Goldman Sachs совершил редкий стратегический разворот менее чем за месяц — от активного продвижения концепции HALO инвесторам до прямого шортинга переоцененных компонентных акций, что отражает опасения по поводу перегретости сделок с тяжелыми активами.

Во вторник руководитель группы тематических сделок Goldman Sachs Фарис Мурад в своем последнем отчете представил шорт-корзину GSXUHALT, нацеленную на американские компании с высокой долей активов, но с нулевыми или отрицательными ожиданиями роста прибыли, чьи акции значительно выросли на волне тренда HALO. Goldman Sachs считает, что рыночный ажиотаж вокруг акций тяжелых активов приобрел недифференцированный характер, и рост некоторых отдельных акций серьезно оторвался от фундаментальных показателей.

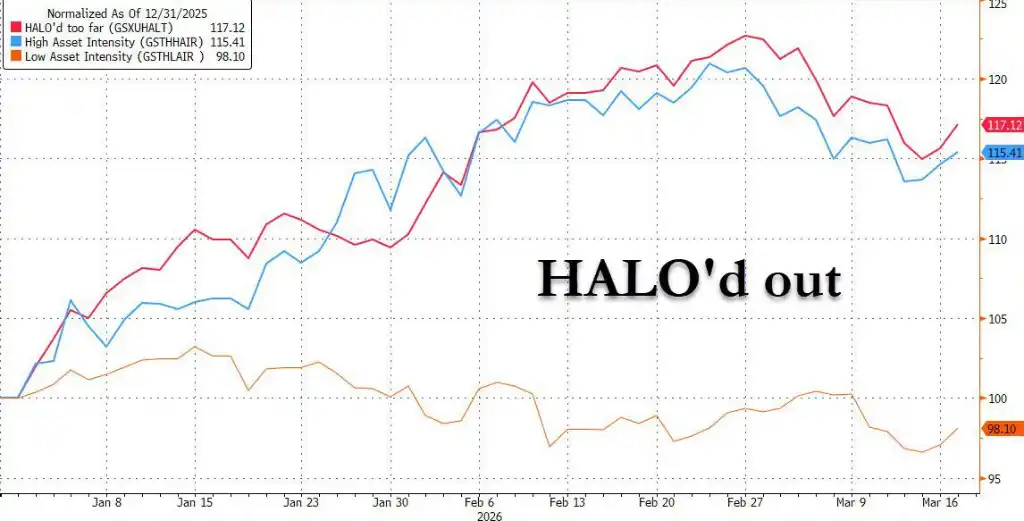

Непосредственное значение этого разворота для рынка заключается в следующем: медовый месяц сделок HALO, возможно, закончился. Данные Goldman Sachs показывают, что корзина GSXUHALT достигла пика в конце февраля и начала снижаться, при этом банк рекомендует инвесторам сочетать эту короткую позицию с предпочитаемыми им тематическими длинными возможностями.

Месяц назад: Goldman Sachs активно продвигает HALO, нарратив о тяжелых активах захватывает Уолл-стрит

Вернемся к 24 февраля. Отдел глобальных инвестиционных исследований Goldman Sachs опубликовал отчет «Эффект HALO: тяжелые активы и низкий уровень устаревания в эпоху ИИ», присоединившись к таким крупным банкам, как JPMorgan, в активном продвижении концепции HALO среди инвесторов — комбинации Heavy Assets (тяжелые активы) и Low Obsolescence (низкий уровень устаревания).

Логика тогда была четкой и убедительной: быстрый рост ИИ оказывает двойное давление на отрасли с легкими активами. С одной стороны, ИИ颠覆ляет ожидания рентабельности в таких отраслях, как программное обеспечение и IT-услуги, и рынок начинает переоценивать их конечную стоимость; с другой стороны, технологические гиганты, чтобы сохранить конкурентное преимущество в вычислительной мощности, запустили беспрецедентный цикл капитальных расходов — по данным Goldman Sachs, ожидается, что CAPEX пяти крупнейших американских технологических компаний в период с 2023 по 2026 год достигнет примерно 1,5 трлн долларов, и только за 2026 год расходы могут превысить 650 млрд долларов, что больше, чем общая сумма за все время до эпохи ИИ.

Данные Goldman Sachs на тот момент также были впечатляющими: с начала 2025 года их портфель тяжелых активов (GSSTCAPI)累计превзошел портфель легких активов (GSSTCAPL) на 35%. На макроуровне более высокие реальные процентные ставки, геополитическая фрагментация и реконфигурация цепочек поставок被认为是共同 создали структурный попутный ветер для акций тяжелых активов.

