1 марта 2026 года на глобальных макрорынках произошло эпическое событие «черного лебедя»: прямые военные удары США и Израиля по Ирану привели к гибели верховного лидера Ирана Хаменеи.

Это экстремальное событие хвостового риска мгновенно изменило модели премии за риск для глобальных классов активов. Полномасштабное возгорание пороховой бочки Ближнего Востока не только вызвало резкие колебания традиционных активов, таких как сырая нефть и убежища, но и подтолкнуло рынок криптовалют, находящийся в ключевой точке博弈, к перекрестку ликвидности и права ценообразования.

Объединяя данные спотового рынка Binance и данные опционов Deribit, с количественной точки зрения и перспективы博弈 производных инструментов, проводится глубокий анализ немедленного воздействия этого геополитического кризиса на рынок криптовалют, а также перспективный прогноз пути волатильности и направления рынка.

Суть геополитического конфликта заключается в изменении глобальных цепочек поставок, цен на энергоносители и связанных с ними инфляционных ожиданий. Финансовые рынки отреагировали на эту внезапную атаку США и Израиля на Иран по классическому сценарию избегания риска: сырая нефть и золото среди товарных активов стали предпочтительными убежищами, в то время как активы с высоким риском подверглись немедленной бессистемной распродаже.

Высокоинтенсивный конфликт на Ближнем Востоке в первую очередь затрагивает глобальные энергетические цепочки поставок и настроения избегания рисков, связанных с системой доверия к фиатным валютам. На традиционных финансовых рынках Brent crude, вероятно, откроется с гэпом вверх на фоне паники из-за разрыва цепочек поставок, а традиционные убежища, такие как золото, также увидят активное накопление позиций институциональными инвесторами. Однако в сфере криптоактивов нарратив BTC как «цифрового золота» и его свойство «актива с высокой волатильностью и риском» вступают в серьезное внутреннее противоречие.

С точки зрения макроликвидности, паника, вызванная геополитикой (резкий рост индекса VIX), обычно мгновенно провоцирует бессистемную распродажу across asset classes для получения долларовой ликвидности. Но после кратковременного выжимания ликвидности, Bitcoin, не контролируемый конкретными суверенными государствами и обладающий свойствами цензуроустойчивости и портативности, часто привлекает часть капитала, бегущего из рискованных фиатных валют развивающихся рынков.

