Автор:Ли Дань

В то время как недавние выпуски продуктов от Anthropic и «апокалиптический отчет» Citrini усилили панику инвесторов, бум искусственного интеллекта (ИИ) прошел прямое испытание: NVIDIA представила «взрывные» результаты, доказав, что спрос, генерируемый ИИ, остается сильным.

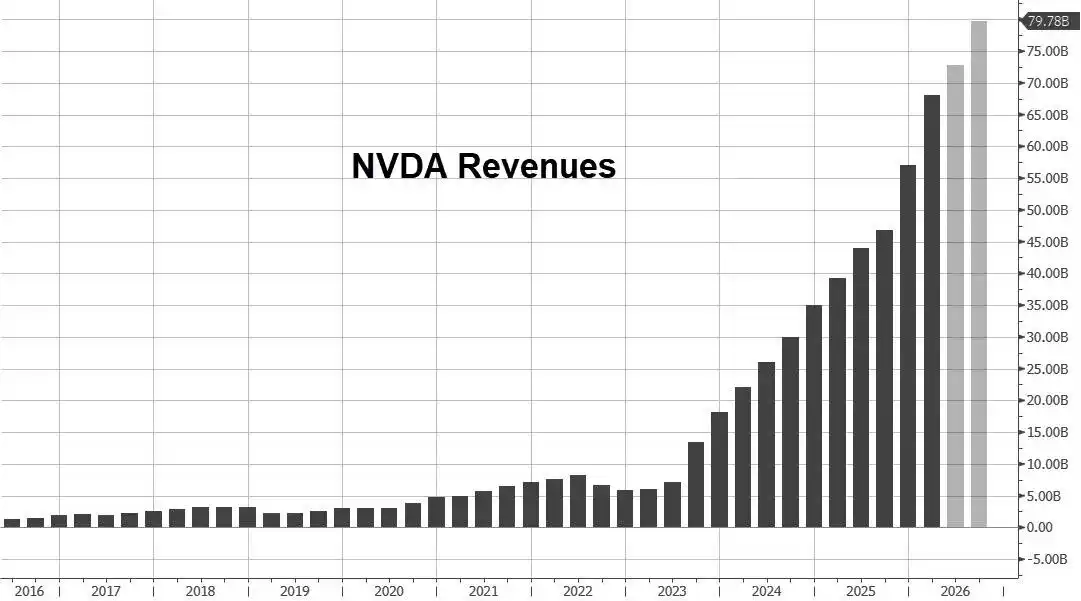

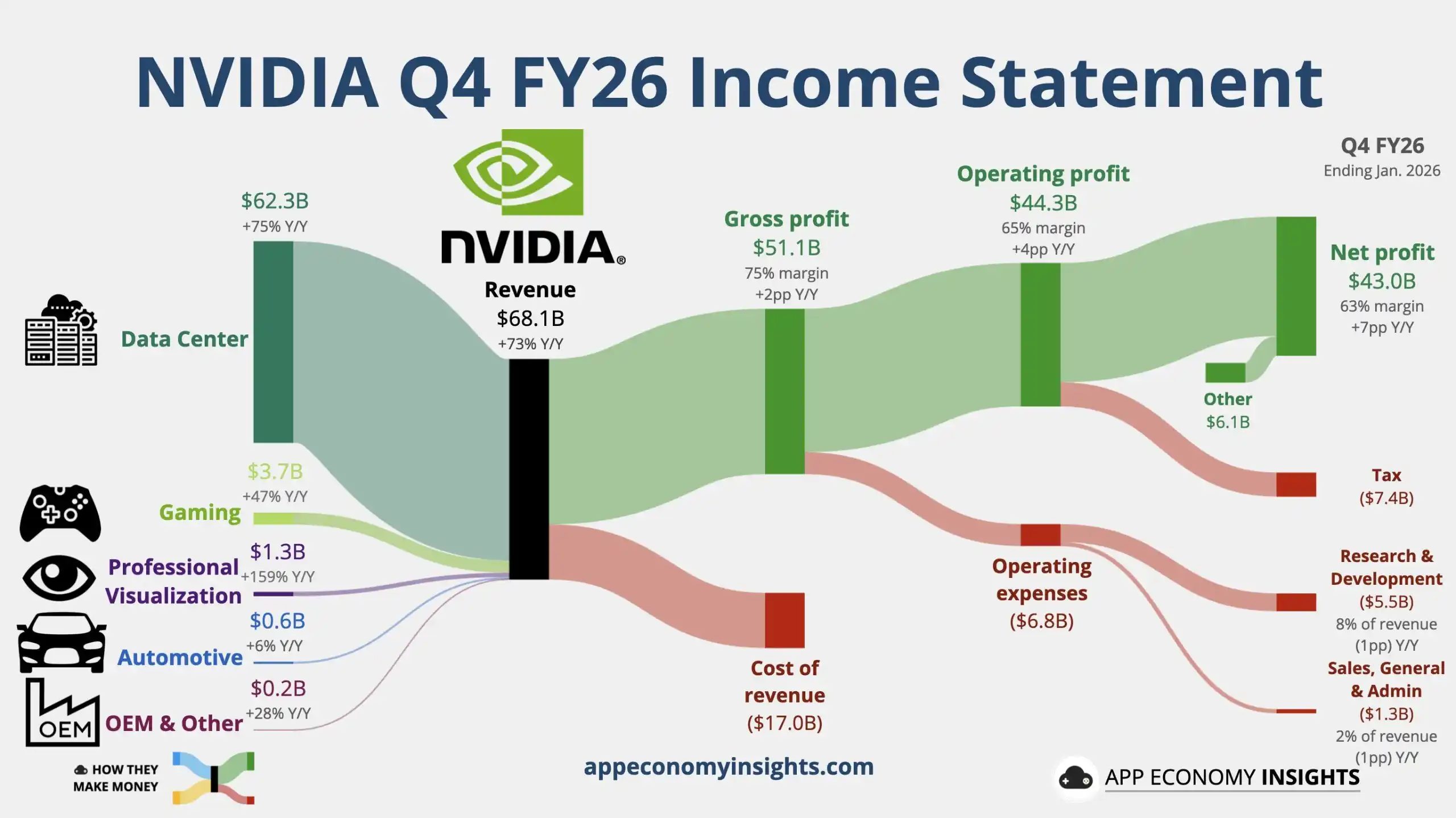

В среду, 25-го числа по восточному времени США, NVIDIA сообщила, что в четвертом финансовом квартале 2026 финансового года (закончившемся 31 января 2026 года) выручка достигла рекордных 681 млрд долларов, увеличившись примерно на 70% в годовом исчислении. Ключевой бизнес центра обработки данных, на который приходится более 90% выручки, также установил рекордный квартальный доход, превысив ожидания аналитиков более чем на 3%.

Прибыль NVIDIA в четвертом квартале также была сильной. Скорректированная прибыль на акцию (EPS) по не-GAAP выросла более чем на 80% в годовом исчислении, что примерно на 5,9% выше ожиданий аналитиков, а валовая прибыль также неожиданно выросла до 75,2%, достигнув максимума за полтора года.

