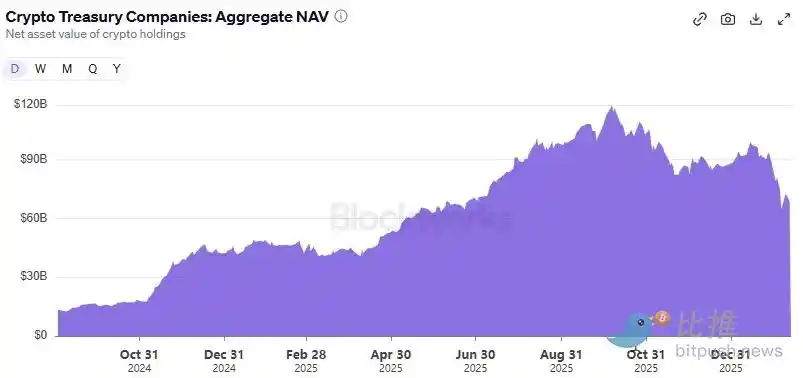

Сегодня, когда общая рыночная капитализация крипторынка за последние четыре месяца сократилась более чем на 45%, соотношение рыночной капитализации к чистой стоимости активов (mNAV) для большинства этих компаний-оболочек упало ниже 1. Это указывает на то, что рынок оценивает эти DAT компании ниже стоимости их крипто-казначейств. Это меняет принцип работы финансового маховика.

Потому что DAT — это не просто оболочка для активов. В большинстве случаев это компания с операционными расходами, затратами на финансирование, юридическими и операционными издержками. В эпоху премии к mNAV DAT финансировали свои покупки криптовалюты и операционные затраты, продавая больше акций или привлекая больше долга. А в эпоху дисконта к mNAV этот маховик рушивается.

В сегодняшнем анализе я покажу вам, что означает устойчивый дисконт к mNAV для DAT, и смогут ли они выжить в крипто-медвежьем рынке.

В период с 2024 по 2025 год более 30 компаний бросились превращаться в DAT. Они создали казначейства вокруг биткоина, ETH, SOL и других blue-chip монет и даже мем-коинов.

