Автор|Azuma(@azuma_eth)

Рынок продолжает оставаться в упадке, фонды бездействуют, протоколы закрываются, крупные игроки молчат, мелкие инвесторы несут убытки... Кажется, что все в индустрии, сверху донизу, теряют деньги. Но даже в таких холодных рыночных условиях печатные станки некоторых проектов продолжают гудеть.

Свежий пример — Polymarket, который полностью открыл шлюзы для комиссий. После недавнего расширения диапазона комиссий и изменения формулы их расчета (рекомендуем к прочтению: «Жесткий разбор формулы комиссий Polymarket: как появилась экстремальная ставка в 90+%?») способность Polymarket генерировать доход значительно выросла; на момент публикации общий доход проекта от комиссий превысил 24 миллиона долларов, а 2 апреля был установлен рекорд дневного дохода — 1.5 миллиона долларов.

В связи с этим автор заглянул в рейтинг доходов на Defillama, чтобы посмотреть, какие бизнесы продолжают стабильно зарабатывать на медвежьем рынке, и результат оказался довольно неожиданным: основной бизнес и источники дохода проектов в списке были предельно ясны, даже, можно сказать, «просты».

Как показано на рисунках выше,相信大部分深耕加密市场的玩家即便不看答案,也能够猜出其中的大多数名字,可能还很清楚它们到底是做什么的。但当这些名字整齐地摆在一起时,我却突然意识到, основные источники дохода этих прибыльных бизнесов高度趋同,甚至 в основном可以用两个大类进行概括:一是 маржа (спред),二是 транзакционный сбор (комиссия).

首先是 маржа, по сути, это работа «финансового посредника». Ее основная логика заключается в привлечении средств по относительно низкой стоимости и их размещении для получения относительно высокой доходности, используя время для постепенного накопления разницы между доходом и затратами — прибыль такого бизнеса зависит от объема привлеченных средств и продолжительности их размещения. Чем больше объем и дольше срок, тем выше прибыль.

К этой категории относятся такие эмитенты стейблкоинов, как Tether и Circle. Их основной доход формируется за счет процентов, полученных от размещения резервов в таких активах, как казначейские облигации США, а затраты в основном связаны с субсидиями, выплачиваемыми партнерам и пользователям. Разница между ними составляет прибыль. Кредитные протоколы, такие как Aave, также относятся к этой категории — маржа здесь представляет собой разницу между относительно высокой процентной ставкой по займам и относительно низкой ставкой по депозитам. Сюда же относятся и сервисы ликвидноcтного стейкинга (LST), такие как Lido, которые удерживают определенный процент от native-вознаграждений за стейкинг ETH в качестве платы за услугу, что также является маржой.

其次是 транзакционный сбор, этот тип бизнеса проще для понимания: whenever происходит связанная с транзакцией активность (включая создание токенов), субъект бизнеса может «взимать налог» в форме комиссии за каждую операцию — прибыль такого бизнеса зависит от объема single операции и frequency операций. Чем больше объем и выше частота, тем больше прибыль.

Независимо от того, специализируется ли платформа на торговле фьючерсами (Hyperliquid, EdgeX), торговле событиями (Polymarket), торговле мем-токенами (pump.fun, GMGN, Axiom, four.meme), спотовой торговле (Aerodrome, Jupiter, Phantom — основной доход которого comes from комиссий за своп во фронтенде кошелька), или торговле NFT (Courtyard, Fragment — тот факт, что они все еще попали в список, действительно удивителен), их основной источник дохода — это транзакционный сбор.

