Автор: David, Deep Chao TechFlow

Сегодня появилась новость: Polygon уволил около 30% сотрудников.

Хотя официального заявления от Polygon не было, CEO Marc Boiron в интервью подтвердил увольнения, добавив, что благодаря новым приобретенным командам общая численность персонала останется стабильной.

В соцсетях также появились посты от уволенных сотрудников, что косвенно подтверждает этот факт.

Но на той же неделе Polygon объявил о покупке двух компаний за 2,5 миллиарда долларов. С одной стороны увольняют, с другой тратят большие деньги — не странно ли это?

Если бы это была простая оптимизация, они бы не тратили 2,5 миллиарда на покупки. Если бы это было расширение, они бы не увольняли 30% персонала. Если рассматривать эти два события вместе, это больше похоже на замену кадров.

Увольняют людей с прежних направлений бизнеса, освобождая места для новых приобретенных команд.

2,5 миллиарда потрачены на лицензии и платежные каналы

Приобретенные компании — Coinme и Sequence.

Coinme — это старая компания, основанная в 2014 году, которая создает каналы для обмена фиата и криптовалют, управляет криптобанкоматами в более чем 50 000 торговых точек США. Её самый ценный актив — лицензии, она имеет лицензии на перевод денег в 48 штатах. В США их очень сложно получить, таким компаниям как PayPal и Stripe потребовались годы, чтобы собрать полный комплект.

Sequence занимается инфраструктурой кошельков и межсетевой маршрутизацией. Проще говоря, это позволяет пользователям не заботиться о таких сложностях, как мосты или замена газа, и осуществлять межсетевые переводы в один клик. Её клиенты включают Polygon, Immutable, Arbitrum и другие сети, также у них есть партнерство по дистрибуции с Google Cloud.

Две сделки обошлись в 2,5 миллиарда долларов. Polygon назвал это «Open Money Stack», позиционируя как промежуточное ПО для платежей стейблкоинами, которое они хотят продавать банкам, платежным компаниям, денежным переводам и другим B2B-клиентам.

Я понимаю логику так:

Coinme предоставляет лицензированные каналы для ввода/вывода фиата, Sequence предоставляет удобные кошельки и межсетевые возможности, а собственная сеть Polygon обеспечивает уровень расчетов. Собрав эти три части вместе, получается полная инфраструктура для платежей стейблкоинами.

Вопрос в том, зачем Polygon?

На пути L2 Polygon уже трудно продвигаться

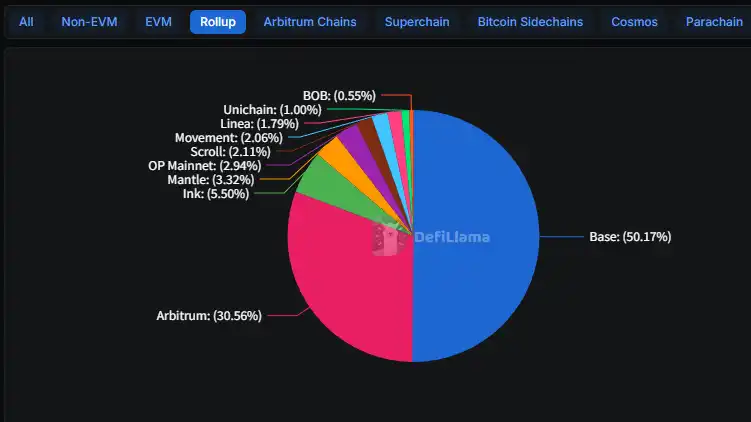

Ситуация в 2025 году ясна: Base победил.

Этот L2 от Coinbase вырос с TVL в 3,1 миллиарда долларов в начале прошлого года до 5,6 миллиарда, заняв 50% всего рынка L2. Arbitrum удержал 30%, но практически не рос. Оставшиеся десятки L2 после раздачи эирдропов в основном остались не у дел.

В чем выиграл Base? У Coinbase более 100 миллионов зарегистрированных пользователей, любая новая функция продукта сразу привлекает пользователей.

Например, депозиты в протоколе кредитования Morpho на Base выросли с 354 миллионов долларов в начале прошлого года до 2 миллиардов сейчас, главным образом потому, что он был интегрирован в приложение Coinbase. Пользователи могут использовать его прямо в приложении, им даже не нужно знать, что такое L2 или Morpho.

У Polygon нет такого входа. В 2024 году они уже проводили увольнения, тогда уволили 20%, это было сокращение на медвежьем рынке, все тогда урезали штат.

На этот раз всё иначе: деньги в казне есть, но всё равно увольняют, что говорит о сознательной смене направления.

