В инвестиционном сообществе широко распространено мнение, что избыточная доходность (Alpha), то есть способность обгонять рынок, является целью, к которой должны стремиться инвесторы. Это совершенно логично. При прочих равных условиях Alpha всегда лучше иметь больше.

Однако наличие Alpha не всегда означает лучшую инвестиционную отдачу. Потому что ваша Alpha всегда зависит от поведения рынка. Если рынок показывает плохие результаты, Alpha не обязательно принесет вам прибыль.

Приведем пример: представьте двух инвесторов, Алекса и Пэт. Алекс очень хорош в инвестициях и каждый год обгоняет рынок на 5%. А Пэт — плохой инвестор, каждый год отставая от рынка на 5%. Если Алекс и Пэт инвестируют в один и тот же период, годовая доходность Алекса всегда будет на 10% выше, чем у Пэт.

Но что, если Пэт и Алекс начали инвестировать в разное время? Возможна ли ситуация, когда, несмотря на большее мастерство Алекса, доходность Пэт окажется выше?

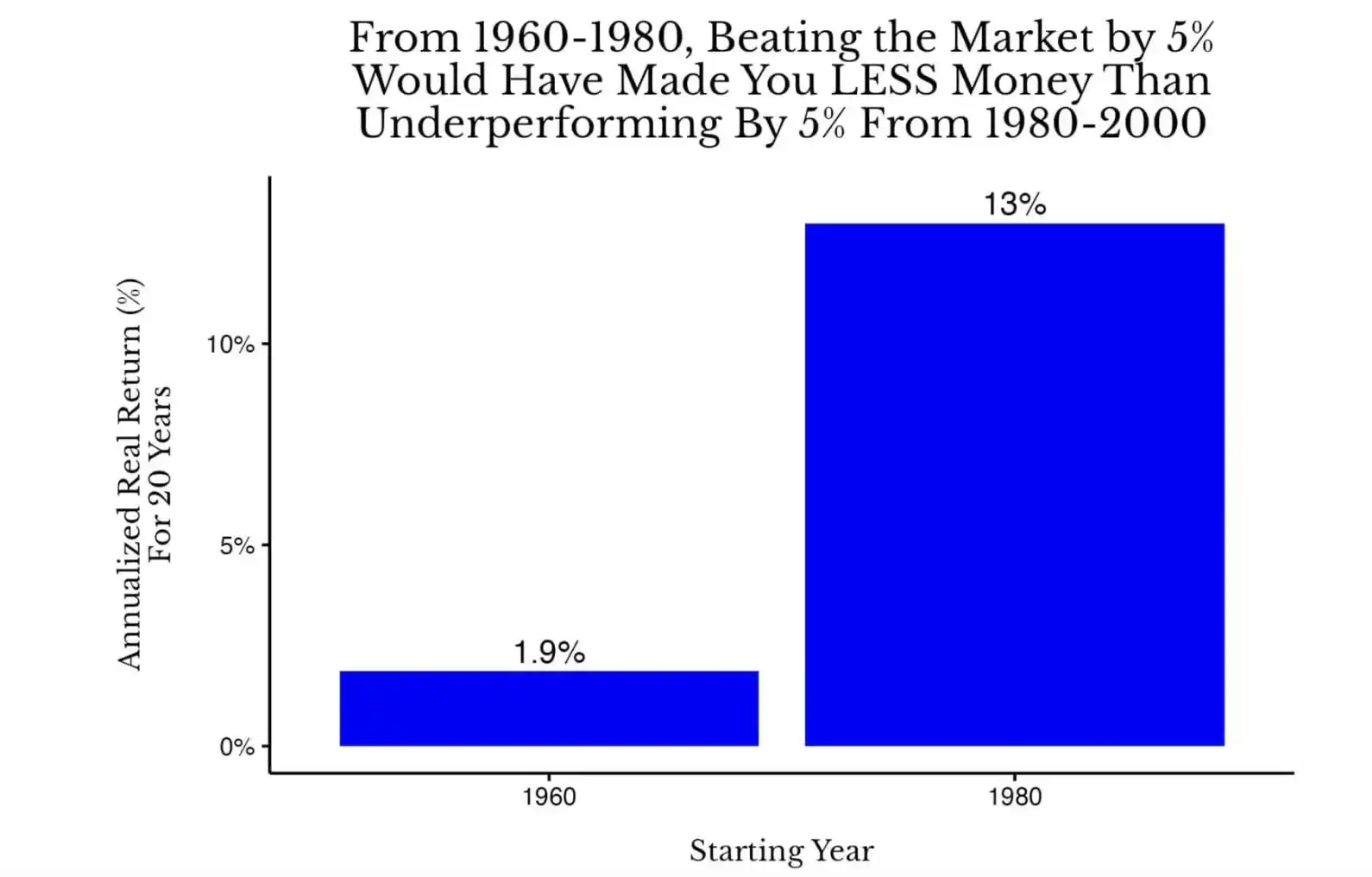

Ответ — да. Фактически, если Алекс инвестировал в американские акции с 1960 по 1980 год, а Пэт — с 1980 по 2000 год, то через 20 лет инвестиционный доход Пэт превысит доход Алекса. На следующем графике это показано:

В этом случае годовая доходность Алекса с 1960 по 1980 год составила 6,9% (1,9% + 5%), а годовая доходность Пэт с 1980 по 2000 год — 8% (13% – 5%). Несмотря на то, что инвестиционные способности Пэт хуже, чем у Алекса, с точки зрения общей доходности с поправкой на инфляцию Пэт показал себя лучше.