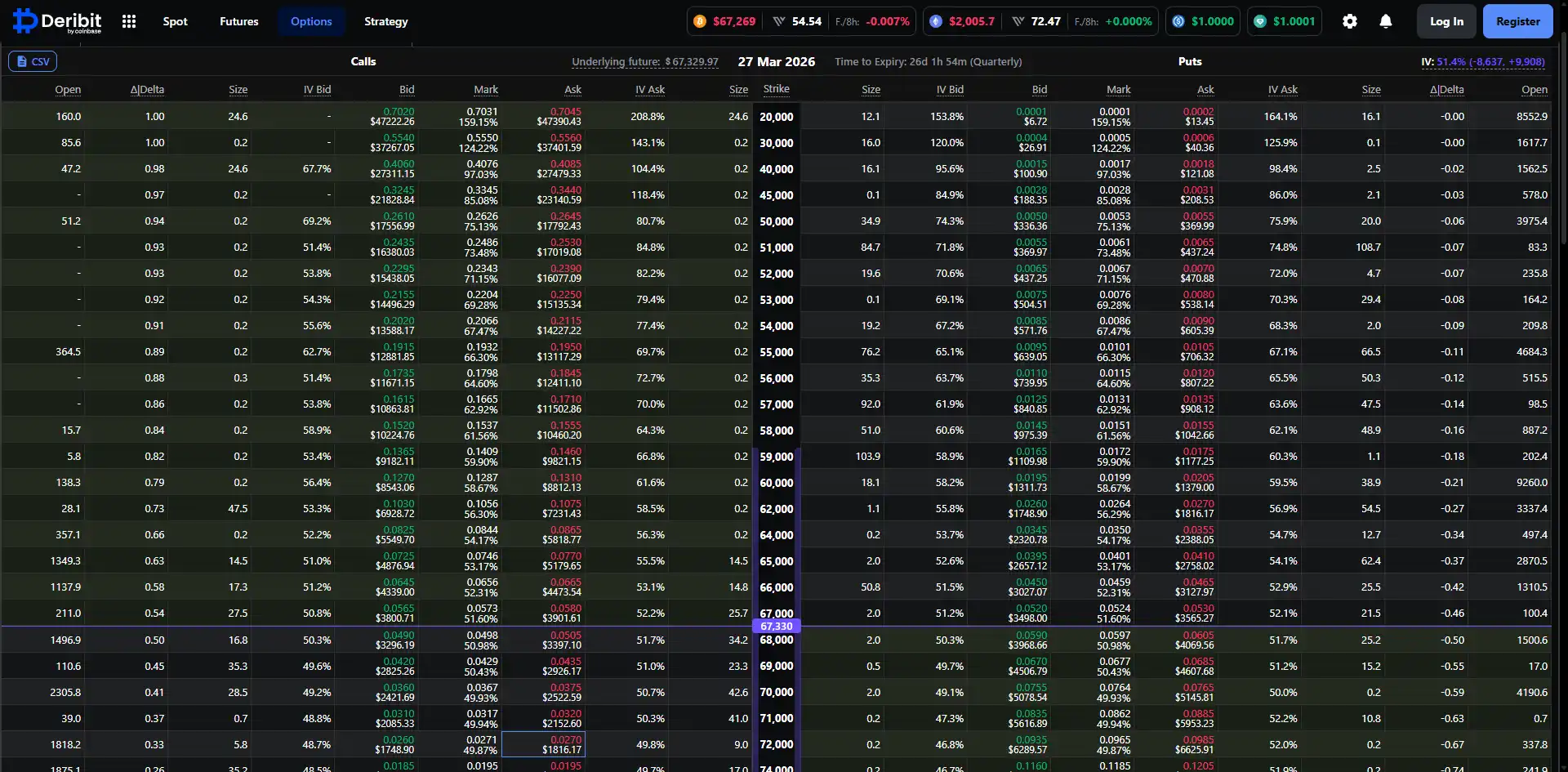

Согласно данным спотового и фьючерсного рынка Binance (по состоянию на 14:00 1 марта 2026 года), спотовая цена BTC/USDT колебалась около 67 392 долларов США. В начале такого масштабного геополитического кризиса BTC не обвалился по образцу «312» 2020 года, а упорно удерживал ключевую поддержку на уровне 67 000 долларов.

Объем торгов за последние 24 часа достиг 1,74 миллиарда долларов США, что указывает на огромные разногласия и смену позиций между быками и медведями на этом уровне. График цен показывает格局 высоких колебаний после формирования бычьего выстраивания скользящих средних, что свидетельствует о необычайно устойчивой силе承接 на спотовом рынке при шоке от внезапных новостей; долгосрочные配置ционные базовые позиции институциональных средств принципиально не изменились.

Чтобы понять истинные намерения умных денег, рынок производных инструментов, особенно данные опционов, предоставляет наиболее直观ное количественное сечение. Анализируя данные опционов BTC на платформе Deribit с истечением 27 марта 2026 года, мы можем четко описать прогноз пути, который основные институты делают на ближайший месяц.

Текущая подразумеваемая волатильность (IV) опционов BTC с истечением 27 марта достигла относительно высокого уровня в 51,3%. На фоне геополитического кризиса продавцы опционов быстро подняли поверхность волатильности, чтобы хеджировать риски exposure Gamma, которые могут возникнуть из-за экстремальных движений рынка. IV выше 51% indicates that the market is hedging against possible wide fluctuations in the next two to three weeks. Для количественных трейдеров соотношение риска и доходности продажи волатильности в этот момент крайне невыгодно, рынок в целом находится в состоянии ажиотажа «покупки стрэддла» или построения защиты от хвостовых рисков.

