Автор: Nic Carter

Компиляция: Deep Tide TechFlow

Введение от Deep Tide: Спецназовец армии США заработал 40 000 долларов на Polymarket, используя конфиденциальную информацию. Это лишь последний скандал. Nic Carter указывает, что прогнозные рынки попали в порочный круг: они зависят от инсайдерской торговли для формирования точных цен, но это заставляет розничных трейдеров чувствовать, что рынок манипулируют, и уходить. Это противоречие определяет, смогут ли прогнозные рынки выжить в долгосрочной перспективе.

Как я писал в феврале этого года, прогнозные рынки имеют серьезную проблему с инсайдерской торговлей, и это не случайность. Это приводит к серьезному режиму сбоя:

Социальная ценность прогнозных рынков заключается в использовании денежных стимулов для разглашения конфиденциальной информации инсайдерами, но со временем это разрушает доверие розничных трейдеров к рынку.

Два дня назад разразился самый крупный на сегодняшний день скандал: Министерство юстиции США обвинило сержанта спецназа Гэннона Кена Ван Дайка в незаконной торговле с использованием конфиденциальной информации. Перед рейдом на Мадуро он заработал 40 000 долларов на Polymarket. Он был не обычным солдатом, а старшим членом "Зеленых беретов", ответственным за планирование и проведение специальных операций.

Скажу прямо: хотя многие призывают к снисхождению к нему из-за распространенной (законной) инсайдерской торговли среди конгрессменов, он все равно должен сесть в тюрьму. Его действия потенциально могли раскрыть детали предстоящего рейда венесуэльцам через торговую активность, что является морально и юридически неприемлемым. Хотя венесуэльцы, похоже, не заметили, правительство не может допустить такого прецедента: элитные военнослужащие раскрывают детали предстоящих операций через рыночную активность в личных интересах. Я сочувствую Ван Дайку, но он действительно нарушил закон и данную им присягу хранить секреты.

Это лишь последний в череде реальных или предполагаемых скандалов с инсайдерской торговлей на прогнозных рынках. Ранее Израиль арестовал двух военнослужащих запаса за использование военной разведывательной информации для торговли на Polymarket. Рынки, связанные со временем начала войны с Ираном, соглашениями о прекращении огня, убийством Хаменеи и помилованием Байдена, также вызывали подозрения, но арестов пока не последовало. Kalshi и Polymarket также отметили и приостановили аккаунты, торгующие на рынках, в которых они были заинтересованы, например, три кандидата в Конгресс, делающие ставки на свои собственные избирательные кампании.

Можно подумать, что эти проблемы исчезнут по мере того, как все больше людей осознают, что торговля с использованием конфиденциальной информации незаконна не только на фондовых рынках, но и на прогнозных рынках. Но я считаю, что проблема глубже.

Предпосылка прогнозных рынков заключается в том, что они информационно эффективны, потому что вознаграждают осведомленных инсайдеров.

Другими словами, прогнозные рынки «хороши», потому что они собирают массу неосведомленных розничных трейдеров, которые создают экономические стимулы для инсайдеров раскрывать частную информацию. (Эта концепция — розничные трейдеры создают стимулы для участия осведомленных инсайдеров — хорошо обоснована в финансовой литературе, и недавняя статья further распространяет ее на прогнозные рынки.) Затем прогнозные рынки могут надежно рекламировать себя как имеющие социальную полезность, поскольку они действительно предоставляют более качественный и своевременный сигнал по сравнению с другими платформами (эксперты, опросы и т.д.). Kalshi и Polymarket знают это, но не хотят прямо признавать. Но они намекают на это в своем маркетинге!

Генеральный директор Kalshi Тарек Мансур в подкасте Sourcery прямо заявил: «На товарных рынках не существует инсайдерской торговли. На самом деле, это вся инсайдерская торговля», что является... крайне творческим толкованием закона. Он добавил:

Я думаю, что есть часть инсайдерской информации (которой трейдеры) не могут торговать, но я думаю, что сейчас мы ограничиваем это немного слишком строго.

