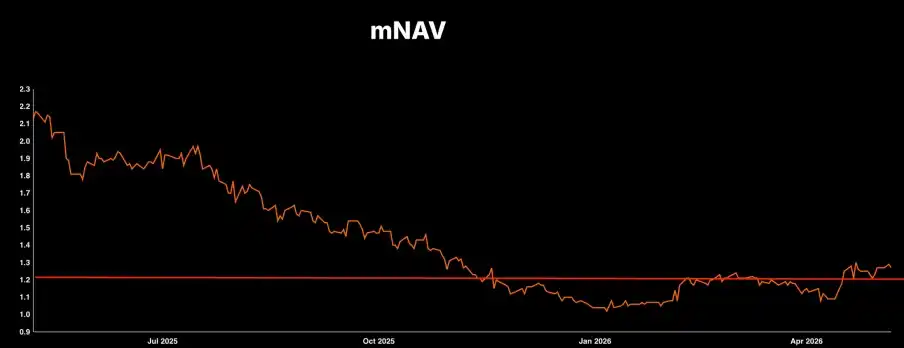

Этот отчёт о прибылях и убытках MicroStrategy (MSTR) кардинально меняет её игру: раньше это было «бездумная эмиссия акций для покупки биткоина», теперь компания официально представила открытый индикатор — премия 1.22x к mNAV (чистой стоимости активов). Именно это значение определяет, будет MSTR дальше покупать или продавать биткоин.

● Для MSTR:

○ Премия > 1.22x: Старая схема продолжается — выпуск дорогих акций, привлечение денег, покупка BTC.

○ Премия < 1.22x (ключевой разворот): Дальнейший выпуск акций становится невыгодным для компании. Руководство открыто заявило, что если премия опустится ниже этого уровня, они будут продавать BTC, чтобы использовать деньги для погашения долга или обратного выкупа акций.

● Как работает арбитраж: Если премия MSTR упадёт ниже 1.22x, откроется условная арбитражная возможность «лонг MSTR / шорт BTC». Потому что в этом случае компания сама выйдет на рынок, чтобы «продать биткоин и купить свои акции». Действия компании по продаже будут стирать спред. Заявление руководства — ключевая основа для уверенности в этой арбитражной сделке.

● Для STRC (привилегированных акций): Раньше все боялись, что маржин-колл MicroStrategy превратит эти привилегированные акции с дивидендами 11.5% в бумагу. Теперь официальная позиция «продавать биткоин для погашения долга при необходимости» означает, что у STRC появилась реальная «подушка безопасности», и это больше не финансовая пирамида.

● Для BTC (биткоина) в целом: Миф о «MicroStrategy, которая никогда не продаёт», разрушен, краткосрочные настроения — медвежьи. Но есть и плюс: активная распродажа монет для снижения левериджа компанией полностью устраняет будущий риск «цепной принудительной ликвидации» в случае глубокой «медвежьей» фазы.

Алмазные руки — больше нет: 1.22x mNAV — линия жизни и водораздел для BTC

За последние два года на рынке было много FUD вокруг MSTR, особенно касательно контроля над левериджем и процентными расходами. Биткоин — актив, не генерирующий денежный поток, но MSTR платит проценты за его финансирование. Откуда они берутся? На этом звонке по итогам 1-го квартала руководство лично заявило: при значении ниже 1.22x mNAV мы будем продавать биткоин.

Это равносильно раскрытию «козырей» компании и её «автоматической программы исполнения»:

● Выше уровня (фаза расширения баланса/«высасывания крови»): Компания — ярый бык по BTC. Пока розничные инвесторы готовы давать премию выше 1.22x, MicroStrategy может осуществлять «расширение баланса без арбитражного риска». Эмиссия акций для «высасывания» денег -> агрессивная покупка BTC -> рост балансовой стоимости активов -> рост цены акций. Этот позитивный маховик будет вращаться.

● Ниже уровня (фаза сжатия баланса/защиты): Маховик резко тормозит. Если MSTR слишком сильно дисконтируется относительно хранимого биткоина, дальнейший выпуск акций означает распродажу активов компании по заниженной цене. Руководство предельно рационально заявляет, что в этом случае продажа BTC за наличные для выплаты дивидендов, управления долгом или обратного выкупа обыкновенных акций MSTR по низкой цене будет иметь наибольший эффект для увеличения стоимости для существующих акционеров.

Это означает, что у MSTR наконец-то появилась жёсткая «линия поддержки стоимости». Это больше не поезд, несущийся без тормозов.

Арбитражная возможность: лонг MSTR / шорт BTC при падении ниже 1.22x mNAV

Чего больше всего боятся в арбитраже? Того, что вы обнаружили отличный спред, но рынок упорно остаётся нерациональным (например, MSTR постоянно торгуется со скидкой), и в итоге ваши хеджирующие позиции «съедаются» финансированием или процентными расходами.

Но порог в 1.22x, объявленный MSTR, предоставляет возможность для арбитража с высокой степенью определённости.

Подробная практическая логика:

● Строгие условия срабатывания: Только когда mNAV MSTR ощутимо опустится ниже 1.22x.

● Действия по открытию позиций: В этот момент цена MSTR оказывается «чрезмерно недооцененной» по отношению к её базовому активу — BTC. Трейдеры в этот момент открывают лонг по MSTR и одновременно шортят BTC на эквивалентную сумму.

