Автор: Кури, Shenchao TechFlow

Тот, кто построил этого лисёнка, больше не хочет строить.

23 апреля сооснователь MetaMask Дэн Финлей объявил об уходе из Consensys, завершив десятилетнюю карьеру разработчика. Причина — профессиональное выгорание и желание проводить больше времени с семьёй.

MetaMask, возможно, самое узнаваемое приложение в криптомире. Логотип с оранжевым лисёнком знает почти каждый, кто устанавливал криптокошелёк. В 2016 году Финлей и другой сооснователь Аарон Дэвис внутри Consensys создали это расширение для браузера, позволяющее обычным пользователям взаимодействовать с Ethereum без необходимости запускать полный узел.

За десять лет, по данным множества сторонних платформ, глобальное количество установок превысило 100 миллионов, месячная аудитория составляет около 30 миллионов пользователей, а функция свопа累计 сгенерировала комиссионных сборов на сумму более 325 миллионов долларов.

Посмотрев открытую информацию, обнаружил, что Финлей за последние десять лет почти не давал интервью. Раньше писал код в Apple, по натуре, должно быть, всё ещё инженер, а не человек, создающий себе имидж.

Когда такой человек говорит, что устал, обычно это значит, что он действительно устал. Просто момент его ухода заставляет много о чём задуматься.

Всего несколько месяцев назад Consensys привлекла J.P. Morgan и Goldman Sachs в качестве консультантов по IPO, и, согласно сообщению Axios, цель — выход на биржу уже в этом году.

Последний раунд финансирования компании состоялся ещё в 2022 году, тогда оценка составляла 7 миллиардов долларов, после чего прошло как минимум два раунда сокращений. А токен $MASK анонсировали ещё в 2021 году, но за пять лет так ничего и не произошло.

Кажется, выпуск токена для кошелька не так уж необходим, что страшнее, кажется, лисёнок тоже не так уж необходим для всех.

Кошелёк по умолчанию, но не обязательный вариант

Раньво многих документациях для разработчиков dApp первым шагом было «Пожалуйста, сначала установите MetaMask». Это был кошелёк по умолчанию для этой отрасли, как синий браузер IE на рабочем столе после установки Windows десять лет назад.

Проблема в том, что значение по умолчанию и предпочтительный вариант уже давно не одно и то же.

