Автор: KarenZ, Foresight News

В Кремниевой долине имя Naval Ravikant само по себе является гарантией.

Он соучредитель AngelList и один из самых влиятельных инвесторов ранних стадий за последнее десятилетие, вложившийся в такие компании, как Uber, Twitter, Notion и другие. Теперь, венчурном фонде USVC Venture Capital Access Fund (USVC), Naval играет номинальную роль. Согласно дополнению к документам фонда от апреля 2026 года, он занимает пост председателя инвестиционного комитета, отвечая за формирование портфеля и надзор за стратегией.

Это важно, потому что USVC продает не просто концепцию «фонда с низким порогом входа». Он действительно пытается упаковать и предложить возможность, которая раньше была доступна лишь немногим: более ранний доступ к растущим частным компаниям до их выхода на биржу.

Если смотреть поверхностно, USVC легче всего понять как «венчурный фонд для розничных инвесторов». Но если совместить сайт, проспект эмиссии и страницу портфеля, основная история, которую хочет рассказать AngelList, становится более четкой и острой: самые перспективные компании сегодня выходят на биржу все позже; IPO все больше напоминает точку выхода, а не точку входа; обычные инвесторы остаются за бортом не только рисков, но и самого «сочного» периода роста.

Значение USVC заключается в том, что он пытается приоткрыть эту дверь.

Суть USVC не в продаже фонда, а в продаже доступа до IPO

На главной странице сайта USVC вопрос ставится прямо: следующий раунд роста происходит на частном рынке. Сайт также приводит показательные данные: в 1980 году медианный возраст американских компаний на момент IPO составлял 6 лет, а сейчас это 13 лет. Лишние 7 лет означают, что значительное создание стоимости происходит вне публичного рынка.

Это ключевая логика продукта USVC. В проспекте эмиссии указано, что USVC в основном инвестирует в венчурные фонды, SPV (специальные целевые vehicle) и частные растущие компании (private growth-oriented companies). Здесь самое легкоупускаемое, но критически важное слово — это частные растущие компании. Определение в документе также прямое: частные компании, которые, по мнению инвестиционного консультанта, «обладают значительным потенциалом роста на момент инвестирования».

Другими словами, изюминка USVC не в абстрактном «распределении в венчурный капитал», а в том, чтобы предоставить обычным инвесторам доступ к самым привлекательным активам на первичном рынке. Он продает канал доступа к непубличным растущим компаниям.