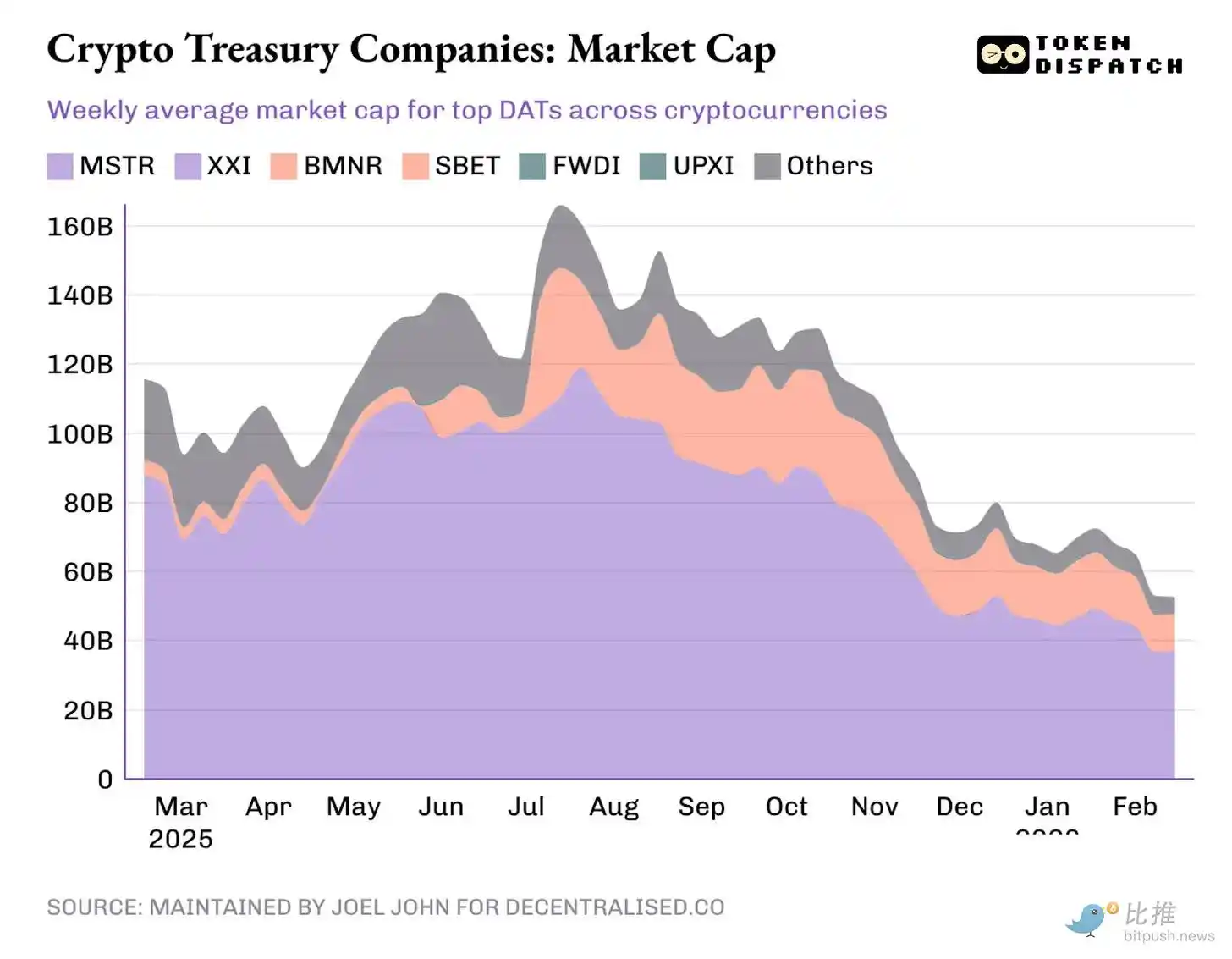

На пике, 7 октября 2025 года, криптовалюты, принадлежащие DAT, стоили 118 миллиардов долларов, а общая рыночная капитализация этих компаний превышала 160 миллиардов долларов. Сегодня криптовалюты, принадлежащие DAT, стоят 68 миллиардов долларов, а их общая рыночная капитализация с дисконтом составляет чуть более 50 миллиардов долларов.

Вся их судьба зависела от одного: их способности упаковывать активы и плести истории, чтобы стоимость упаковки превышала стоимость активов. Эта разница и становилась премией.

Сама премия стала продуктом. Если акции торгуются в 1,5 раза выше mNAV, DAT может продать акций на 1 доллар, купить экспозицию к криптоактивам на 1,5 доллара и описать эту сделку как «создающую добавленную стоимость». Инвесторы были готовы платить премию, веря, что DAT сможет и дальше продавать акции с премией и использовать выручку для накопления большего количества криптовалюты, тем самым увеличивая стоимость криптоактивов на акцию с течением времени.

Проблема в том, что премия не может существовать вечно. Как только рынок перестает платить дополнительные деньги за эту упаковку, маховик «продать акции, купить больше криптовалюты» дает сбой.

Когда акции больше не торгуются в 1,5 раза выше стоимости их активов, каждый выпуск новой акции позволяет купить меньше криптовалюты. Премия перестает быть попутным ветром и превращается в дисконт.

