Автор: Tiger Research

Компиляция: AididiaoJP, Foresight News

Комиссия по ценным бумагам и биржам США (SEC) готовится официально представить на этой неделе рамки «инновационного освобождения», которые позволят третьим сторонам токенизировать акции американских компаний, такие как Apple и Tesla, без одобрения самих компаний. Этот шаг может ускорить переход традиционных фондовых рынков на блокчейн, но также вызывает у бирж глубокую обеспокоенность по поводу фрагментации ликвидности и утечки доходов.

Как сообщило Bloomberg 18 мая, эта инициатива берет начало из видения дерегуляции, предложенного в феврале прокрипто-комиссарами Полом Аткинсом и Хестер Пирс. Coinbase и Blockchain Association уже направили официальные письма поддержки, настоятельно призывая предоставить третьим сторонам право на токенизацию. Однако руководящие указания, опубликованные Пирс 22 мая, оказались более узкими по охвату, чем ожидалось рынком. Они применяются только к инструментам на базе блокчейна, полностью сохраняющим права акционеров, и прямо исключают синтетические токенизированные акции без прав голоса или получения дивидендов.

Две ключевые угрозы: фрагментация ликвидности и фрагментация доходов

Ключевое влияние токенизированных акций заключается в «фрагментации». В криптоиндустрии часто говорят об агрегации ликвидности, но традиционные финансы видят в этом структурную угрозу.

- Фрагментация ликвидности: Когда одна и та же акция токенизируется на разных блокчейнах и децентрализованных платформах, торговые объемы и потоки заказов, которые ранее концентрировались на NYSE или Nasdaq, рассредоточатся по множеству площадок. Это приведет к ценовым различиям между платформами, увеличению проскальзывания при крупных сделках и снижению общей эффективности рынка.

- Фрагментация доходов: После рассредоточения торговых площадок комиссии за сделки и доходы посредников, которые ранее принадлежали местным биржам, потекут в зарубежные или другие конкурирующие платформы, напрямую влияя на финансовую конкурентоспособность страны.

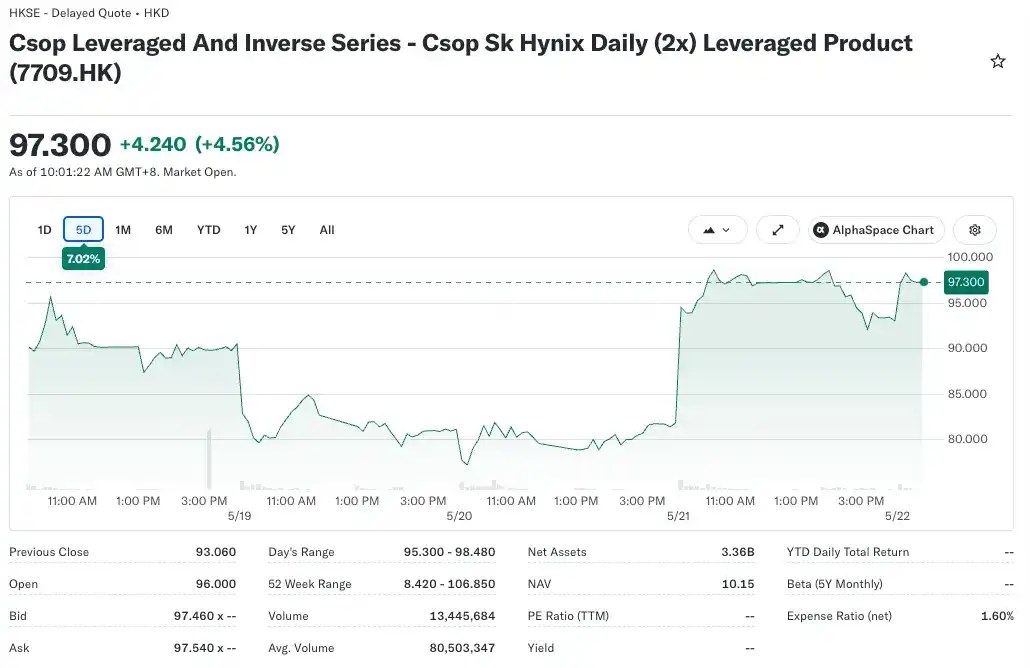

Отчет Tiger Research приводит в пример Южную Корею: ETF с двойным кредитным плечом на акции SK Hynix, запущенный гонконгской управляющей компанией CSOP, вырос до крупнейшего в мире ETF с кредитным плечом на отдельную акцию с активами под управлением более 110 млрд вон (около 80 млрд долларов США). Если бы Корея первой, через регуляторные песочницы, запустила подобный продукт, эти комиссии за управление и финансовые доходы могли бы остаться внутри страны.