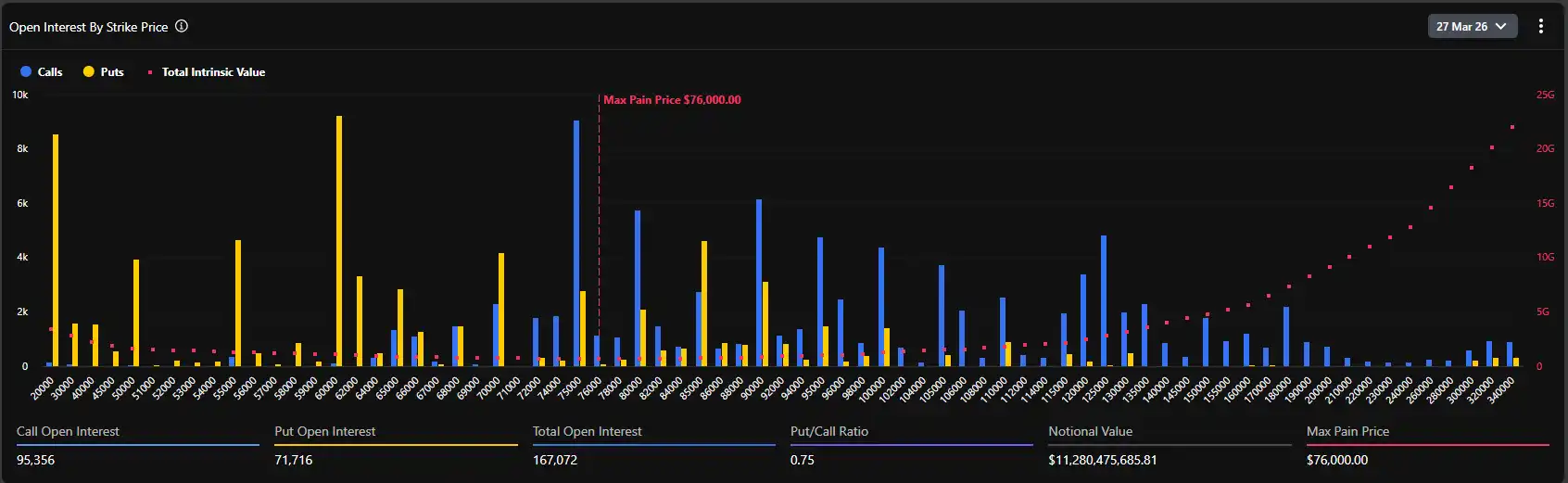

Согласно графику распределения открытого интереса по опционам, текущая максимальная боль для всего рынка составляет целых 76 000 долларов. Это чрезвычайно前瞻性 и спорные данные.

Обычно при приближении к экспирации цена базового актива имеет тенденцию двигаться к точке максимальной боли, чтобы минимизировать общую стоимость для покупателей опционов. Однако текущая спотовая цена (около 67 400 долларов) имеет дисконт почти в 12% по сравнению с максимальной болью (76 000 долларов). Это значительное отклонение раскрывает две ключевые логики:

Во-первых, до кризиса рынок изначально находился в состоянии крайнего оптимизма и бычьих настроений, большие средства делали ставки на прорыв к новым историческим максимумам (диапазон 75 000–80 000 долларов) к концу марта, что напрямую подняло уровень максимальной боли.

Во-вторых, возникновение геополитического кризиса стало сильным внешним шоком, подавившим восходящий импульс спотовой цены. Но судя по общему объему открытого интереса в 167 072 BTC (номинальная стоимость превышает 11,2 миллиарда долларов), быки не устроили массовую распродажу и давку из-за военных новостей.

Данные показывают, что текущее соотношение открытого интереса пут/колл (Put/Call Ratio, на основе OI) составляет 0,75. Это значение ниже 1 indicates that с точки зрения глобального объема открытого интереса, опционы колл (Call) по-прежнему占据绝对主导地位. Особенно на страйках 75 000, 80 000 и даже 100 000 долларов скопились огромные объемы открытых позиций колл (максимальный объем по одному страйку接近 10k BTC).

Однако值得注意的是, суточное соотношение объемов пут/колл (Put/Call Volume Ratio) достигло 1,37. Расхождение между долгосрочным bias в сторону покупки (0,75) и краткосрочным bias в сторону продажи (1,37) идеально отражает текущую рыночную психологию: долгосрочные институты по-прежнему维持原有的 бычьи exposure (не продают спот, не закрывают long Call), но в краткосрочной перспективе после начала войны на Ближнем Востоке большие средства хлынули на покупку внебиржевых опционов пут (OTM Puts) для тактического хеджирования, что привело к резкому росту объема краткосрочных сделок пут.