Резкий разворот: недифференцированная рыночная гонка, рост некоторых акций тяжелых активов потерял фундаментальную поддержку

Однако всего через месяц позиция Goldman Sachs значительно изменилась.

Мурад в своем последнем отчете指出, что компании, входящие в корзину GSXUHALT, — это те, кто рос вместе с общим трендом тяжелых активов, но сами не имеют ожиданий роста прибыли, а доходность显著отстает от высококачественных объектов HALO. Другими словами, рынок, гоняясь за свойством «неподверженности ИИ», без разбора вливал средства во все акции тяжелых активов, не区分их качество.

Данные подтверждают эту оценку: рост корзины GSXUHALT实际上превзошел рост высококачественной корзины с высокой долей активов (GSTHHAIR), что означает, что акции тяжелых активов с низкой доходностью и без роста,反而обогнали真正имеющие конкурентные барьеры аналогичные активы. При этом движение цен этой корзины до конца прошлого года еще保持валосинхронность с ожиданиями прибыли, но затем произошло显著расхождение.

При отборе компонентов для GSXUHALT Goldman Sachs выбрал компании из индекса Russell 1000 с самыми высокими долями активов в своих отраслях, одновременно исключив все активы, связанные с долгосрочными трендами, такими как спутники, роботы, квантовые вычисления и ИИ, и оставив только те акции, которые показали значительный рост с начала года, но имеют持平илисниженные ожидания прибыли. Средний коэффициент密集ности активов в этой корзине составляет около 1,4.

Сигналы оценки: премия за тяжелые активы находится на уровне выше среднего за исторический период

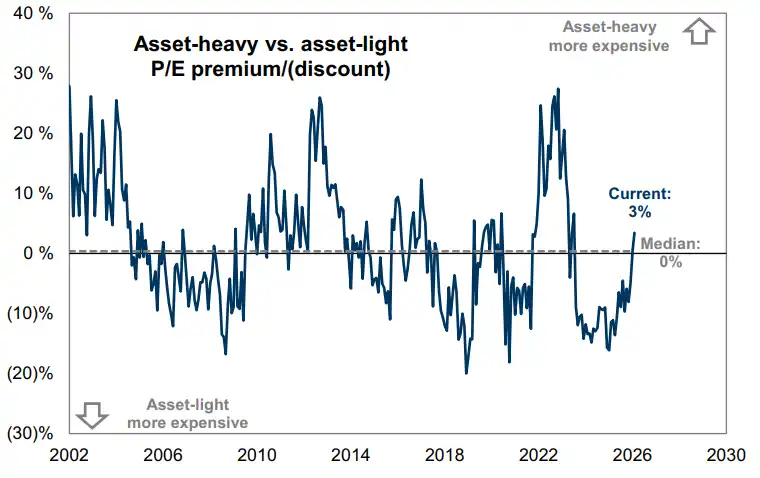

Исследование Goldman Sachs прошлого месяца уже указывало, что акции тяжелых активов в настоящее время торгуются с премией к оценке по отношению к акциям легких активов. По состоянию на прошлый месяц премия к P/E акций тяжелых активов составляла около 3%, что находится на 62-м процентиле за последние десятилетия, и хотя все еще ниже исторических пиков 2004, 2012 и 2022 годов, но уже не является дешевой.

С ноября прошлого года нейтральная к отраслям корзина тяжелых активов Goldman Sachs (GSTHHAIR)累计превзошла корзину легких активов (GSTHLAIR) примерно на 20%. Эта сильная表现тяжелых активов, по мнению Goldman Sachs, коренится в сильном спросе инвесторов на активы, «защищенные от ИИ» — то есть поиск акций материальных активов, которые不易颠覆ляются ИИ и多年来отставали в表现.

Goldman Sachs рекомендует сочетать короткую позицию GSXUHALT с предпочитаемыми банком тематическими длинными возможностями. В отчете指出, что недавняя рыночная коррекция создала крупнейшую с момента «Дня освобождения» возможность «покупки на коррекции» на全球рынках акций, и инвесторы могут, открывая короткие позиции по акциям тяжелых активов без фундаментальной поддержки, одновременно открывать длинные exposureна направлениях, поддерживаемых долгосрочными трендами.

За этим изменением стратегии стоит четкое суждение Goldman Sachs о внутреннейдифференциациисделок HALO: не все акции тяжелых активов заслуживают持有,真正имеющие конкурентные барьеры и восходящий импульс прибыли активы и те отдельные акции, которые лишь используют ярлык «тяжелых активов» для проезда зайцем, подошли к моменту, когда к ним нужно относиться по-разному.