В 2026 году рынок акций США демонстрирует крайнюю раздробленность: Nasdaq не обновлял максимумы уже 4 месяца, а оценки лидеров ИИ страдают в тупиковой ситуации томительного ожидания нового цикла снижения ставок; однако, на другом конце рынка, промышленные, энергетические и коммунальные акции прорываются вперед под грохот «старого мира».

Этот раскол посылает четкий сигнал: конкуренция в сфере ИИ окончательно превратилась из борьбы алгоритмов в борьбу за физические ресурсы. Если 2024 год был «годом чипов», то 2026 год становится «годом модернизации энергосистем».

В настоящее время переоценка стоимости активов электроэнергетики стала неизбежной. В 2023-2024 годах рынок покупал «мозги» (чипы), а в 2025-2026 годах капитал устремляется к «сердцу и сосудам» (электроэнергия и энергосистемы).

Эта статья предоставит инвесторам полный анализ структурных изменений, конкурентной среды и возможностей, содержащихся в американской индустрии электроэнергетики и энергосистем.

Команда исследований RockFlow считает, что инвесторам следует сосредоточиться на трех уровнях: уровне программного обеспечения и автоматизации с высокой маржой, представленном такими компаниями как GEV, уровне производства оборудования с высокой предсказуемостью, где доминируют Eaton и Schneider, и на прямых получателях红利 от инфраструктуры, возглавляемых PWR.

1. Ударный спрос со стороны ИИ и «старческие болезни» американской энергосистемы

За последние несколько десятилетий американцы почти забыли, что такое «дефицит электроэнергии». В начале 2000-х годов, благодаря распространению светодиодного освещения и принудительному внедрению сертификации EPA «Energy Star», потребление энергии в США чудесным образом стабилизировалось, несмотря на рост населения.

Но этот застой был полностью нарушен в 2025 году. С экспоненциальным ростом крупномасштабных центров обработки данных и приложений ИИ кривая спроса на энергию показала почти вертикальный перелом:

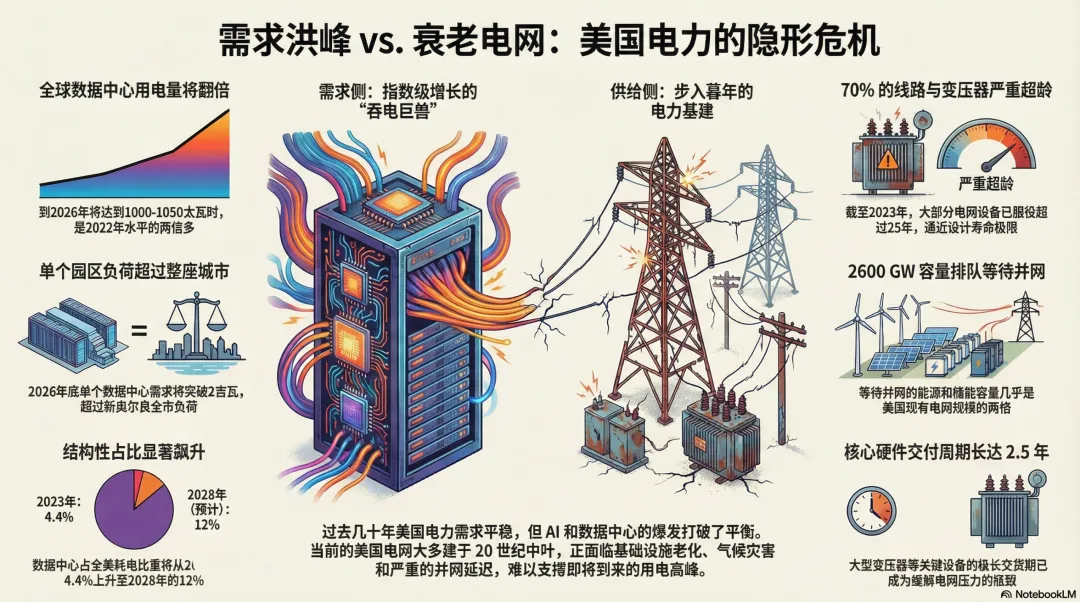

- Удвоенное потребление: Ожидается, что к 2026 году мировое потребление электроэнергии центрами обработки данных достигнет 1000-1050 ТВт·ч (Тераватт-час), что более чем в два раза превышает уровень 2022 года.

- Масштаб города: К концу 2026 года потребность в электроэнергии отдельного кампуса центра обработки данных превысит 2 ГВт (Гигаватт). Это эквивалентно нагрузке среднего города.

- Структурная доля: В 2023 году центры обработки данных составляли лишь 4.4% от потребления электроэнергии в США; а к 2028 году, по прогнозам, этот показатель взлетит до 12%.