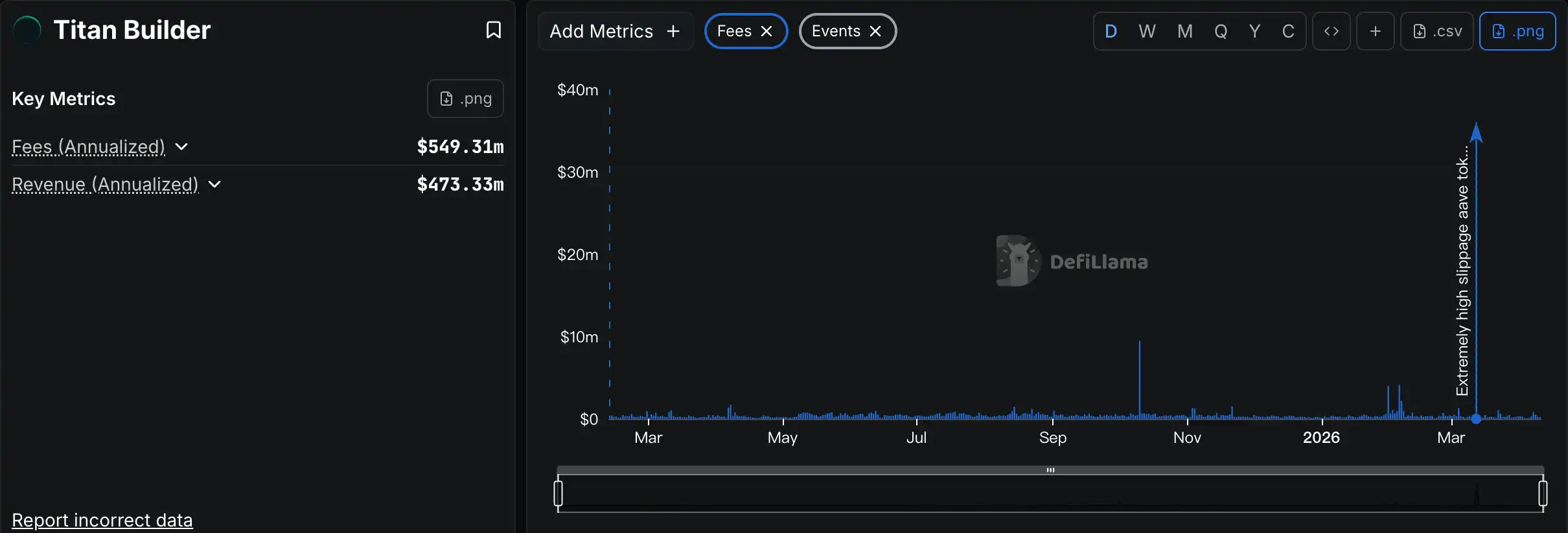

Единственными особыми случаями в рейтинге являются Grayscale, Chanilink и Titan Builder. Grayscale здесь выглядит somewhat странно, ее основной доход comes from управленческих сборов ETF и фондов, по сути, это традиционный бизнес по управлению активами, сфокусированный на криптовалютном рынке. Chanilink же определенно заслуживает упоминания, ее основной доход comes from платы за данные, выплачиваемой проектами за использование оракула (что в определенном смысле также можно отнести к транзакционному сбору), это больше похоже на B2B SaaS-бизнес в блокчейне, но, как вы можете видеть, эффект Матфея на этом пути будет более выраженным, чем в других сегментах. Titan Builder — это чисто случайное явление, это провайдер услуг по построению блоков, в нормальных условиях не считающийся особо прибыльным бизнесом, он попал в список лишь потому, что в прошлом месяце в результате инцидента с сэндвич-атакой на крупную сделку с AAVE Titan Builder получил самый большой кусок (подробнее см. «50 миллионов USDT в обмен на 35 тысяч долларов в AAVE: как произошла катастрофа?»).

Прим. Odaily: вот что значит три года не открывать лавку, а потом за один раз пропитаться на три года.

Таким образом, вывод уже ясен. Проекты, которые продолжают стабильно зарабатывать на медвежьем рынке, — это не те, которые ищут сложные механизмы и высокорискованные возможности, а те, которые могут продолжать работать благодаря простой и понятной модели получения дохода. На все еще нестабильном криптовалютном рынке более простая модель дохода продемонстрировала более высокую устойчивость, лучше выдерживая испытание рыночными колебаниями.

Однако более простая модель дохода отнюдь не означает, что сам бизнес «проще в реализации», как раз наоборот, за простой моделью дохода往往 скрываются более сложные продуктовые услуги и тщательное управление, и именно в этом заключается реальное отличие, которое лидеры рейтинга «вырвали» в конкурентной борьбе. От дизайна взаимодействия до накопления ликвидности, управления рисками и обратной связи с пользователями... Чтобы выделиться в условиях激烈的 конкурентной борьбы на рынке存量, необходимо вкладывать больше усилий в продукт и услуги.

Криптозима еще не закончилась, и проекты, которые действительно могут выжить и даже получать прибыль, — это往往 те, которые гибко сочетают простую модель дохода со сложными продуктовыми услугами. Возможно, в этом и заключается долгосрочный код для прохождения через бычьи и медвежьи рынки.