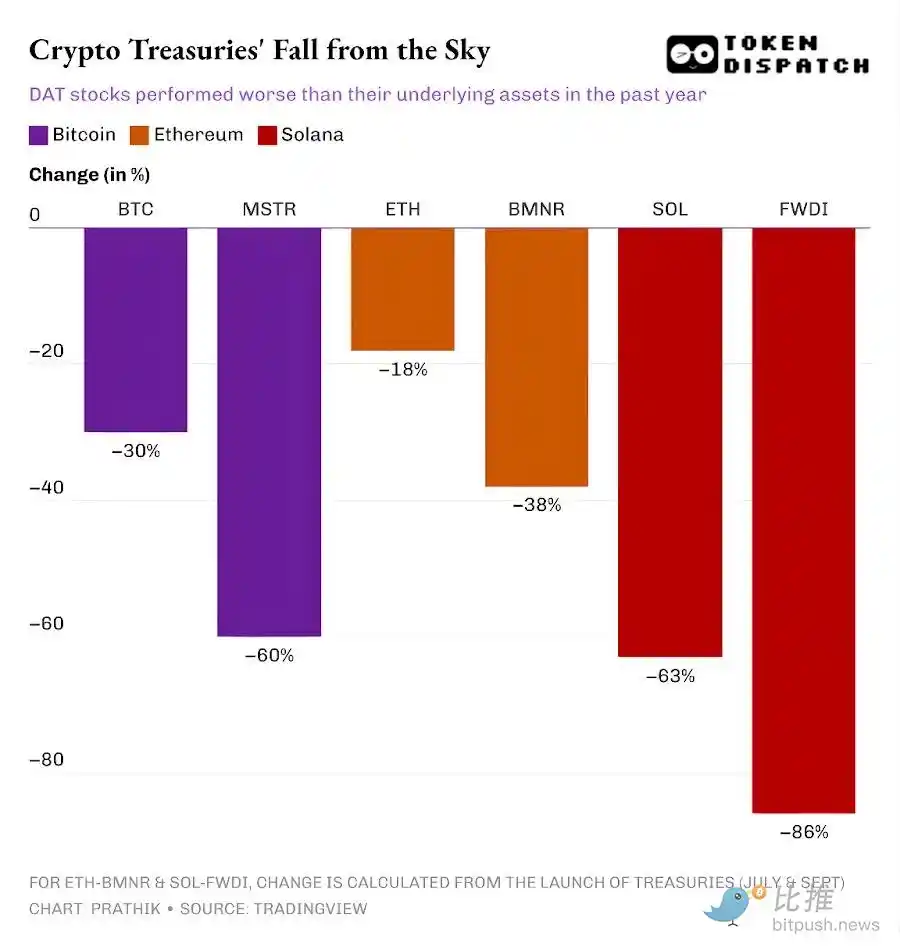

За последний год цены акций ведущих BTC, ETH и DAT SOL упали больше, чем сами криптовалюты.

Как только премия акций к базовым активам исчезает, инвесторы естественным образом задаются вопросом: почему бы им не купить криптовалюту напрямую в другом месте, например, на децентрализованных или централизованных биржах, или через биржевые фонды, по более низкой цене?

Мэтт Левин из Bloomberg задал важный вопрос: если DAT торгуются ниже чистой стоимости активов, не говоря уже о премии, почему инвесторы не заставляют компанию ликвидировать свое крипто-казначейство или выкупить акции?

Многие DAT, включая лидера отрасли Strategy, пытались убедить инвесторов, что они будут держать криптовалюту в течение медвежьего рыночного цикла, дожидаясь возвращения эпохи премий. Но я вижу более серьезную проблему. Если DAT не могут привлечь дополнительные средства в обозримом долгосрочном периоде, откуда они возьмут деньги на поддержание операционной деятельности? У этих DAT есть счета и зарплаты к выплате.

Strategy является исключением по двум причинам.