Помимо ИИ как «пожирателя энергии», реиндустриализация и общая электрификация общества (электромобили, тепловые насосы и т.д.) также одновременно повышают нагрузку. Электроэнергетика превращается из скучной отрасли «нулевого роста» в новый период быстрого расширения.

Ярким контрастом этому выступают «старческие болезни» американской энергосистемы.

Текущая энергосистема США не была designed для поддержки эры ИИ. Она больше похожа на «лоскутное чудовище», собранное из технологий середины XX века и залатанное.

Энергосистема состоит в основном из трех частей: генерация, передача и распределение. Проблема заключается в следующем:

- Устаревшая инфраструктура: По состоянию на 2023 год, 70% линий электропередач и трансформаторов в США прослужили более 25 лет. Большая часть сетей была построена в 60-70-х годах прошлого века и приближается к предельному сроку службы в 50-80 лет.

- «Последняя капля» изменения климата: В первой половине 2025 года произошли десятки погодных катастроф с ущербом в миллиарды долларов. Экстремальная жара, вызывающая провисание линий, и ураганы, выводящие из строя энергосистемы, становятся нормой региональных отключений.

С другой стороны, мы видим отчаянный «кризис очередей». В настоящее время почти 2600 ГВт энергетических и储能ционных мощностей (почти вдвое больше существующего размера сети США) ожидают в очереди подключения к сети.

Сообщается, что сроки поставки крупных трансформаторов увеличились до 2.5 лет. Только в 2026/27 финансовом году клиенты компании PJM Interconnection будут дополнительно платить 3.5 миллиарда долларов за мощности из-за узких мест с подключением.

2. Переопределение умной сети

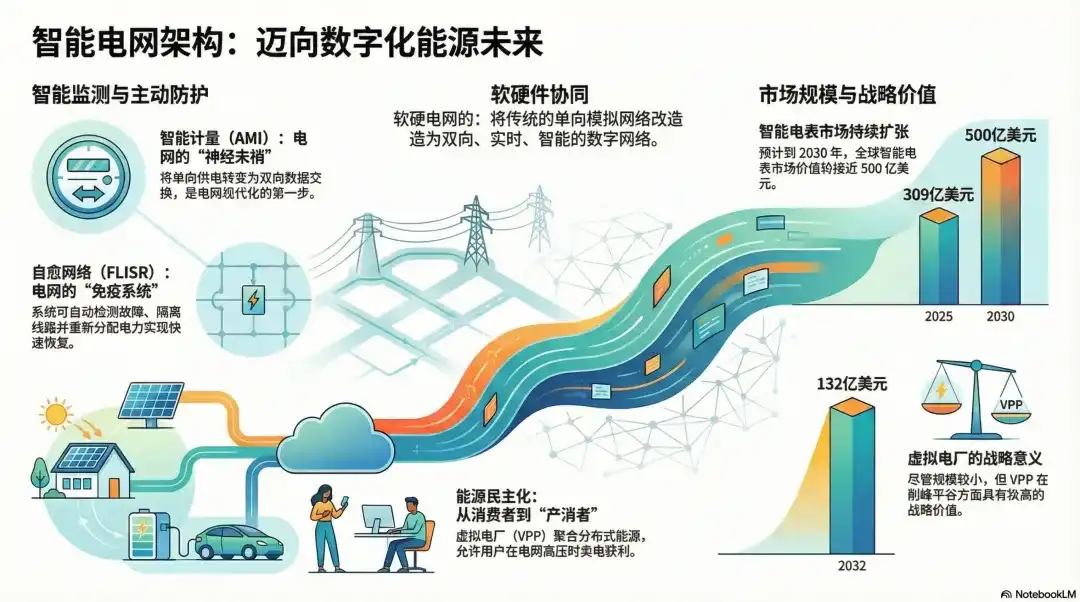

Так называемая модернизация энергосистемы — это не просто прокладка дополнительных линий электропередач, а преобразование традиционной однонаправленной аналоговой сети в двунаправленную, работающую в реальном времени, интеллектуальную цифровую сеть.

Нервные окончания: Интеллектуальный учет (AMI)

Усовершенствованная измерительная инфраструктура (AMI) — это первый шаг к модернизации. Она превращает однонаправленную подачу электроэнергии в двунаправленный обмен данными. Ее суть заключается в том, что интеллектуальные счетчики передают данные обратно в систему по радиочастоте или сотовой сети.

По данным статистики, в 2025 году мировой рынок интеллектуальных счетчиков оценивался примерно в 309 миллиардов долларов США, и ожидается, что к 2030 году он приблизится к 500 миллиардам.

