Автор: Stablecoin Insider / McKinsey×Artemis

Компиляция: Deep Tide TechFlow

Введение от Deep Tide: Совместный отчет McKinsey и Artemis сделал то, что редко делают в индустрии: разобрали данные об объеме транзакций стейблкоинов по косточкам. Вывод: из примерно 35 трлн долларов ежегодного объема ончейн-транзакций только около 390 млрд долларов (примерно 1%) являются реальными платежными операциями, причем 58% из них — это операции корпоративных финансов между предприятиями, с годовым ростом на 733%. Использование стейблкоинов конечными потребителями практически ничтожно, и это не случайность — в статье归纳了 пять структурных причин, объясняющих, почему пропасть между институциональными и розничными пользователями — это не просто временное отставание.

Полный текст ниже:

У индустрии стейблкоинов есть проблема на уровне заголовков.

С одной стороны, сырые ончейн-данные показывают, что ежегодно в блокчейнах перемещаются триллионы долларов. Эта цифра порождает бесконечные сравнения с Visa, Mastercard и прогнозы о скором замещении SWIFT.

С другой стороны, знаковый отчет McKinsey & Company и Artemis Analytics, опубликованный в феврале 2026 года, очистил все это и задал более прямой вопрос: какая часть из этого является реальными платежами?

Ответ — примерно 1%.

Из примерно 35 трлн долларов годового объема транзакций стейблкоинов только около 390 млрд долларов представляют собой настоящие платежи конечных пользователей, такие как оплата счетов поставщиков,跨境 переводы, выплата заработной платы и оплата картой. Остальное — это торговая активность, внутреннее перемещение средств, арбитражные операции и автоматизированные циклы смарт-контрактов.

В отчете делается вывод, что раздутые заголовочные цифры должны быть «отправной точкой для анализа, а не прокси-показателем для оценки уровня принятия платежей».

Но внутри этого реального базового уровня в 390 млрд долларов есть история, которая заслуживает более глубокого изучения, и она почти полностью вращается вокруг корпоративных финансов, а не кошельков потребителей.

B2B доминирует: что на самом деле говорят данные

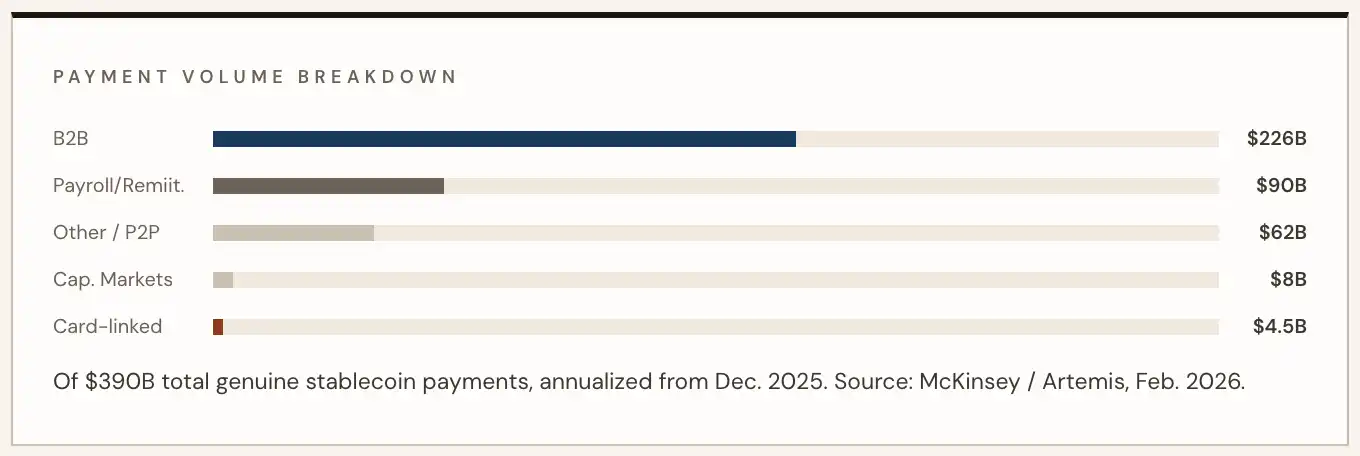

Согласно анализу McKinsey/Artemis (основанному на данных об активности за декабрь 2025 года), транзакции между предприятиями (B2B) составляют 226 млрд долларов от всех реальных платежных объемов стейблкоинов, или около 58%.