-

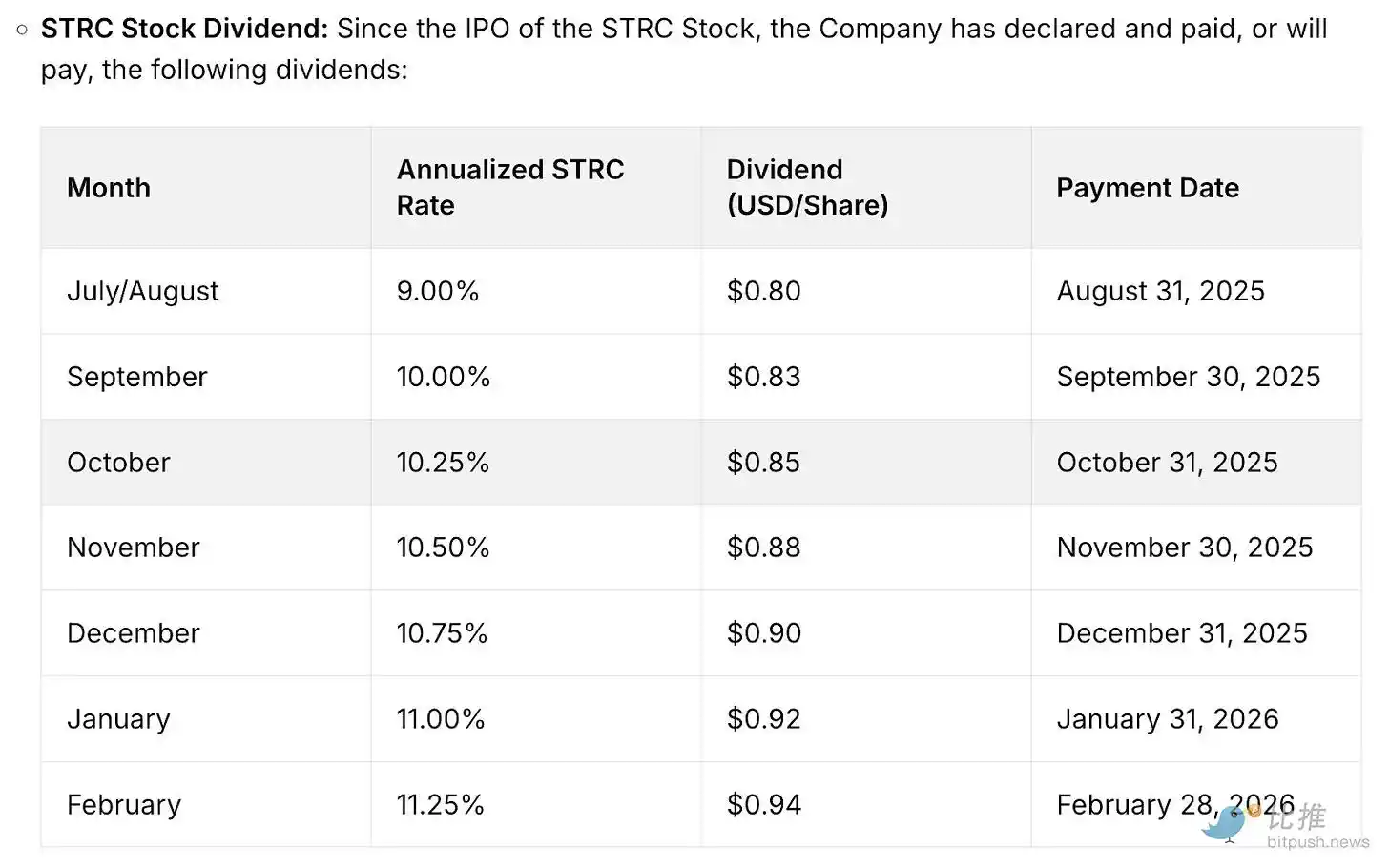

Согласно отчетам, у нее есть резервы в размере 2,25 миллиарда долларов, которых достаточно для покрытия ее дивидендных и процентных обязательств примерно на 2,5 года. Это важно, потому что Strategy больше не полагается исключительно на конвертируемые облигации с нулевым купоном для привлечения средств. Она также выпустила привилегированные инструменты, по которым необходимо выплачивать существенные дивиденды.

-

У нее также есть операционный бизнес, каким бы маленьким он ни был, который все еще приносит регулярный доход. В четвертом квартале 2025 года Strategy сообщила о совокупном доходе в 123 миллиона долларов и валовой прибыли в 81 миллион долларов. Хотя чистая прибыль Strategy может значительно колебаться из-за переоценки по рыночной стоимости криптоактивов каждый квартал, ее отдел бизнес-аналитики является единственным tangible источником денежных потоков.

Но это все еще не делает стратегию Strategy неуязвимой. Рынок по-прежнему может наказывать ее акции — как это происходило в прошлом году — и подрывать способность Strategy продолжать привлекать средства с низкой стоимостью.

