Автор оригинала:Raoul Pal, CEO Real Vision и GMI

Перевод: CryptoLeo(@LeoAndCrypto)

Сегодня утром CEO Real Vision и GMI (инвестиционной библии Рауля Пала) Рауль Пал опубликовал статью «Ложные нарративы... и другие мысли», в которой с помощью сравнения данных и макроанализа объяснил недавний спад и кризис в криптоиндустрии, заявив, что зимний период скоро закончится, и призвал сохранять терпение и не терять веру в отрасль. Odaily Planet Daily перевел ее следующим образом:

Это были выводы, которые я сделал для GMI на выходных, надеюсь, они придадут вам уверенности. Обычно я оставляю такие материалы для обсуждения в GMI и Pro Macro, но я знаю, что вам всем это нужно, чтобы расслабить напряженные нервы.

Основной нарратив: Криптовалюта закончилась?

Основное мнение заключается в том, что биткоин и криптовалюты рухнули, этот цикл завершен, все кончено, ничего не будет как раньше. Криптовалюты оторвались от других активов, это вина CZ, вина BlackRock и т.д. Это, несомненно, заманчивая нарративная ловушка, особенно когда цены на основные монеты падают каждый день.

Но вчера один хедж-фонд клиент GMI прислал мне сообщение, спрашивая, стоит ли покупать акции SaaS на падении, или, как все сейчас говорят, Claude Code уже уничтожил индустрию SaaS.

Поэтому я начал исследовать SaaS и в процессе обнаружил, что полученные выводы опровергают как основной нарратив о биткоине, так и нарратив об индустрии SaaS. Графики SaaS и BTC выглядят одинаково?

Индекс SaaS UBS и динамика биткоина

Это указывает на то, что есть еще один фактор, который все упускают из виду и который влияет на это движение.

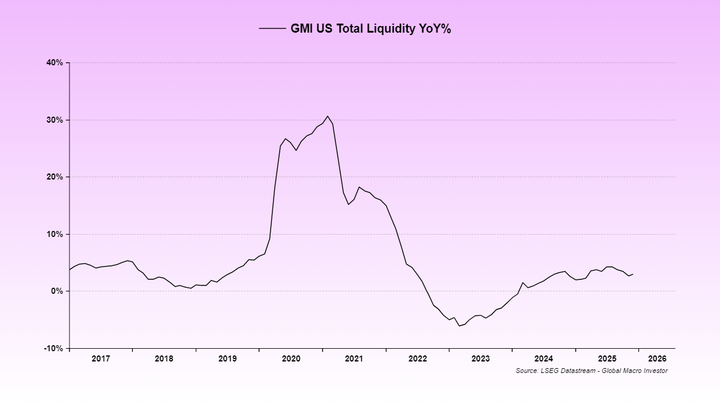

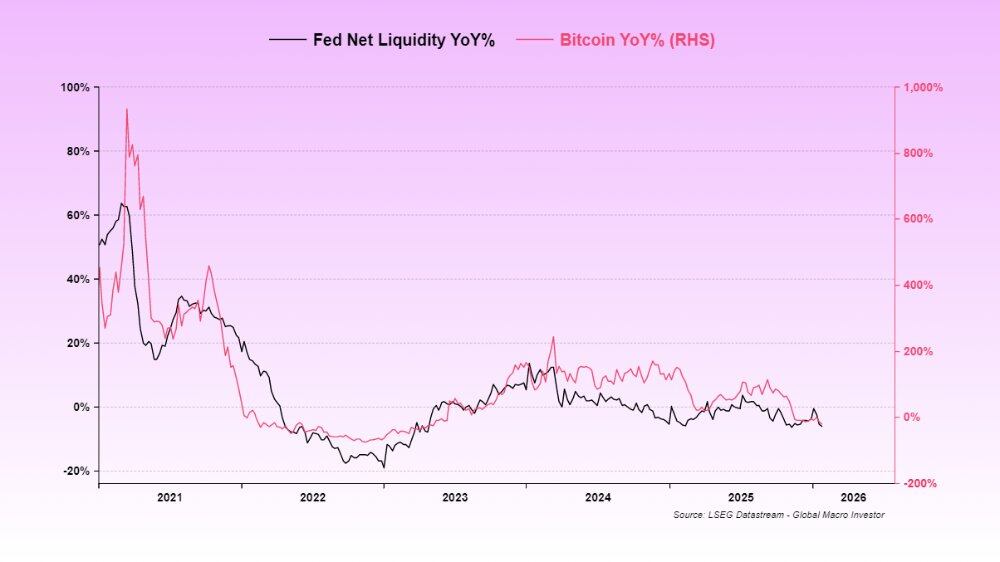

Этот фактор: Из-за двух шатдаунов и проблем с базовой финансовой системой США (механизм обратного выкупа (RRP) фактически был полностью восполнен только в 2024 году) ликвидность в США была подавлена. Таким образом, восстановление TGA (счета Казначейства) в июле и августе не имело соответствующих монетарных компенсирующих мер, что привело к сокращению ликвидности.

