Автор оригинала: Maher, Foresight News

Примерно в 4:00 утра 2 июня нативный токен edgeX, EDGE, испытал резкие аномальные колебания. Цена за короткое время рухнула более чем на 77% с отметки около 1,14 доллара США, достигнув минимума около 0,32 доллара, в настоящее время восстановившись до уровня около 0,64 доллара, с рыночной капитализацией примерно в 2,5 миллиарда долларов.

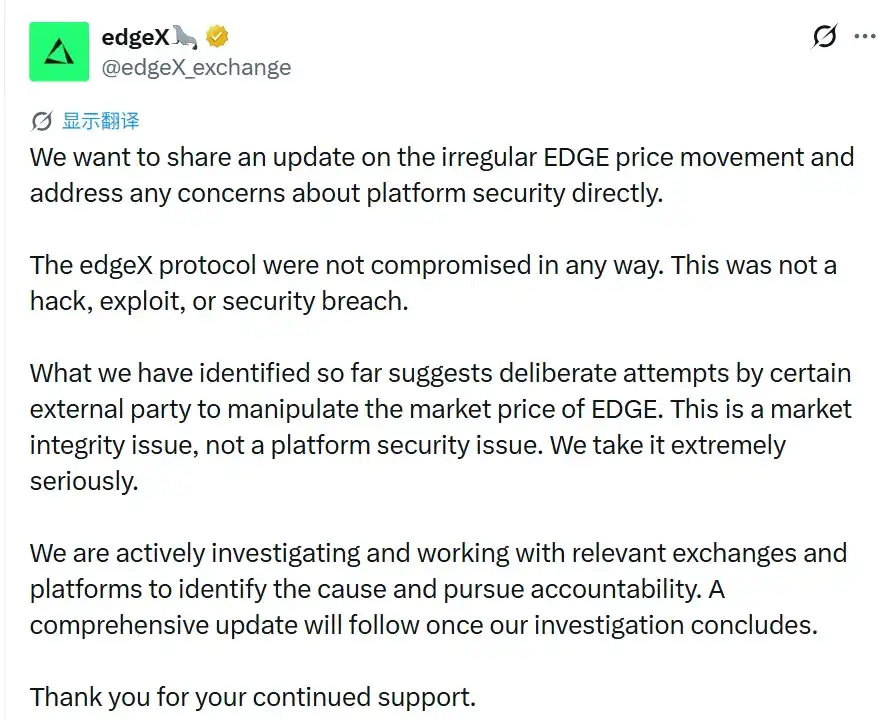

Команда edgeX оперативно отреагировала, четко исключив хакерские атаки или уязвимости безопасности платформы, и указала на «умышленные рыночные манипуляции со стороны конкретных внешних субъектов».

edgeX заявила, что ее протокол не был взломан, хакерских атак или уязвимостей безопасности нет. Данные ценовые аномалии, предположительно, вызваны умышленными рыночными манипуляциями со стороны конкретных внешних субъектов, что является рыночной проблемой, а не проблемой безопасности платформы. В настоящее время команда активно расследует ситуацию и сотрудничает с соответствующими биржами и платформами для выявления ответственных сторон. Полные результаты расследования будут опубликованы по его завершении.

edgeX подчеркнула, что ключевые контракты, такие как SpotVault, работают нормально, подозрительной активности не обнаружено, что дополнительно фокусирует внимание на внешнем рыночном поведении, а не на самом протоколе.