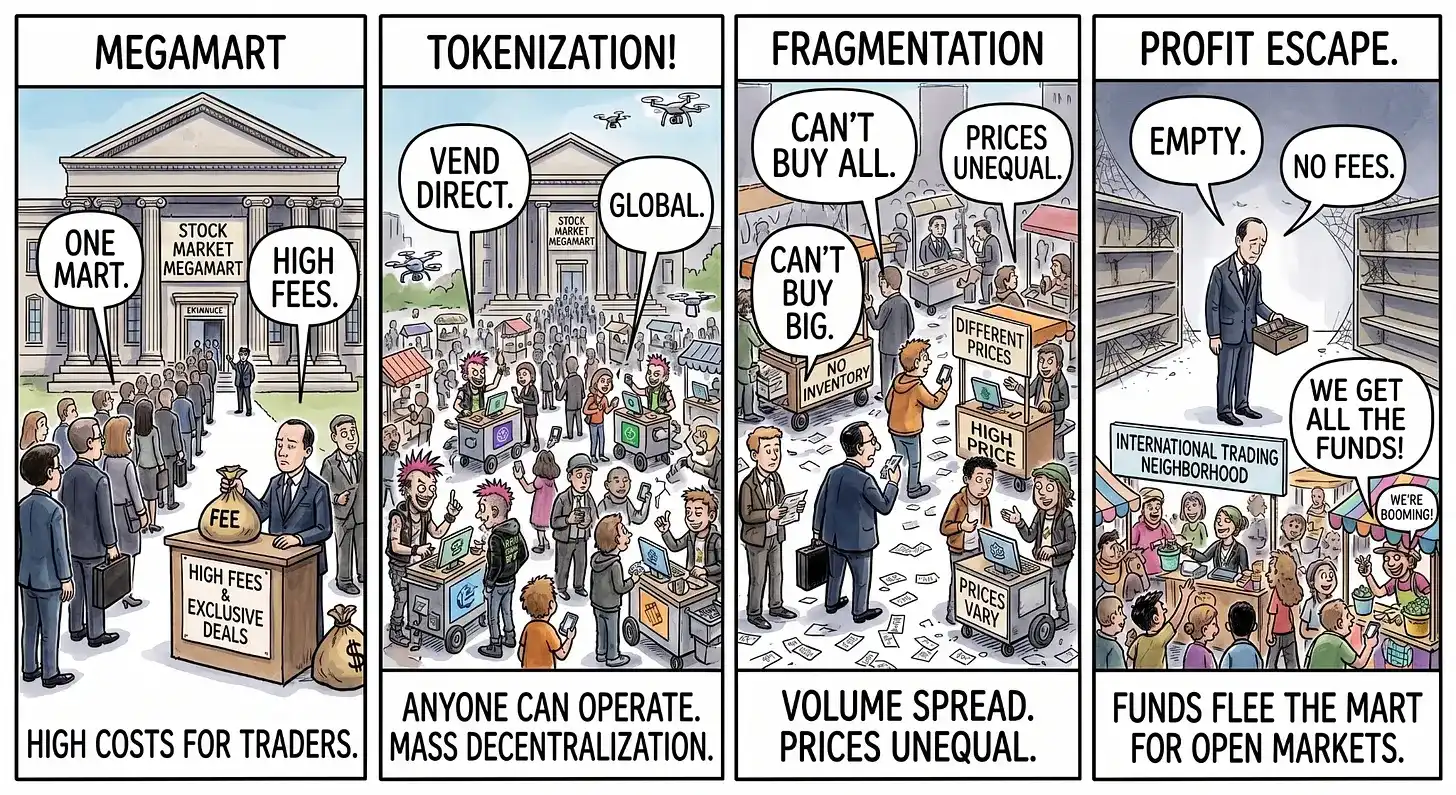

Монополии традиционных бирж, похожим на «супермаркеты», грозит конец

Отчет описывает эти изменения с помощью яркой аналогии: традиционный фондовый рынок похож на единственный в своем роде супермаркет, где концентрируются все покупатели и продавцы, а биржа монополизирует торговлю и взимает сборы. Токенизация акций эквивалентна разрешению любому без разрешения открывать тысячи уличных ларьков и совершать сделки прямо снаружи этого супермаркета.

Такое рассредоточение приведет к потере покупателей, снижению глубины стакана на каждой площадке, затруднению крупных сделок и разделу источников дохода. Если местные биржи будут медлить из-за регуляторных ограничений, конкурирующие платформы из других юрисдикций первыми перехватят потоки глобального капитала и доходы посредников.

Фрагментация капитала уже происходит

В тот же день, когда SEC подала сигнал о запуске рамок (18 мая), открытый интерес к RWA (активам реального мира) на децентрализованной платформе Hyperliquid превысил 2,6 миллиарда долларов, установив исторический рекорд. Под влиянием спроса на круглосуточную торговлю традиционными активами в сети, объемы торгов RWA на перпетуальных DEX, как ожидается, будут стремительно расти.

Традиционные финансовые институты и регуляторы сталкиваются с дилеммой: либо, как NYSE, активно строить инфраструктуру для токенизации через сотрудничество, либо лоббировать регуляторов для блокировки инноваций с целью защиты существующих доходов. Регуляторы также в раздумьях: им необходимо контролировать темп инноваций, но при этом не допустить перехвата внутренних доходов зарубежными платформами.

Даже после официального объявления рамок потенциальные конфликты только начинаются. Две ключевые проблемы в будущем включают:

- Вторую «битву за ясность» вокруг прав акционеров;

- То, как включить в регуляторную систему такие платформы, как Hyperliquid, которые выросли в регуляторной серой зоне. Если они будут признаны нелицензированными биржами, это может вызвать новый шок для ликвидности и неопределенности.

В эпоху цифровых активов финансовые институты и юрисдикции, которые не смогут действовать быстро, навсегда потеряют долгосрочные монопольные права на сборы и финансовое лидерство, а капитал продолжит рассредоточиваться во всех направлениях.