Еще более обнадеживающим для инвесторов стало то, что руководство NVIDIA на первый финансовый квартал 2027 финансового года также оказалось лучше ожиданий. Ожидается, что выручка снова достигнет рекордного уровня, среднее значение прогноза на 7,1% выше среднего прогноза аналитиков и даже на 4% выше оптимистичных ожиданий покупателей, при этом годовой темп роста ускорился по сравнению с четвертым кварталом до почти 77%. NVIDIA отметила, что этот прогноз не включает доход от вычислений в центрах обработки данных на рынке Китая.

На телеконференции по результатам в эту среду генеральный директор NVIDIA Хуан Жэньсюнь также повысил предыдущий прогноз по доходам от чипов, заявив: «Мы превысим цель в 5 триллионов долларов. Поставки удовлетворят спрос вплоть до следующего года». На конференции GTC в октябре прошлого года Хуан Жэньсюнь透露, что NVIDIA в общей сложности получила заказы на чипы на 5 триллионов долларов на 2025 и 2026 календарные годы, включая чипы следующего поколения Rubin, серийное производство которых начнется в этом году.

Хуан Жэньсюнь заявил, что клиенты соревнуются в инвестициях в ИИ-вычисления. Спрос на вычисления стремительно растет. Использование агентов предприятиями резко возросло. Говоря о «космических центрах обработки данных», он отметил, что текущая экономика космических ЦОД еще «скудна», но ситуация будет меняться со временем.