Иммунная система: Автоматизация и самовосстанавливающиеся сети (FLISR)

Это переход инфраструктуры от пассивной к активной. Используя программное обеспечение, разработанное такими компаниями, как GE Vernova, модернизированная энергосистема может:

1. Автоматически обнаруживать: Точно определять место падения дерева или взрыва трансформатора.

2. Автоматически изолировать: Мгновенно отключать неисправную линию.

3. Автоматически восстанавливать: Перераспределять электроэнергию с соседних фидеров в нормальные зоны, достигая «самозаживления».

Демократизация энергии: Виртуальные электростанции (VPP)

VPP используют облачное программное обеспечение для агрегации домашних солнечной энергии, аккумуляторов электромобилей. Потребители больше не просто покупают электроэнергию, а превращаются в «просьюмеров» (Prosumers), продавая электроэнергию и зарабатывая деньги в периоды высокой нагрузки на сеть.

Хотя объем нишевого рынка составляет всего несколько сотен миллиардов долларов, его стратегическое значение для сглаживания пиков нагрузки чрезвычайно велико.

3. Кто делит этот огромный пирог?

Основываясь на отраслевых атрибутах и структуре прибыли текущей электроэнергетики и энергосистемы США, команда исследований RockFlow делит компании-бенефициары на четыре уровня:

Программное обеспечение и автоматизация: Интеллектуальный «мозг»

Это звено с самой высокой маржой и самыми глубокими рвами.

- GE Vernova (GEV): Координирует весь жизненный цикл энергии через платформу GridOS. Как чистый актив после разделения GE, она является абсолютным лидером в цифровизации энергосистем.

- Siemens (SIEGY): Обладает передовой системой Spectrum Power. Ее новая платформа Gridscale X определяет стандарты цифровизации на стороне распределения.

- Itron (ITRI): Король интеллектуального учета. Его продукты «Edge Intelligence» могут обнаруживать отключения в реальном времени без необходимости центральной обработки, являясь «хранителем» на конечных участках распределительной сети.

Производство оборудования и силовая электроника: Важный краеугольный камень

- Eaton (ETN): Гигант распределительных устройств. От автоматических выключателей до трансформаторов, продуктовый портфель Eaton охватывает почти все физические узлы модернизации сети.

- ABB: Глобальный эксперт в области высоковольтной продукции и автоматизации. Его рекордный объем невыполненных заказов в основном обусловлен проектами модернизации сетей.

- Schneider Electric (SBGSY): Специализируется на технологиях интеллектуальных сетей и решениях для микросетей, предоставляет комплексные решения для управления энергопотреблением, помогая центрам обработки данных максимизировать энергоэффективность. Через платформу EcoStruxure глубоко интегрирует аппаратное обеспечение с цифровым управлением, доминируя особенно в области центров обработки данных и микросетей.

Инжиниринг, закупки и строительство (EPC): Строители

- Quanta Services (PWR): Доминатор в области подрядов на передачу и распределение электроэнергии в Северной Америке. Ее недавнее гигантское соглашение с AEP на 72 миллиарда долларов является лучшим свидетельством тренда модернизации сетей.

- MasTec (MTZ): Специализируется на интеграции возобновляемых источников энергии в сеть. Ее невыполненные заказы на 17 миллиардов долларов предвещают всплеск результатов в ближайшие два года.

Регулируемые коммунальные предприятия: Консервативные «управляющие»

- NextEra Energy (NEE): Крупнейшая американская компания в области чистой энергии, специализирующаяся на ветровой и солнечной энергетике, обладает значительными активами возобновляемой энергетики и связывает себя с крупными клиентами через долгосрочные соглашения о покупке электроэнергии (PPA), обеспечивая стабильный доход.

- Duke Energy (DUK): Обладает обширной инфраструктурой энергосистем, охватывающей несколько кластеров центров обработки данных. Благодаря модернизации сетей передачи и распределения, компания может предоставлять центрам обработки данных услуги по高效、低损耗的电力传输服务 (эффективной передаче электроэнергии с низкими потерями). Кроме того, DUK также инвестирует в генерацию чистой энергии, удовлетворяя спрос центров обработки данных на зеленую электроэнергию.

Заключение: «Переоценка стоимости» активов электроэнергетики уже началась

В 2026 году электросеть больше не является забытой «коммунальной услугой», а становится ключевым активом, от которого зависит национальная безопасность и победа в гонке ИИ.

Команда исследований RockFlow считает, что для инвесторов компании, занимающиеся автоматизацией на основе программного обеспечения (GEV, ITRI), обладают самым высоким потенциалом премии; производители оборудования (ETN, ABB) имеют самую определенную видимость заказов; а гиганты EPC (PWR) являются прямыми получателями红利 от инфраструктуры.

В ближайшие пять лет альфа на американском рынке акций будет существовать не только в коде, но и в гудении каждого интеллектуального трансформатора.