Согласно детальным данным опционов Deribit, мы наблюдаем, что в диапазоне от 67 000 до 70 000 долларов распределение значений Delta опционов чрезвычайно плотное. Текущая спотовая цена 67 495 долларов находится в зоне «мясорубки» ожесточенной борьбы между быками и медведями.

Если геополитическая ситуация further ухудшится, что приведет к масштабному оттоку макрокапитала, и спот провалится ниже 65 000 долларов (уровень сильной поддержки), маркет-мейкеры, чтобы хеджировать свои exposure от продажи путов, будут вынуждены проводить продажи на спотовом или фьючерсном рынках, что может спровоцировать волну локальной negative обратной связи по ликвидности, testing психологический уровень 60 000 долларов.

И наоборот, если ситуация на Ближнем Востоке после кратковременного ожесточенного конфликта перейдет в阶段僵持ной阶段 при посредничестве крупных держав, и панические настроения рынка достигнут пика и пойдут на спад, отскок на крипторынке будет extremely резким. Поскольку в диапазоне от 70 000 до 76 000 долларов скопилось большое количество опционов колл,一旦 спотовая цена стабилизируется и突破 уровень сопротивления 70 000 долларов, маркет-мейкеры будут вынуждены покупать спот для хеджирования своего negative Gamma exposure. Этот классический эффект «Gamma Squeeze (Гамма-сжатие)» с невиданной скоростью强行 подтолкнет цену BTC к максимальной боли около 76 000 долларов.

Отголоски ближневосточного геополитического震荡 будут продолжаться. Последующие действия США и Ирана определят конечное направление потоков глобального капитала в убежища. В обозримом краткосрочном периоде спот BTC будет совершать剧烈ые колебания в широком диапазоне 62 000~70 000 с反复ными свечными хвостами (пинами). Кредитное плечо на фьючерсном рынке будет в этом процессе反复 вымываться. Количественные стратегии должны в основном «снижать плечо, играть на волатильности», подходя для построения календарных спредов или маркет-мейкинга по сетке на ключевых уровнях поддержки/сопротивления, избегая exposure одностороннего тренда.

С точки зрения структуры открытого интереса по опционам, массовая экспирация 27 марта является гравитационным центром, которого рынок не может избежать. Если только не разразится глобальный, неконтролируемый кризис ликвидности уровня Третьей мировой войны, то по мере边际ного снижения панических настроений, «свойство убежища» и «свойство защиты от инфляции» BTC будут переоценены. Во второй половине марта рынок, вероятно, начнет восстановительный отскок, и у спотовой цены будет сильный стимул приблизиться к 75 000–76 000 долларам (максимальная боль и плотный диапазон страйков колл).

Это событие ознаменовало вступление геополитики в более опасную阶段. Будь то возрождение инфляционных ожиданий из-за войны (резкий рост цен на нефть), или кризис доверия к фиатным валютам, вызванный финансовыми санкциями против specific стран, все это на фундаментальном уровне усиливает стратегическую ценность Bitcoin как «неподконтрольного границам несуверенного твердого актива». Для семейных офисов, макрохедж-фондов и других крупных институтов,单一的 портфель из американских облигаций и акций США 60/40 уже не может应对 текущих хвостовых рисков. Доля BTC в инвестиционном портфеле как «актива без корреляции» после этого кризиса迎来系统性 скачок.

Удар США и Израиля по Ирану стал первым громом, изменившим глобальный финансовый ландшафт в начале 2026 года. Под поверхностью паники данные рынка криптоопционов хладнокровно revealed底牌 институциональных средств: «краткосрочное защитное хеджирование, долгосрочный бычий настрой».

Для профессиональных финансовых работников, отделяя шум эмоций и внимательно следя за тенденциями изменения подразумеваемой волатильности и转移 Gamma exposure маркет-мейкеров, является核心ным кодом для проникновения сквозь туман войны и овладения правом ценообразования на следующий раунд активов. В то время как максимальная боль опционов в 76 000 долларов стоит как маяк, каждая глубокая коррекция, вызванная паникой, накапливает потенциал для будущего прорыва.