Автор | Odaily Planet Daily (@OdailyChina)

Автор | Asher (@Asher_ 0210)

Рынки предсказаний, несомненно, являются одним из самых обсуждаемых направлений в Web3 на данный момент.

Торговля прогнозами, касающимися макроэкономических событий, криптоиндустрии и даже развлекательных тем, продолжает набирать обороты, а количество обсуждений и участников постоянно растет. Однако, по мере быстрого развития рынка, постепенно стали появляться и диссонирующие голоса — некоторые события при расчетах расходятся с ожиданиями пользователей, основанными на здравом смысле или «понимании реальности», что вызывает споры о дизайне правил, справедливости и даже доверии к платформам.

В последнее время на рынках предсказаний произошло два высококонфликтных события. Ниже Odaily Planet Daily проведет их обзор и анализ.

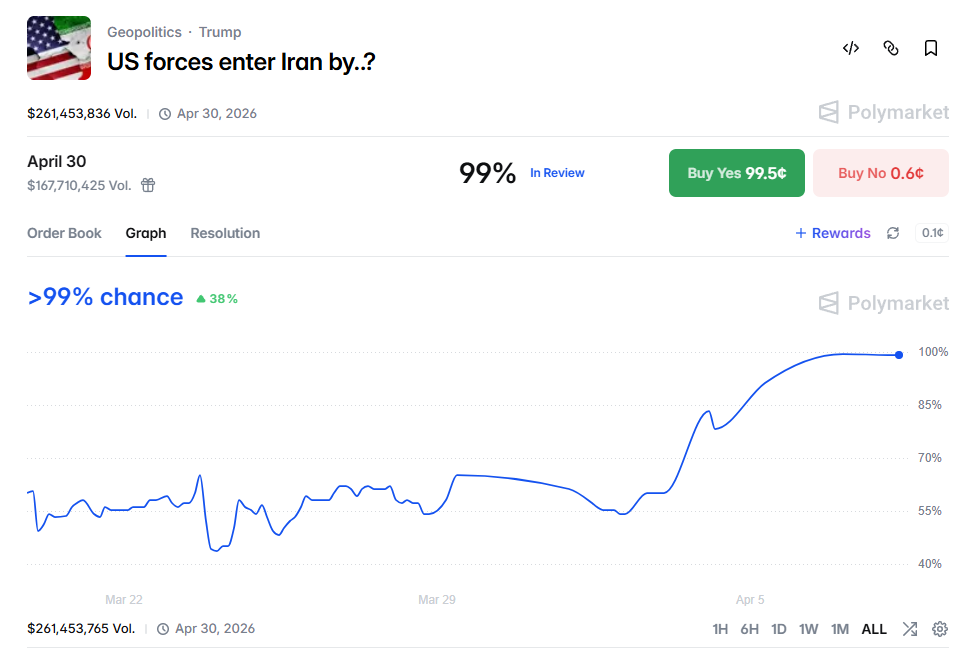

Polymarket: Спасение США пилота ВВС на территории Ирана было признано вторжением США в Иран

3 апреля истребитель ВВС США F-15E Strike Eagle был сбит иранской системой ПВО на юго-западе Ирана. Два члена экипажа (пилот и офицер по вооружениям) катапультировались, один был быстро спасен, другой пропал без вести на несколько дней, скрываясь в иранских горах.

- ВВС США随后展开搜索与救援(SAR)行动,涉及武装飞机、直升机等,最终成功救出第二名伤势严重的机组人员(特朗普亲自宣布“WE GOT HIM”).

- Спасательная операция предусматривала вход войск США на территорию Ирана (поиск в горах, возможные наземные или низковысотные операции), что привлекло внимание на фоне нынешней чувствительной геополитической обстановки.

Поскольку вход войск США на территорию Ирана в некоторой степени также является вторжением США в Иран, это напрямую повлияло на событие прогнозирования на платформе Polymarket о том, когда США вторгнутся в Иран (US forces enter Iran by?).

Согласно правилам расчета, вход действующих военнослужащих США (включая силы специальных операций) на сухопутную территорию Ирана до указанной даты считается вторжением, сбитые пилоты не считаются вторжением, но отправленные США силы специальных операций действительно вошли на территорию Ирана для спасения пилота. Таким образом, вход сил специальных операций в Иран для спасения пилота соответствует критерию判定为 Yes для вторжения США в Иран.

Событие «спасение пилота» Polymarket уже признал вторжением США в Иран, что вызвало серьезные споры в сообществе.

Сторонники «засчитать вход» (сторона Yes) считают, что эта операция соответствует определению «входа» в правилах. Силы специальных операций США намеренно (deliberately) вошли на территорию Ирана для выполнения задачи, и в правилах четко указано, что «special operation forces will qualify», а также охватывается «for operational purposes (including humanitarian)». С объективной точки зрения, это первое подтвержденное проникновение американских войск на землю на фоне текущего конфликта, военнослужащие США действительно ступили на иранскую землю, поэтому это следует рассматривать как «вход».