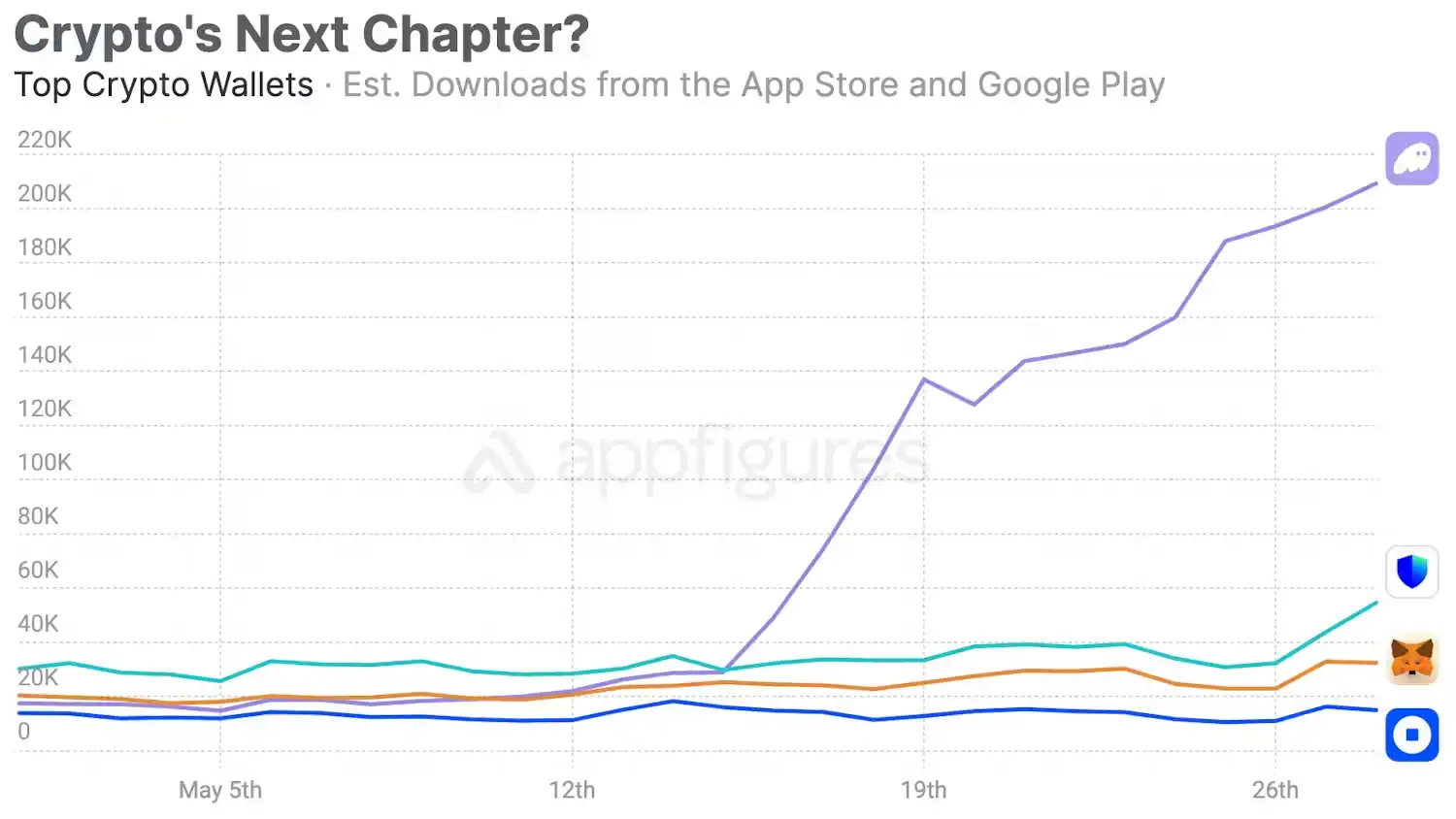

Компания Phantom изначально делала кошелёк только для Solana, позже расширилась на Ethereum и Bitcoin. В январе 2025 года привлекла 150 миллионов долларов в раунде C, оценка — 3 миллиарда.

Согласно оценкам whales.market, основанным на данных из блокчейна, годовой доход Phantom составляет около 108 миллионов долларов; для сравнения, у MetaMask — около 46 миллионов. Разница более чем в два раза, при этом Phantom младше MetaMask на пять лет.

Phantom стартовала на Solana в 2021 году и воспользовалась全过程 восстановления и взрывного роста экосистемы Solana. По данным Helius, в 2024 году объём торгов на DEX Solana уже превысил Ethereum, а в 2025 году общий доход от приложений в блокчейне достиг 2.39 миллиарда долларов, увеличившись на 46% год к году. 725 миллионов новых кошельков провели свою первую транзакцию в Solana в 2025 году. Эти пользователи заходили, а Phantom ждала их у входа.

А MetaMask? Нативную поддержку Solana запустила только в мае 2025 года. До этого пользователи, желавшие через MetaMask взаимодействовать с Solana, могли установить стороннее расширение под названием Snaps, опыт был сродни установке ядра Chrome в браузер IE...

За эти пять лет Solana из цепи, которая чуть не умерла из-за краха FTX,一度 стала цепью с наибольшим объёмом торгов. Phantom也跟着 росла в оценке, в начале 2025 года привлекла融资 в 150 миллионов долларов в раунде C, оценка — 3 миллиарда.

Автор считает, что медлительность MetaMask вызвана не технической невозможностью, но также вопросом идентичности. MetaMask — родное дитя Ethereum, а основатель материнской компании Consensys — сооснователь Ethereum Джо Любин.

Поддержка Solana для Phantom — это экспансия, для MetaMask — предательство. Когда скорость роста экосистемы Ethereum действительно замедлилась и пришлось выходить в мультичейн, окно возможности早已 закрылось.

Конечно, совместимость MetaMask внутри экосистемы Ethereum по-прежнему самая сильная, почти все dApp на EVM-цепях тестируют её как вариант по умолчанию, 30 миллионов месячных активных пользователей — не ложь.

Но эта привязка исходит не от продуктивности, а от成本 миграции. А成本 миграции может только остановить уход старых пользователей, но не предотвратить приход новых.

Человек, который начал играть в ончейн только в 2025 году, при установке кошелька, скорее всего, получит от друга рекомендацию уже не MetaMask.

Лисёнок, ожидающий своей цены

Продукт отстаёт, люди уходят, но Consensys готовится к IPO.

Согласно сообщению Axios, в октябре 2025 года Consensys привлекла J.P. Morgan и Goldman Sachs в качестве консультантов по IPO, цель — выход на биржу уже в этом году. В случае успеха это будет первая компания, глубоко связанная с核心 инфраструктурой Ethereum, вышедшая на американский фондовый рынок.

Но в том же году, когда привлекли инвестиционный банк, Consensys прошла как минимум через два раунда сокращений.

В октябре 2024 года уволила 20% сотрудников, около 160 человек,理由 генеральный директор Джо Любин назвал макроэкономическое давление и регуляторную неопределённость. В середине 2025 года прошёл ещё один раунд, на этот раз формулировка сменилась на «стимулирование прибыльности».