● Непобедимая базовая логика: Даже если участники рынка не позволят спреду вернуться к норме, руководство MicroStrategy заставит его это сделать. После падения ниже порога, для достижения цели максимизации «биткоинов на акцию», руководство запустит объявленные операции по самоспасению — «продажа BTC, обратный выкуп недооценённых акций MSTR». Понимаете? Направление ваших лонг/шорт позиций будет полностью совпадать с направлением действий по поддержке со стороны самой компании на сотни миллиардов долларов. Вам не нужно гадать, вырастет или упадёт BTC завтра. Вам просто нужно спокойно забрать прибыль от «схождения спреда» — этот практически безрисковый доход.

Подсказка для наблюдения за рынком: В настоящее время премия MSTR колеблется около 1.28x, условия для арбитража не сработали. Слепое открытие позиций — это преждевременные действия. Но она уже вошла в зону отличного прицеливания. Установите ценовые оповещения и действуйте только после пробития уровня вниз.

3. Заметно повысилась «подушка безопасности» для STRC (привилегированных акций)

STRC предлагают дивидендную доходность до 11.5%. По старому «медвежьему» сценарию, MicroStrategy была игроком, взявшим огромный леверидж. В случае чёрного лебедя и обвала биткоина более чем вдвое, денежный поток MSTR иссяк бы, и такие привилегированные акции, как STRC, мгновенно превратились бы в бумагу.

Но отчёт за 1-й квартал полностью раскрыл реальную бухгалтерию компании, что не только стало ответом «медведям», но и успокоило капитал на рынке фиксированного дохода:

● Удивительная толщина активов: На стороне обязательств у компании есть привилегированные акции на 13.5 млрд долларов и конвертируемые облигации на 8.2 млрд долларов, но на стороне активов им соответствуют резервы BTC на ошеломляющую сумму в 64 млрд долларов. Чистый коэффициент левериджа составляет ничтожные 9%, что в традиционных финансах считается чрезвычайно устойчивым балансом.

● Стресс-тест в условиях экстремальной просадки: Даже если крипторынок повторит большой крах и BTC рухнет на 90% от текущих значений (до 7,300 долларов), продажи монет всё равно хватит, чтобы погасить весь чистый долг.

● Денежный ров: На крайний случай, если ликвидность биткоина на короткое время иссякнет и его будет не продать, на счетах компании лежат 2.25 млрд долларов чистых денежных средств. Одних процентов по этим деньгам на депозите достаточно, чтобы с закрытыми глазами оплачивать будущие 1.5 года ежегодных процентных платежей по долгу и дивидендов по привилегированным акциям (15 млрд в год). В совокупности, при условии, что BTC будет расти всего на 2.3% в год, процентные обязательства по STRC будут полностью покрыты.

Самое главное изменение ожиданий заключается в том, что руководство разрушило догматическую веру в «никогда не продавать монеты». Это означает, что до наступления экстремального кризиса они будут активно и постепенно продавать биткоин, чтобы сохранить кредитный рейтинг компании и платёжеспособность. STRC окончательно сбросили ярлык «крипто-пирамидальных высокодоходных облигаций», их логика ценообразования рисков уже приближается к традиционным качественным корпоративным облигациям, и впоследствии, вероятно, последуют покупки со стороны капитала традиционных институциональных инвесторов.

4. Влияние на BTC (биткоин) в целом: потеря «фанатичного покупателя последней инстанции», устранение «риска цепной ликвидации»

Эмоциональное воздействие этого звонка на спотовый рынок BTC двойственное, и трейдерам нужно смотреть на него в разных временных рамках:

● Краткосрочные трудности (негатив для настроений): Ранее розничные инвесторы воспринимали MicroStrategy как «пиксиу», который только покупает, никогда не продаёт и всегда может поддержать дно. Теперь руководство лично признало: «будем продавать монеты, если оценка неправильная». Это напрямую разрушает икону веры быков, что является серьёзным ударом по рыночным настроениям и спекулятивному ажиотажу в краткосрочной перспективе.

● Долгосрочная польза (улучшение структуры фундамента): Любой трейдер, немного знакомый с историей циклов, знает, почему прошлый «медвежий» рынок (2022 год) был таким жестоким? Потому что такие гиганты, как LUNA, Three Arrows Capital, Celsius, «держались до конца», пока ликвидность полностью не иссякала и их не ликвидировали принудительно, что вызывало цепные обвалы. Теперь MicroStrategy — это уже не «верующий», увлекаемый фанатизмом, а «старый волк с Уолл-Стрит», умеющий считать. Она установила чёткую линию предупреждения о продаже и научилась на ранних стадиях кризиса снижать леверидж путём активной перебалансировки. Это равносильно заблаговременному обезвреживанию самой большой «ядерной бомбы системного маржин-колла», висевшей над крипторынком.

Итог: MicroStrategy по-прежнему остаётся крупнейшим «главнокомандующим быками по BTC» на всём рынке акций США. Просто она эволюционировала из безрассудного солдата, знающего только атаку, в расчётливого стратега, умеющего и наступать, и отступать, и даже использовать рыночные настроения в свою пользу.