Эта цифра представляет собой рост на 733% в годовом исчислении, обусловленный в основном платежами в цепочках поставок,跨境 расчетами с поставщиками и управлением финансовой ликвидностью. Азия лидирует по географической активности, но внедрение также ускоряется в Латинской Америке и Европе.

Остальная часть реального платежного пространства распределена между выплатой заработной платы и денежными переводами (90 млрд долларов), расчетами на рынках капитала (8 млрд долларов) и оплатой с привязанных карт (4.5 млрд долларов).

По данным McKinsey, объем оплаты с привязанных к стейблкоинам карт вырос на惊人的 673% в годовом исчислении, но в абсолютном выражении он по-прежнему составляет лишь небольшую часть B2B-потока.

Для справки: этот общий объем в 390 млрд долларов составляет лишь 0.02% от более чем 2 квадриллионов долларов общих ежегодных全球 платежей, по оценкам McKinsey. Конкретно B2B-поток стейблкоинов составляет около 0.01% от全球 рынка B2B-платежей в 160 трлн долларов.

Эти цифры велики в контексте стейблкоинов, но仍微乎其微 в контексте全球 финансовой системы.

Данные о ежем объеме (monthly Run Rate)更直观地 показывают, где находится импульс. Согласно данным, приведенным BVNK со ссылкой на отчет McKinsey/Artemis, в январе 2024 года ежемесячный объем платежей стейблкоинами составлял всего 5 млрд долларов; к началу 2026 года эта цифра превысила 30 млрд долларов — шестикратный рост менее чем за два года, причем наиболее крутой рост пришелся на вторую половину 2025 года.

В годовом исчислении этот темп如今 превышает 390 млрд долларов.

«То, что реальные платежи стейблкоинами значительно ниже обычных оценок, не умаляет долгосрочный потенциал стейблкоинов как платежного рельса, это лишь устанавливает более четкий базовый уровень для оценки текущего положения рынка». — McKinsey/Artemis Analytics, февраль 2026 г.

Почему существует разрыв: пять структурных сил, исключающих розницу

Расхождение между взрывным внедрением в B2B и ничтожным объемом использования потребителями — не совпадение, а продукт структурной асимметрии, которая систематически благоприятствует корпоративным кейсам использования, а не розничным.

Вот пять сил, движущих институциональный разрыв:

1) Финансовая эффективность побеждает удобство для потребителя

Корпоративных финансовых директоров движут конкретные, измеримые болевые точки: цепочки банков-корреспондентов SWIFT, расчеты по которым занимают от одного до пяти рабочих дней, окна конвертации валют, связывающие оборотные средства, и комиссии посредников, накладываемые на каждом этапе сделки.

Стейблкоины решают все три проблемы одновременно. Для компании, которая платит поставщикам в пятнадцати странах, экономический расчет очевиден; для потребителя, покупающего кофе — нет. Стимулы для переключения на корпоративной стороне на порядки больше, чем для индивидуального пользователя.

2) Программируемость не имеет эквивалентной ценности в рознице

Взрывной рост B2B — отчасти история программируемых платежей. Смарт-контракты реализуют условную логику — триггеры по счетам, подтверждение доставки, релиз эскроу — что позволяет автоматизировать весь процесс кредиторской задолженности в масштабе.

Это естественно подходит для операций корпоративных финансов, поскольку процессы structured, повторяющихся платежей с высокой стоимостью greatly выигрывают от автоматизации. Розничным платежам не хватает类似 сценариев применения триггеров в любом масштабе.

Потребителям не нужны программируемые условия для покупки продуктов, им нужно что-то, что работает как карта. Когнитивная сложность нативных блокчейн-платежей по-прежнему является барьером на розничном конце, и программируемость здесь не помогает.

3) Нормативная архитектура смещена в пользу институтов

После принятия «Закона GENIUS» институциональные операторы адаптировали compliance-архитектуру под требования AML/CFT, правила Travel Rule, лицензионные требования и建立了 юридическую инфраструктуру, позволяющую уверенно работать.

У команд корпоративных финансов есть专职 функции compliance, способные поглотить friction входа; индивидуальные потребители — нет. В результате в большинстве юрисдикций каналы онбординга для розничных пользователей операционно остаются сложными, а разрыв в принятии мерчантами сохраняется в全球 масштабе.

Каждый бесфрикционный B2B-платеж сегодня — это точка данных, которую институты используют для обоснования дальнейших инвестиций; а потребительская экосистема ждет появления compliant, плавного входа, который еще не появился в массовом масштабе.