Kalshi использовала слоганы типа «Торгуйте чем угодно» и «Каждый в чем-то эксперт», оба из которых предполагают, что обычные люди могут монетизировать на платформе любую привилегированную информацию, которой они случайно обладают.

Генеральный директор Polymarket Шейн Коплан в прошлом году имел такой диалог с CBS:

Андерсон Купер: Но прогнозные рынки действительно полагаются на то, что некоторые люди обладают инсайдерской информацией.

Шейн Коплан: Угу. Да. Я думаю, что это хорошо, когда люди имеют преимущество на рынках. Очевидно, ими нужно управлять, нужно очень четко и строго определять границы, например, с этической точки зрения, мы тратим на это много времени. Но это в некоторой степени неизбежно, и от этого можно получить много пользы. Знаете, люди адаптируются.

Шейн также говорил, что прогнозные рынки — это «самая точная вещь, доступная человечеству на данный момент, пока кто-нибудь не создаст какой-нибудь супер-хрустальный шар». Часть этой точности исходит от инсайдеров.

Генеральный директор Robinhood Влад Тенев (сотрудничающий с Kalshi) сказал:

Прогнозные рынки фактически позволяют вам получать новости быстрее, в некоторых случаях даже до того, как они произошли. Я думаю, что это действительно имеет огромную экономическую ценность.

Экономист Робин Хэнсон, которого многие считают крестным отцом прогнозных рынков, прямо принимает эту точку зрения и высказал пространную защиту инсайдерской торговли на прогнозных рынках. В 2024 году он сказал:

Если цель (прогнозного) рынка — получить точную информацию в цене, то вы определенно хотите разрешить инсайдерам торговать, даже если это заставляет других не желать делать ставки из-за ощущения несправедливости, потому что это сделает цену более точной. Это приоритет.

Должен отметить, что и у Kalshi, и у Polymarket есть политика против инсайдерской торговли. Kalshi регулируется CFTC и всегда четко запрещала торговлю на основе существенной непубличной информации (MNPI) и проводила мониторинг рынка. Когда я писал предыдущий блог в феврале, я заметил, что Polymarket не санкционировал явно инсайдерскую торговлю, но в марте они обновили свод правил, добавив подробный запрет на следующие виды торговли:

- Торговля на основе украденной конфиденциальной информации (если вы солдат, планы операций принадлежат не вам, а правительству)

- Торговля на основе информации, незаконно переданной вам инсайдером

- Торговля по любому контракту, на результат которого вы можете повлиять

Цель этого раздела не в том, чтобы винить Kalshi или Polymarket или их руководство за намеки на то, что трейдеры имеют информационное преимущество. Я считаю, что их политика (после обновления в марте 2026 года) достаточно ясна. Вместо этого я хочу указать на фундаментальное противоречие, которое преследует эти рынки:

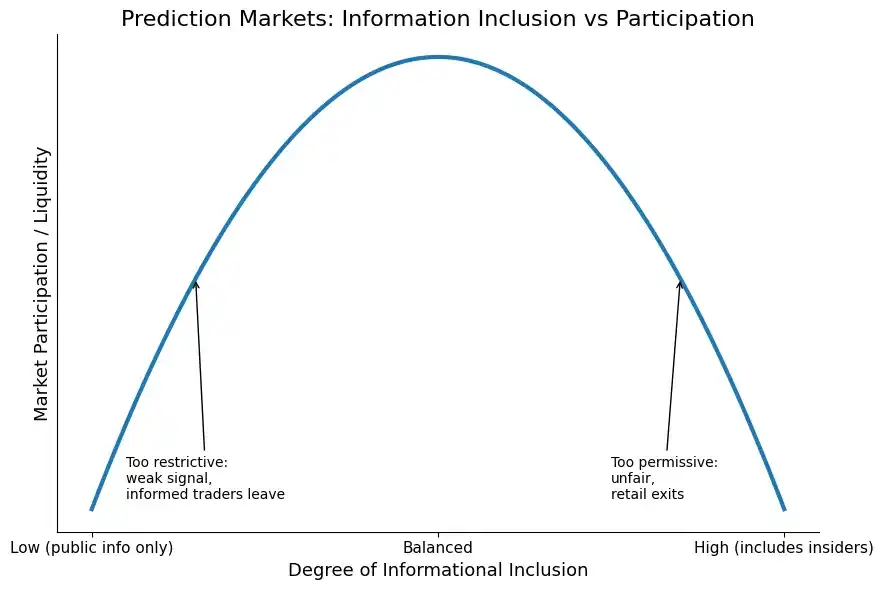

Прогнозные рынки зависят от информированных трейдеров для формирования точных цен, но также зависят от неинформированных трейдеров, создающих экономические стимулы для привлечения информированного потока сделок. Это создает напряжение:

- Если слишком терпимо относиться к инсайдерской торговле, неинформированные трейдеры могут уйти, чувствуя несправедливость

- Если слишком строго ограничивать инсайдерскую торговлю, рынок может исключить свои наиболее ценные источники информации

Таким образом, существует компромисс между информационной эффективностью и воспринимаемой справедливостью. Вот визуальная версия той же идеи:

График: Кривая компромисса между информационной эффективностью и воспринимаемой справедливостью

В итоге мы сталкиваемся с несколькими различными режимами сбоя:

Слишком много акул, которые съедают всю рыбу

Стандарты инсайдерской торговли слишком мягкие, рынок становится очень информационно эффективным, но розничные трейдеры явно чувствуют, что рынок «манипулируют», и они всегда делают ставки против инсайдеров. Следовательно, розничные трейдеры уходят, ликвидность рынка снижается. Это тот режим сбоя, о котором я говорил ранее. Это то, где мы находимся сейчас, но я думаю, что мы отскочим в другом направлении.

Нет акул, нет преимущества

Это другая сторона спектра. Инсайдерская торговля строго регулируется на платформах, осуществляется мониторинг рынка в реальном времени и строгая регуляторная отчетность, информированный поток сделок уходит. Эти рынки, следовательно, производят меньше информации, представляющей социальную ценность, становясь просто агрегаторами настроений, а не генераторами «новостей до новостей». Таким образом, платформы не могут эффективно продвигать себя.

Экзистенциальный вопрос заключается в том, существует ли золотая середина: ликвидность максимизирована, розничные трейдеры считают рынок «достаточно справедливым», а информированные потоки сделок все еще получают вознаграждение за свою информацию. График предполагает, что она может существовать, но реальность более хаотична.

Мой прогноз февраля все еще в силе. Как я тогда сказал:

Серьезный риск остается: скандалы с инсайдерской торговлей заставят розничных трейдеров почувствовать, что рынком манипулируют, что приведет к их уходу с платформы. Я предсказываю череду событий, связанных с инсайдерской торговлей в этом году, которые убедят платформы значительно усилить мониторинг рынка и приведут к тому, что Polymarket, в частности, отойдет от анонимного режима.

Я ожидаю, что Polymarket полностью отменит возможность торговать без KYC (что сейчас имеет место на платформе для не-США) и усилит выявление подозрительных сделок на платформе. Будет много уголовных дел о краже инсайдерской информации, но искушение останется. Хотя платформы не признают этого, существует «социально оптимальный» количество инсайдерской торговли. Но смогут ли они оптимально его откалибровать? Разрешат ли им это регуляторы?

Стоит отметить, что не все информированные трейдеры являются инсайдерами. Вы можете стать информированным, собирая публичную информацию и торгуя на ее основе. Но часть информированных трейдеров действительно составляют инсайдеры, присваивающие информацию.