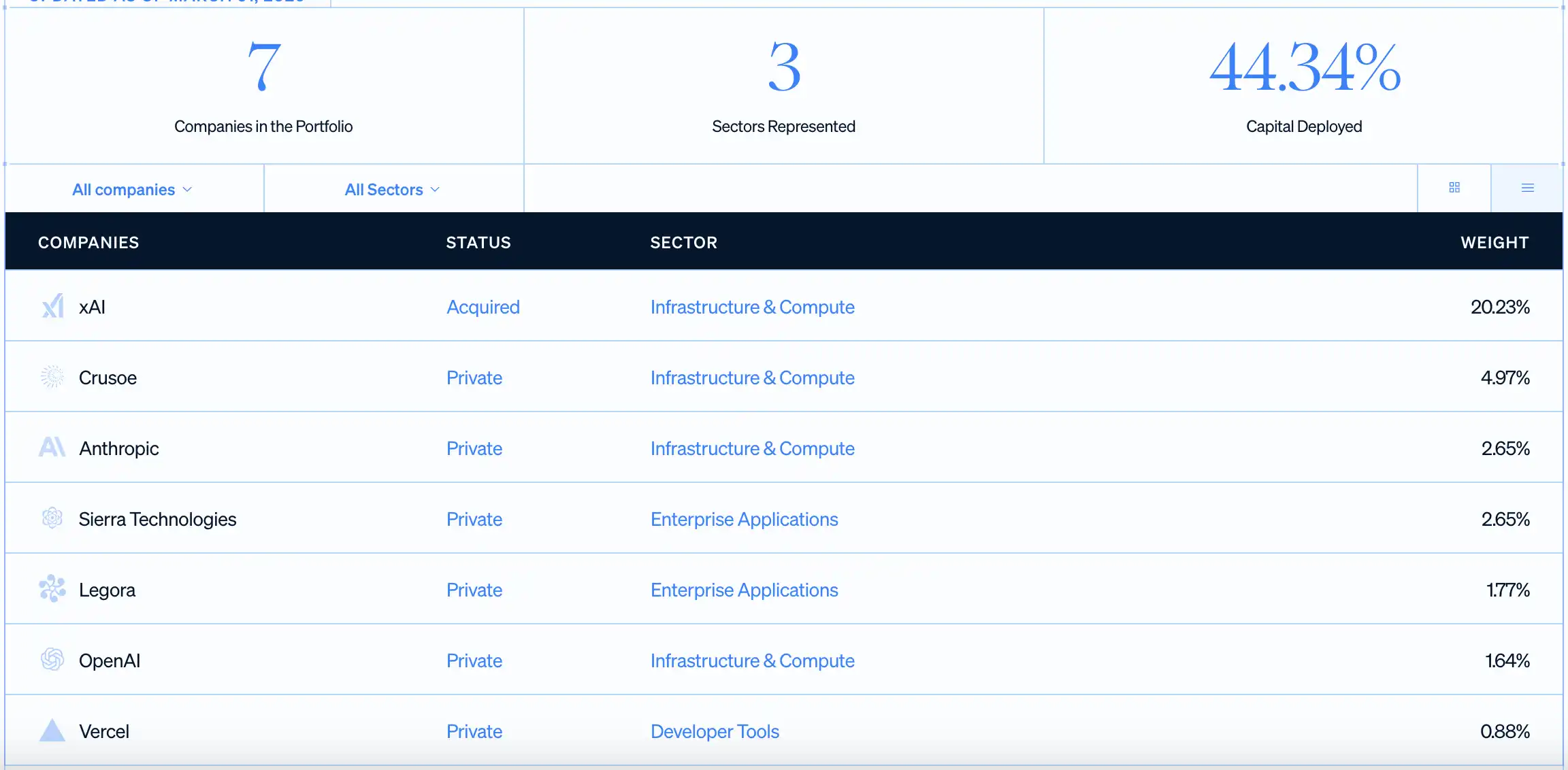

Именно поэтому он постоянно упоминает такие имена, как OpenAI, Anthropic, xAI, Vercel. На странице портфеля указано, что по состоянию на 31 марта 2026 года USVC развернул 44,34% капитала, в портфеле уже 7 компаний, крупнейший актив — xAI, за ним следуют Crusoe, Anthropic, Sierra, Legora, OpenAI и Vercel. Независимо от итоговых результатов этих вложений, сообщение, которое AngelList хочет донести до инвесторов, достаточно ясно: раньше вы могли только читать об этих компаниях в новостях, теперь через этот фонд вы можете получить некоторую долю в них до их IPO.

Для обычного инвестора это очень привлекательно. Потому что по традиционному пути у них обычно есть возможность купить акции только после IPO компании. А к тому моменту самый ранний и бурный рост, скорее всего, уже получен основателями, сотрудниками, ранними фондами и институциональными инвесторами.

С юридической точки зрения, этот фонд зарегистрирован как закрытая управляющая инвестиционная компания в соответствии с американским Законом об инвестиционных компаниях 1940 года. Он был создан 8 апреля 2021 года, 7 августа 2025 года преобразован в Delaware statutory trust (траст по законодательству Делавэра) и в настоящее время проводит непрерывное размещение. Первоначальный порог входа — 500 долларов, последующие допвложения не имеют минимума, на сайте даже поддерживается регулярное ежемесячное инвестирование.

Эта упаковка очень умна. С одной стороны, она сохраняет главную приманку частного рынка — растущие компании до IPO. С другой стороны, она старается сделать процесс покупки похожим на розничный финансовый продукт. Американским пользователям не нужно сначала становиться аккредитованными инвесторами, входить в круг состоятельных лиц или сталкиваться со сложной обработкой налоговых форм, как в традиционных私募基金 (частных фондах). По крайней мере, точка входа сделана максимально простой.

Доступ к частным компаниям не означает, что это простое инвестирование

И именно потому, что нарратив USVC достаточно соблазнителен, необходимо четко прописать лежащие в его основе ограничения.

Во-первых, инвесторы покупают лишь долю в фонде. Фонд через венчурные фонды, SPV и прямые инвестиции косвенно или прямо владеет этими непубличными растущими компаниями. То есть, инвесторы получают возможность «доступа к непубличным растущим компаниям», а не четкий опыт владения, как при покупке акций, с возможностью мгновенной продажи.