После публикации отчетности акции NVIDIA, которые в среду уже выросли более чем на 1%, резко подскочили во внеурочных торгах, их рост быстро расширился, в какой-то момент превысив 4%. Аналитики считают, что ключ к тому, что рынок «покупается», заключается в следующем: доходы от центра обработки данных и общая выручка превысили ожидания; валовая прибыль продолжает улучшаться по мере наращивания производства чипов нового поколения Blackwell, и, даже без учета части доходов с китайского рынка, руководство на этот финансовый квартал является более сильным, укрепляя нарратив о resilience спроса на вычислительные мощности ИИ.

Однако во время телеконференции акции NVIDIA продолжали отдавать gains, уйдя в минус во внеурочных торгах, в какой-то момент упав более чем на 1%. Некоторые комментарии гласят, что разворот акций вниз показывает, что инвесторы не впечатлены новым guidance, намекая, что опасения по поводу перегрева экономики ИИ продолжат беспокоить NVIDIA. Другие аналитики отмечают, что высокие темпы роста операционных расходов и включение вознаграждений на основе акций (SBC) в не-GAAP показатели, начиная с первого квартала, могут в краткосрочной перспективе изменить восприятие инвесторами «темпов роста прибыли».

Q4: Выручка достигла рекордного квартального уровня, валовая прибыль - максимум за полтора года

Выручка NVIDIA в четвертом квартале выросла на 73% в годовом исчислении до 681,27 млрд долларов, что значительно выше роста в 62% в предыдущем квартале и превышает собственный прогноз компании в 650 млрд долларов (mediana). Аналитики ожидали выручку в 659,1 млрд долларов при росте примерно на 68% г/г. Годовая выручка NVIDIA также достигла рекордного уровня: 2159,38 млрд долларов, что на 65% больше, чем в предыдущем году.

Валовая прибыль стала еще одной яркой точкой четвертого квартала: по не-GAAP она составила 75,2%, увеличившись на 1,7 п.п. в годовом исчислении и на 1,6 п.п. кв/кв, достигнув максимума со второго финансового квартала 2025 финансового года и превысив консенсус-прогноз аналитиков в 74,7% и оптимистичный прогноз в 75,0%.

Финансовый директор (CFO) NVIDIA Колетт Кресс пояснила, что улучшение валовой прибыли в годовом исчислении связано с «сокращением отчислений в резервы под запасы», а квартальное улучшение связано с «улучшенной продуктовой и cost структурой» благодаря продолжающемуся наращиванию объемов чипов Blackwell.

Однако за весь 2026 финансовый год валовая прибыль по не-GAAP снизилась с 75,5% в предыдущем финансовом году до 71,3%, упав на 4,2 п.п. в годовом исчислении, что свидетельствует о том, что на этапе перехода на новые платформы и наращивания поставок рентабельность за год по-прежнему подвергалась структурным сбоям.

Центры обработки данных: рост вычислительной мощности стабилизировался, сеть ускоряется

В четвертом квартале бизнес NVIDIA по центрам обработки данных показал выручку в 623,14 млрд долларов, что на 75% больше, чем год назад, и выше роста в 66% в предыдущем квартале. Аналитики ожидали роста почти на 70% г/г до 603,6 млрд долларов.

Внутри сегмента центров обработки данных NVIDIA предоставила две более值得注意 цифры:

- Доход от вычислений (Compute) в ЦОД: 513,34 млрд долларов, рост на 58% г/г, что немного выше роста в 56% в третьем квартале.

- Доход от сетей (Networking) в ЦОД: 109,80 млрд долларов, рост на 263% г/г, что значительно превышает рост в 162% в третьем квартале.

NVIDIA приписала взрывной рост сетевых доходов: «запуску и continued ramp» NVLink compute fabric для систем GB200 и GB300, а также continued росту платформ Ethernet и InfiniBand.

Другими словами, рынку не следует следить только за темпами поставок самих GPU, но и видеть, что NVIDIA упаковывает «вычислительную мощность, interconnect, системы» в комплексные решения, которые труднее заменить, причем высокие темпы роста сетевых доходов являются финансовым отражением этой стратегии.

Что касается структуры клиентов, компания disclosed: в четвертом квартале на долю доходов от hyperscale-провайдеров пришлось чуть более 50% от общего дохода бизнеса центров обработки данных, что по-прежнему делает их крупнейшей категорией клиентов, но рост доходов в квартале в большей степени пришел от других клиентов ЦОД, что свидетельствует о диверсификации источников дохода и marginal снижении риска концентрации.

