Рынок альткоинов продолжает испытывать трудности под давлением устойчивых продаж, при этом слабость сохраняется в течение нескольких месяцев, поскольку общие условия остаются неблагоприятными для рисковых активов. Несмотря на периодические восстановительные ралли, большинство альткоинов не смогли продемонстрировать значительного восстановления, что отражает рынок, по-прежнему управляемый осторожностью, а не уверенностью.

Недавние инсайты, которыми поделился аналитик CryptoQuant Darkfost, подтверждают эту точку зрения. Анализ объемов торговли на Binance и других крупных биржах показывает явный и устойчивый спад интереса инвесторов. Уровни активности значительно снизились по сравнению с предыдущими фазами расширения, что сигнализирует о снижении участия как розничных, так и институциональных трейдеров.

Эта тенденция наблюдается на фоне того, что более широкий медвежий рынок по-прежнему сохраняет свои позиции. Альткоины не только не восстанавливаются, но и показывают худшие результаты, чем Биткоин, который продолжает поглощать большую часть доступной ликвидности. В условиях избегания риска капитал обычно консолидируется в более сильные активы, оставляя альткоины с высокой бета-коэффициентом более уязвимыми для продолжительного спада.

В то же время макроэкономические условия продолжают оказывать давление на настроения. Постоянные геополитические напряженности и глобальная экономическая неопределенность ограничивают аппетит к риску, препятствуя агрессивным позициям в спекулятивных активах. В этом контексте рынок альткоинов отражает структурное сжатие, при котором снижающиеся объемы и устойчивое давление продаж указывают на затяжную фазу слабости, а не на неизбежное восстановление.

Объемы альткоинов рухнули на фоне сокращения участия на рынке

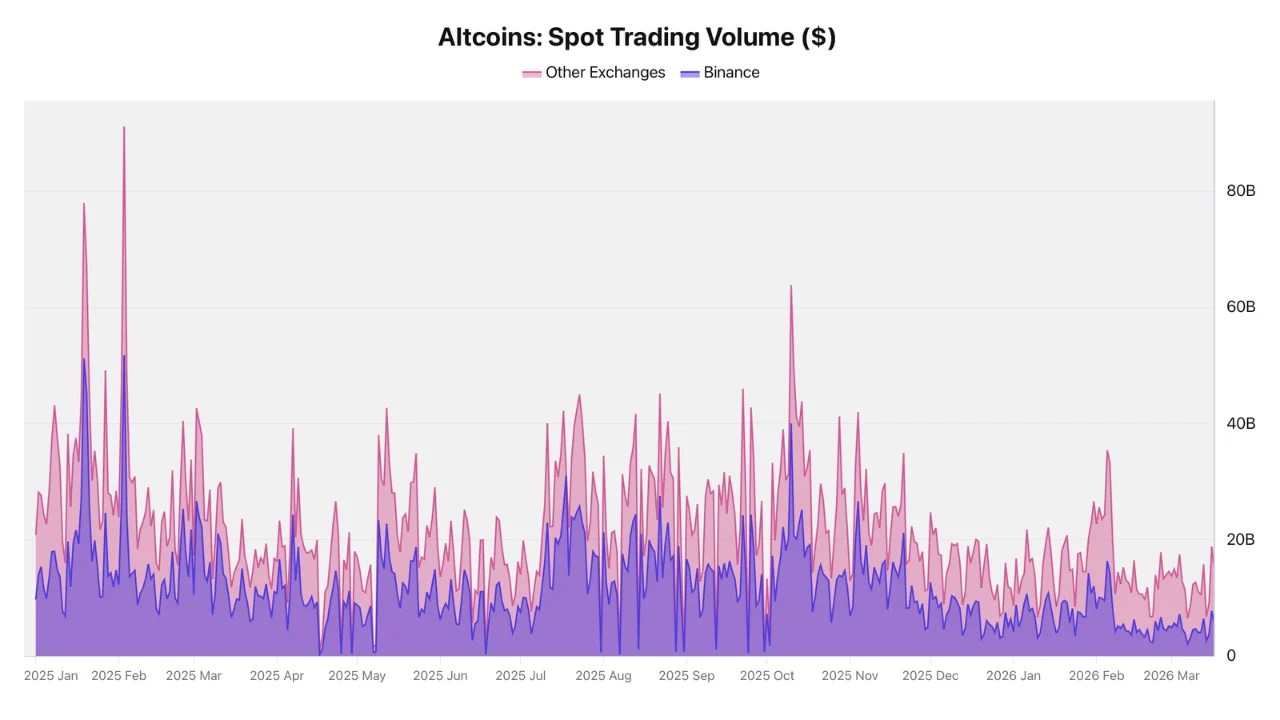

Darkfost дополнительно контекстуализирует текущую слабость, указывая на резкое снижение объемов торговли альткоинами на крупных биржах. На Binance объемы упали до примерно до $7,7 миллиарда, в то время как другие ведущие платформы в совокупности составляют около $18,8 миллиарда. Эти цифры свидетельствуют о значительном сокращении активности, что подтверждает мнение о том, что участие инвесторов существенно снизилось.

Контраст с предыдущими рыночными фазами разителен. В более активные периоды, такие как октябрь и февраль 2025 года, Binance фиксировала объем торговли альткоинами в размере от $40 до $50 миллиардов, в то время как другие биржи достигали уровней от $63 до $91 миллиарда. Таким образом, текущая среда отражает существенную потерю ликвидности и вовлеченности.

В относительном выражении Binance теперь представляет примерно 40% от общего объема торговли альткоинами, что подчеркивает ее доминирование в качестве основной площадки для активности. Эта концентрация предполагает, что ликвидность не только сокращается, но и становится более централизованной.

Важно отметить, что предыдущие всплески объемов совпадали с локальными рыночными пиками, часто вызванными FOMO (страхом упустить выгоду), когда поздние участники обеспечивали ликвидность для выхода более стратегическим игрокам. В отличие от этого, сегодняшние низкие объемы указывают на отсутствие спекулятивного спроса. Однако исторически такие условия часто предшествовали возможностям, поскольку наиболее привлекательные сетапы, как правило, появляются, когда интерес минимален, а позиционирование остается слабым.