Противники «засчитать вход» (сторона No) считают, что такое определение является чрезмерным расширением. По своей сути эта операция была краткосрочной, ограниченной по масштабам гуманитарной спасательной операцией (humanitarian rescue), а не боевым вторжением (invasion), и не имела intent оккупации, что не соответствует общепринятому пониманию «входа войск США в Иран». Кроме того, в правилах четко исключено, что «pilots who are shot down... will not qualify», а данная операция как раз была围绕 сбитого пилота, имея характер «вынужденного входа», и по логике должна относиться к аналогичным исключительным случаям. Ссылаясь на прецеденты (например, подобные действия в регионе не рассматривались как вторжение), спасательные операции не должны приравниваться к военному входу; если判定为 Yes, это может поощрить маргинальные интерпретации правил, подрывая серьезность и последовательность рынка. Китайское сообщество также普遍 считает, что «вход в Иран»更应该 относиться к крупномасштабным наземным или amphibious операциям, а не к краткосрочным акциям по принципу «спасли и ушли».

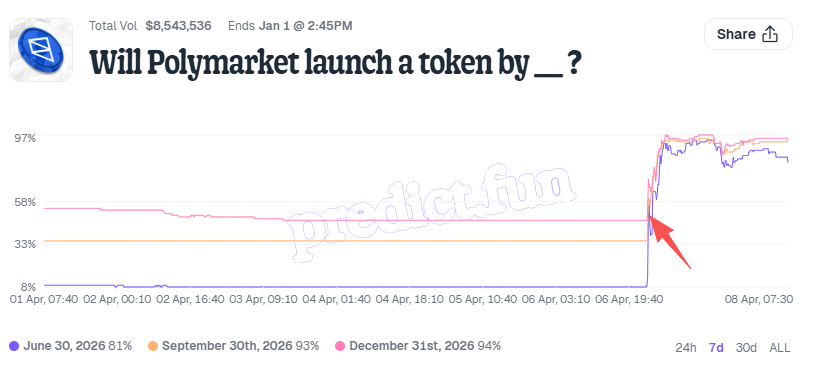

Predict.fun: Выпуск стейблкоина Polymarket был признан выпуском токена

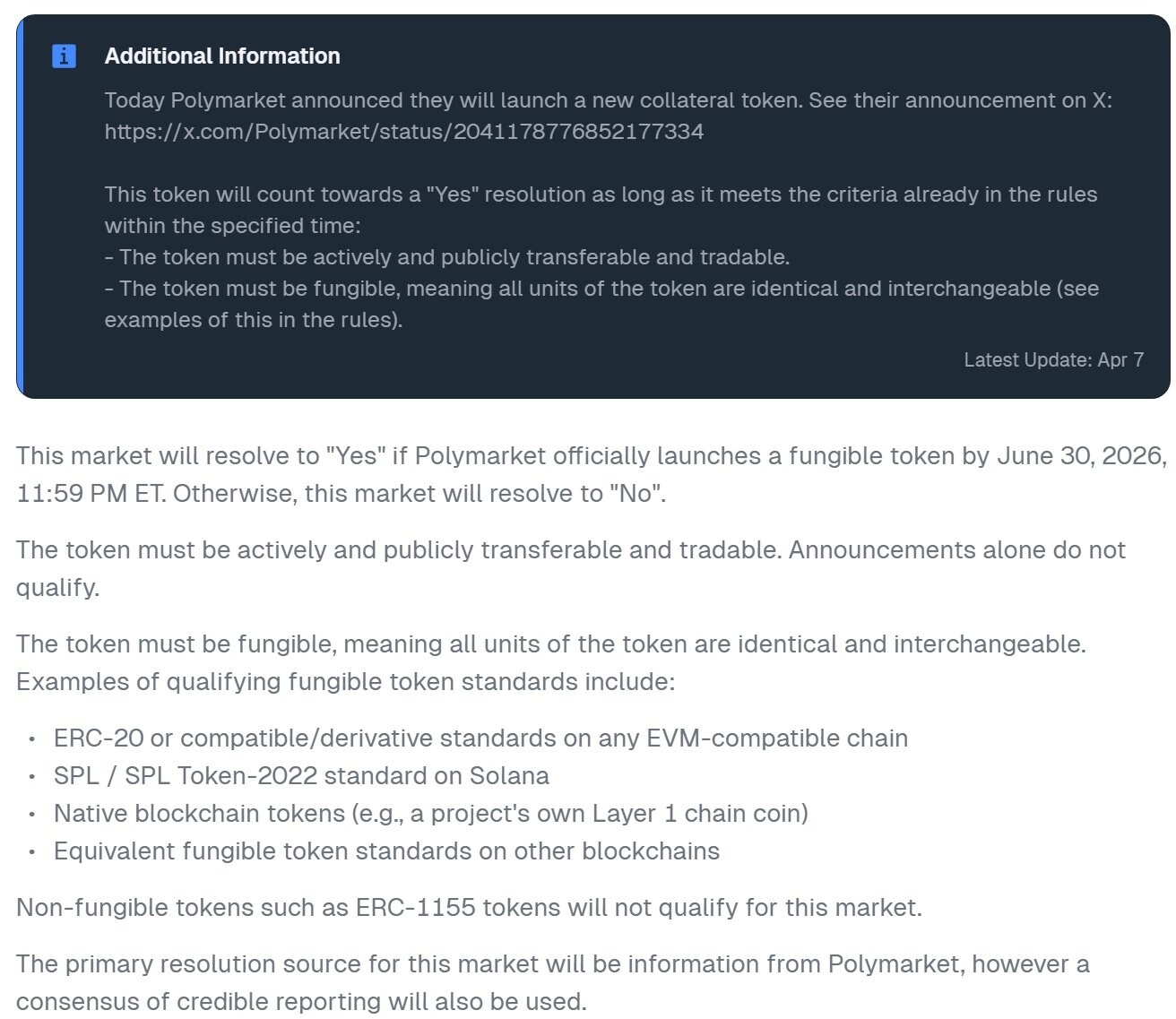

Вечером 6 апреля Polymarket официально announced в X о进行全面 обновления биржи:

- Перестроить торговый движок, обновить смарт-контракты;

- Выпустить новый нативный залоговый токен Polymarket USD (привязанный 1:1 к USDC, для замены USDC.e, снижения рисков бриджинга).

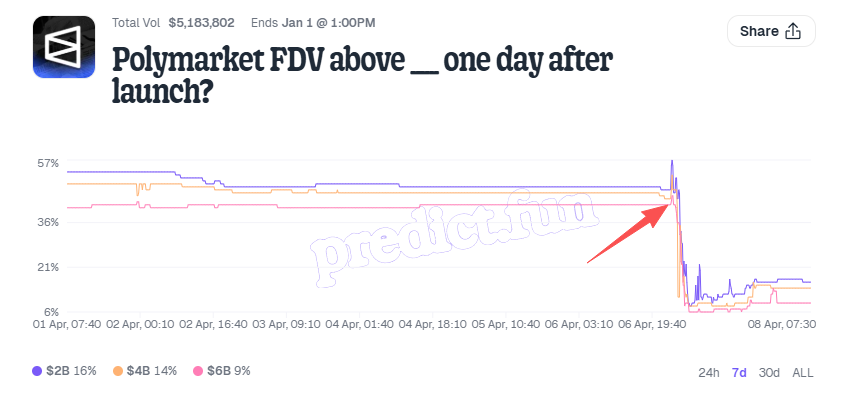

Второй пункт提及 о выпуске нативного залогового токена Polymarket USD напрямую повлиял на вероятность двух связанных событий прогнозирования на платформе Predict.fun:一是 выпуск токена;二是 рыночная капитализация после выпуска:

1、Когда Polymarket выпустит токен (Will Polymarket launch a token by ___ ?)

2、FDV Polymarket через день после запуска (Polymarket FDV above ___ one day after launch?);

Если смотреть согласно документации правил расчета, там четко указано, что «Любой выпускаемый Polymarket взаимозаменяемый токен (fungible token) считается 'выпуском токена' в данном событии», стейблкоин, конечно, не исключение. Поэтому стейблкоин Polymarket соответствует критерию判定为 Yes.