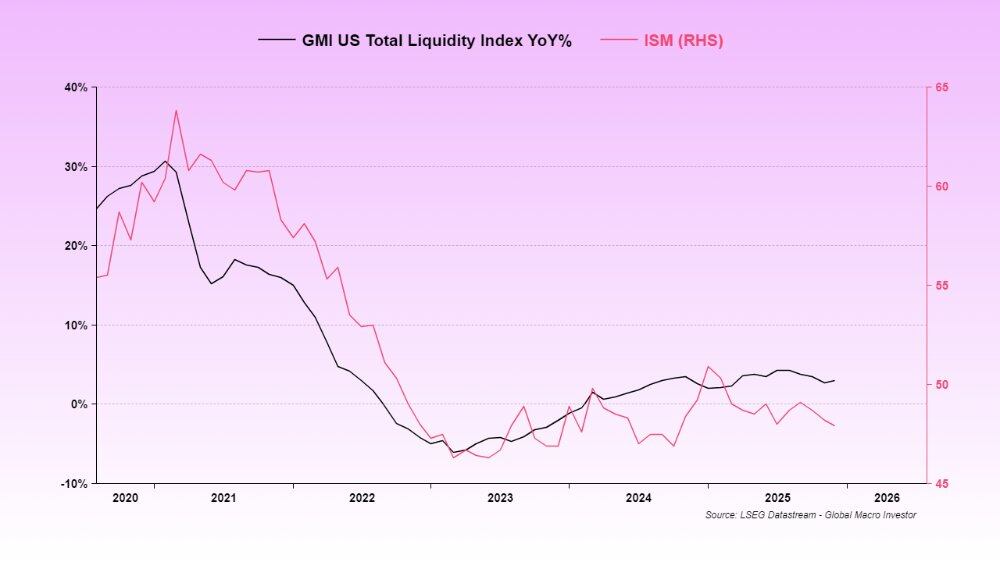

До сих пор низкая ликвидность является причиной того, что индекс деловой активности в обрабатывающей промышленности ISM остается на низком уровне.

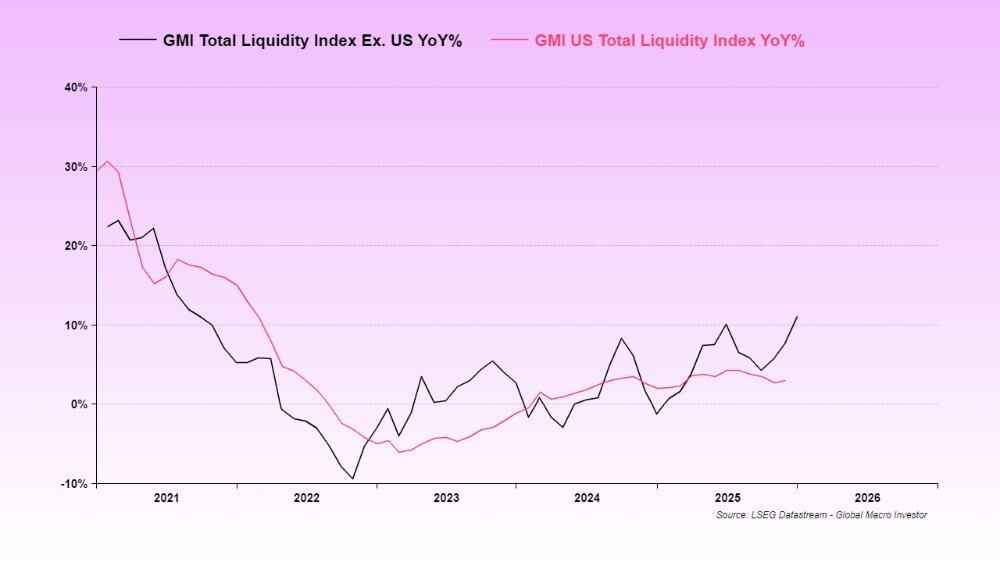

Мы обычно используем показатель глобальной совокупной ликвидности, поскольку он имеет наибольшую долгосрочную корреляцию с BTC и Nasdaq, но на данном этапе американская совокупная ликвидность кажется более важной, поскольку США являются основным поставщиком глобальной ликвидности.

В этом цикле индекс глобальной совокупной ликвидности GMI опережает индекс совокупной ликвидности США и вот-вот начнет восстанавливаться (и, следовательно, поднимет индекс ISM).

Это именно то, что влияет на SaaS и BTC. Оба этих актива являются самыми долгосрочными из существующих, и оба упали из-за временного оттока ликвидности.

Рост золота基本上 забрал маржинальную ликвидность, которая в противном случае могла бы поступить на рынки биткоина и SaaS, в системе не хватило ликвидности для поддержки этих активов, поэтому высокорисковые активы пострадали и упали, ничего не поделаешь.

Сейчас правительство США снова остановлено, и Министерство финансов приняло превентивные меры: после последнего шатдауна они не использовали никакие средства TGA, а наоборот, увеличили размер активов (т.е. ликвидность further уменьшилась). Это кризис, с которым мы столкнулись сейчас, он вызвал резкие колебания цен, и наши любимые криптовалюты по-прежнему испытывают нехватку ликвидности.