Помните, раньше Polygon рассказывал историю о корпоративном внедрении: акселератор с Disney, программа NFT-членства Starbucks, чеканка в Instagram от Meta, аватары Reddit и т.д.

Прошло четыре года, большинство из этих合作 (сотрудничеств) заглохли. Программа Odyssey от Starbucks тоже закрылась в прошлом году.

Продолжать напрямую бороться с Base на поле L2 у Polygon почти нет шансов на победу. Технологический разрыв можно нагнать, точку входа для пользователей — нет. Вместо того чтобы задерживаться на проигранном поле боя, лучше поискать новые возможности.

Платежи стейблкоинами — хорошее направление, но переполненное

Рынок платежей стейблкоинами действительно растет.

В 2025 году общая рыночная капитализация стейблкоинов превысила 3000 миллиардов долларов, что на 45% больше, чем годом ранее. Сфера использования также меняется: с первоначального арбитража на биржах до трансграничных платежей, корпоративных финансов, выплаты зарплат и других сценариев.

Но этот рынок уже переполнен.

Stripe в прошлом году потратила 1,1 миллиарда долларов на покупку инфраструктурной компании для стейблкоинов Bridge, а недавно получила право на выпуск стейблкоина USDH на Hyperliquid. PYUSD от PayPal уже занимает 7% доли стейблкоинов на Solana.

Circle сама продвигает Payments Network. JPMorgan, Wells Fargo, Bank of America и другие крупные банки формируют альянс для выпуска собственных стейблкоинов.

Основатель Polygon Sandeep Nailwal в интервью Fortune сказал, что это приобретение ставит Polygon в положение конкурента Stripe.

Честно говоря, это громкое заявление.

Stripe потратила на приобретение 1,1 миллиарда, Polygon — 2,5 миллиарда. У Stripe миллионы merchants (торговцев), клиенты Polygon в основном разработчики. Самое главное, Stripe积累了 (накапливала) лицензии на платежи и банковские связи более десяти лет.

В лобовом столкновении это противники разного масштаба.

Но Polygon, возможно, делает ставку на другую тактику. Stripe хочет встроить стейблкоины в свой закрытый контур, чтобы merchants (торговцы) по-прежнему использовали Stripe, но уровень расчетов стал бы стейблкоинами, быстрее и дешевле.

Polygon хочет создать открытую инфраструктуру, чтобы любой банк или платежная компания могли строить на ней свой бизнес.

Один — вертикальная интеграция, другой — горизонтальный вход. Эти две модели не обязательно конкурируют напрямую, но борются за внимание одних и тех же клиентов.

Смена стратегии, будущее неопределенно

В конечном счете, за последние два года увольнения в криптоиндустрии не редкость.

OpenSea сократила 50%, Yuga Labs, Chainalysis — все оптимизируются. ConsenSys уволила 20% в прошлом году, и снова в этом. В основном это вынужденные сокращения, денег в казне нет, нужно сначала выжить.

С Polygon всё иначе. Деньги в казне есть, могут выделить 2,5 миллиарда на покупки, но всё равно выбирают уволить 30% персонала.

Замена кадров, смена стратегии выживания, но в этом есть риск.

Приобретенная Polygon компания Coinme, основной бизнес — криптобанкоматы, установленные в более чем 50 000 торговых точек по всей Америке, позволяющие пользователям покупать монеты за наличные и обменивать монеты на наличные.

Проблема в том, что в прошлом году в этом бизнесе случился инцидент.

Регуляторы Калифорнии оштрафовали Coinme на 300 000 долларов за то, что её банкоматы позволяли пользователям превышать лимит снятия, нарушая установленный дневной лимит в 1000 долларов. В штате Вашингтон поступили жестче, введя запрет, который был снят только в декабре прошлого года.

CEO Polygon говорил, что соответствие Coinme требованиям «превышает нормы». Но регуляторные штрафы — это факт черным по белому, красивые слова этого не изменят.

Если соотнести эти события с токеном, то нарратив токена $POL также изменится.

Раньше чем больше использовали сеть, тем ценнее был POL. После приобретения, Coinme берет комиссию с каждой транзакции — это реальный доход, а не нарратив токена. Официально заявляют, что ожидают объем более 100 миллионов долларов в год.

Если это действительно удастся, Polygon может превратиться из «протокола» в «компанию» с доходами, прибылью и точкой锚да оценки. Это редкий вид в криптоиндустрии.

Однако скорость входа традиционных финансов явно ускоряется, и окно возможностей для нативных криптокомпаний сужается.

В индустрии есть поговорка: на медвежьем рынке строят, на бычьем — пожинают плоды.

Проблема Polygon сейчас в том, что он всё еще строит, но собирать урожай на бычьем рынке, возможно, будет уже не ему.