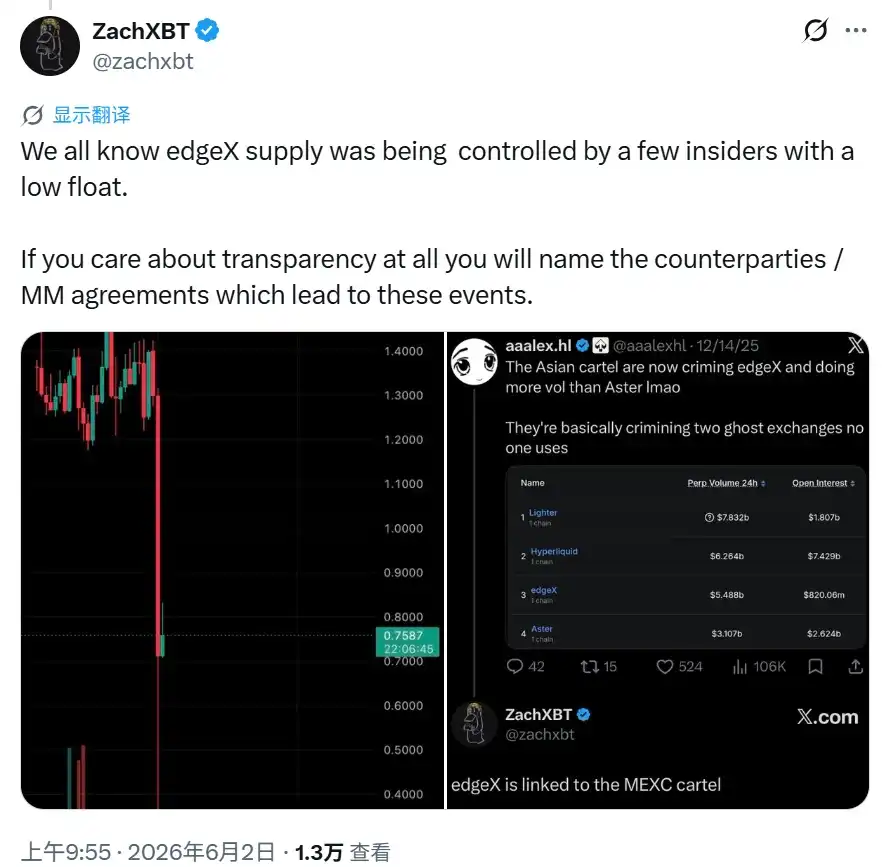

Крипто-детектив ZachXBT высказался после инцидента, отметив, что предложение edgeX долгое время контролируется небольшим кругом инсайдеров, а объем в обращении низок, и потребовал от команды проекта раскрытия информации о маркет-мейкерах и контрагентах для повышения прозрачности.

После развития событий многие пользователи связали эти колебания с прошлыми действиями проекта, выразив разочарование в честности команды. Один из участников сообщества прямо заявил: «Обвал EDGE даже не обсуждают, у команды этого проекта нет честности, они идут на попятную, действительно нет особого желания ловить падение».