Blackwell стимулирует игровой спрос, краткосрочные помехи от поставок и каналов

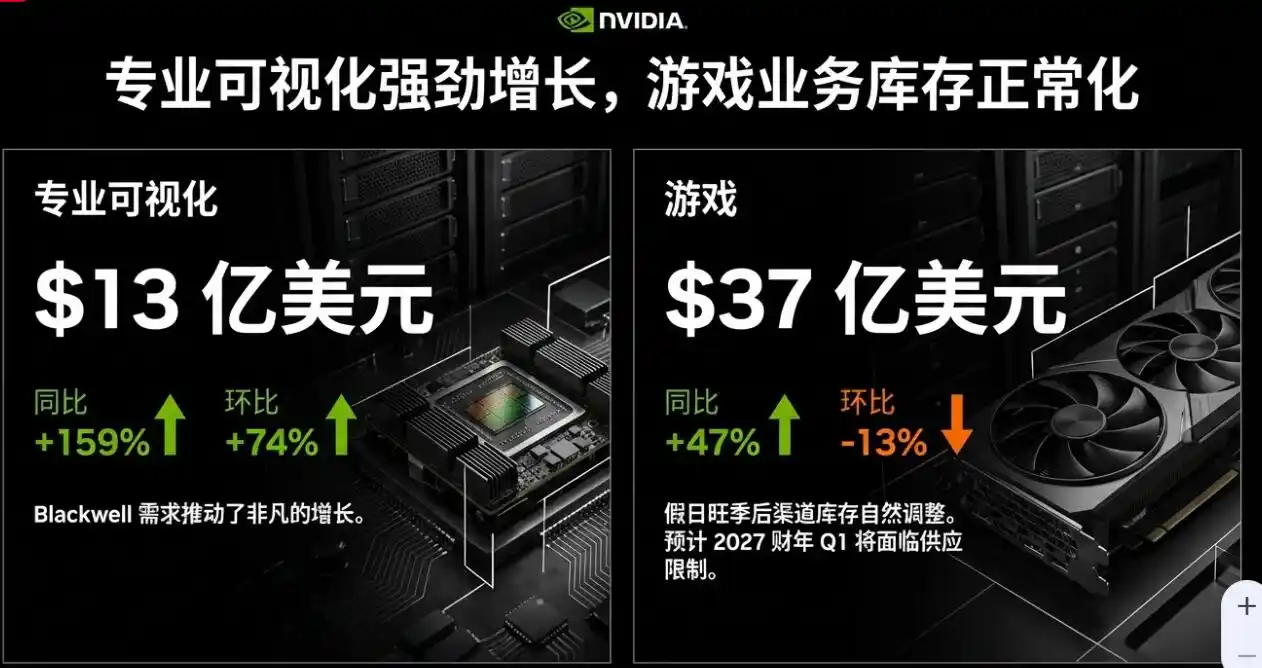

Выручка игрового подразделения NVIDIA в четвертом квартале составила 37,27 млрд долларов, увеличившись на 47% в годовом исчислении. Аналитики ожидали 40,1 млрд долларов, в предыдущем квартале рост составил 30% г/г.

Ускорение роста игрового бизнеса в четвертом квартале NVIDIA объяснила главным образом strong спросом на чипы Blackwell. Однако доходы в этом сегменте снизились на 13% кв/кв из-за «естественного снижения канальных запасов после праздничного сезона». Тревожно, что NVIDIA четко предупредила: ожидается, что limited поставки станут headwind для игрового бизнеса в первом квартале и beyond.

Выручка от профессиональной визуализации в четвертом квартале составила 13,21 млрд долларов, рост на 159% г/г. Аналитики ожидали 7,707 млрд долларов, в предыдущем квартале рост составил 56% г/г.

Профессиональная визуализация также показала рост доходов более чем в два раза в годовом исчислении и на 74% кв/кв благодаря Blackwell, став одним из самых ярких businesses роста помимо центров обработки данных. Однако объем этого бизнеса намного меньше, чем у ЦОД.