Но что, если соперником Алекса будет настоящий инвестор? До сих пор мы предполагали, что конкурент Алекса — это Пэт, человек, который каждый год отстает от рынка на 5%. Но в реальности настоящим конкурентом Алекса должен быть индексный инвестор, чья годовая доходность соответствует рыночной.

В этом сценарии, даже если Алекс с 1960 по 1980 год каждый год обгонял рынок на 10%, он все равно отстал бы от индексного инвестора периода 1980-2000 годов.

Хотя это крайний пример (то есть выброс), вы удивитесь, насколько часто наличие Alpha приводит к отставанию от исторических показателей. Как показано на графике ниже:

Как видите, когда у вас нет Alpha (0%), вероятность обогнать рынок по сути эквивалентна подбрасыванию монетки (около 50%). Однако с ростом дохода от Alpha эффект сложного процента, конечно, снижает частоту отставания от индекса, но рост не так велик, как можно было бы предположить. Например, даже при ежегодном alpha-доходе в 3% в течение 20-летнего периода, в другие периоды истории американского рынка все еще существует вероятность около 25% показать результат хуже, чем у индексного фонда.

Конечно, некоторые могут argue, что важна именно относительная доходность, но я лично с этим не согласен. Спросите себя: вы предпочли бы получить среднюю рыночную доходность в нормальные времена или «немного меньше потерять» во время Великой депрессии (то есть получить положительный Alpha)? Я, конечно, выбрал бы индексную доходность.