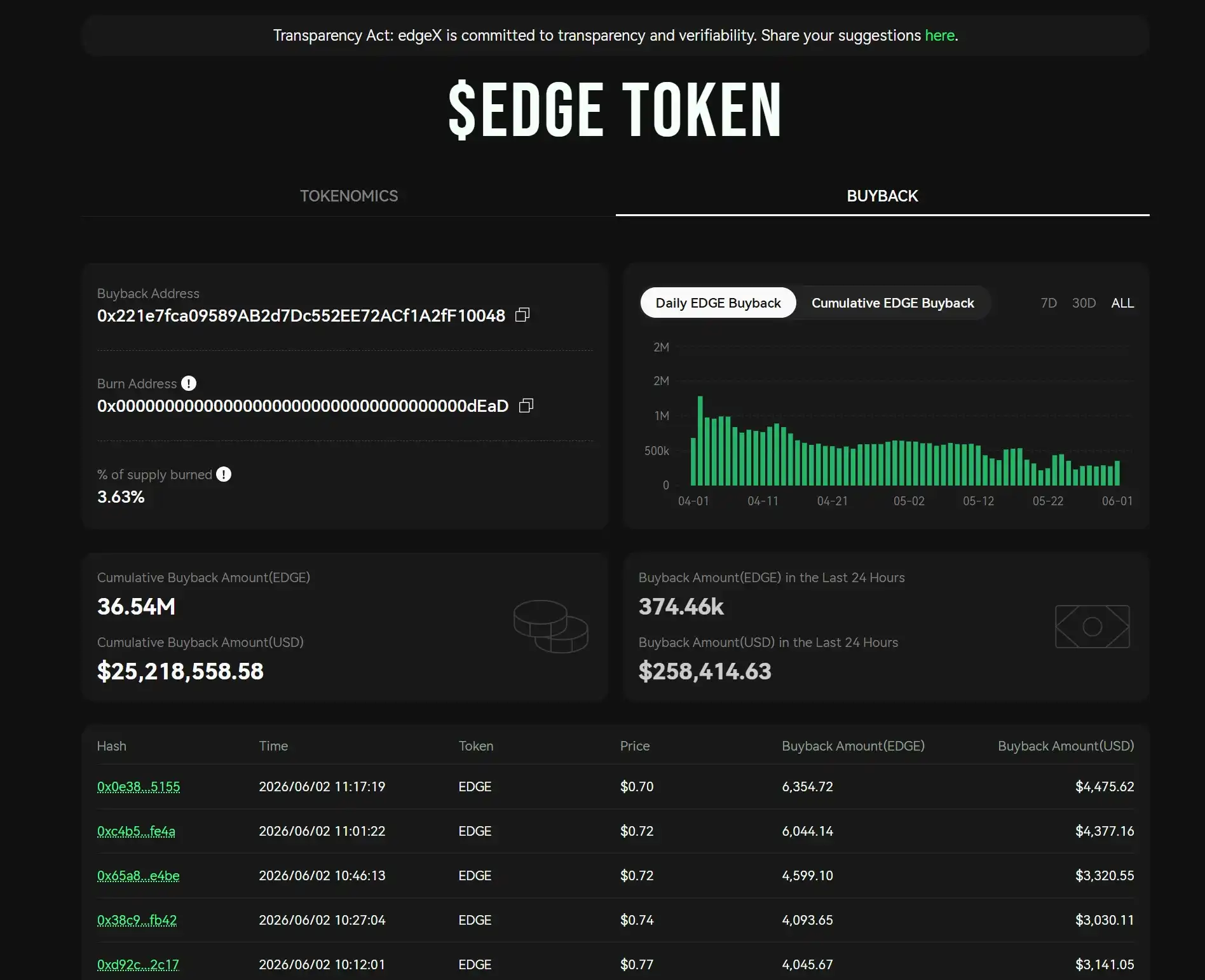

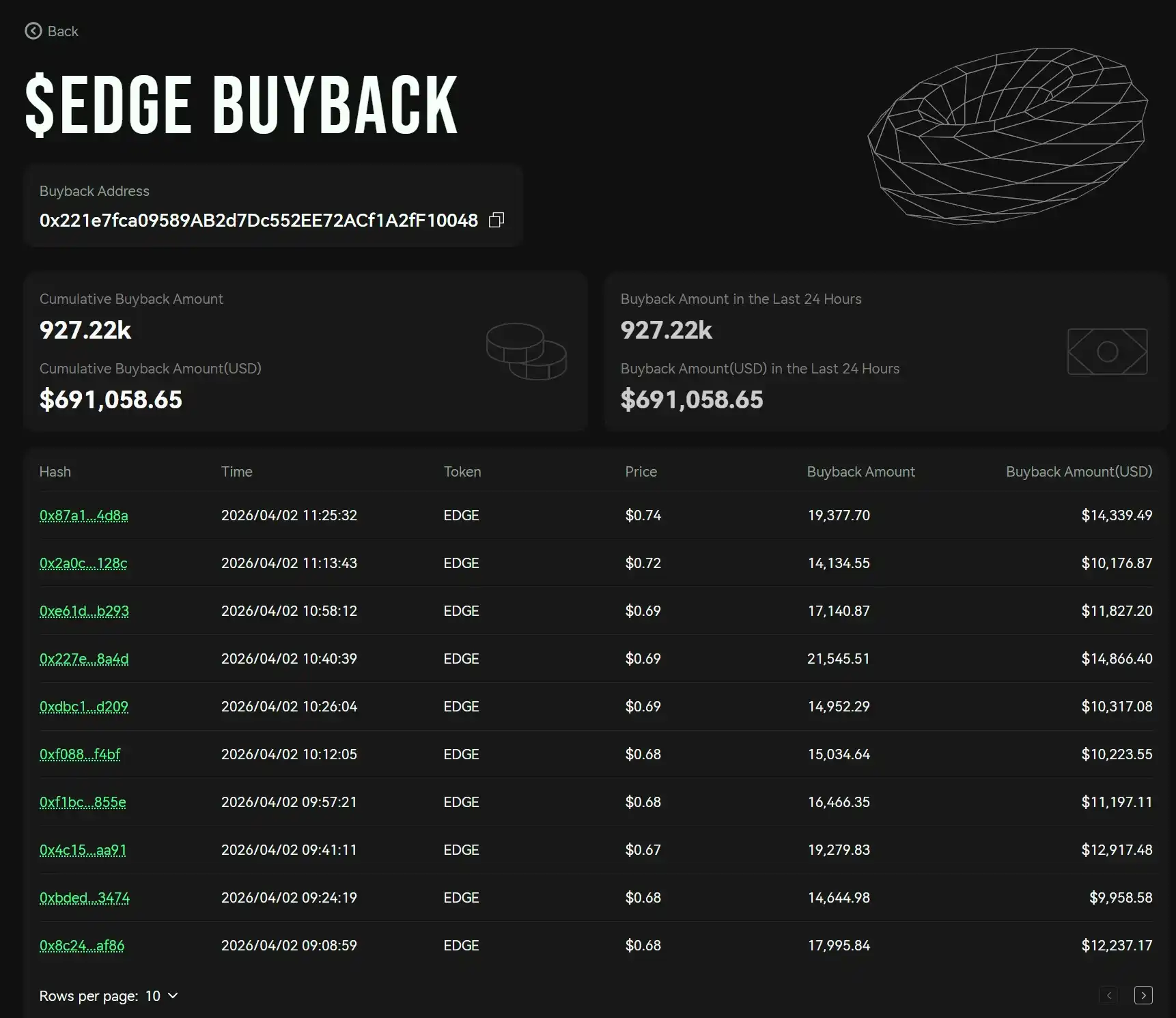

После TGE токена edgeX его цена выросла с 0,7 доллара до 1,5 доллара, впоследствии оставаясь в районе 1,4 доллара. Кроме того, официальная команда специально запустила веб-сайт токена, чтобы доказать прозрачность. В конце мая этого года протокол запустил V2 и скорректировал токеномику, направив всю прибыль на выкуп EDGE. Согласно данным на официальном сайте, на данный момент выкуплено около 36,54 миллиона токенов на общую сумму примерно 25 миллионов долларов.

Кроме того, согласно имеющейся информации, протокол получил инвестиции от Circle Ventures и Amber Group, сумма которых не раскрывается.

Прошлые споры вокруг эирдропа заложили основу для последующего обвала

Этот инцидент трудно рассматривать отдельно от предыдущих споров вокруг эирдропа edgeX. В апреле 2026 года автор подробно изложил весь процесс TGE, вызвавший недовольство сообщества, в статье «edgeX Эирдроп провалился: тщательно спланированный обман?». Проект обещал сообществу 25% доли токенов, но фактически обычным трейдерам было распределено всего около 4%, в то время как около 14% (по тогдашней оценке на сумму около 94,6 миллиона долларов) поступило на кошельки партнеров. График распределения токенов от Arkham показал, что как минимум 80 связанных адресов были созданы в 2025 году, с одинаковым поведением: сначала небольшие тестовые операции, затем крупные депозиты, а после TGE — централизованный вывод, связанный с переводом токенов на сумму около 90 миллионов долларов, часть средств ушла на биржи.

Более важным спорным моментом стала непрозрачность механизма конвертации очков. Пользователи сообщали о значительных различиях в коэффициенте конвертации при одинаковом объеме торгов. Кроме того, разница между ожидаемой стоимостью очков (рыночные ожидания перед TGE составляли 30-40 долларов за очко или выше по FDV) и фактически полученной превысила 80%. Ранние контрибьюторы и держатели NFT также столкнулись с примерами «самого низкого распределения в сети». Участники сообщества обрушились с критикой на официальный аккаунт в Твиттере, команда временно отключила комментарии.