В известном зарубежном сообществе для поиска работы Glassdoor отзывы сотрудников выглядят хуже, чем сами сокращения.

Кто-то написал, что компания сокращает как минимум два раза в год, увольняют только рядовых сотрудников, руководство никогда. Другой сказал, что после того, как поделился с начальником своими карьерными aspirations, в следующем списке на сокращение оказалось своё имя.

Неизвестно, сколько в этих отзывах эмоций, а сколько фактов. Но то, что компания перед冲刺 к IPO大幅 сокращает штат, одновременно с этим боевой дух сотрудников падает до дна, — это само по себе сигнал.

Затем история с токеном MASK.

В 2021 году Любин в твиттере написал «Wen $MASK?», сообщество всколыхнулось. В 2022 году он further объяснил, что планирует сделать токен и DAO, продвигать «постепенную децентрализацию». В мае 2025 года Финлей в интервью The Block на вопрос о том, когда появится токен, ответил: может быть.

Для пользователей токен MASK — это морковка, висящая впереди, заставляющая продолжать использовать, продолжать взаимодействовать, продолжать贡献 данные из блокчейна для MetaMask. Для Consensys токен — это козырь, который ещё не разыграли перед IPO.

Выпустишь рано — разбавишь叙事 оценки, выпустишь поздно — сообщество потеряет терпение. Сейчас сооснователь ушёл, токен ещё не выпущен, а IPO уже на подходе.

Конкурентоспособность продукта MetaMask снижается, эту тенденцию в краткосрочной перспективе трудно逆转. Но узнаваемость бренда MetaMask сохраняется,那个 оранжевый лисёнок по-прежнему самый узнаваемый крипто-логотип в мире.

Скорость衰减品牌ной ценности и продуктной ценности разная, бренд衰减 медленнее.

Для криптокомпаний зачастую на IPO продают не продукт, а бренд плюс叙事. «Инфраструктура Ethereum», «вход в Web3», «крупнейший в мире некастодиальный кошелёк»... Эти ярлыки несколько лет назад всё ещё хорошо смотрелись в презентациях для питчей. Сам Любин является сооснователем Ethereum, этот статус перед传统 инвесторами обладает自带 ореолом.

Поэтому выбор Consensys таков: пока бренд ещё стоит денег, пока регуляторное окно ещё открыто, пока Уолл-стрит ещё испытывает энтузиазм к криптоинфраструктуре, упаковать MetaMask в оболочку публичной компании и позволить公开市场 оценить её.

Молчание — не золото

На уход сооснователя Финлея в圈里 CT (Crypto Twitter) отреагировали спокойно. Не было прощальных длинных постов, заполонивших ленту, не было感慨ций вроде «конец эпохи», большинство甚至 не интересовалось этой новостью.

Тема прихода и ухода сооснователя Metamask по热门 даже不如 какой-нибудь KOL, жалующийся на сокращение сувениров на конференции в Гонконге.

Это само по себе кое о чём говорит.

MetaMask — редкий案例 в криптоиндустрии. Она обладает крупнейшим брендом в этой отрасли,но её основатели几乎 не имеют личного бренда.

В отрасли, где основатель является最大的营销资源ом, два основателя MetaMask выбрали невидимость. Продукт говорил за них, пока продукт не смог больше говорить.

Автор считает, что история MetaMask по сути является историей о «значении по умолчанию».

В технологической индустрии стать选项ом по умолчанию — это самое мощное конкурентное преимущество и самый опасный наркотик. Когда ты вариант по умолчанию, рост пользователей не требует от тебя никаких действий, он приходит сам.

Но этот рост маскирует тот факт, что сам продукт стареет. Когда ты обнаруживаешь, что пользователи уходят, уход往往 уже длится давно.

IE был браузером по умолчанию, проиграл Chrome. Nokia была телефоном по умолчанию, проиграла iPhone.

Windows Media Player был проигрывателем по умолчанию, проиграл всем. Когда эти продукты проиграли, их доля рынка была ещё высока, узнаваемость бренда всё ещё сильна, но новые пользователи уже их не выбирали.

MetaMask сейчас находится на этой позиции. Пользователи存量 ещё есть, бренд ещё громкий, но прирост уже ушёл в другие места. План IPO от Consensys, в конечном счёте, заключается в монетизации存量.

На этапе, когда品牌ная ценность выше продуктной, продавать — действительно рациональный выбор.

В день ухода Финлея MetaMask как раз запустила новую функцию расширенных разрешений под названием ERC-7715. Он сказал, что с нетерпением ждёт возможности体验 её в качестве обычного пользователя в будущем.

Создатель продукта становится его обычным пользователем — это, пожалуй, самое простое и тихое прощание в криптоиндустрии.

Но для MetaMask, сколько обычных пользователей будут点击 на того лисёнка каждый день в следующем году? Ты всё ещё используешь его?