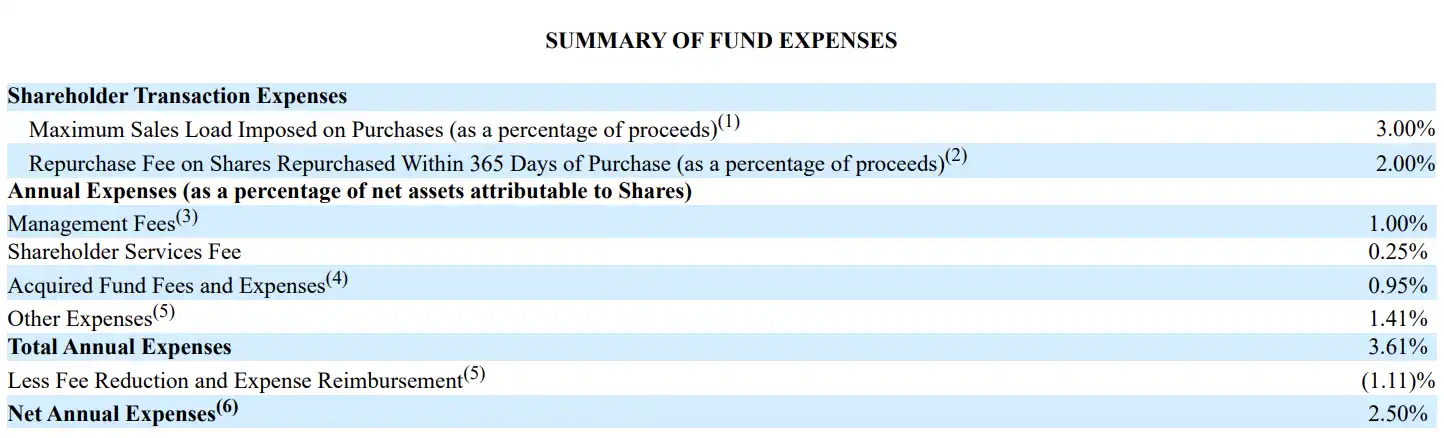

Во-вторых, этот доступ платный, и стоимость немалая. Таблица сборов на странице 20 проспекта показывает, что управленческий сбор USVC составляет 1,00%, сбор за обслуживание акционеров — 0,25%, сборы и расходы базовых фондов — 0,95%, прочие расходы — 1,41%, общая годовая ставка сборов — 3,61%. После применения скидки (действует как минимум до 29 октября 2026 года) чистая годовая ставка сборов составляет 2,50%. С учетом затрат на базовые венчурные vehicle и операционных расходов, инвесторы сталкиваются с продуктом, чья текущая чистая ставка сборов не так уж мала.

В-третьих, этот фонд не предоставляет обычным инвесторам по-настоящему ликвидный путь для выхода. USVC не торгуется на бирже, у него нет публичного рынка, ликвидность в основном зависит от того, будет ли совет директоров инициировать квартальный выкуп, причем выкуп обычно не превышает 5% чистой стоимости активов. В документах изначально был установлен сбор за выкуп в размере 2% при владении менее года, но совет директоров в настоящее время решил отменить его (может быть изменен или прекращен). Это означает, что он немного гибче традиционного венчурного фонда, но до возможности «входить и выходить когда угодно» еще далеко.

В-четвертых, у USVC нет фиксированной даты ликвидации, как у традиционных венчурных фондов 10+2, но это также долгосрочная закрытая структура без четкого срока окончания. Реализация стоимости базовых активов по-прежнему зависит от того, произойдут ли такие события ликвидности, как IPO, слияния и поглощения или сделки на вторичном私募 (частном) рынке. В проспекте также прямо указано, что многим портфельным инвестициям могут потребоваться годы, чтобы показать appreciation (рост стоимости).

И даже после IPO портфельных компаний они часто подпадают под ограничения lock-up, обычный период блокировки — 180 дней. В течение этого времени сам фонд или управляющие базовыми VC/SPV, в которые инвестировал фонд, могут быть не в состоянии немедленно продать акции.

Почему эталонный фонд привлекает внимание сообщества Web3?

Дополнительное внимание со стороны сообщества Web3 к USVC также связано с многолетней вовлеченностью Навала и AngelList в криптоиндустрию.

Навал давно является одним из самых публичных сторонников криптоактивов и нарратива Web3 среди инвесторов Кремниевой долины. В 2017 году в интервью Laura Shin он сказал, что его внимание уже тогда largely (в значительной степени) переключилось на Crypto; к 2021 году он вместе с партнером a16z Крисом Диксоном в длинной беседе с Тимом Феррисом системно обсудил Web3, NFT и цифровую собственность.

На платформы AngelList все эти годы не относилась к Crypto как к периферийному бизнесу, начав в 2022 году поддерживать инвестиции через USDC на своей платформе. На сайте AngelList сейчас есть отдельная страница решений для Crypto, где четко указано, что они сотрудничают с CoinList для поддержки Crypto SPV и связанных фондовых vehicle.

Кроме того, все больше криптобирж и проектов Web3 ускоряют запуск продуктов Pre-IPO. USVC представляет собой медленную институциональную переменную, в то время как большинство продуктов Web3 Pre-IPO представляют собой быстрые переменные, движимые эффективностью, и часто предлагают возможность выхода в любое время.

Два мира изначально говорили на разных языках, но теперь начинают конкурировать за одних и тех же инвесторов, за один и тот же нарратив и за одно и то же беспокойство: если великие компании выходят на биржу все позже, может ли обычный человек вообще получить свою долю «до IPO»?

Имя Навала может приоткрыть эту дверь. Сетевая платформа AngelList может приблизить частные компании. Но мир за дверью от этого не становится намного проще.