Однако все указывает на то, что нынешний правительственный шатдаун будет разрешен на этой неделе, что устранит последнее препятствие для ликвидности.

Прим. Odaily: Спикер Палаты представителей США Майк Джонсон в воскресенье в интервью программе NBC News «Meet the Press» заявил, что, по его мнению, он получил поддержку республиканцев, чтобы обеспечить прекращение шатдауна некоторых government agencies к вторнику.

Я уже多次 упоминал о рисках этого правительственного шатдауна, но он скоро закончится, и тогда мы сможем продолжить dealing с предстоящим вливанием ликвидности, которое включает меры от eSLR, частичный возврат TGA, фискальные стимулы, снижение ставок и т.д., и все это связано с промежуточными выборами.

Прим. Odaily: Законопроект американских регуляторов о смягчении требований к левериджу для облегчения давления на капитал нескольких крупных банков, включая Bank of America (BAC.US).

В полном торговом цикле время часто важнее цены. Цены могут быть повреждены, но со временем, по мере развития цикла, все уладится и в最终一切 устаканится.

Вот почему я всегда подчеркиваю, что нужно «терпение», события должны развиваться,一味关注 прибылями и убытками只会 влиять на ваше психическое здоровье, а не на ваш инвестиционный портфель.

Ложный нарратив о ФРС

Что касается снижения ставок, то существует также ошибочное мнение, что Кевин Уорш является ястребом. Это полная чепуха, в основном эти заявления относятся к 18-летней давности.

Работа и задача Уорша заключалась в выполнении стратегии эпохи Гринспена. И Трамп, и Безос (здесь предположительно опечатка, имелся в виду, вероятно, влиятельный человек, но не Безос; контекст говорит о будущей администрации) говорили (здесь не подробно, но основное направление - снижение ставок), чтобы поддерживать экономику в горячем состоянии, и предполагать, что рост производительности благодаря искусственному интеллекту подавит рост базового ИПЦ (как в эпоху 1995-2000 годов).

Прим. Odaily: Гринспен является одним из самых долгоправящих председателей ФРС в истории, его денежно-кредитная политика (контроль инфляции + содействие максимальной занятости) была highly гибкой, но на деле более антиинфляционной,同时 в кризисы активно вливала ликвидность.

Ему не нравится баланс, но система ограничена резервами, поэтому он, скорее всего, не изменит свою текущую практику, иначе это разрушит кредитные рынки.

Уорш будет снижать ставки и ничего больше не будет делать. Он не будет вмешиваться в действия Трампа и Безоса (см. выше) по управлению ликвидностью через банки. Член совета управляющих ФРС Милан, вероятно, будет настаивать на полном снижении eSLR, чтобы ускорить этот процесс.

Не верите мне, тогда поверьте Друку ↓

На изображении выше: содержание о monetary policy理念 Уорша и его соглашения с Безосом (?) после вступления в должность председателя ФРС от «инвестиционного гуру» Стэнли Дракенмиллера.

Я знаю, как трудно услышать оптимистичный нарратив, когда ситуация с криптой выглядит такой мрачной, мой SUI держится отвратительно, мы не знаем, чему или кому верить. Во-первых, мы много раз проходили через это. Когда BTC падает на 30%, альткоины могут упасть и на 70%. Но если это качественные альты, они и восстановятся быстрее.

Mea Culpa (Моя вина)

Ошибка GMI заключалась в том, что мы не рассматривали американскую ликвидность как текущий драйвер, обычно доминирующим在整个 цикле является глобальная совокупная ликвидность. Но теперь ситуация прояснилась, все возможно.

Они не unrelated. Просто мы не могли предсказать комбинацию событий (исчерпание ликвидности RRP > восстановление TGA > шатдаун правительства > рост золота > сноватый шатдаун) или мы не anticipated их влияние.

Это скоро закончится, и很快 мы сможем вернуться к нормальной работе.

Мы не можем гарантировать, что каждый шаг будет безошибочным (теперь у нас есть более глубокое понимание), и мы по-прежнему очень оптимистично настроены в отношении перспектив на 2026 год, потому что мы понимаем стратегию Трампа/Безоса (?)/Уорша. Эти трое repeatedly говорили нам: нам нужно только слушать и сохранять терпение, в инвестировании на полный цикл время важнее цены.

Если вы не циклический инвестор и у вас нет такой высокой толерантности к риску, это совершенно нормально. У каждого свой стиль, но Джулиен (глава макроисследований GMI) и я не擅长 свинг-трейдинг (нас не волнуют взлеты и падения внутри цикла), но мы проверены и имеем подтвержденные результаты в полном цикле инвестирования, лидируя в отрасли в течение последних 21 года. (Предупреждение: мы тоже ошибаемся, как в 2009 году). Сейчас не время сдаваться, удачи, и давайте достигнем больших результатов в 2026 году.

Подкрепление ликвидности уже в пути!