В то время как Strategy, возможно, переживет крипто-медвежий рынок, новые DAT, у которых нет достаточных резервов или операционного бизнеса для покрытия своих неизбежных расходов, ощутят давление.

Это различие еще более заметно среди ETH DAT.

Крупнейший DAT на основе Ethereum — BitMine Immersion, имеет маргинальный операционный бизнес, поддерживающий его ETH-казначейство. В квартале, закончившемся 30 ноября 2025 года, BMNR сообщила о совокупном доходе в 2,293 миллиона долларов, включая доходы от консалтинга, аренды и стейкинга.

Ее баланс показывает, что компания держит цифровые активы на сумму 10,56 миллиарда долларов и эквиваленты денежных средств на 887,7 миллиона долларов. Операционная деятельность BMNR привела к чистому отрицательному денежному потоку в 228 миллионов долларов. Все ее денежные потребности удовлетворялись за счет выпуска новых акций.

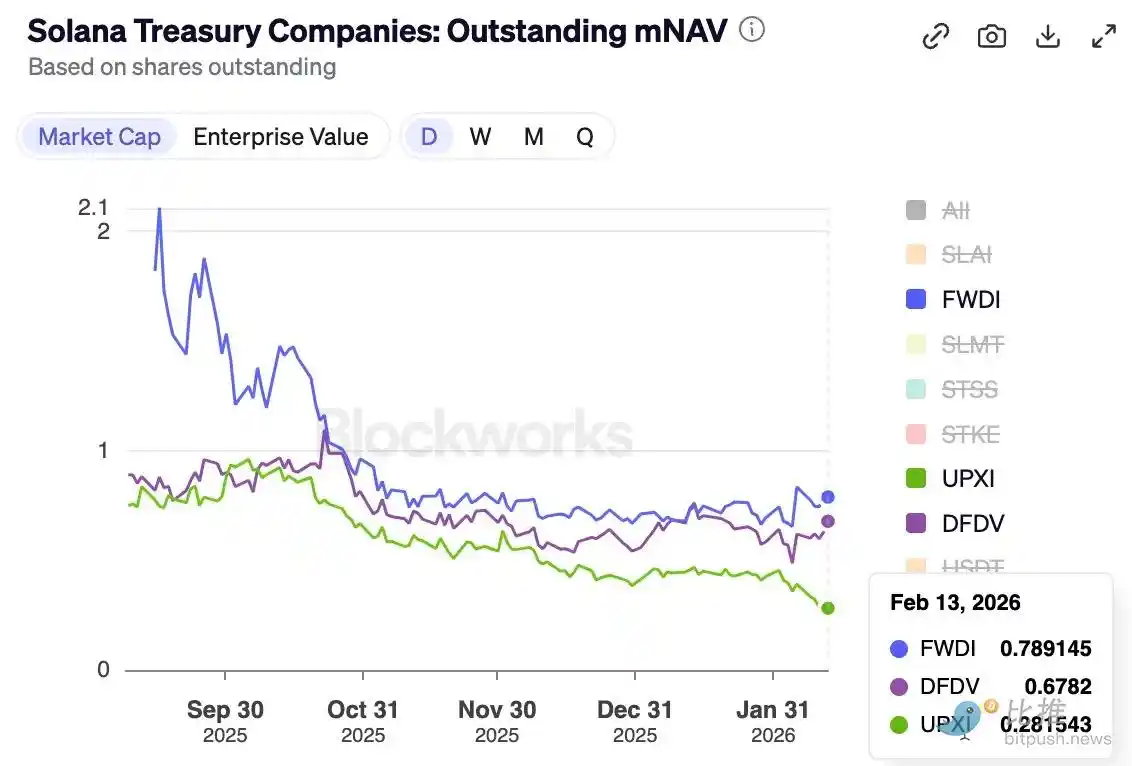

В прошлом году, поскольку акции BMNR большую часть года торговались с премией к mNAV, привлечь средства было относительно легко. Но за последние шесть месяцев ее mNAV снизился с 1,5 примерно до 1.