Пояснения, связанные с правилами расчета

Сообщество развернуло вокруг этого дебаты.

Сторонники считают, что согласно букве правил, «выпуск токена» не ограничивается только « governance токеном» (governance token), а является общим обозначением для всех токенов. При этом Polymarket USD как выпускаемый Polymarket взаимозаменяемый токен ERC20/SPL по своей сути соответствует определению «выпуска токена». Кроме того, последующие дополнительные разъяснения официальных лиц являются скорее重申原有规则, а не临时修改规则, поэтому具有一定的 обоснованностью с точки зрения compliance.

Однако скептики не принимают это объяснение. С одной стороны, они считают, что включение стейблкоина в категорию «выпуска токена» является чрезмерной интерпретацией правил, типичной игрой слов; с другой стороны, даже если признать, что стейблкоин也算 «выпуск токена», ядром данного рынка прогнозов является «Polymarket FDV», а не «Polymarket USD FDV». Стейблкоин скорее является инструментом залога (collateral) или расчетов, его структура рыночной капитализации fundamentally отличается от структуры основного токена проекта (например, governance токена POLY), поэтому не должен напрямую приравниваться или заменять логику общей оценки проекта.

Вы на чьей стороне?

В целом, все спорные события на рынках предсказаний сводятся к核心问题: вы ставите на «реальность» или на «правила». Часто эти два понятия не полностью совпадают.

Для нас, участников рынков предсказаний, понимание самих правил, возможно, важнее, чем предсказание исхода события. Как определяются источники информации, есть ли исключительные条款, есть ли пространство для интерпретации — эти детали в关键时刻 напрямую определяют победу или поражение.

Именно поэтому некоторые события с высокой вероятностью, кажущиеся «инвестиционными сделками»,未必 не несут рисков, а反而 могут быть потенциальными «сделками с потерей всего». Многие развороты происходят как раз в этих упущенных из виду деталях. Вместо слепых ставок, лишний взгляд на правила полезнее, чем жалобы после потери денег.