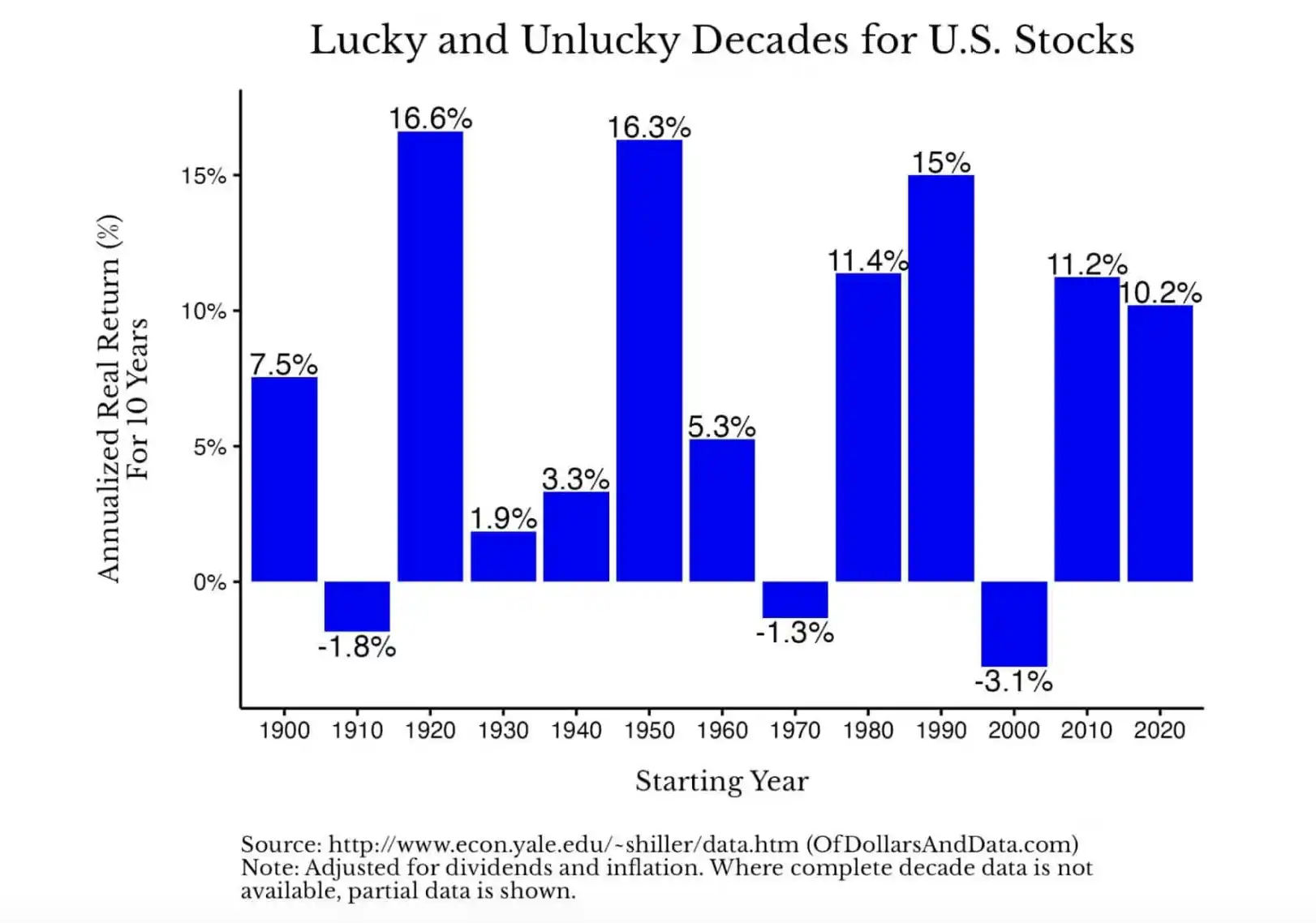

В конце концов, в большинстве случаев индексная доходность приносит довольно неплохие результаты. Как показано на следующем рисунке, реальная годовая доходность американских акций колеблется по десятилетиям, но в основном является положительной (примечание: данные за 2020-е годы показывают доходность только до 2025 года):

Все это показывает, что хотя инвестиционное мастерство важно, часто ключевым является поведение рынка. Другими словами, молитесь на Beta, а не на Alpha.

На техническом уровне, β (Beta) измеряет, насколько доходность актива колеблется относительно рынка. Если у акции Beta равна 2, то при росте рынка на 1% ожидается, что эта акция вырастет на 2% (и наоборот). Но для простоты рыночную доходность обычно называют Beta (то есть с бета-коэффициентом, равным 1).