4) Преимущество закрытого цикла

Успех B2B-платежей стейблкоинами обусловлен именно тем, что это закрытый цикл: предприятие отправляет предприятию, у обеих сторон есть кошельки, compliance-инфраструктура, и ни одной из них не нужна общая сеть мерчантов.

Потребительские платежи сталкиваются с классической проблемой курицы и яйца: мерчанты не будут инвестировать в инфраструктуру приема стейблкоинов, пока не будет спроса со стороны потребителей; а потребители не будут активировать кошельки, пока не смогут широко тратить.

Институциональный мир полностью обошел эту проблему, работая в двусторонних или альянсных средах, без какой-либо открытой сети мерчантов.

5) Стимулы институтов направлены вверх по течению

Корпоративные финансовые директора, держащие стейблкоины, получают доходность, снижают валютные риски, улучшают управление ликвидностью — эти преимущества накапливаются внутри, а их распределение вниз по течению introduces сложность или конкурентную уязвимость.

Расширение использования стейблкоинов до поставщиков поставщиков, сотрудников или конечных потребителей требует построения сети, которая приносит пользу этим downstream сторонам, что не обязательно является выгодой для инициирующей финансовой команды.

При отсутствии явной ROI, заставляющей сеть расширяться вовне, предприятия рационально выбирают консолидацию внутренних выгод.

Контекст рынка

Собственные инфраструктурные данные BVNK с точки зрения оператора подтверждают доминирование B2B. В 2025 году компания обработала 30 млрд долларов годового объема платежей стейблкоинами, что в 2.3 раза больше, чем годом ранее, причем треть объема пришлась на рынок США.

Ее список клиентов (Worldpay, Deel, Flywire, Rapyd, Thunes) — это лидеры в области跨境 B2B-инфраструктуры и инфраструктуры выплаты зарплат, а не потребительских приложений.

Как отметила BVNK в своем обзоре по итогам 2025 года:

«Исходное предположение, что денежные переводы и потребительские трансферы будут引领 первоначальный рост стейблкоинов, не стало основным драйвером; эту роль взял на себя B2B».

Когда розница догонит — если вообще догонит

Базовый уровень McKinsey/Artemis позволяет четко увидеть текущее положение. Что он не может ответить, так это то, сузится ли институциональный разрыв, расширится или permanently закрепится.

Вот три возможных сценария на ближайшие 18 месяцев:

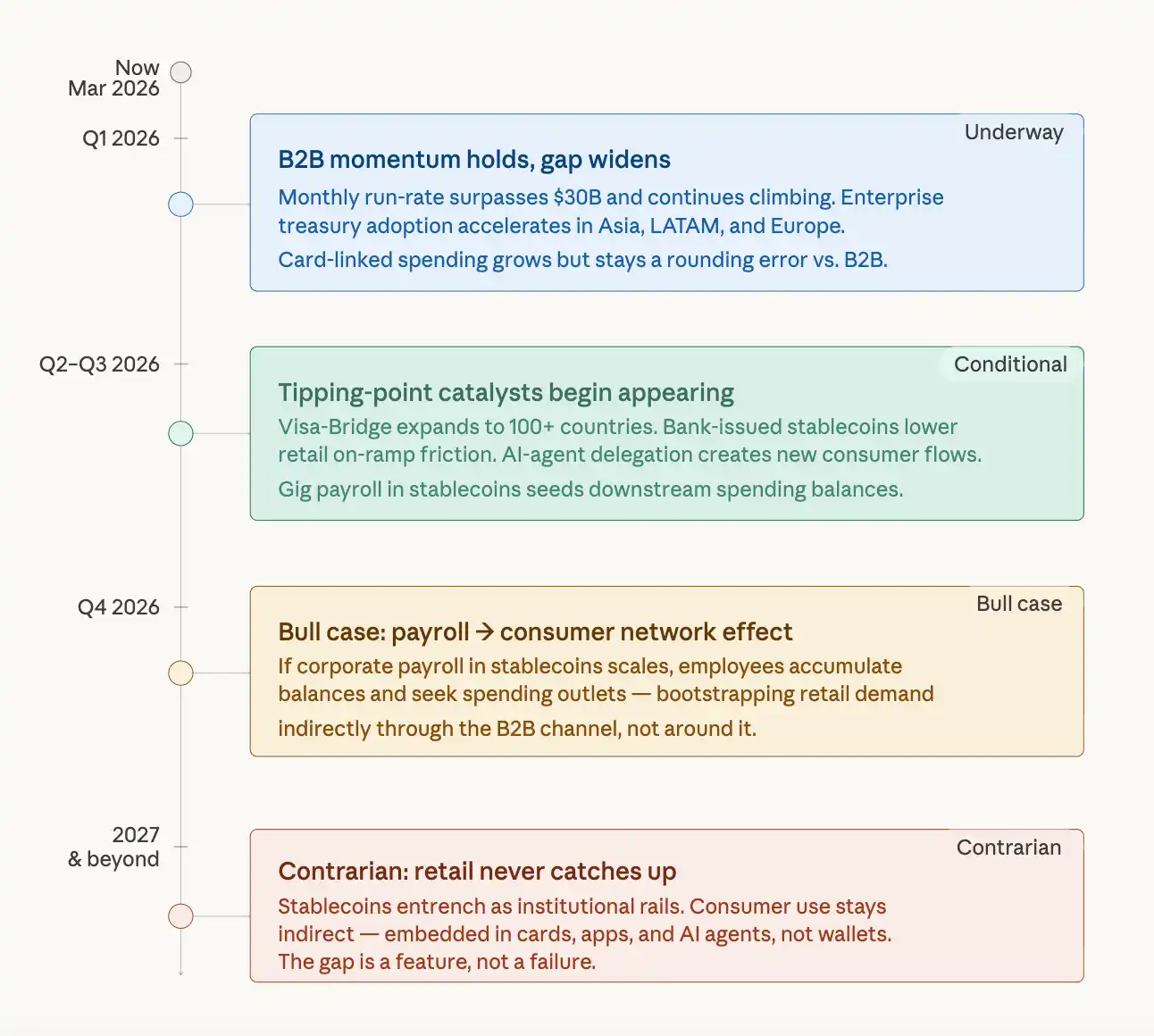

Ближайший период, 2026 г. — разрыв увеличивается

Импульс B2B не показывает признаков замедления. Ежемесячный объем свыше 30 млрд долларов продолжает тренд по мере того, как все больше предприятий используют стейблкоин-рельсы для跨境 кредиторской задолженности и финансовых операций. Потребительские платежи стейблкоинами с карт незначительно растут, но в абсолютном выражении остаются ничтожными по сравнению с B2B-потоком. Даже если розничное внедрение медленно продвигается в процентах, разрыв в абсолютных долларах увеличивается.

Среднесрочный период, конец 2026 — 2027 гг. — начинают появляться точки перелома

Несколько катализаторов могут начать сокращать разрыв: выпуск банками мультивалютных стейблкоинов снижает трение при входе для розницы; программируемые функции延伸至 потребительских приложений через делегирование платежей AI-агентам; выплата заработной платы в стейблкоинах в гиг-экономике создает у сотрудников балансы для downstream трат.

Министр финансов США Скотт Бессент预测, что объем предложения стейблкоинов к 2030 году может достичь 3 трлн долларов, и эта траектория предполагает, что в конечном итоге появятся сетевые эффекты для потребителей.

Обратная точка зрения — розница может никогда не "догнать", и, возможно, в этом и есть суть

Самое честное прочтение данных McKinsey заключается в том, что стейблкоины, возможно, эволюционируют в то, о чем в отчете намекается: программируемый расчетный уровень в интернете для машин, финансовых отделов и институтов, где потребительское принятие является косвенным, встроенным受益тием, а не основным случаем использования.

Если эта рамка верна, то институциональный разрыв — это не провал внедрения, а особенность естественной архитектуры технологии. Выплата корпоративной заработной платы в стейблкоинах может в конечном итоге создать downstream потребительские расходы, но путь от B2B-инфраструктуры к розничным кошелькам долог и извилист и зависит от прорывов в пользовательском опыте, которые еще не появились в массовом масштабе.

Честный базовый уровень

Отчет McKinsey/Artemis сделал нечто более ценное, чем фиксация роста стейблкоинов: он установил честный базовый уровень, которого индустрии явно не хватало.

Очистка от торгового шума, внутреннего перемещения и автоматизированных циклов смарт-контрактов reveals действительно растущий платежный рынок — реальный объем платежей с 2024 по 2025 год удвоился — но он структурным, неслучайным образом highly сконцентрирован на институциональном конце.

Рост B2B на 733% — это не отложенная потребительская история, а созревающая финансовая история.

Предприятия, строящие сегодня на стейблкоин-рельсах, решают реальные операционные проблемы —跨境 трения, неэффективность банков-корреспондентов, задержки оборотного капитала — которые не имеют никакого отношения к тому, есть ли у потребителей стейблкоин-кошельки. Они будут продолжать строить в любом случае.