Так что же происходит, когда акции больше не торгуются с премией? Выпуск большего количества акций со скидкой может снизить цену ETH на акцию, сделав их менее привлекательными для инвесторов, чем прямая покупка ETH на рынке.

Это объясняет, почему BitMine в прошлом месяце заявила, что инвестирует 200 миллионов долларов в акции Beast Industries, частной компании, принадлежащей YouTube-блогеру Джимми «MrBeast» Дональдсону. Компания заявила, что будет «изучать способы сотрудничества в рамках инициатив DeFi».

ETH и SOL DAT могут также утверждать, что доход от стейкинга — то, чем не могут похвастаться BTC DAT — может помочь им поддерживать операционную деятельность во время обвала рынка. Но это все равно не решает проблемы выполнения денежных обязательств компании.

Даже со стейкинг-вознаграждениями (начисляемыми в виде криптовалют, таких как ETH или SOL), пока эти вознаграждения не конвертированы в фиатные деньги, DAT не может использовать их для выплаты зарплат, аудиторских сборов, листинговых затрат и процентов. Компания должна либо иметь достаточный фиатный доход, либо продавать или рестейкать активы своего казначейства для удовлетворения денежных потребностей.

Это ярко проявляется в крупнейшем держателе SOL DAT — Forward Industries.

FWDI в четвертом квартале 2025 года сообщила о чистом убытке в 586 миллионов долларов, несмотря на получение 17,381 миллиона долларов дохода от стейкинга и связанных с ним activities.

Менеджмент четко дал понять, что ее «существующие денежные остатки и оборотный капитал достаточны для удовлетворения наших потребностей в ликвидности по крайней мере до февраля 2027 года».

FWDI также раскрыла агрессивную стратегию привлечения капитала, включая выпуск акций по рыночной цене, выкуп и эксперимент с токенизацией. Однако, если премия к mNAV не будет существовать в течение длительного времени, все эти попытки могут не увенчаться успехом в управлении ценой их упаковки.

Путь вперед

В основе бума DAT прошлого года лежала скорость накопления активов и способность привлекать средства за счет выпуска акций с премией. Пока упаковка торговалась с премией, DAT могли продолжать превращать дорогой акционерный капитал в больше криптоактивов на акцию и называть это «бетой». Инвесторы также делали вид, что единственный риск — это цена самого актива.

Но премия не вечна. Криптовалютные циклы могут превратить ее в дисконт. Я писал об этом, когда впервые наблюдал падение премии вскоре после события ликвидации 10/10 прошлого года.

Однако этот медвежий рынок заставит DAT оценить, должны ли они продолжать существовать,一旦 их упаковка больше не торгуется с премией.

Одним из способов решения этой дилеммы является то, что компании повышают свою операционную эффективность, дополняя свою DAT-стратегию бизнесом, генерирующим положительный денежный поток, или избыточными резервами. Потому что, когда история DAT больше не может привлекать инвесторов в условиях медвежьего рынка, история обычной компании будет определять их выживание.

Если вы читали статью «Strategy & Marathon: Вера и сила», вы вспомните, почему Strategy до сих пор выстояла в нескольких криптоциклах. Однако новая волна компаний, включая BitMine, Forward Industries, SharpLink и Upexi, не могут полагаться на ту же силу.

Их нынешние попытки с доходами от стейкинга и слабым операционным бизнесом могут рухнуть под рыночным давлением, если они не рассмотрят другие варианты покрытия обязательств в реальном мире.

Мы наблюдали это на примере ETHZilla, компании-казначейства Ethereum, которая в прошлом месяце продала активов ETH примерно на 115 миллионов долларов и купила два реактивных двигателя. Затем этот DAT сдал двигатели в аренду крупной авиакомпании и нанял Aero Engine Solutions для управления за ежемесячную плату.

В перспективе будут оценивать не только стратегии накопления цифровых активов, но и условия, при которых они могут выжить. В текущем цикле DAT только те компании, которые смогут управлять разводнением, долгом, фиксированными обязательствами и торговой ликвидностью, переживут рыночный спад.