После этого edgeX объявила о блокировке спорной 14% доли на один год и запуске программы выкупа, но отклонила требование сообщества о сжигании токенов в сети Ethereum.

Эти нерешенные проблемы напрямую заложили основу для текущих колебаний: концентрация фишек на небольшом количестве адресов или связанных сторон облегчает внешним субъектам влияние на цену через крупные операции. Низкий объем в обращении — не случайность, а неизбежный результат раннего распределения и условий блокировки. Когда на рынке возникает аномальное давление продаж, отсутствие достаточной глубины для амортизации легко приводит к цепной реакции.

Структурные риски и проверка прозрачности

edgeX ранее занимала свою нишу в отрасли благодаря скорости торговли, низкому проскальзыванию и инновациям в области бессрочных контрактов. После TGE проекта наблюдался временный рост, а объем торгов и доходы от комиссий также многократно входили в число лидеров DeFi. Согласно последним данным DefiLlama, общий доход протокола от комиссий за последние 30 дней составил 10,7 миллиона долларов, а объем бессрочных DEX за последние 30 дней достиг 42,765 миллиарда долларов.

Но от споров по распределению эирдропа до нынешних ценовых аномалий эта модель «низкий оборот + высокий контроль + непрозрачный маркет-мейкинг» стала «цепной схемой обмана», которую новые проекты успешно применяют в последние два года. На словах — сообщество превыше всего, но кошельки честно сбрасывают фишки связанным сторонам, это всего лишь игра в одни ворота под прикрытием DeFi.

Обвинения во внешних манипуляциях трудно немедленно подтвердить, но аномальные переводы на блокчейне, доступные для отслеживания, уже достаточны для того, чтобы вызвать настороженность в сообществе.

Ирония в том, что в самый разгар обвала цены токена EDGE, прогнозы его цены уже незаметно появились на Polymarket.

Команда проекта занята самооправданием, попавшие в ловушку мелкие инвесторы злятся и требуют справедливости. А на Polymarket некоторые игроки уже начинают делать ставки на то, сколько же он сможет вырасти или упасть в этом году.