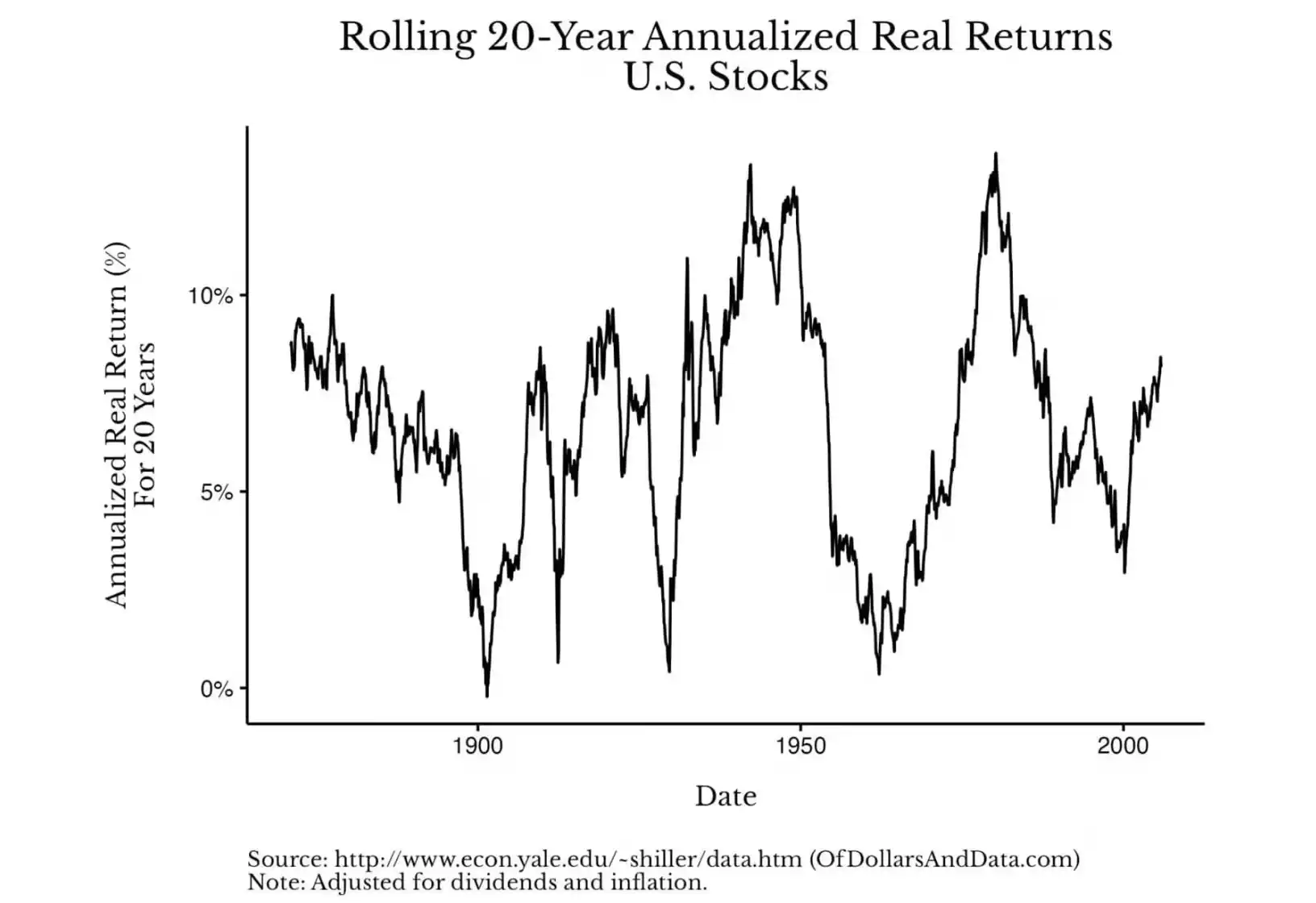

Хорошая новость заключается в том, что если рынок в один период не предоставляет достаточного «Beta», он может наверстать упущенное в следующем цикле. Вы можете увидеть это на следующем графике, который показывает 20-летнюю скользящую годовую реальную доходность американских акций с 1871 по 2025 год:

Этот график наглядно показывает, как доходность сильно восстанавливается после спадов. Взяв в пример историю американского рынка, если бы вы инвестировали в американские акции в 1900 году, ваша годовая реальная доходность за следующие 20 лет была бы близка к 0%. Но если бы вы инвестировали в 1910 году, ваша годовая реальная доходность за следующие 20 лет составила бы около 7%. Аналогично, инвестиции в конце 1929 года дали бы годовую доходность около 1%, а инвестиции летом 1932 года — целых 10%.

Эта огромная разница в доходности снова подтверждает важность общей рыночной эффективности (Beta) по сравнению с инвестиционным мастерством (Alpha). Вы можете спросить: «Я не могу контролировать, как поведет себя рынок, так какое это имеет значение?»

Это важно, потому что это освобождение. Это освобождает вас от давления «обязательности победы над рынком» и позволяет сосредоточиться на том, что действительно可控. Вместо того чтобы тревожиться из-за того, что рынок вам не подчиняется, рассматривайте это как одну вещь меньше, о которой нужно беспокоиться. Считайте это переменной, которую вам не нужно оптимизировать, потому что вы просто не можете ее оптимизировать.

Так что же вам следует оптимизировать вместо этого? Оптимизируйте свою карьеру, норму сбережений, здоровье, семью и так далее. В долгом измерении жизни ценность, создаваемая в этих областях, гораздо значимее, чем мучительные поиски лишних процентов超额收益 в инвестиционном портфеле.

Посчитайте просто: 5%-ное повышение зарплаты или один стратегический карьерный переход могут увеличить ваш пожизненный доход на шестизначную сумму или даже больше. Точно так же поддержание хорошей физической формы — это эффективное управление рисками, которое может значительно хеджировать будущие расходы на медицинские услуги. А время, проведенное с семьей, подает правильный пример для их будущего. Польза от этих решений намного превышает ту доходность, на которую могут рассчитывать большинство инвесторов, пытаясь обогнать рынок.

В 2026 году сосредоточьте свою энергию на правильных вещах, гонитесь за Beta, а не за Alpha.