Прогноз по выручке на Q1: среднее значение роста ~77% г/г, без доходов от вычислений в ЦОД в Китае

Что касается guidance, NVIDIA сообщила, что ожидает выручку в первом квартале в размере 780 млрд долларов плюс-минус 2%, то есть от 764,4 до 795,6 млрд долларов. Этот диапазон означает, что выручка компании в этом финансовом квартале обновит рекорд, установленный в четвертом квартале.

По среднему значению прогноза выручки NVIDIA ожидает, что выручка в первом квартале вырастет на 76,9% в годовом исчислении, further ускорившись по сравнению с ростом в 73% в четвертом квартале.

Среднее значение прогноза выручки NVIDIA не только выше среднего прогноза аналитиков в 727,8 млрд долларов, но и превышает оптимистичные ожидания покупателей в 740–750 млрд долларов.

Валовая прибыль NVIDIA в первом квартале, как ожидается, снова достигнет максимума со второго финансового квартала 2025 финансового года, что соответствует оптимистичным ожиданиям Уолл-стрит.

Ожидается, что скорректированная валовая прибыль по не-GAAP в первом квартале составит 75% плюс-минус 50 базисных пунктов, то есть от 74,5% до 75,5%. Оптимистичный прогноз покупателей — 75%, консенсус-прогноз продавцов — 74,7%.

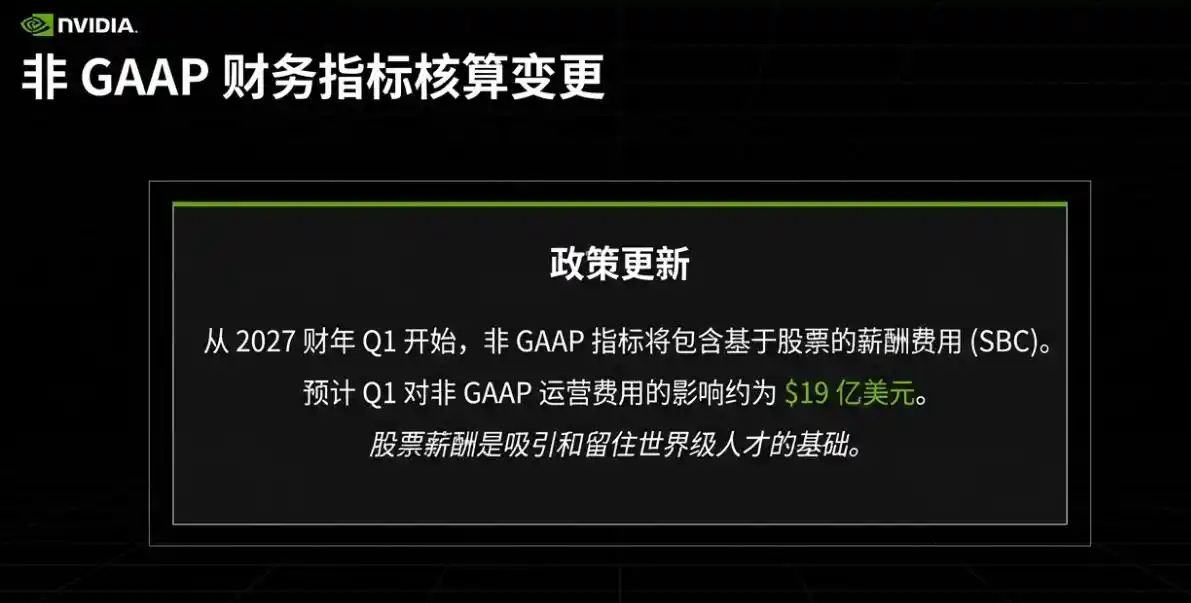

С Q1 вознаграждения на основе акций включаются в не-GAAP

Одновременно с публикацией отчетности NVIDIA объявила, что, начиная с первого квартала, финансовые показатели по не-GAAP больше не будут исключать вознаграждения на основе акций (SBC). В результате этой корректировки NVIDIA ожидает, что операционные расходы по не-GAAP в первом квартале будут затронуты на сумму approximately 19 млрд долларов.

Это изменение напрямую изменит «привычную методологию», которую рынок долгое время использовал для сравнительного анализа рентабельности и расходов, и в краткосрочной перспективе может потребовать повторной калибровки consensus моделей, а также позволит инвесторам более четко увидеть реальные затраты NVIDIA на сохранение лидерства в талантах и разработках.